OCT 17//GOLD CLOSED UP $14.55 TO $1658.25//SILVER WAS UP 53 CENTS TO $18.73//PLATINUM WAS UP $17.55 TO $919.25//PALLADIUM WAS DOWN 35 CENTS TO $2006.45//BIDEN’S BAN ON CHIP EXPORTS PLAYING HAVOC TO CHINA’S ECONOMY//AS PER UK, BAILEY HAS STOPPED FUNDING BRITISH GILTS AS YIELDS RISE TESTING HIS FORTITUDE//KIEV POUNDED BY DRONES//BRANDON SMITH, A MUST READ DISCUSSES WHERE WE ARE AT WITH RESPECT TO UKRAINE VS RUSSIA//COVID UPDATES/DR PAUL ALEXANDER//VACCINE IMPACT//SWAMP STORIES FOR YOU TONIGHT//

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD $2262.60 CDN DOLLARS PER OZ DOWN $15.55 CDN DOLLARS

BRITISH GOLD IN POUNDS: 1452.39 POUNDS PER OZ DOWN 16.38 BRITISH POUNDS PER OZ/

EURO GOLD: 1676.38 EUROS PER OZ// DOWN 14.40 EUROS PER OZ///

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

NIL

JPMORGAN STOPPED 0/0

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 0 NOTICES FOR NIL OZ or NIL TONNES

total notices so far: 22,205 contracts for 2,220,500 oz (69.066 tonnes)

SILVER NOTICES: 9 NOTICE(S) FILED FOR 4,500 OZ/

total number of notices filed so far this month 427 : for 2,135,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $14.55

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////A WITHDRAWAL OF 3.28 TONNES INTO THE GLD//

INVENTORY RESTS AT 941.13 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 53 CENTS

AT THE SLV// :/BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A HUGE DEPOSIT OF 1.151 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 486.071 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STAGGERING SIZED 5168 CONTRACTS TO 136,325 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE GIGANTIC GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.77 LOSS IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS/HFT WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.77)., BUT UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS. HUGE NUMBERS OF SPECS CONTINUE TO ADD TO THEIR SHORTFALLS FROM WHICH OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS.

WE MUST HAVE HAD: I) MINIMAL SPECULATOR SHORT COVERINGS ////CONTINUED BANKER OI COMEX ADDITIONS /// CONSIDERABLE NEWBIE SPEC SHORT ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING A 290,000 OZ QUEUE JUMP / // V) GIGANTIC SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: — 31

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 13 days, total 53,247 contracts: 26.623 million oz OR 2.046MILLION OZ PER DAY. (409 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 26.623 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 26.623 MILLION OZ INITIAL

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5169 DESPITE OUR HUGE $0.77 LOSS IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 945 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /STRONG BANKER ADDITIONS // STRONG SHORT ADDITIONS//CONSIDERABLE NEWBIE SPEC LONG ADDITIONS// /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S 290,000 QUEUE JUMP .. WE HAD AN ATMOSPHERIC SIZED GAIN OF 6113 OI CONTRACTS ON THE TWO EXCHANGES FOR 30.720 MILLION OZ..

WE HAD 9 NOTICE(S) FILED TODAY FOR 45,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 1371 CONTRACTS TO 437,368 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED — -19 CONTRACTS.

.

THE SMALL SIZED INCREASE IN COMEX OI CAME DESPITE OUR LOSS IN PRICE OF $26.50//COMEX GOLD TRADING/FRIDAY // MINIMAL SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE. JUMP OF 3600 OZ//NEW STANDING 70.905 TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $26.50 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 4867 OI CONTRACTS 15.138 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3496 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 437,368

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4867 CONTRACTS WITH 1371 CONTRACTS INCREASED AT THE COMEX AND 3496 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4867 CONTRACTS OR 15.138 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3496) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (1371): TOTAL GAIN IN THE TWO EXCHANGES 4867 CONTRACTS. WE NO DOUBT HAD 1) ZERO SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS/// STRONG NEWBIE SPEC SHORT ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 3600 OZ QUEUE. JUMP ///NEW STANDING 70.905 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) SMALL SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

30,357 CONTRACTS OR 3,035,700 OZ OR 94.423 TONNES 13 TRADING DAY(S) AND THUS AVERAGING: 2335 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAY(S) IN TONNES: 94.423 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 94.423/3550 x 100% TONNES 2.64% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 94.423 TONNES INITIAL ( MUCH SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GIGANTIC SIZED 5168 CONTRACT OI TO 136,326 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 945 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 945 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 945 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 5168 CONTRACTS AND ADD TO THE 945 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF 6113 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 30.565

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED UP 12.96 PTS OR 0.42% //Hang Seng CLOSED UP 25.21 OR 0.15% /The Nikkei closed DOWN 314.97PTS OR 1.16% //Australia’s all ordinaires CLOSED DOWN 1.36% /Chinese yuan (ONSHORE) closed DOWN TO 7.2010 //OFFSHORE CHINESE YUAN UP 7.2092// /Oil DOWN TO 85.61 dollars per barrel for WTI and BRENT AT 90.89 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 1371 CONTRACTS TO 437,368 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS SMALL COMEX INCREASE OCCURRED DESPITE OUR HUGE FALL IN PRICE OF $26.50 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (3496 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3496EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :3496 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3496 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 4854 CONTRACTS IN THAT 3496LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 1388 CONTRACTS..AND THIS GOOD GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $26.50//WE HAD SPEC SHORTS ADDING TO THEIR POSITIONS WITH BANKERS TAKING THE OTHER SIDE AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD SOME ADDITIONAL NEWBIE SPECS GOING LONG DUE TO THE ATTRACTIVE PRICE

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (70.905),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 70.905 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $26.50) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS (THEY ADDED TO THEIR POSITIONS) AS WE HAD A GOOD SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 4854 CONTRACTS // WE HAVE REGISTERED A GOOD GAIN OF 15.097 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (70.905 TONNES)…THIS WAS ACCOMPLISHED WITH A FALL IN PRICE OF $26.50

WE HAD -19 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 4867 CONTRACTS OR 486700 OZ OR 15.138 TONNES

Total monthly oz gold served (contracts) so far this month

22,205 notices 2,220,500 69.066 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into Brinks: 1101.154 oz

total deposits 1101.54 oz

customer withdrawals:2

i) Out of JPMorgan: 17,361.540 oz (540 kilobars)

ii) Out of Manfra: 1101.154 oz

total: 18,462.694 oz

total in tonnes: 0.574 tonnes

Adjustments: 4// all dealer to customer

i)HSBC 31,568.761 oz

ii) JPMorgan 19,772.862 oz

iii) Malca 3,568.761 oz

iv) Brinks 54,383.756 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 591 contracts having LOST 480 contracts . We had 516 contracts

filed on FRIDAY, so we GAINED A STRONG 36 contracts or an additional 3600 oz will stand in this active delivery month of Oct. From this point

we should gain in total gold standing through to the end of Oct.( This is queue jumping and in reality it is the exercising of London based EFP;s for gold at the comex)

November LOST 19 contracts to stand at 3122

December GAINED 843 contracts up to 361,986

We had0 notice(s) filed today for NIL oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (22,205) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 591 CONTRACTS) minus the number of notices served upon today 0 x 100 oz per contract equals 2,279,600 OZ OR 70.905 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (22,205) x 100 oz+ (591) OI for the front month minus the number of notices served upon today (0} x 100 oz} which equals 2,279,600, oz standing OR 70.905 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 70.905 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 427 x 5,000 oz = 2,135,000 oz

to which we add the difference between the open interest for the front month of OCT(163) and the number of notices served upon today 9 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 427 (notices served so far) x 5000 oz + OI for front month of OCT (163) – number of notices served upon today (9) x 5000 oz of silver standing for the OCT contract month equates 2,905,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

GLD INVENTORY: 941.13 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLIONOZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

As Peter Schiff put it in a recent podcast, the inflation insanity continues.

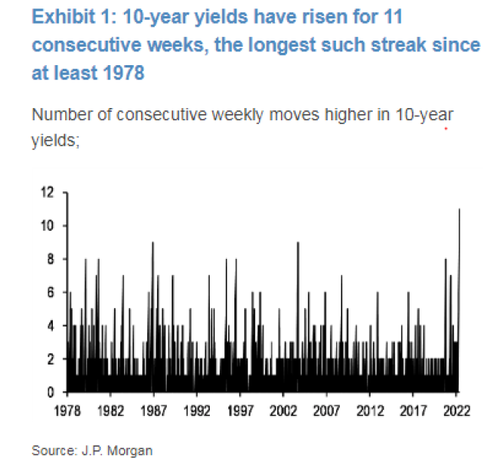

We got the September Consumer Price Index (CPI) data and it once again came in hotter than expected. Month-on-month, CPI was up 0.4%. That was double the 0.2% expectation. On an annual basis, the CPI was 8.2%.

