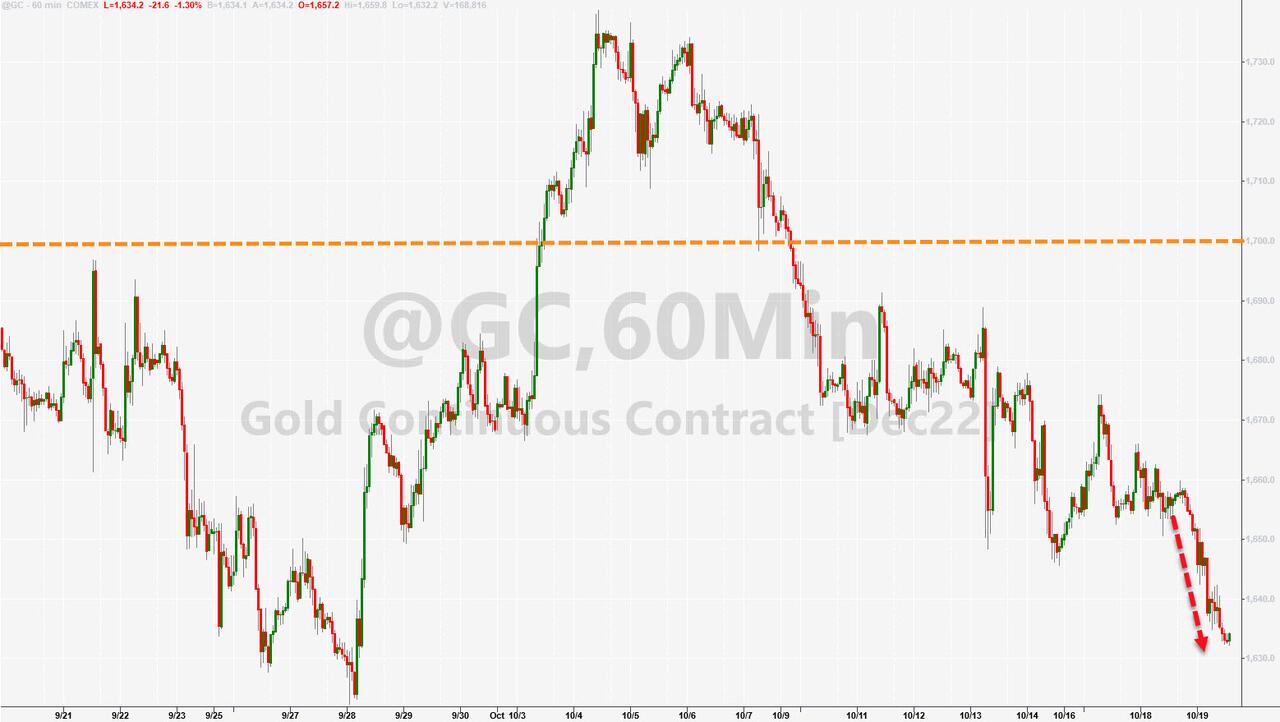

OCT 19//ANOTHER PAPER GOLD/SILVER RAID: GOLD CLOSED DOWN $20.65 TO $1630.20//SILVER IS DOWN 27 CENTS TO $18.41//PLATINUM IS DOWN 24.10 TO $888.75//PALLADIUM IS DOWN 20.15 TO $1997.45//COVID UPDATES: DR PAUL ALEXANDER//VACCINE INJURY//VACCINE IMPACT//IMPORTANT ARTICLES TO READ: TOM LUONGO ON USA VS EUROPE (DAVOS CROWD)//MATHEW PIEPENBERG//UPDATES ON RUSSIA VS UKRAINE//SWAMP STORIES FOR YOU TONIGHT//FINALLY BILL HOLTER INTERVIEW WITH GREG HUNTER A MUST VIEW

323 C HSBC 15 435 H SCOTIA CAPITAL 16 657 C MORGAN STANLEY 1

TOTAL: 16 16 MONTH TO DATE: 22,275

JPMORGAN STOPPED 0/54

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 16 NOTICES FOR 1600 OZ or 0.0497 TONNES

total notices so far: 22,575 contracts for 2,257,500 oz (69.284 tonnes)

SILVER NOTICES: 0 NOTICE(S) FILED FOR NIL OZ/

total number of notices filed so far this month 439 : for 2,145,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $20.65

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////A WITHDRAWAL OF 0.29 TONNES INTO THE GLD//

INVENTORY RESTS AT 938.81 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 27 CENTS

AT THE SLV// :/BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A HUGE WITHDRAWAL OF 1.105 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 486.624 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 751 CONTRACTS TO 136,055 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE GIGANTIC GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.05 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS/HFT WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.05)., BUT UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS. HUGE NUMBERS OF SPECS CONTINUE TO ADD TO THEIR SHORTFALLS FROM WHICH OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS.

WE MUST HAVE HAD: I) SOME SPECULATOR SHORT COVERINGS ////CONTINUED BANKER OI COMEX ADDITIONS /// CONSIDERABLE NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING A 5,000 OZ E.F.P. JUMP TO LONDON / // V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: +2

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 15 days, total 54,815 contracts: 27.408 million oz OR 1.8272MILLION OZ PER DAY. (365 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 27.408 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 27.408 MILLION OZ INITIAL

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 751 DESPITE OUR $0.05 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 618 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /STRONG BANKER ADDITIONS // STRONG SHORT ADDITIONS//CONSIDERABLE NEWBIE SPEC LONG ADDITIONS// /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S 5,000 E.F.P. JUMP TO LONDON .. WE HAD A HUGE SIZED GAIN OF 1369 OI CONTRACTS ON THE TWO EXCHANGES FOR 6.845 MILLION OZ..

WE HAD 0 NOTICE(S) FILED TODAY FOR NIL OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1725 CONTRACTS TO 434,701 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED +100 CONTRACTS.

.

THE GOOD SIZED INCREASE IN COMEX OI CAME DESPITE OUR LOSS IN PRICE OF $7.40//COMEX GOLD TRADING/TUESDAY // CONSIDERABLE SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE. JUMP OF 29,500 OZ//NEW STANDING 72.202TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $7.40 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 3298 OI CONTRACTS 10.258 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1573 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 434,601

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3198 CONTRACTS WITH 1625 CONTRACTS INCREASED AT THE COMEX AND 1573 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3198 CONTRACTS OR 9.947 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1573) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (1625): TOTAL GAIN IN THE TWO EXCHANGES 3298 CONTRACTS. WE NO DOUBT HAD 1) MINOR SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS/// STRONG NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 29,500 OZ QUEUE. JUMP ///NEW STANDING 72.202 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

34,684 CONTRACTS OR 3,468,400 OZ OR 107,88 TONNES 15 TRADING DAY(S) AND THUS AVERAGING: 2312 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAY(S) IN TONNES: 107.88 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 107.88/3550 x 100% TONNES 3.04% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 107.88 TONNES INITIAL ( MUCH SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 751 CONTRACT OI TO 136,055 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 618 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 618 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 618 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 751 CONTRACTS AND ADD TO THE 950 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 1369 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 6.845 MILLION OZ//

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

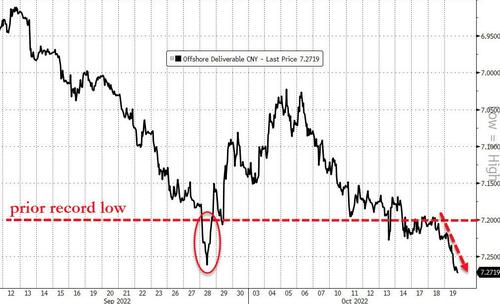

SHANGHAI CLOSED DOWN 36.58 PTS OR 1.19% //Hang Seng CLOSED DOWN 403.30 OR 2.38% /The Nikkei closed UP 101.24PTS OR 0.37% //Australia’s all ordinaires CLOSED UP 0.34% /Chinese yuan (ONSHORE) closed UP TO 7.2278 //OFFSHORE CHINESE YUAN UP 7.2642// /Oil DOWN TO 83.99 dollars per barrel for WTI and BRENT AT 90.71 / Stocks in Europe OPENED MOSTLY RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 1725 CONTRACTS TO 434,705 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS SMALL COMEX INCREASE OCCURRED DESPITE OUR FALL IN PRICE OF $7.40 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (1573 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1573EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 1573 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1573 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3298 CONTRACTS IN THAT 1573LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 1725 CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $7.40//WE HAD SPEC SHORTS ADDITIONS, WITH BANKERS AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD SOME ADDITIONAL NEWBIE SPECS GOING LONG

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (72.202),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 72.202 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $7.40) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS (THEY ADDED TO THEIR POSITIONS) AS WE HAD A FAIR SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 3198 CONTRACTS // WE HAVE REGISTERED A FAIR GAIN OF 10.258 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (72.202 TONNES)…THIS WAS ACCOMPLISHED WITH A FALL IN PRICE OF $7.40

WE HAD -100 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3298 CONTRACTS OR 329,800 OZ OR 10.258 TONNES

Total monthly oz gold served (contracts) so far this month

22,275 notices 2,227,500 69.284 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into Brinks 28,935.900 oz (900kilobars)

total deposits 28,935.900 oz

customer withdrawals:3

i) Out of Manfra 28,935.900 oz (900 kilobars)

ii) Out of Brinks 1993.370 oz

iii) Out of HSBC 96,318.620 oz

total: 127,247.890 oz

total in tonnes: 3.95 tonnes

Adjustments: 1// dealer to customer

i)HSBC 11,042.900 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 954 contracts having GAINED 241 contracts . We had 54 contracts

filed on TUESDAY, so we GAINED A STRONG 295 contracts or an additional 29,500 oz will stand in this active delivery month of Oct. From this point

we should gain in total gold standing through to the end of Oct.( This is queue jumping and in reality it is the exercising of London based EFP;s for gold at the comex)

November GAINED 157 contracts to stand at 3461

December GAINED 1685 contracts up to 359,038

We had 16 notice(s) filed today for 1600 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 16 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (22,275) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 954 CONTRACTS) minus the number of notices served upon today 16 x 100 oz per contract equals 2,321,300 OZ OR 72.202 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (22,275) x 100 oz+ (954) OI for the front month minus the number of notices served upon today (16} x 100 oz} which equals 2,321,300 oz standing OR 72.202 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 72.202 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 429 x 5,000 oz = 2,145,000 oz

to which we add the difference between the open interest for the front month of OCT(234) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 429 (notices served so far) x 5000 oz + OI for front month of OCT (234) – number of notices served upon today (0) x 5000 oz of silver standing for the OCT contract month equates 3,315,000,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

GLD INVENTORY: 938.81 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: AWITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

CLOSING INVENTORY 486.624 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

As we have discussed previously gold is migrating from West to East

As Bloomberg described it, many western investors – particularly at the institutional level – are dumping bullion. Meanwhile, Asian buyers are taking advantage of lower prices to snap up less expensive jewelry, coins, and bars.

According to the Bloomberg report, “large volumes of metal are being drawn out of vaults in financial centers like New York and heading east to meet demand in Shanghai’s gold market or Istanbul’s Grand Bazaar.”

In fact, Asian suppliers are having a difficult time getting enough bullion into Asian markets. As a result, there has been a significant increase in premiums in many Asian countries. September’s average premium in China reached the highest monthly level for nearly six years.

“The incentive to hold gold is a lot lower. It’s going from west to east now,” MKS PAMP SA head of trading Joseph Stefans told Bloomberg.

“We are trying to keep up as best we can.”

New York and London vaults have reported an exodus of more than 527 tons of gold since the end of April, according to data from the CME Group and the London Bullion Market Association. At the same time, gold imports into China hit a four-year high in August.

India, Turkey, Thailand and Saudi Arabia have also reported increased imports of gold.

There is also growing demand for silver in Asian markets, particularly India. The premium on silver has tripled in recent months.

We also see the Asian appetite for gold in central bank purchases. Central banks globally have been net gold buyers for five straight months and all of the big purchases have been in the East.

Turkey has added more gold to its reserves in 2022 to date than any other country. With an 8.9-ton purchase in August, Turkey had increased its gold reserves by 84 tons through the first eight months of the year. Turkey now holds 478 tons of gold between its central bank and treasury holdings, the highest level since Q2 2020.

The Reserve Bank of India has also been a big buyer in 2022. Its total gold reserves now stand at 782.7 tons, ranking it as the ninth-largest gold-holding country in the world. Since resuming buying in late 2017, the Reserve Bank of India has purchased over 200 tons of gold. In August 2020, there were reports that the RBI was considering significantly raising its gold reserves.

Other big gold buyers in 2022 include Kazakhstan, Uzbekistan, Qatar and Iraq.

In the East, many people still use gold as their primary form of savings and wealth preservation. An article published by Seeking Alpha summarizes this dynamic.

For millions of people in Asia gold still is the ‘basic form of saving.’ In contrast to the West, where financialization started decades ago, and gold has slowly been removed from people their day-to-day lives. Until a financial crisis emerges, that is. In the West, people own little or no physical gold when they feel financially confident. People in the East have retained a long-term view concerning gold. Their ancestors saved in gold, and so have they been taught. With the knowledge that ultimately, gold doesn’t lose its purchasing power.”

For instance, Indian households own an estimated 25,000 tons of gold and that number may be higher given the large black market in the country. Gold is not just a luxury in India. Even poor people buy gold in the Asian nation. According to an ICE 360 survey in 2018, one in every two households in India purchased gold within the last five years. Overall, 87% of households in the country own some amount of the yellow metal.

So, while investors in the West are dumping gold as the price falls, investors in the East are taking advantage of the relatively low prices (even though gold is more expensive in many non-dollar fiat currencies) and gobbling up gold as inflation eats away at the value of their local currencies.

END

A good read: The Fed is going to have to choose to pivot or not

My guess: they will not pivot as they blow up Europe. Please see tom Luongo’s huge commentary in the European section of my commentary.

The Federal Reserve is between a rock and a hard place, and it’s going to have to make a hard choice – inflation or economic implosion. Peter Schiff talked about it on his podcast.

Peter said we are very close to another financial crisis and it could be worse than in 2008.

2008 was all about too much debt and the inability to pay. Well, we’ve got a lot more debt now, and we’re even less able to pay. The only thing that kept it going was the artificially low interest rates.”

About a year ago, Treasury Secretary Janet Yellen said there was no reason to worry about the national debt because interest rates were so low. But since the Fed started jacking up interest rates, the cost of financing the national debt has increased by a factor of 16.

So, if the debt wasn’t a problem because it was so cheap to finance it, well, it’s a huge problem now when the cost is 16-times higher.”