By the way, the month-on-month CPI in September 2021 was also 0.4%. So, prices continue to increase at the same clip they were a year ago. In other words, inflation is still running rampant, despite all the Fed has done to try to stop it.

Core CPI excluding more volatile food and energy prices was up 0.6% from last month and charted a 6.6% year-on-year increase. That was the highest jump in annual core inflation since August 1982.

Peter said it makes no sense that people keep expecting better inflation numbers and continue to be surprised when they come out worse than expected.

The classic definition of insanity – doing the same thing over and over again, yet expecting a different result. In fact, the insanity goes all the way back to the days when everybody just said inflation was transitory. I remember — we’d keep getting a hotter-than-expected inflation number and everybody said, ‘Don’t worry about it. It’s going to go away. It’s transitory,’ and so each time we got a new report, everybody thought that the number would be lower, and everybody would be surprised when it wasn’t lower, or it went higher. In fact, when they kind of went from transitory inflation to peak inflation, every time we got a number that made a new high, they kept repeating the same phrase. ‘OK, now inflation is peaked. Oh, no, now inflation has peaked.’ And now, they just keep expecting inflation to go lower because the Fed has raised interest rates.”

In fact, the Fed has hiked rates significantly since last March, with four 75 basis point increases. The rate now stands at 3.25%. And we’ve seen the impact of these hikes on the economy. It is demonstrably slowing.

So, everybody expects lower inflation, yet every month, investors are surprised by higher-than-expected inflation. This high inflation is not going to go away. It’s not going to go away anytime soon. In fact, it’s not going to go away anytime in this decade.”

A lot of people think the current inflation problem is solely the result of the monetary policy mistakes made after COVID. But as Peter talked about in a previous podcast, this inflation problem was decades in the making.

We are paying for monetary mistakes going back into the early 1990s, or even late 1980s. It’s not simply the mistakes that were made after 2020. It was all the mistakes that were made prior to 2020.”

And despite all of the Fed hiking, we still have negative real interest rates. That means we still have a stimulative monetary policy.

Even when the Fed hikes rates to 4% in November, you’re still half the inflation rate. You’re still discouraging people from saving and encouraging people to take on more debt. You are stoking inflation’s fires. You’re not putting it out.”

Peter noted that Pepsi recently announced price increases of 17%. He said that’s more indicative of inflation than the CPI.

Pepsi’s prices are real prices. There’s no hedonics. There’s no substitution. They are what they are. And they’ve raised prices by 17%. That probably reflects what’s going on with inflation. Because, remember, Pepsi doesn’t want to raise prices. It’s trying not to. In fact, remember the early days in the inflation. All of these companies were eating these price hikes. They thought it was transitory. So, they were absorbing the higher costs. They weren’t raising prices.”

At the time, Peter said these companies would eventually realize inflation wasn’t transitory, and they would throw in the towel and raise prices to recover their higher costs.

So, a 17% inflation rate, to me, is more believable than the government’s 8.5%. And what Pepsi is selling is what America is buying. This is what’s going on with prices.”

Peter pointed out that even after Paul Volker hiked rates to 20% to get inflation under control, the CPI was rarely under 2% during the 1980s and 1990s. What makes anybody think the Fed can quickly get CPI back down to that level today?

The problem is we have printed so much money since then, the debts are so much larger, that bringing an inflation rate down to the level we had in the 1980s, and 1990s, or 2000s, is nearly impossible.”

Peter said, “We’re not going down to 2%.”

The aberration was the inflation of 2% or less that we got following the 2008 financial crisis. … Now, what we are going to have is a lot of high inflation to make up for all those years of low inflation. It’s a reversion to the mean. Except we’re really not going to revert to the mean. We’re going to revert to something much higher than the mean because of massive and unprecedented money printing that has gone on – not just since COVID, but before COVID.”

In this podcast, Peter also talked about the market reaction to the CPI data, how the increase in Social Security benefits will stoke the inflation fire, the impact of rate hikes on the national debt, bitcoin, and how gold is holding up better than stocks.

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

LAWRIE WILLIAMS: Blip in China September gold demand y-o- y?

Anecdotal accounts have Chinese gold demand riding high already this year with talk of price premiums and bullion shortages developing, but this does not seem to be being confirmed by the latest data from the Shanghai Gold Exchange (SGE). This suggests that gold demand actually slipped a little in the September month and that the cumulative total for the first nine months of the current year may be slightly below that of the corresponding nine month period of 2021. Not by enough perhaps to worry about yet, but sufficient to generate further close attention to figures that may arise month by month for the remainder of the year. That would be sufficient to make our earlier prediction of an overall Chinese annual gold consumption figure for the current year of around 1,800 tonnes perhaps a little on the optimistic side. The occasional draconian lockdowns in key cities to prevent any spread of the Covid virus may be having and undue effect on overall earnings and gold demand.

The SGE withdrawal figures on a month by month basis year to date are set out in the table below. Assuming similar withdrawal levels to last year for the final quarter of the year, Chinese gold consumption for 2022 looks perhaps more likely to end up around 1,700 tonnes, which would still make the nation comfortably the world’s largest gold consumer.

Of course the big unknown here remains Russia – the world’s second or third largest gold producer depending on whose figures one takes. U.S. and European imposed economic sanctions have cut off the Russian-produced gold from its normal markets and it will have been searching for ‘friendly’ outlets for its gold production, in part at least to help it finance its ongoing military incursions into Ukraine. China is an obvious outlet for this Russian gold and is certainly receiving some of it, although the figures that have been forthcoming in official announcements so far do not account for very much of it.

Both nations have histories of being extremely secretive about what they may consider to be strategic matters and this could well cover gold flows between these two neighbouring countries which are supposedly allies. Russia mines over 300 tonnes of gold annually and China is believed by many to be surreptitiously building up its gold reserves to match, or exceed those of the U.S., and secret Russian gold imports could well be a means to this end. This is all speculation of course, but could provide an answer that would seem to meet both nations’ assumed needs.

16 Oct 2022

end

END

3.Chris Powell of GATA provides to us very important physical commentaries

Wary of U.S. dollar hegemony, Chinese state researchers float idea of a pan-Asian digital currency

Submitted by admin on Fri, 2022-10-14 09:53Section: Daily Dispatches

By Frank Tang South China Morning Post, Hong Kong Thursday, October 13, 2022

The conditions are right for the establishment of a pan-Asian digital currency that could enhance regional monetary cooperation and loosen reliance on the U.S. dollar, Chinese state researchers say.

The idea of an Asia-wide digital token comes as Beijing tries to consolidate its economic influence in the region and its position as a global leader in digital currency development.

China is also working studiously to reduce its reliance on the U.S. dollar system amid threats of financial decoupling from Washington.

“More than 20 years of deepened economic integration in East Asia has laid a good foundation for regional currency cooperation. The conditions for setting up the Asian yuan have gradually formed,” said researchers Song Shuang, Liu Dongmin, and Zhou Xuezhi, from the Institute of World Economics and Politics under the Chinese Academy of Social Sciences.

The digital token would be pegged to a basket of 13 currencies, including the yuan, Japanese yen, South Korean won, and those of the 10 member countries in the Association of Southeast Asian Nations, the researchers wrote in an article. Weighting for each could be similar to that of the International Monetary Fund’s special drawing rights, an international reserve asset. …

Jan Nieuwenhuijs: Europe has been preparing a gold standard since the 1970s

Submitted by admin on Fri, 2022-10-14 11:22Section: Daily Dispatches

By Jan Nieuwenhuijs Gainesville Coins, Lutz, Florida Friday, October 14, 2022

There is more evidence of how European central banks are equalizing their monetary gold reserves proportionally to Gross Domestic Product.

Secret agreements make countries sell or buy gold to balance gold reserves within Europe, and relative to large economies abroad.

Evenly distributed gold reserves are a requirement for a stable transition toward a gold standard whereby concurrently the debt overhang can be extinguished. Europe has been preparing for this reset. …

Ted Butler: Stand up against market manipulation and make a difference

Submitted by admin on Fri, 2022-10-14 23:44Section: Daily Dispatches

By Ted Butler SilverSeek.com Friday, October 14, 2022

If you are tired of witnessing silver (and gold) continuing to be manipulated in price, here’s a no-cost, no-risk, high-potential return action you can take that will only involve a few minutes of your time. Quite literally, there’s absolutely nothing to lose and quite a lot of potential good to be had.

The Commodity Futures Trading Commission is the taxpayer-funded federal commodities regulator whose main mission is to prevent and root out manipulation and protect the public. Four of the five commissioners have been in office for little more than six months and it’s not clear that they are even aware that silver has been manipulated in price on the Comex.

Here is your opportunity to ensure that this is an issue they should be concerned about. Please take the time to copy and paste the letter below and email it to addresses listed. If you would prefer using your own name and not mine, you have my permission to do so. …

If you are tired of witnessing silver (and gold) continuing to be manipulated in price, here’s a no-cost, no-risk, high potential return action you can take that will only involve a few minutes of your time. Quite literally, there’s absolutely nothing to lose and quite a lot of potential good to be had.

The Commodity Futures Trading Commission (CFTC) is the taxpayer-funded federal commodities regulator whose main mission is to prevent and root out manipulation and protect the public. Four of the five commissioners have only been in office for little more than six months and it’s not clear that they are even aware that silver has been manipulated in price on the COMEX. Here is your opportunity to ensure that this is an issue they should be concerned about. Please take the time to copy and paste the enclosed letter and email it to addresses listed. If you would prefer using your own name and not mine, you have my permission to do so.

US citizens might also consider forwarding the same to your local congressman or woman, and senators, asking them to send it on the CFTC, which will guarantee the agency will respond.

Commodity Futures Trading Commission Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581

The evidence has become overwhelming that the price of silver does not reflect developments in the physical world of supply and demand. There has developed a physical shortage in both the retail and wholesale silver market accompanied by declining inventories. Nevertheless, the price has fallen. Increasingly, there has developed among the public a conviction that the culprit for this mispricing is trading by a handful of large traders in silver futures on the Commodities Exchange, Inc. (COMEX), owned and operated by the CME Group, Inc.

The Commission has considered the question of a silver price manipulation in the past. I would call on the Commission to explain why such large and concentrated dealings, particularly on the short side of COMEX silver futures, are not artificially depressing the price. I would also call on the Commission to end what many believe to be an ongoing price manipulation. Thanks for your consideration and attention to this matter.

Sincerely,

Theodore Butler

4. OTHER PHYSICAL SILVER/GOLD

5.OTHER COMMODITIES:

end

COMMODITIES IN GENERAL/

END

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.2019

OFFSHORE YUAN: 7.20920

SHANGHAI CLOSED UP 12.96 PTS OR 0.42%

HANG SENG CLOSED UP 25.21 OR 0.15%

2. Nikkei closed DOWN 314.97 PTS OR 1.16%

3. Europe stocks SO FAR: ALL GREEN

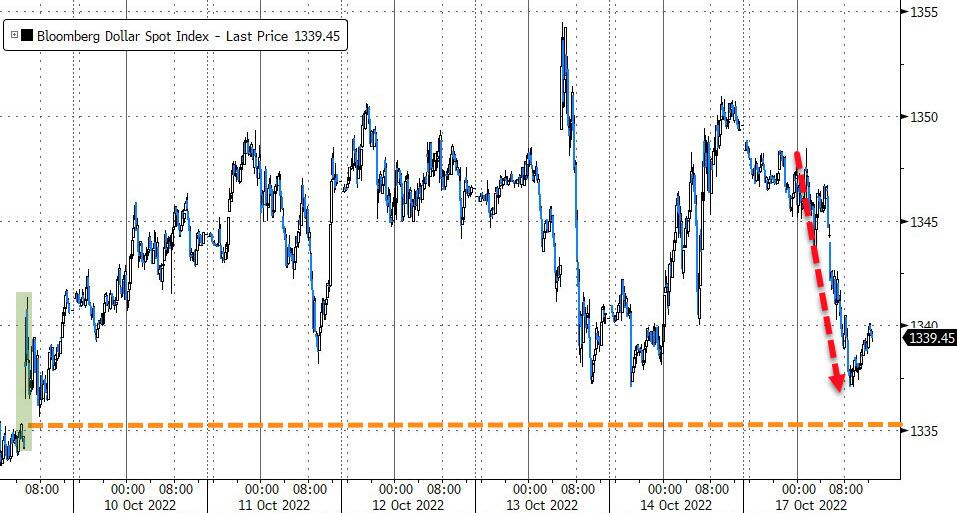

USA dollar INDEX DOWN TO 112.89/Euro RISES TO 0.9737

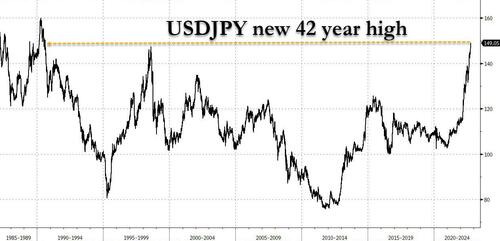

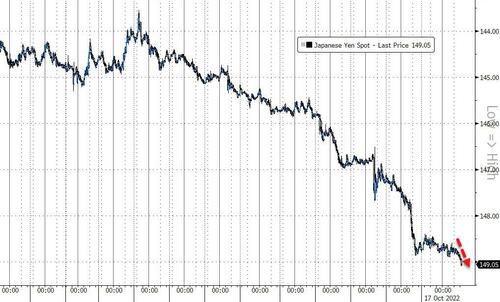

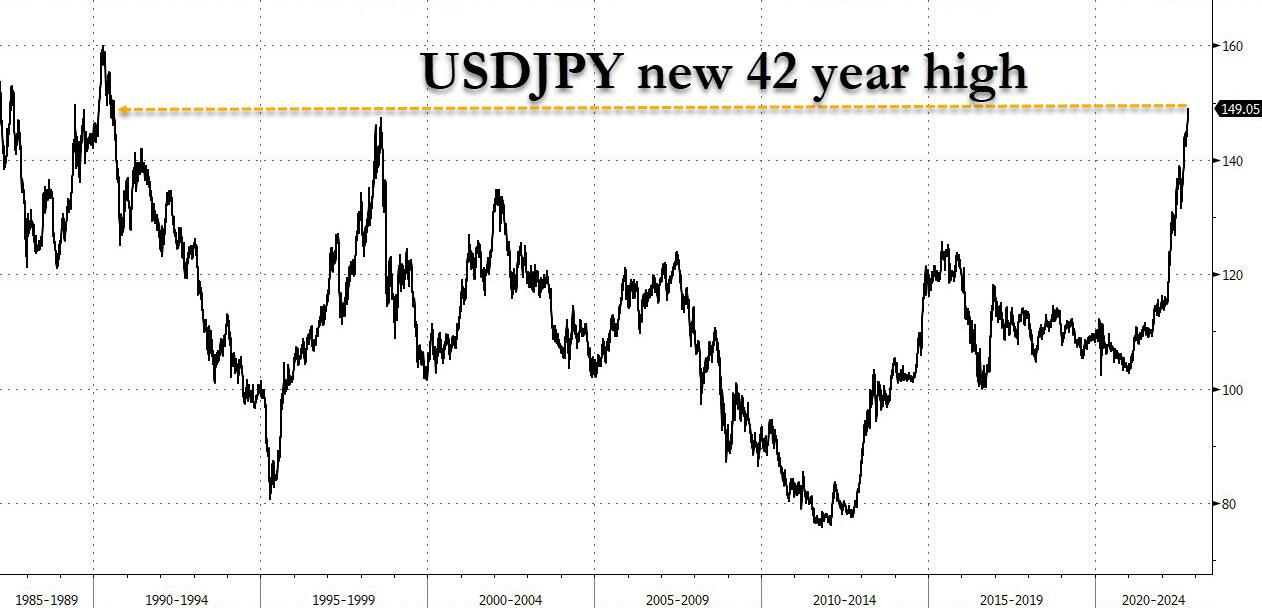

3b Japan 10 YR bond yield: RISES TO. +.249/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 148.88/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.252%***/Italian 10 Yr bond yield RISES to 4.698%*** /SPAIN 10 YR BOND YIELD RISES TO 3.429%…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.921//

3j Gold at $1664.90//silver at: 18.80 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 18/100 roubles/dollar; ROUBLE AT 61.93//

3m oil into the 85 dollar handle for WTI and 90 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 148.88DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 1.0022–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9757well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