Peter reminded the audience that in 2018, the Fed was all about monetary tightening until the economy started to unravel and the stock market crashed. At that point, it pivoted back to rate cuts and QE (that they refused to call QE) – even before the pandemic. At that point, the Fed’s balance sheet was only at $4 trillion. Now it is closer to $9 trillion.

If the Fed really couldn’t get interest rates above 2.5% back then — it’s already got them above that now…”

Peter said he thinks the markets are starting to question the narrative, but they still haven’t figured out that the Fed is stuck between a giant rock and a hard place.

The Fed is going to have to pivot. But inflation is going to run out of control. They’ve got to make a choice. Do they want inflation? Or do they want economic implosion?”

Of course, if the central bank chooses inflation, we’re still going to have an implosion because we’ll ultimately end up with stagflation. It will just happen later.

That’s good enough for the politicians. All they care about is that it doesn’t happen now.”

There’s only one way to legitimately fight inflation. They have to raise interest rates above the rate of inflation so real interest rates are positive. Right now, real rates are at -5%, Meanwhile, the US government has to make massive spending cuts.

They’re not even considering that. Because right now, the way the government pays for spending is with inflation. Inflation is the stealth tax by which the government pays for everything. … How did we get all this government? We didn’t get it for free. We paid for it with inflation. They created money to pay for all this stuff. Now, if the government wants to get rid of inflation, they have to get rid of that money.”

That’s not happening. So, that brings us back to the choice.

Do we want to have a financial crisis, and cut government spending, and allow bankruptcies and defaults and all these losses, or, do we want to have inflation?”

Peter said they’ll pick inflation.

The reason the Fed is going to pick inflation is because that happens later. And, as we’ve seen, they can come up with a scapegoat — blame inflation on somebody else. They never accept responsibility for the inflation they create. So, if the Fed keeps hiking rates and everything implodes, well, hey, we did that to ourselves. If prices run out of control, we can blame OPEC. After all, they just cut production for oil. We could blame Putin. We could blame greedy corporations. We could blame capitalism, speculators. I mean, maybe they’ll even try to blame me. Who knows?!”

Social Security recipients will be getting a big raise in 2023. That’s good news if you’re receiving benefits from the program, but not so great if you’re hoping inflation will abate any time soon.

The Social Security Administration recently announced an 8.7% cost of living adjustment (COLA) for next year. That goes on top of a substantial 5.9% COLA for 2022. The 2023 increase is the largest in 40 years.

The COLA will translate to an additional $140 per month for the average Social Security recipient.

The last time Social Security recipients got a bigger raise was in 1981 when the COLA was 11.2%.

The increase will add about $100 billion of spending per year. The Social Security Board of Trustees said the trust fund can pay full benefits through 2035. After that, the board projects the program will be able to pay 80% of benefits.

A spokesperson for the Committee for a Responsible Federal Budget told CNBC the COLA could accelerate the depletion of the trust funds by at least one calendar year.

The Social Security Administration calculates the COLA based on a formula that uses the “Consumer Price Index for All Urban Wage Earners and Clerical Workers” (CPI-W). Like most government numbers, it doesn’t actually reflect the actual cost of living for most retirees. According to calculations done in 2020, Social Security benefits had lost 33% of their buying power since 2000. And that was in the era of “low” inflation.

This underscores a couple of key points.

1. You can’t count on Social Security to actually secure you a comfortable retirement.

2. You need to plan to protect your wealth from the persistent, insidious erosion of inflation.

More bad news – the COLA increase could actually add to the inflationary spiral.

Peter Schiff talked about it during a recent podcast, pointing out that the people who receive this additional $100 billion will go out and spend it. In other words, the government will be handing out more money so people can cope with higher prices. But that will inevitably push prices higher.

People are supposed to cut back when prices go up. But if the government gives everybody more money to pay the higher prices. You’re just fueling the inflation, and it’s like a dog chasing its tail. You’re never going to catch it, which is why the government is never going to bring inflation down.”

In effect, the extra money will prop up demand, and possibly even increase it. Higher demand without corresponding higher supply inevitably means higher prices. That will likely be reflected in future CPI data.

Social Security faces another problem. With the labor force participation rate falling, there are fewer people paying into the system. As Peter pointed out, the system depends on younger people working and paying into the system in order to keep the Ponzi scheme going.

The problem is those young people aren’t there working. And in fact, older people are retiring earlier, and so we have this smaller labor force participation rate. So, the gap between what the government collects in Social Security taxes and what it’s spending in benefits is rising.”

No matter how you slice it, it’s clear the Social Security system isn’t solvent over the long term.

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

Atlanta Fed hid his trades as the Fed rescued Wall Street

(Pam and Russ Martens)

Pam and Russ Martens: Atlanta Fed president hid his trades as Fed rescued Wall Street

Submitted by admin on Mon, 2022-10-17 11:09Section: Daily Dispatches

By Pam and Russ Martens Wall Street on Parade Monday, October 17, 2022

It was one year ago that Wall Street On Parade raised a multitude of red flags about Raphael Bostic, the president of the Federal Reserve Bank of Atlanta. We have published the entirety of that article below so that our readers can see just how long it took both Bostic and the Atlanta Fed to come clean with the American people about his trading on Wall Street.

On Friday, Bostic released a seven-page statement in which he owned up to the following: failing to list a multitude of trades that were conducted on his behalf by trading firms on Wall Street over a period of five years; failing to properly report income on his assets on his financial disclosure forms; trading during blackout periods when trading was barred by the Federal Reserve; and providing inaccurate values on his financial disclosure forms. The upshot was that Bostic had to restate his financial disclosure forms for the entire five-year period he has filed them at the Atlanta Fed, 2017 through 2021.

If a publicly-traded company had to restate its earnings and admit that it had lied to the American people for five straight years, you can bet that the CEO and CFO would be fired in short order by the Board of Directors. But the Board of the Atlanta Fed is sticking with Bostic — at least for now. …

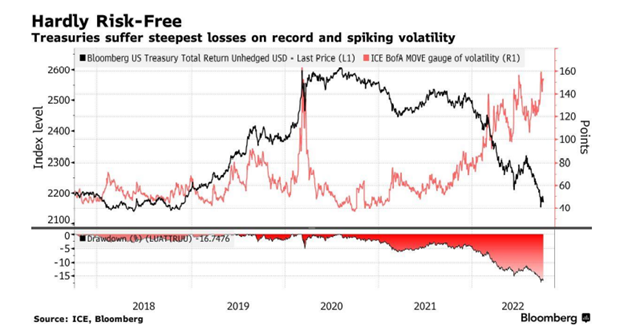

This illiquid Dollar, as argued since the first repo crisis of late 2019, combined with a now weaponized US Dollar on the backs of intentionally rising rates by a cornered and Volcker-wannabe Fed, all converge to spell short-term power for the Greenback and longer-term misery for just about every other asset class and economy in a now openly fractured global financial system.

As to the stark reality/risk of this illiquid Dollar, rather than just say “we told you so,” it would be better to “re-show-you so” by making specific reference to a prior report published in December of 2021.

Since penning that report just over 10 months ago, it’s worth revisiting the implications of an illiquid Dollar and the financial crisis of which we warned then and now find ourselves today.

Why Strong is Weak

It may intuitively feel good to see one’s currency beating all the others and hence puff American chests in a kind of proud admiration for the strongest currency on the block.

Nothing, however, could be further from the truth.

In fact, bragging about a strong US dollar in today’s global neighborhood would be akin to bragging about the healthiest (yet terminally ill) patient in an overcrowded hospice center.