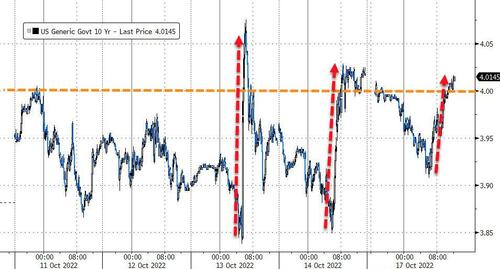

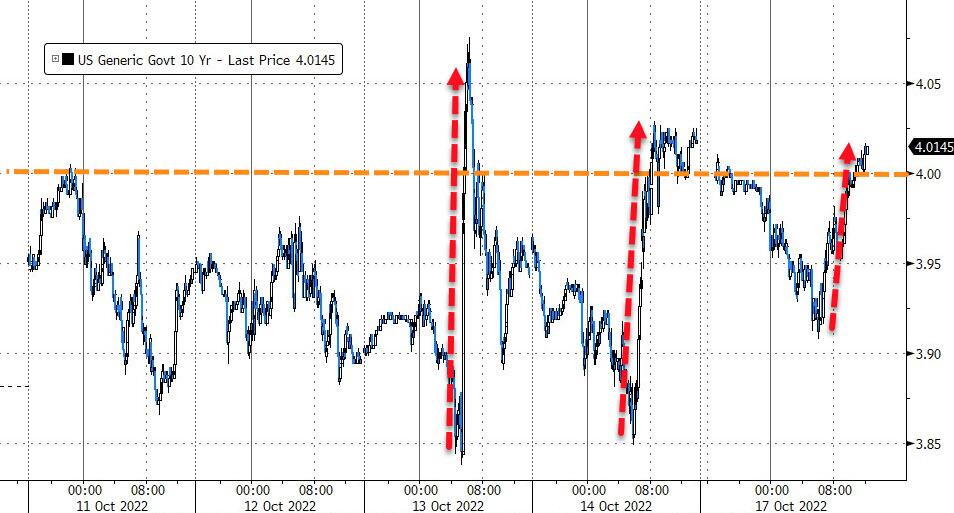

USA 10 YR BOND YIELD: 3.949 DOWN 6 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.944 DOWN 3 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

USA DOLLAR VS TURKISH LIRA: 18,59…GETTTING DANGEROUS

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

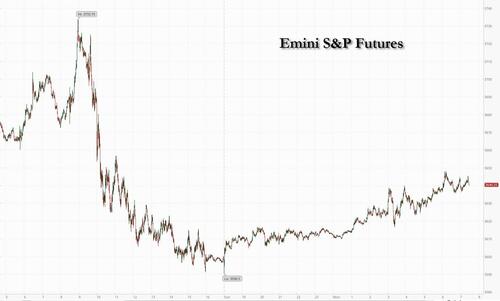

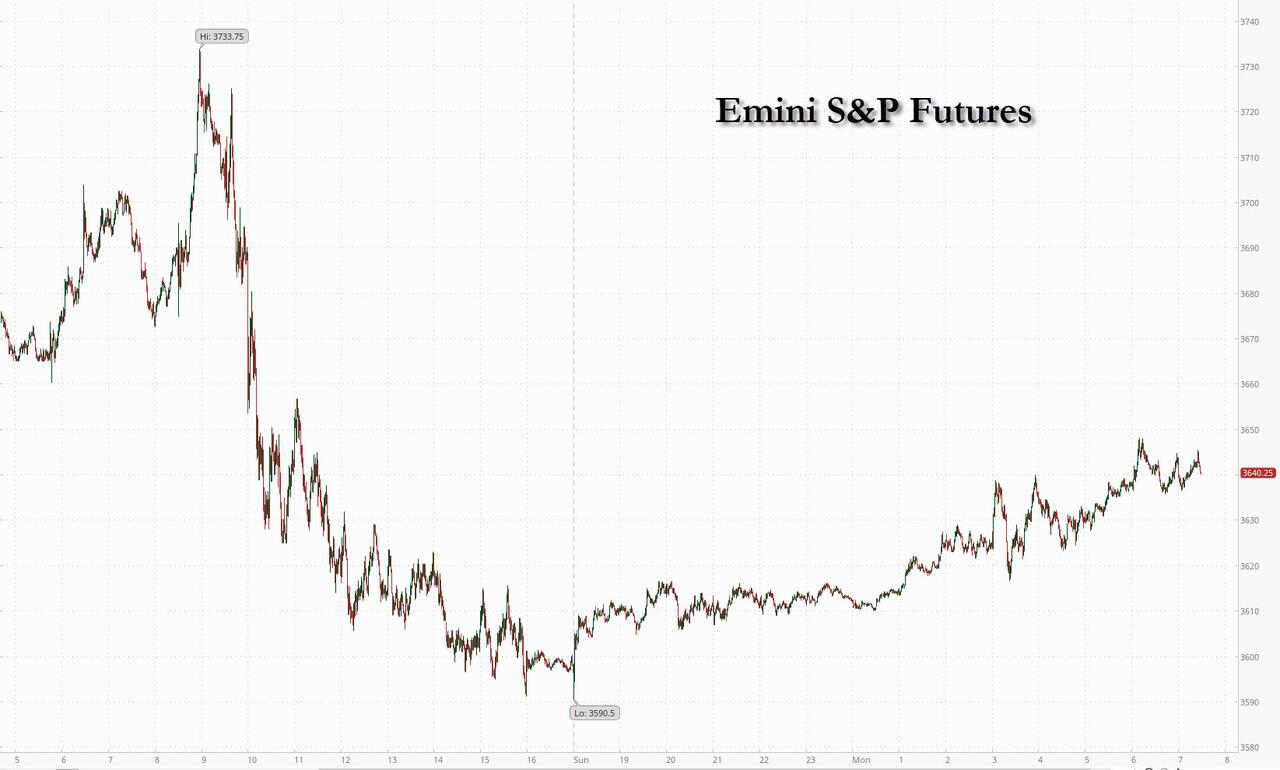

Futures Jump, Squeezed By Reversal In UK Fiscal Plans And Apocalyptic Trader Sentiment

MONDAY, OCT 17, 2022 – 07:49 AM

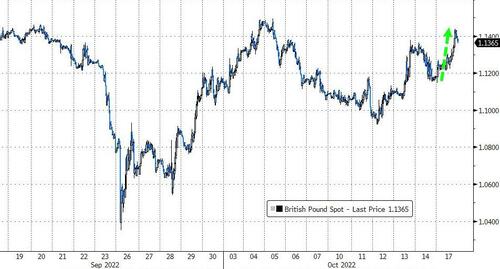

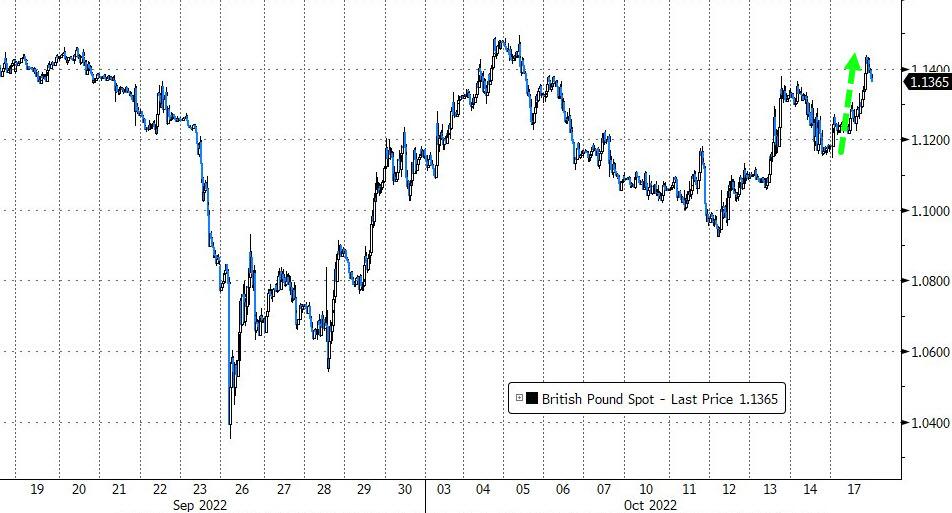

As we discussed and previewed over the weekend in “Behind Friday’s Market Massacre: A Huge Burst Of Hedge Funds Shorting, Setting Up Another Squeeze“, futures are indeed sharply higher to start the week as Treasury yields slumped and the dollar eased as the British peso (also called Britcoin) rallied and UK bonds surged as the new Chancellor Jeremy Hunt scrapped plans to cut taxes and signaled consumers would shoulder more of the increase in energy prices from next April as he set out a package of measures to get a grip on the public finances, effectively reversing pretty much all UK tax cut measures announced just a few weeks ago. Sentiment was also boosted by company results after Bank of America reported beats on the top and bottom line, rising in premarket trading while utilities and auto stocks led gains in Europe. That was indeed enough to spark a modest (for now) squeeze and as of 730am, S&P 500 futures trade higher by 1.3% and Nasdasq 100 futs rose 1.5% bouncing back from a selloff on Friday that left the technology-heavy gauge at its lowest since July 2020; Europe’s Estoxx50 rose 0.7% in early London session, which sees cable higher by 1%. The BBG Dollar index was down 0.2% and the 10Y traded at 3.95%.

And if all those record retail puts purchased in recent days get monetized, expect another epic meltup today.

Among notable premarket movers, Splunk rose after a Wall Street Journal report about activist investor Starboard Value building a stake of just under 5% in the application software company. Opendoor Technologies Inc. slipped after Goldman Sachs downgraded the stock to sell. US-listed Chinese stocks gained as President Xi Jinping reiterated that economic development is the party’s top priority in his speech at the Communist Party Congress, although he signaled little change in the Covid Zero strategy and housing market policies. Alibaba (BABA US) +1.9%, Pinduoduo (PDD US) +2.8%, JD.com (JD US) +3.3%, Nio (NIO US) +2.7%, Li Auto (LI US) +2%. Here are some other notable premarket movers:

Opendoor Technologies (OPEN US) slides 1.8% in premarket trading after Goldman Sachs downgrades stock to sell, saying it sees the ongoing weakness in housing through next year to “depress” the online real estate platform’s earnings power and in turn limit upside in shares.

Keep an eye on Fox Corp. (FOXA US) and News Corp. (NWSA US) shares after the companies said on Friday they were exploring options to recombine, while analysts suggested a deal is unlikely to solve the valuation problem for the pair.

Watch PPG Industries (PPG US) shares as KeyBanc Capital Markets initiated coverage of the stock with an overweight recommendation, saying there’s probably going to be a sharp decline in costs in 1H23 that will help offset cyclical volume pressure.

Keep an eye on household products stocks as Morgan Stanley is starting to warm to the sector with margins seen rebounding in 2023, while toning down its preference for beverage stocks.

The broker upgrades Church & Dwight (CHD US) and Clorox (CLX US) to equal-weight from underweight, while cutting Edgewell Personal Care (EPC US) to underweight from equal-weight.

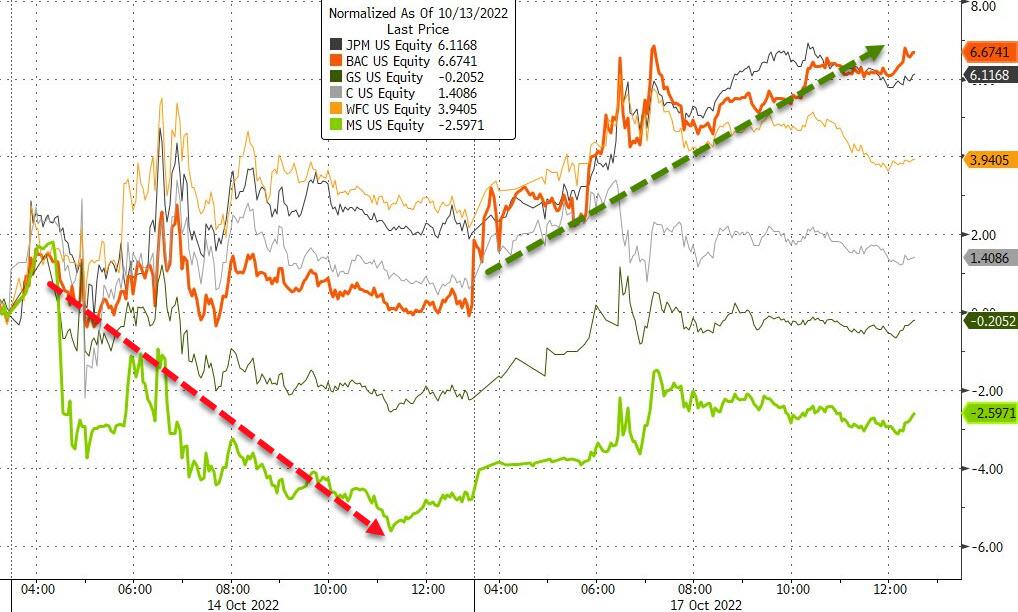

Investors are focused on results due this week — including from Bank of America which just reported stronger than expected revenues and EPS, Goldman Sachs and Tesla — for clues about how company earnings are holding up. They’re also monitoring the possibility of more aggressive rate hikes in the US after Federal Reserve Bank of St. Louis President James Bullard on Friday left open the possibility that the central bank would raise interest rates by 75 basis points at each of its next two meetings.

“I think the likelihood of them doing 75bps and more is definitely higher after the University of Michigan survey last week, reason being is that they’re late to the party of inflation control and the world economy is paying the price,” said Sunaina Sinha Haldea, global head of private capital advisory at Raymond James. “The risk is that they break growth, but what is much more concerning is that they’re risking financial stability in parts of the market, which is a risk that needs to be priced in,” she said on Bloomberg TV.

In major corporate reorganization news, the WSJ reported that Goldman Sachs plans to recombine the bank’s asset management and private wealth businesses into one unit in yet another overhaul.

Morgan Stanley’s in-house permabear, Michael Wilson, echoed precisely what we said on Saturday, namely that technicals may now take the upper hand over fundamentals, with the 200-week moving average acting as a strong support to equities, while inflation expectations peak. They see a tactical rally looking likely until earnings estimates are cut or a full-blown recession arrives.

Meanwhile, the outlook for consumer prices in the US continues to fuel bets that the Federal Reserve may make jumbo rate hikes at its next two meetings, weighing broadly on the outlook for global economic growth and markets. Fed officials in their latest comments suggested they were ready to hike rates higher than previously planned. Kansas City Fed President Esther George said the terminal rate may need to be higher to cool prices. San Francisco Fed’s Mary Daly said she’s “very supportive” of raising to restrictive levels and to between 4.5% and 5% “is the most likely outcome.”

In European stocks, utilities, autos and insurance are the strongest performing sectors. Euro Stoxx 50 rises 0.3%. IBEX outperforms peers, adding 1.1%. Here are the most notable European movers:

ITV shares jump as much as 9.7%, the most since March, after the Financial Times reported that the company is exploring options for its production arm ITV Studios, including a stake sale.

Nel shares rise as much as 10%, the most since late July, after the company won a NOK600m contract to provide alkaline electrolyser equipment to Woodside Energy.

Made.com shares soared as much as 35% after the online furniture seller said it has received several “non-binding indicative proposals,” including possible offers for the company.

Sulzer shares climb as much as 4.4% after the Swiss company announced Suzanne Thoma will replace CEO Frédéric Lalanne, who is stepping down at the end of the month. Thoma’s experience and continuation of the company’s strategic review is viewed as a positive, according to analysts.

Hargreaves Lansdown shares fall as much as 7.9% after its 1Q trading update, with its CEO announcing his intention to retire amid a lawsuit relating to a failed equity fund run by Neil Woodford.

Asos shares drop as much as 13% after the online fast fashion retailer said it was in talks with banks to boost its financial flexibility, following a Sky News report that the firm’s lenders were hiring restructuring advisers, including AlixPartners.

Draegerwerk shares tumble as much as 7.5% after company withdrew FY22 guidance following market close on Friday, based on its preliminary 9-month figures.

Shares in bike helmet maker Mips plunge as much as 27%, the most in three years, as Handelsbanken said lower-than-expected 3Q sales from the company show the bike boom of the past years turning “into a bust” while 2023 risks becoming a “lost year.”

European luxury stocks drop after Chinese President Xi Jinping signaled no change in China’s strict Covid rules at the country’s Communist Party congress in Beijing on Sunday. LVMH shares decline as much as 1.8%.