In the end, of course, all fiat currencies revert to the value of their paper, which as Voltaire reminds, is zero.

Or as J.P. Morgan warned years ago, gold is the only money, the rest is debt.

But I digress…

In simplest terms, the strong US Dollar is only relatively strong because every other currency is tanking faster by the second, and this collective spiral is a direct result of the rising US Dollar exporting its inflation to its neighbors and using the bullying power of its world reserve status to weaken, well…the world.

Let’s explain/dig in.

How We Got Here

So, how did we, and the rest of the world’s tanking currencies, get to this embarrassing as well as fatal turning point?

Again, and despite trillions in printed/mouse-clicked US Dollars, much of those dollars are all tangled up in the morass (or “milkshake” aka Brent Johnson) of a highly illiquid derivatives market and increasingly illiquid Euro Dollar market.

As we indicated then:

“As Egon von Greyerz and I have said many times, the first overt signs of this danger in the cash-poor (i.e., illiquid) market reared its ‘repo head’ in September of 2019.

This [repo illiquidity] was a neon-flashing signal of long-term trouble ahead. And it had nothing to do with COVID…

Informed investors in the autumn of 2019 had sifted through all the confusing minutia and noise behind the September panic in the otherwise open-fraud scheme that is the U.S. repo market (i.e., private banks levering GSE deposits for guaranteed payouts from Uncle Sam which the U.S. taxpayer funds).

Despite all this noise, and despite being completely ignored (and deliberately downplayed) by an otherwise teenage-savvy mainstream financial media, the entire repo story simply boiled down to this: There weren’t enough available dollars to keep it (and the banks) going.

As a result, the 2019 Fed printed more dollars and immediately dumped a $1.5 trillion rollover facility into the repo pits.

Much, much more followed.”

And boy did it follow.

As recently reported, the Fed has already begun daily rollover liquidity boosts of over $2T in overnight money-market loans to the increasingly illiquid reverse repo swamp.

This is basically “backdoor QE” and serves as just another sign of a USD-addicted system with a never-ending survival thirst for less and less available (and hence more expensive) Dollars.

The Euro Dollar: All Tangled Up in Blues…

The other skunk in the illiquid Dollar woodpile was what we called the “ticking timebomb” of the misleadingly-named ‘Euro Dollar’ market, discussed as follows:

“In fact, Eurodollars have been floating around the world in greater force since the mid-1950s.

But banks (and bankers) always come up with clever ways to make simple [and liquid] Eurodollar transactions complex [and illiquid], as they can easily hide all kinds of greed-satisfying and wealth-generating schemes behind such deliberate Eurodollar complexity.

Specifically, rather than foreign banks using U.S. Dollars overseas (i.e., Eurodollars) to make simple, direct loans to corporate borrowers that can be easily tracked and regulated on the asset and liability columns of offshore bank balance sheets, these same bankers have spent the last few decades getting more and more creative with the Eurodollar – which is to say, more and more toxic and out of control.

Rather than using Eurodollars for direct loans from Bank “X” to Borrower “Y,” offshore financial groups have been busy using these Eurodollars for complex inter-bank borrowing, swap schemes, futures contracts, and levered derivative transactions.

Tangled Dollars = Unusable, Unavailable and Illiquid Dollars

All of this scheming, leverage and swapping boils down to not enough available (i.e., liquid) USDs in a global financial system in which nearly everything—from debt, to oil to derivatives—still has to be paid in increasingly scarce and hence increasingly expensive Dollars.

In addition to this twisted, illiquid and over-levered swamp, the USD rises even higher on Powell rate hikes, all of which combine to force the world’s other currencies to fall.

Why?

Because other countries and central banks have no choice but to swallow/import USD inflation, monetary policy and American political self-interest. Indeed, with financial allies like the U.S., who needs enemies?

Whenever the Fed, for example, prints more of the world reservecurrency or raises its interest rate, the rest of the world, which is tied to that currency, is forced to react—i.e., debase, hike and suffer.

We remind that nearly $14T in USD-denominated debt is owed by both emerging market and developed market economies.

As the USD rises in strength on the back of Powell’s impossible Volcker-revival and tangled derivatives, other Dollar-desperate nations from Argentina to Japan find themselves with not enough Greenbacks to pay their debts or settle trades, wires and oil purchases, which thus forces them to print (i.e., debase) more of their local currencies to make USD-denominated payments.

But Japan takes the cake for debasing its own currency all on its own, as no nation has ever loved a money printer and currency-debaser more.

This might explain why Japan is leading the charge in dumping its USTs into the FOREX markets, which only adds more pressure to rising yields and hence rising rates.

Thanks Kuroda—just one more central banker with a mouse-clicker gone mad… Perhaps he’ll be next in line for a Nobel Prize?

But Japan is not alone, as other nations dump the once sacred UST just to keep their currencies afloat…

In short: The strong USD is crippling the word, and that world, as we’ve written numerous times, will be de-dollarizing at a steady and irreversible pace.

No shocker there. At some point, Dollar-indebted nations crack and this twisted global game ends in a credit crisis for the history books.

Other Domino Effects of the Illiquid Dollar

It’s also worth noting that a current and temporarily strong USD effectively knee-caps US exports, as anything that is actually produced in the USA is now far more expensive and hence less competitive abroad, further adding to US trade deficits (not to mention budget deficits) in a world marching toward a financial cliff.

As importantly, as the USD rises in a new environment of rising rates and less liquid dollars, commercial banks in the US (10X levered) and in Europe (20X levered) are exploiting this higher rate policy to de-lever their derivatives exposure, which squeezes an already fatally toxic $2 quadrillion derivatives market, thereby making that ticking timebomb one tick closer to full implosion.

So, no, a strong and illiquid Dollar (world reserve currency) is hardly good for America, the markets or the world. It’s a poison rather than inflation-killer.

How to Fix the Poison?

For those waiting for the Fed to fix the morass we now find ourselves, there is no miracle cure ahead but merely a choice among poisons.

Pick Your Poison

As we’ve warned numerous times, the Fed is caught between a rock and hard-placeof its own profoundly inept design.

Should Powell continue his open ruse to allegedly “fight inflation” (which is 50% unreported anyway) using rising rates, then the USD and DXY will keep rising until the global (and debt-driven) economy completely buckles under the expensive weight of unpayable (and dollar-denominated) IOU’s.

Meanwhile, truth-allergic (as well as history-blind and math-inept) politicos will scramble from one government-complicit, PRAVDA-like propaganda platform to the next blaming the looming credit and currency implosion they engineered on a virus, a Vladimir, an oil well or a coal plant.

However, once the US policy makers admit we are in a recession, there will be no way to fight that recession (and the additional $300B in interest expenses owed for every 1% rate hike) without mouse-clicking more USDs and hence forcing the Dollar and rates down rather than up, as no recession in history has ever been defeated with high rates and a roaring currency.

Alas, what is high today will be low tomorrow, and the Fed (controlling a US economy driven by over 91T in combined public, household and corporate debt and a 125% public debt to GDP ratio) will have to choose between saving the bond and stock markets or killing its currency.

That is, the Fed will eventually (don’t ask me when) join the ranks of the UK, Japan and other nations forced to revert/pivot toward their smoking money printers.

Pivot Point?

For now, I still see Mr. Powell heading toward in inevitable (though not imminent) pivot from hawk to dove once credit markets and economies are in even more peril than their press secretaries can deny.