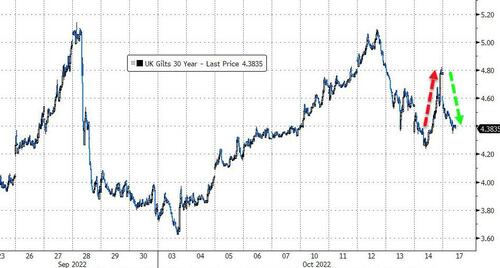

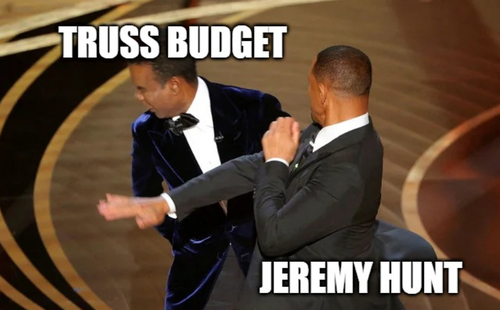

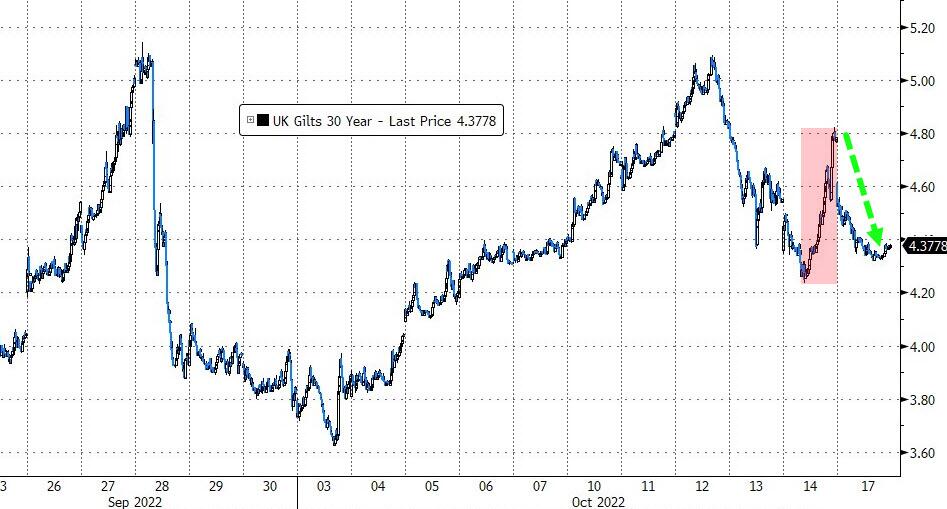

As noted above, the yield on 10-year gilts fell 36 basis points to 3.97% and the pound traded 1.1% higher at $1.1293 after new Chancellor Jeremy Hunt scrapped plans to cut taxes and signaled consumers would shoulder more of the increase in energy prices as he set out a package of measures to get a grip on public finances in a televised statement on Monday. It’s the start of what may be a particularly torrid week for British assets, with the beleaguered Truss battling to rescue her premiership after the Bank of England ended its emergency bond-buying program on Friday and as mutinous backbenchers plot to oust her.

“I think we’re in for a period where UK credibility is continually questioned and UK assets remain incredibly volatile for a significant period of time,” Benjamin Jones, Invesco Director of Macro Research, said on Bloomberg Television. “Watching the gilt market will be absolutely key in understanding if the market does believe Hunt to be more stable and if he will be able to push these policies through.”

Hunt will also speak to the House of Commons at 3:30 p.m. London time and Truss is due to host a reception for the Cabinet at 10 Downing Street on Monday evening. U-turns on the government’s “mini budget” now total £32 billion, however that may not be enough as the official estimate of the black hole in the public finances is believed around £70 billion.

Earlier in the session, Asian equities resumed their decline, led by tech stocks, as investors analyzed Chinese President Xi Jinping’s speech at Party Congress, in which he ruled out changes to strict Covid rules. The MSCI Asia Pacific Index retreated as much as 1.4% before paring the drop, with TSMC and Keyence among the biggest drags after a broader US tech selloff last week. All sectors but real estate were in the red. Taiwan’s benchmark was a notable regional loser, ending 1.2% lower as the local currency weakened following comments by Xi’s about the island. Stock gauges in Japan fell about 1% after the Bank of Japan vowed to continue with monetary easing as the yen approached a key level. Benchmarks in Hong Kong erased losses, while gains in defense and tech stocks helped gauges in mainland China close moderately higher after Xi’s Sunday speech emphasized national security and self-reliance in core technologies. Planned steps by Chinese regulators to stem a slump in equities also buoyed sentiment. Asian stocks have underperformed US and European peers this year as the region struggles with challenges in China in addition to aggressive rate hikes by the Federal Reserve, prompting an exodus of foreign funds from emerging countries.

“The work report made no reference to future policy changes on Covid containment,” Nomura economists including Ting Lu wrote in a note, adding that they expect Chinese markets to suffer regardless due to disappointment about either no real opening or a surge in Covid infection numbers. Concerns of aggressive tightening by the Fed were reinforced after a survey Friday showed US year-ahead inflation expectations rose in early October for the first time in seven months. “More bad news is baked into Asia, which might suggest that the risk reward is a little bit better if we can see overall the Fed starts to stabilize at some point, perhaps early next year,” Timothy Moe, chief Asia equity strategist at Goldman Sachs, said in an interview with Bloomberg TV, citing Asia’s “excessive discounting particularly in valuations.”

Japanese stocks dropped, with electronics makers the biggest drag, following US peers lower after a report showed American year-ahead inflation expectations rose for the first time in seven months. The Topix fell 1% to close at 1,879.56, while the Nikkei declined 1.2% to 26,775.79. Keyence Corp. contributed the most to the Topix Index decline, decreasing 2.9%. Out of 2,167 stocks in the index, 476 rose and 1,603 fell, while 88 were unchanged

Australia stocks slid, the S&P/ASX 200 index falling 1.4% to close at 6,664.40, tracking a decline in US shares last week after inflation expectations rose. All sub-gauges slid, with energy and materials companies the worst performers. In New Zealand, the S&P/NZX 50 index fell 0.8% to 10,785.92.

In FX, the dollar weakened against all of its G-10 peers apart from the yen, as the Bloomberg dollar spot index fell 0.2%. SEK and JPY are the weakest performers in G-10 FX, GBP and AUD outperform; the pound topped the leaderboard and UK government bonds surged on the fiscal policy u-turn. Yields on 10-year gilts fell 26 basis points to 4.05%, while sterling advanced up to 1.2% higher on the day to touch $1.1305 after the BOE confirmed it terminated its emergency bond-buying program. Hedging the pound overnight remains a costly exercise after UK Chancellor of the Exchequer Jeremy Hunt announced measures to “support fiscal sustainability”. Commodity currencies also outperformed. The Australian and New Zealand dollars rose as traders covered shorts after Chinese President Xi warning of “dangerous storms” ahead failed to spur broader selling. The euro traded in a narrow $0.9711-57 range. Bunds and Italian bonds rose alongside Treasuries as central bank tightening bets were pared. Japan’s Yen traded in a narrow range, close to 32-year lows, as traders await fresh impetus to drive it lower and assess potential action from Japanese authorities. Japan’s 30-year bond yield rose to a seven-year high.

In rates, Treasuries rallied, led by the belly and richer by 5bp to 8bp across the curve with gains led by front-end and belly, richening the 2s5s30s fly by almost 5bp on the day; 10-year yields around 3.945%, richer by 7.5bp on the day and lagging gilts by additional 27bp in the sector, following a surge across gilts as BOE rate-hike premium is pared after Chancellor Hunt scraps vast portions of the expansive fiscal stimulus plan that had plunged the market into turmoil. UK yields off lows of the day, although remain richer by 35bp to 40bp across the curve into early US session. UK bonds rally across the curve, led by the long-end, as the new Chancellor is expected to make a statement on the government’s fiscal plans, with the yield on 10-year gilts falling 36 basis points to 3.97% and the pound traded 1.1% higher at $1.1293.

In commodities, WTI drifts 0.2% lower to trade near $85.41 as it fluctuated after a weekly slump as fears over an economic slowdown continue to weigh on the outlook for demand. French PM Borne said about 30% of the country’s petrol stations face supply issues due to a slight worsening of strikes at refineries, while Borne also stated that TotalEnergies ( TTE FP) CEO agreed to extend the fuel discount, according to Reuters. Spot gold is propped up by a softer Dollar, with the yellow metal back above USD 1,650/oz and eyeing its 21 DMA at USD 1,670.10/oz. LME metals are mixed with 3M copper losing some ground and just about holding onto USD 7,500/t+ status, whilst LME aluminium underperforms following an enormous LME stockpile increase of over 65k tonnes.

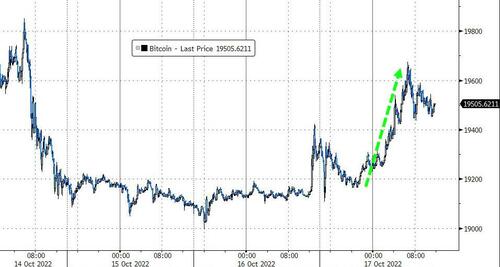

Bitcoin was rangebound and holding just above the USD 19k mark at present.

Looking at the day today, it’s a quiet day with just the Empire Manufacturing index on deck (exp. -4.3).

Market Snapshot

S&P 500 futures up 0.9% to 3,630.00

STOXX Europe 600 up 0.3% to 392.36

MXAP down 0.8% to 136.71

MXAPJ down 0.6% to 442.50

Nikkei down 1.2% to 26,775.79

Topix down 1.0% to 1,879.56

Hang Seng Index up 0.2% to 16,612.90

Shanghai Composite up 0.4% to 3,084.94

Sensex up 0.6% to 58,280.17

Australia S&P/ASX 200 down 1.4% to 6,664.44

Kospi up 0.3% to 2,219.71

German 10Y yield little changed at 2.27%

Euro little changed at $0.9728

Brent Futures down 0.2% to $91.45/bbl

Gold spot up 0.63% to $1,654,87

U.S. Dollar Index down 0.17% to 113.12

Top Overnight News from Bloomberg

UK Chancellor of the Exchequer Jeremy Hunt will accelerate plans on Monday to try to bring order to the UK’s public finances and reassure markets, after Liz Truss’s economic program triggered weeks of turmoil

Chinese President Xi Jinping signaled no change in direction for two main risk factors dragging down China’s economy — strict Covid rules and housing market policies — providing little lift to a worsening growth outlook

Double-digit inflation is set to return in the UK and linger through the end of this year despite the government’s effort to cap energy bills, a survey of economists shows

Speculation intensified among Tokyo’s yen watchers that Japan may be using subtle ways to slow the currency’s decline, zeroing in on the volatility seen after Thursday’s surprise US inflation data. By one estimate, authorities may have spent around 1 trillion yen ($6.7 billion) to support the currency

Further rate hikes are costs without benefits, Polish Monetary Policy member Ireneusz Dabrowski says in interview with Parkiet newspaper

ECB Governing Council member Martins Kazaks said interest rates should be raised beyond year- end — a time when economists increasingly expect the euro zone to be in the midst of a recession

ECB Governing Council member Olli Rehn said financial stability risks on the international markets are “clearly increasing”

EU natural gas prices fell to the lowest level in more than three months as the European Commission plans to propose a temporary mechanism to prevent extreme price spikes in derivatives trading through a dynamic limit for transactions on the Dutch Title Transfer Facility, according to a draft document seen by Bloomberg News.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were negative as the region took its cue from last Friday’s declines on Wall St where risk assets were pressured by inflationary concerns, while the region also digested hawkish global central bank rhetoric and China sticking to its strict zero-COVID policy. ASX 200 was led lower by the commodity-related sectors and with Australian Treasurer Chalmers flagging an increase in the cost of living due to floods in the primary food growing areas. Nikkei 225 weakened with Japan said to consider a rise in corporation tax as an option to fund the nation’s defence budget which could double in the next few years. Hang Seng and Shanghai Comp. were lower following Chinese President Xi’s speech to kick-start the Communist Party Congress in which he defended the zero-Covid policy and reaffirmed intentions for the reunification of Taiwan, while attention was also on the PBoC which rolled over CNY 500bln of MLF loans and kept the rate at 2.75% which suggests a likely pause in its benchmark rates later this week.

Top Asian News

Chinese will delay the release of Q3 economic indicators including GDP, according to the Stats Bureau; no new date mentioned.

PBoC injected CNY 500bln via 1-year MLF with the rate kept at 2.75%, as expected.

China locked down nearly 1mln people near an Apple (AAPL) iPhone factory in which Zhengzhou city ordered residents in one district to stay home, according to Bloomberg.

BoJ Governor Kuroda said the BoJ is continuing with monetary easing since Japan’s headline inflation is likely to fall below 2% next fiscal year, while he added it is appropriate to continue monetary easing to ensure a shift in the deflationary norm and achieve the inflation target in a sustainable and stable manner, according to Reuters.

BoJ Deputy Governor Wakatabe said it is up to the Finance Ministry to decide on whether or not to intervene in the FX market and that current FX fluctuations are clearly too rapid and too one-sided.

Japanese top currency diplomat Kanda said they are ready to take decisive action if excess FX moves continue and are backed by speculative trading, while Kanda reiterated that recent JPY moves were somewhat rapid, according to Reuters.

BoK Governor Rhee said he does not see interest among US officials in pursuing a plaza accord to stem the dollar strength, while Rhee also stated that the BoK needs a little bit more experience and technical capacity for forward guidance, according to Reuters.

South Korean Finance Minister Choo said the government will scrap taxes on foreigners’ income from Korean treasury bonds and monetary stabilisation bonds from Monday, according to Reuters.

China Delays Release of GBP Data Due Tuesday, No Reason Given

Xi Says China’s Power Has Increased, Warns of ‘Dangerous Storms’

EU Agrees to New Iran Sanctions Over Human-Rights Issues

Mizuho CEO Eyes Expanding Investment Banking in US: Nikkei

European bourses see a choppy session but have tilted towards the green after experiencing a mixed cash open. Sectors are mostly firmer with no overaching theme – Insurance, Autos, and Utilties lead the gains whilst Chemicals, Retail and Consumer Products lag. US equity futures see gains across the board following the steep losses on Friday – with the NQ and RTY narrowly outperforming

Top European News

BoE Governor Bailey said they will not hesitate to raise interest rates to meet the inflation target and that the Bank had to intervene to deal with the threat to the stability of the financial system, while they think inflation should peak at around 11% and his best guess is that inflationary pressures will require a stronger response than perhaps thought in August, according to Reuters.

BoE Governor Bailey said he does not comment on fiscal policy but has to emphasise sustainability, while he spoke with UK Chancellor Hunt and said that there is a meeting of minds on sustainability. Furthermore, Bailey said they are going to have to stay very focused on the risks of second-round effects on inflation, according to Reuters.

UK Chancellor Hunt said taking difficult decisions now is the best way to stop interest rates from rising and that the PM hasn’t changed the destination, she has changed the way we are going to get there. Hunt also commented that the PM is in charge and the last thing they need is another Conservative leadership campaign, according to Reuters.

UK Chancellor Hunt said ‘yes’ when asked if he can change the mini-Budget plans and noted that the priority will be to help struggling businesses and families, while he is leaving all possibilities open when asked about government spending and stated that tax will not be cut as quickly and some taxes will go up, according to Reuters.

UK Chancellor Hunt is to make a statement later today, bringing forward measures from the Medium-Term Fiscal Plan that will support fiscal sustainability, via Treasury. Hunt will deliver the full medium-term fiscal plan, to be published with OBR forecasts, on 31st October. Chancellor Hunt met with BoE Governor Bailey and the DMO head on Sunday night, to brief them on these plans.

UK Chancellor Hunt is to delay plans to reduce the basic rate of income tax by a year and it was also reported that the draft forecast by the OBR fiscal watchdog sees the UK will have a black hole in public finances of up to GBP 72bln by 2027/28, according to The Sunday Times.

Senior Tories will hold talks this week on a “rescue mission” that could see the swift removal of Liz Truss as leader, after the new Chancellor Hunt tore up her economic package and signalled a new era of austerity, according to The Observer. Furthermore, The Times reported that Tories held secret talks on installing a new leader and Daily Mail also reported that UK lawmakers will attempt to oust UK PM Truss this week despite warnings from Downing Street that it could trigger a general election.

Reportedly almost all of Kwarteng’s GBP 45bln of unfunded tax reductions is set to be scrapped by Chancellor Hunt, via FT’s Parker; “including income tax cut and stuff on dividends, stamp duty, foreign shoppers and IR35.”

US President Biden said he wasn’t the only one who thought that UK PM Truss’s original economic plan was a mistake, according to Reuters. It was also separately reported that Goldman Sachs downgraded its UK growth outlook after the government tax U-turn.

Head of UK’s Unison union warned the largest nationwide strike of NHS workers since the early 1980s could occur this winter if ministers ignore calls to match pay with inflation, according to FT.

BoE is publishing a market notice which sets out how energy firms and commercial lenders can apply to participate in the energy markets financing scheme; open to applications today; alongside this the UK Gov’t has published a release, outlining the financing scheme and specifying that the gov’t will only be liable if a firm defaults on their repayment; scheme is designed to help firms facing temporary shot-term financing problems.