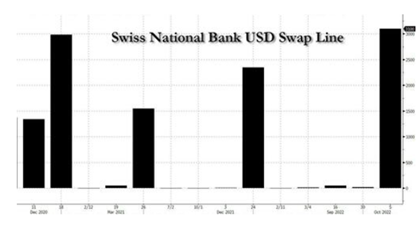

Again, lack of USDs in general (and GDP growth in particular) has already forced the Bank of England to confess its mouse-click/QE addiction, and just recently the Swiss National Bank took a $3.3 billion swap line from the Fed to give its central bank more of those otherwise scarce and expensive USDs.

In the interim, the deliberate efforts by the Fed to engineer a painful recession after they engineered the greatest/grossest asset bubble (and wealth transfer) in history can only be seen as either intentionally evil or unpardonably stupid.

Pick your own verdict. I’d vote for both…

At that pivot point, the Dollar will fall, inflation will rise and stagflation will become the new normal for many years to come, for it’s also worth noting that no modern nation has ever enjoyed a “softish-landing” (quoting Powell) in a recessionary backdrop in which inflation was greater than 5%–and we are already far ahead of that embarrassing and central-bank-created marker.

So, and again, pick your poison: Depression or Inflation? Dead market or dead currency?

A Prize for the Guilty?

As for this current and one-way trip toward global ruin, we can thank Mr. Powell (as well as Bernanke, Greenspan and Mrs. Yellen), none of whom deserve a Nobel Prize, and yet the fact that Bernanke (who gave Japan its QE and Yen-destroying playbook in the late 80’s) now has such a prize is just further proof that this rigged to fail system has completely lost any mooring to sanity, honesty, ethics or economic decency.

Bernanke’s “nobel/noble” policy is the equivalent of buying one’s son a home with an Amex card and then sending the invoice to the grandson.

In short, Bernanke holding a Nobel Prize makes as much sense as Bernie Madoff winning “trader of the year”—but then again, neither ethics nor truth ever stopped Madoff from becoming the NASDAQ’s chairman…

I can’t help but think of La Rochefoucauld’s maxim that “the highest offices are rarely, if ever, served by the highest minds…”

We’ve written too many articlesand books to make the Fed’s guilt any more clear today than it already was yesterday.

As for debt-soaked, Frankenstein markets now reeling under rising rates and ever scarcer Dollars, we are nowhere near a bottom and no way out of the woods of ever more volatility to come.

And as for Gold…

As for gold, it rises as fiat currencies tank. For now, the relative and short-lived power of the Fed’s rising rates has been a tailwind to the Greenback and thus a headwind to USD-priced gold.

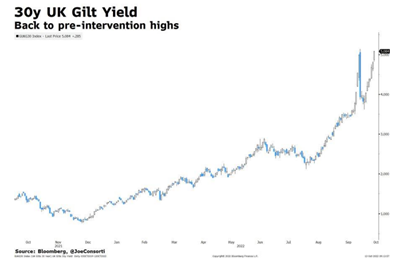

For other countries like Japan or the UK, however, their central banks simply can’t afford the same rate hikes which the Fed’s suicidal reserve eminence allows, so the gold price in the Yen is rising as the purchasing power of the Yen is falling…

…and the same is true for the tanking British pound and rising gold price there:

But like Japan and the Bank of England, every other major central bank from the ECB onward will need to print more local currencies to keep their bonds from tanking and yields from spiking…

Despite its world reserve status, the US Treasury markets face a similar fate and the hard math points toward more inevitable mouse-click QE from the Fed to purchase its own debt.

This makes a tanking USD plain to see coming, and hence gold’s historical USD rise equally plain to predict.

In the interim, the LBMA and COMEX markets are using forward contracts to force gold down in pricing so they can take physical delivery for themselves before the metals skyrocket in USD.

Smart money is catching on, as flows out of paper gold and into physical gold mark a new direction.

For informed investors, now is the value window to do the same with physical gold.

Unfortunately, and as in every asset class and historically-confirmed bubble, the common psychology is to buy high and sell low rather than buy low and sell high.

Informed gold investors, however, are not making this human-all-too-human error as the world tilts each day toward dying paper and rising metals.

Unless, of course, you still think the Fed has your back?

Jeeeessshhhhh.

3.Chris Powell of GATA provides to us very important physical commentaries

China’s huge Zijin Mining to buy Iamgold’s Rosebel gold mine in Suriname. It is not a big deal

(Reuters)

China’s Zijin Mining buys Iamgold’s Rosebel gold mine in Suriname

Submitted by admin on Tue, 2022-10-18 21:14Section: Daily Dispatches

Iamgold Shares Surge on Sale of Suriname Mine to China’s Zijin Mining

By Ruhi Soni Reuters via Nasdaq.com Tuesday, October 18, 2022

Canadian gold miner Iamgold Corp. shares surged 16% today after it decided to sell 95% stake in Rosebel Gold Mines unit in northeastern Suriname to China’s Zijin Mining Group Co. Ltd. for about $401 million.

The Toronto-based company said the proceeds from the sale will be used to construct its flagship Cote Gold project in Canada so that it can stay on track to begin production in early 2024.

The Rosebel Gold Mine unit holds a mine in Suriname of the same name as well as a 70% interest in the Saramacca Mine, Iamgold said, adding that the country’s government will continue to hold the remaining 5% interest in the unit. …

Correction – no lead in the US, and only 202 tons of zinc in US, which is in New Orleans.

it gets worse

The only aluminum in US warehouses is 7,000 tons and change in Toledo, but not a single pound in the eligible category. This is all going to hit after the election. BB

end

COMMODITIES IN GENERAL/

END

END

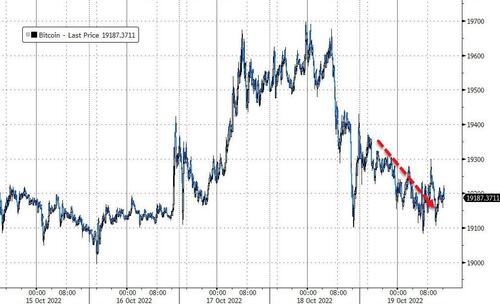

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.2278

OFFSHORE YUAN: 7.2642

SHANGHAI CLOSED DOWN 36.58 PTS OR 1.19%

HANG SENG CLOSED UP 403.30 OR 2.38%

2. Nikkei closed UP 101.24 PTS OR 0.37%

3. Europe stocks SO FAR: MOSTLY RED

USA dollar INDEX DOWN TO 112.72/Euro FALLS TO 0.9774

3b Japan 10 YR bond yield: RISES TO. +.249/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 149.65/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.352%***/Italian 10 Yr bond yield RISES to 4.752%*** /SPAIN 10 YR BOND YIELD RISES TO 3.51%…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 5.05//

3j Gold at $1634.10//silver at: 18.44 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 21/100 roubles/dollar; ROUBLE AT 61.37//

3m oil into the 83 dollar handle for WTI and 90 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 149.65DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 1.0034–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.98044well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