Europe Gas Drops to 3-Month Low as EU Plans More Crisis Measures

Germany Faces $85 Billion Hit as Labor Shortages Intensify

Dominant Hunt Refuses to Rule Out New U-Turn on Truss Taxes

ITV Jumps as Report Says It’s Exploring Options for Studios Unit

FX

Pound perkier on premise that new UK Chancellor will be more frugal with public finances, Cable comfortable on 1.1200 handle and EUR/GBP probing 50 DMA just shy of 0.8650.

Aussie and Kiwi recover amidst less risk-off environment ahead of RBA minutes and NZ Q3 CPI; AUD/USD hovering around 0.6250 and NZD/USD just under 0.5600.

Loonie, Franc and Euro all firmer vs Greenback as DXY slips from Friday’s peak to pivot 113.000, USD/CAD eyeing 1.3800, USD/CHF close to parity and EUR/USD above 0.9750.

Yen propped ahead of 149.00 vs Dollar as Japanese officials turn up volume of verbal intervention.

PBoC set USD/CNY mid-point at 7.1095 vs exp. 7.1331 (prev. 7.1088)

Major Chinese state-owned banks were seen swapping yuan for dollars in the forwards market and selling dollars in the spot market to stabilise the local currency, according to sources cited by Reuters.

Fixed Income

Gilts gap-up and lead the way ahead of a potential “mini-Budget” U-turn from new Chancellor Hunt, peers buoyed in turn.

Specifically, Gilt Dec’22 posts upside of over 300 ticks around the 97.00 mark with the associated 10yr yield down to near 4.0%.

Amidst this, SONIA is taking a dovish-turn despite the weekend’s remarks from Bailey, with pricing dipping to ‘just’ a ~75% chance of a 100bp increase in November.

Stateside, USTs are firmer by around 15ticks with the US-specific docket comparably sparse after last week’s key inputs.

BoE Gilt statement: As previously announced, the Bank terminated these operations and ceased all bond purchases on Friday 14 October. As intended, these operations have enabled a significant increase in the resilience of the sector.

Commodities

WTI and Brent futures trimmed earlier gains in downside that was exacerbated after reports China is to delay is Q3 GDP release.

French PM Borne said about 30% of the country’s petrol stations face supply issues due to a slight worsening of strikes at refineries, while Borne also stated that TotalEnergies ( TTE FP) CEO agreed to extend the fuel discount, according to Reuters.

Spot gold is propped up by a softer Dollar, with the yellow metal back above USD 1,650/oz and eyeing its 21 DMA at USD 1,670.10/oz.

LME metals are mixed with 3M copper losing some ground and just about holding onto USD 7,500/t+ status, whilst LME aluminium underperforms following an enormous LME stockpile increase of over 65k tonnes.

CCP National Congress

Chinese President Xi declared the new core mission of the party is to lead China united in the challenge to be a powerful, modern socialist nation by 2049. Chinese President Xi said they will promote a high level of opening to the outside world and will maintain pluralistic and stable economic relations with other countries. Furthermore, Xi said they will strengthen the ability to prevent and control the epidemic, while he also commented that the next five years will be crucial for building a modern socialist power and will aim for high-quality growth, as well as support the private economy unwaveringly, according to Reuters.

China Communist Party spokesman Sun said China is capable of greater miracles going forward but noted China has entered a new normal of slower growth and is more focused on fixing long-term issues than growth. Sun also stated that they all hope the pandemic will end soon but what they see now is that the pandemic is still on and that their Covid prevention policy is the best and most economically efficient, according to Reuters.

Chinese government officials are backpedalling on efforts to organise a meeting between US President Biden and Chinese President Xi on the sidelines of the G20 summit next month, according to Politico.

Chinese President Xi said they will firmly promote reunification efforts with Taiwan and it is up to the Chinese people to resolve the Taiwan issue, while he added they will never renounce the right to use force and said reunification of the motherland must and will certainly be achieved.

Chinese Communist Party spokesman Sun said achieving reunification with Taiwan by peaceful means best meets the interest of all and the use of force is the last resort under compelling circumstances, while he added that Taiwan will plunge into a disaster if pro-independence Taiwan and external forces are left unchecked, according to Reuters.

OPEC Headlines

OPEC Secretary-General al-Ghais said slow economic growth reflects on oil demand and that OPEC+ took the pre-emptive decision, while he added OPEC doesn’t target a specific price but targets a balance between supply and demand. Al Ghais also stated that they do not control oil prices and that their decisions are purely technical, as well as noted that there is always space for flexibility in OPEC when asked about reviewing this month’s oil output cut. Furthermore, he commented that oil markets are going through a stage of great fluctuations, according to Reuters.

Iraq said OPEC+ decisions are based on economic indicators and there is consensus in OPEC+ to be pre-emptive to deal with the current uncertainty in oil markets, while it added that the OPEC+ latest decision is based on market inputs and it is essential to achieve market stability, according to a SOMO statement cited by Reuters.

UAE Energy Minister said the OPEC decision was purely technical and unanimous not political as some described, according to Reuters.

Kuwait said it welcomes the recent decision by OPEC+ to cut output and said it is keen to maintain balance in the oil markets for the benefit of consumers and producers, while it added that expected slow global economic growth led to more disturbance in the balance of supply and demand in oil markets, according to Reuters. Furthermore, Kuwait appointed Badr Al Mulla as its new Oil Minister and appointed Wahab Al Rasheed as Finance Minister, according to a tweet.

Oman’s Energy Ministry said OPEC+ decisions are based on purely economic considerations, as well as realities of supply and demand in the market, while the decision was important and necessary to reassure the market and support its stability, according to a Tweet.

Bahrain’s Oil Minister said the OPEC+ decision was reached by consensus among all member states and that OPEC+ will study any economic developments in the future to ensure the stability of markets and global supply, according to the state news agency cited by Reuters.

ECB Headlines

ECB’s Knot said he is increasingly convinced that rates need to rise above neutral and once rates hit a neutral level, it makes sense to consider running off APP stock, according to Reuters.

ECB’s Rehn said the threat of stagflation has intensified. The stability risks of international financial markets are clearly increasing. Although the global financial crisis has been avoided for now, it is not time to breathe a sigh of relief.

ECB’s Lane expected to propose a 75bps hike at the upcoming ECB meeting, according to an ECB insider cited by Econostream.

ECB’s de Guindos expects FX rate to stabilise in the coming months, via Reuters.

Some ECB officials are seeing legal basis to toughen bank TLTRO terms, according to Bloomberg sources.

Geopolitics

Ukrainian President Zelensky said Bakhmut and Soledar in eastern Donbas are hotspots at the front with heavy fighting, while it was separately reported that that Kyiv’s Mayor Klitschko said blasts hit Kyiv’s city centre, according to Reuters.

Russian Defence Ministry said Russia destroyed three US-made M777 Howitzers in Ukraine’s Kharkiv region and that Russian troops repelled Ukrainian attempts to advance in the regions of Donetsk, Kherson and Mykolaiv, according to Reuters.

Russian Defence Ministry said 11 people were killed and 15 were wounded after two Tajikistan citizens committed an act of terrorism at a training ground in Russia’s Belgorod.

08:30: Oct. Empire Manufacturing, est. -4.2, prior -1.5

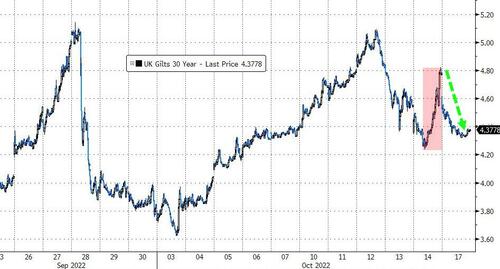

DB’s Jim Reid concludes the overnight wrap

After numerous weeks of immense volatility, will the fact that US payrolls and CPI are out the way and the fact that the UK has sacked its Chancellor, and is gradually backtracking, bit by bit, on its recent fiscal giveaway, lead to calmer markets? We shouldn’t underestimate how much the relatively small UK market has buffeted global markets in recent weeks. The politics are slowly moving in a more market friendly direction but a very sharp sell-off in Gilts on Friday afternoon left a nasty taste as we ended the week. 30yr Gilts closed +24bps on Friday to 4.79% but were around +55bps higher from the lunchtime lows. The Bank of England won’t be buying today for the first time in this mini-crisis so we’ll soon have a decent idea if there are still pension fund liquidity problems.