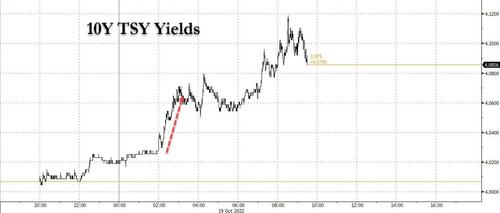

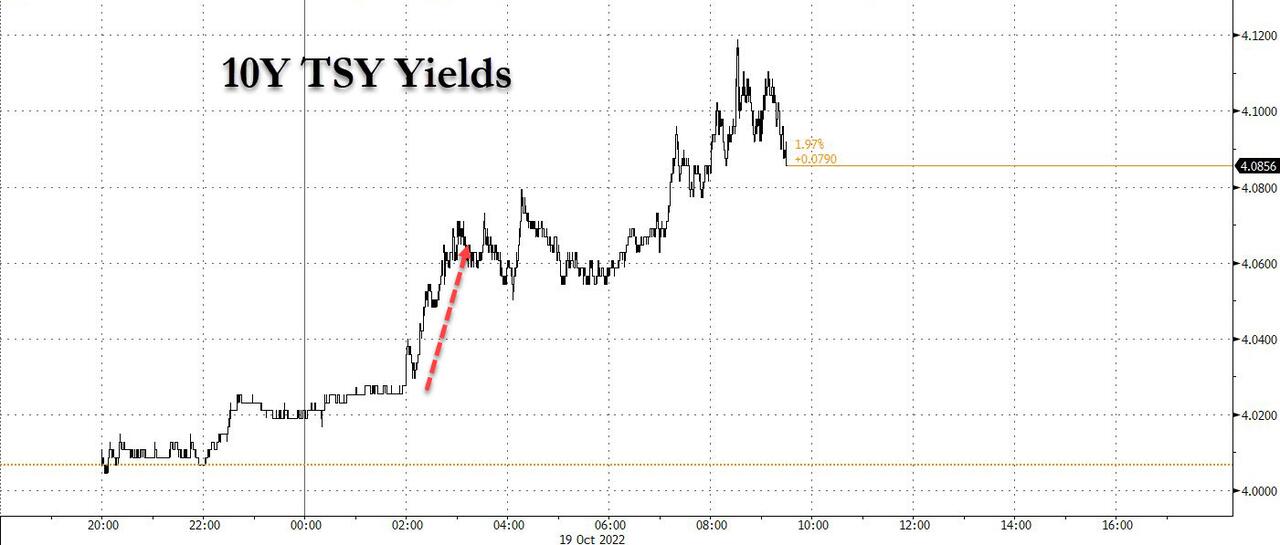

USA 10 YR BOND YIELD: 4.079% UP 8 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 4.080% UP 6 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,59…GETTTING DANGEROUS

GREAT BRITAIN/10 YEAR YIELD: 4.05%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Fumble 1% Gain, Turn Sharply Lower As Yields, Dollar Soar

WEDNESDAY, OCT 19, 2022 – 08:08 AM

US stock futures erased overnight gains of over 1% as worries about the impact of scorching inflation and a looming recession took the shine off a strong start to the corporate earnings season. Contracts on the S&P 500 dropped 0.4% in an extremely illiquid session at 7:15 a.m. in New York after earlier rising as much as 1.1%. Nasdaq 100 futures were also down 0.4%, despite a boost from a better-than-expected report from Netflix which sent the stock soaring 13% in premarket trading.

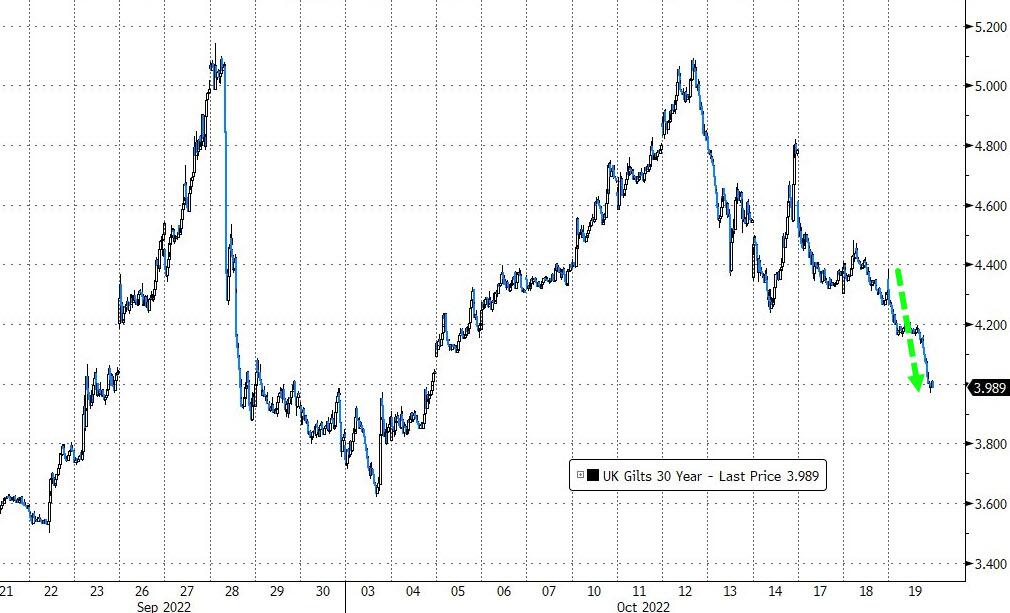

Behind the sudden, violent slump is today’s renewed surge in interest rates which pushed the 10Y Yield to 4.10%, the highest level since October 2008, potentially driven by news that the BOE would launch gilt sales on Nov 1.

A surge in the dollar sparked by a plunge in sterling, which tumbled after soaring food prices drove UK inflation back into double digits in September, matching a 40-year high of 10.1% and intensifying pressure on the central bank and Liz Truss’s government to act. Gilts were broadly lower weighing on rates sensitive sectors like banks, property and construction and retail. The result is that UK equities dropped following four days of gains.

In premarket trading, Netflix soared as much as 14% in premarket trading, set for its biggest jump since January 2021, after the video streaming company handily beat estimates for paid subscribers, signaling the worst of the slowdown is likely over. Shares of other video-streaming companies are rising after Netflix’s quarterly results reassured investors that its business was back on track. Walt Disney +2.8%, Roku +3.7%, Warner Bros Discovery +1.7%, fuboTV +3.4%. Bank stocks are lower in thin premarket trading Wednesday, putting them on track to snap a two-day winning streak. In corporate news, Mitsubishi UFJ Financial Group is evaluating an acquisition of some loan portfolios from Credit Suisse to expand its business in the US. HSBC has been reprimanded by a UK watchdog for violating environmental advertising rules, after it sought to depict itself as a green bank in a set of posters. Here are other notable premarket movers:

United Airlines shares jump 7.1% in US premarket trading Wednesday following earnings that beat estimates, with analysts saying results and outlook are impressive on strong demand, better costs. Here’s what they are saying:

Lam Research leads fellow chip-tool makers higher in premarket trading after ASML said its fourth-quarter sales would likely be better than estimates, driven by strong demand for its advanced chip-making machines. Lam Research (LRCX US) +3.1%, Applied Materials (AMAT US) +1.7% and KLA (KLAC US) +2%

Olaplex shares plummet 42% in premarket trading after the hair-care products company slashed full-year forecasts due to slowing sales and announced the departure of its COO Tiffany Walden.

Evercore ISI cuts Best Buy, Lowe’s, Advance Auto and Petco Health & Wellness to in-line from outperform in note on Wednesday. All the stocks drop in premarket trading. Best Buy (BBY US) falls 1.6%, Lowe’s (LOW US) -1.1%, Advance Auto (AAP US) -1.1%, Petco (WOOF US) -3.2%

Keep an eye on Polaris as the stock was cut to neutral from buy at Citi as the broker flags retail environment being “substantially worse than previously anticipated” after it made checks with the company’s off-road vehicle dealers.

Intuitive Surgical shares jumped 7.4% in postmarket trading on Tuesday after the company posted revenues and adjusted earnings per share for the third quarter that were higher than consensus analyst estimates.

Upbeat company results, cheaper valuations and UK policy reversals have helped buoy risk appetite in recent sessions. At the same time, investors are having to keep track of weakness in the global economy and the impact of persistent inflation on decisions by policymakers at the Federal Reserve and other central banks.

Indeed, US stocks have had a roller-coaster October so far as investors swing between fears about a hawkish Federal Reserve and optimism over early third-quarter reports that have showed signs of resilience to higher prices. While a Bank of America survey showed full capitulation among stock investors, strategists have warned that the uncertain macroeconomic outlook could fuel further declines, according to Bloomberg.

“While it looks like capitulation, we probably have not seen a bottom yet,” said Randeep Somel, a portfolio manager at M&G Investments. “Companies’ earnings are not reflecting wider macro economic expectations yet, and that isn’t likely to dissipate until around early next year once we got through what is likely to be a rough winter,” he said on Bloomberg TV.

Quantitative strategists at Citigroup Inc. said US stocks were pricing in the highest odds of a recession than any other asset class, but still could be poised for more losses. “US equities have priced the most (but not enough) recession risk, and earnings estimates have further to adjust,” strategists including Alex Saunders wrote in a note dated Oct. 18 (he must be ignoring commodities, which are pricing in a global depression).

“US equities have priced the most (but not enough) recession risk, and earnings estimates have further to adjust,” strategists including Alex Saunders wrote in a note. “US bonds have priced the least risk, but it will take some time before bonds react to recession risks given the hawkish Fed.”

European stocks struggled to eke out a fifth day of gains as most sectors decline; real estate, retail and utilities drop, while tech and insurance outperform. Euro Stoxx 50 rises 0.2%, paring earlier gains; Stoxx 600 is down 0.2%. IBEX lags, dropping 1%. Utilities stocks fell, led by German names, after Handelsblatt reported that the German Economy Ministry is planning to cap electricity prices along the lines of the proposals made to cap gas prices. The sector is among the worst-performing groups on the broader gauge, down 1.1%, with Encavis, RWE and BKW all down at least 4.5%. In Germany’s plan, utilities will have to offer relief for consumers on a base contingent designed to encourage energy saving, according to the report

Earlier in the session, Asia stocks fell, with shares in Hong Kong dropping the most in the region as the maiden policy speech by the territory’s leader failed to ease concerns about China’s earnings outlook and rising mainland Covid cases. The MSCI Asia Pacific lost as much as 0.8%, erasing an earlier gain, as shares of technology companies such as Alibaba, Tencent and TSMC weighed. A selloff in consumer stocks dragged down Hong Kong and China gauges as a plan unveiled by Chief Executive John Lee to woo back foreign talent and ease housing woes failed to offset concerns about earnings and Covid. Benchmarks in Japan and Australia rose in tandem with gains in Wall Street. Read: HK Developers Drop as Stamp Duty Rule Disappoints: Street Wrap Most Asia fund managers in a survey by Bank of America expect weaker corporate profits in the region during the next 12 months, with net 72% of the view that consensus estimates for earnings per share growth are too high. It’s been almost a year since Bitcoin hit a record. Where do you see it going from here? Fill out our survey. “Global growth expectations are shrouded in pessimism but improving on the margin for China,” the survey report said. “However, investors are wary that the continued pursuit of a zero-Covid strategy could pour cold water on their fledgling hope for a China recovery.” China’s intermittent lockdowns continue to weigh on sentiment, with the ongoing party congress in China offering little hope to investors and traders assessing the impact on corporate profits in the latest results season. The MSCI Asia gauge is trading near April 2020 levels after dropping more than 28% this year

Japanese stocks extended their advance to second day, driven by gains in information companies and machinery makers. The Topix rose 0.2% to 1,905.06 as of 3 p.m. close in Tokyo, while the Nikkei 225 advanced 0.4% to 27,257.38. SoftBank Group contributed the most to the Topix’s gain, increasing 3.7%. Out of 2,166 stocks in the index, 1,376 rose and 674 fell, while 116 were unchanged.

Australian stocks edged higher, with the S&P/ASX 200 index rising 0.3% to close at 6,800.10 as investors digested quarterly output reports from commodity producers. All sectors gained except for energy and technology. Banks and industrials contributed the most to the gauge’s advance. In New Zealand, the S&P/NZX 50 index rose 0.6% to 10,916.65.

Indian stocks indexes rose for the fourth straight session before giving away the majority of gains, dragged by the rupee’s slide against the dollar. The S&P BSE Sensex rose 0.3% to 59,107.19 in Mumbai, while the NSE Nifty 50 Index advanced 0.1%. The gauges rose as much as 0.7% before paring the advance in the last hour of trading. For the week, they are up about 2% each. The Indian rupee tumbled to a record, declining to 82.98 against the greenback in late trading, as the central bank was seen moving away from supplying dollars. The looming expiry of weekly derivative contracts also weighed on local shares. Ten of the 19 sector sub-gauges compiled by BSE Ltd. advanced today, led by energy companies, while utilities and power firms were the worst performers. “Domestic institutions have been strong buyers in the market over the last week, as 2QFY23 results have come in line or stronger than expected,” S Hariharan, head of institutional equity at Emkay Global Financial, said.

In FX, the Bloomberg dollar spot index spiked 0.3% as the greenback rose against all of its Group-of-10 peers apart from the New Zealand dollar; the yen tumbled to a fresh 32 year low of 149.70 against the dollar while the pound slumped below $1.13. The euro slumped to almost $0.98. The shift in the euro’s volatility term structure shows that traders are following central banks into being more data dependent than before. Australian and New Zealand dollars trim intraday gains alongside similar moves in US futures.

In Japan, authorities continued their jawboning of the yen, with Finance Minister Shunichi Suzuki saying he is increasing the frequency of monitoring foreign-exchange markets. The currency hovered above 149 per dollar. The 10-year government bond yield rose above the 0.25% upper limit of the central bank’s target range, a breach that’s likely to prompt the Bank of Japan to step up bond purchases to limit the advance.

“The outlook for the UK is very, very difficult and certainly when focusing on our asset allocation it’s predominantly in the US where we have much higher conviction and certainty of outcome,” Grace Peters, JPMorgan Private Bank’s head of investment strategy, said on Bloomberg Television.

In rates, Treasuries were cheaper across the curve with losses led by belly, cheapening 2s5s30s spread by 3bp into early US session. US yields cheaper by nearly 7bp across belly of the curve, flattening 5s30s spread by almost 3bp following three successive steepening sessions; 10-year around 4.09%, cheaper by ~8bp on the day. US coupon issuance resumes with $12b 20-year bond reopening; WI yield near 4.34% is above all auction stops since the May 2020 reintroduction of the tenor and ~52bp cheaper than September auction, which stopped through by 1.3bp

Front-end bund yields rose by 12bps as the curve bear- flattened after Germany’s Finance Agency said it will increase the amount of securities it can lend to traders in the repo market by €54b, a move strategists say will help ease a collateral squeeze that has plagued the debt market in recent months. Bunds underperform gilts and USTs. German 10-year yield is up 7 bps to 2.35%, while gilts 10-year yield is up 3bps to below 4% and Treasuries 10-year yield climbs ~5bps to above 4%. Most UK bonds fell, while the pound dropped as much as 0.6% after data showed UK CPI rose 10.1% last month from 9.9% in August, exceeding economists expectations of 10% and adding to pressure on policy makers to lift the key rate significantly next month. The bank of England also confirmed that it will start selling down its portfolio of gilts.

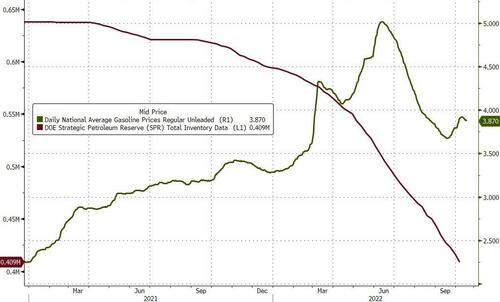

In commodities, oil rose amid concerns that the European Union’s latest sanctions on Russian fuel could exacerbate the market tightness that the US is trying to alleviate with additional sales. The Biden administration will announce Wednesday a plan to release 15 million barrels from US emergency oil reserves in an effort to ease high gasoline prices. WTI and Brent Dec futures are firmer intraday after yesterday’s decline, which saw Brent dip under USD 90/bbl but settle at the figure. LME metals are mostly softer amid the firmer Dollar and risk aversion, with 3M copper extending its losses under USD 7,500/t. US President Biden will lay out plans on Wednesday to continue using the SPR to gain more stability in gas prices and will reiterate that gasoline company profits are too high and should be returned to consumers, according to a senior administration official. Furthermore, the Biden administration agreed to make future oil purchases to refill reserves at prices at or below USD 67.00-72.00/bbl, while President Biden will announce 15mln additional barrels for delivery from SPR in December, extending the initial timeline and completing the 180mln commitment. Spot gold trades lower intraday and back under the USD 1,650/oz mark as the Dollar picks up in pace.

Japan plans to further loosen crypto rules as soon as December “by making it easier to list virtual coins, potentially boosting the country’s allure for Binance and rival exchanges”, according to Bloomberg.

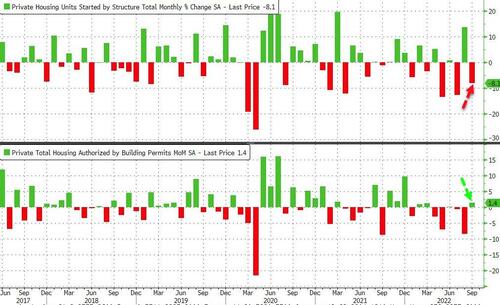

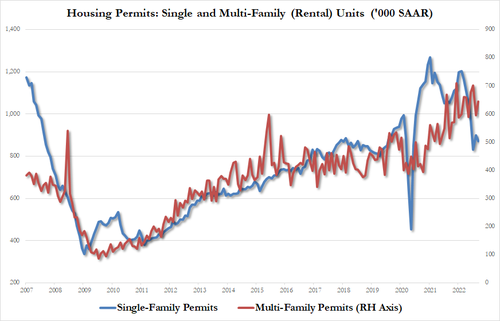

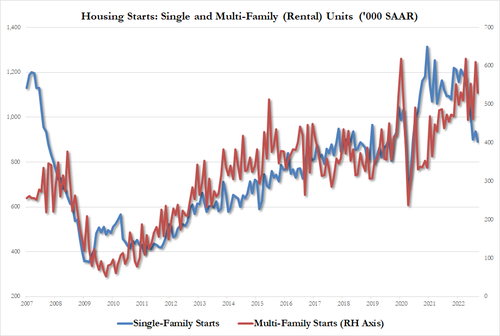

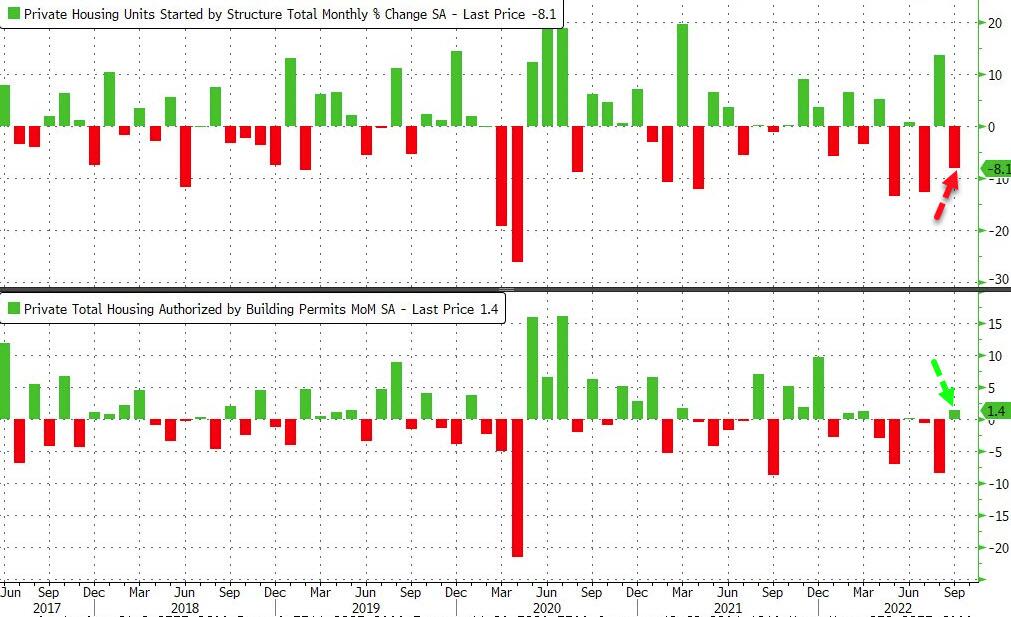

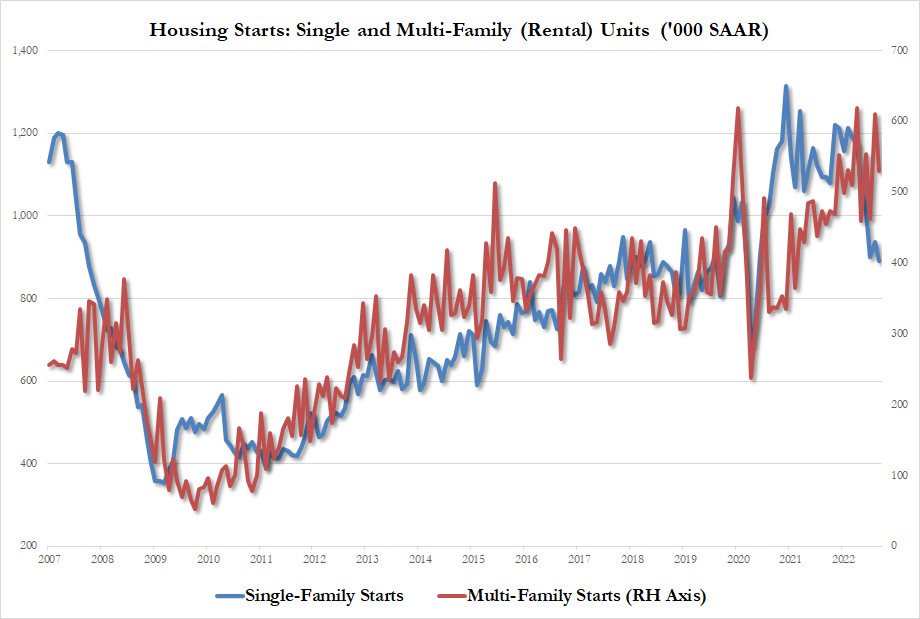

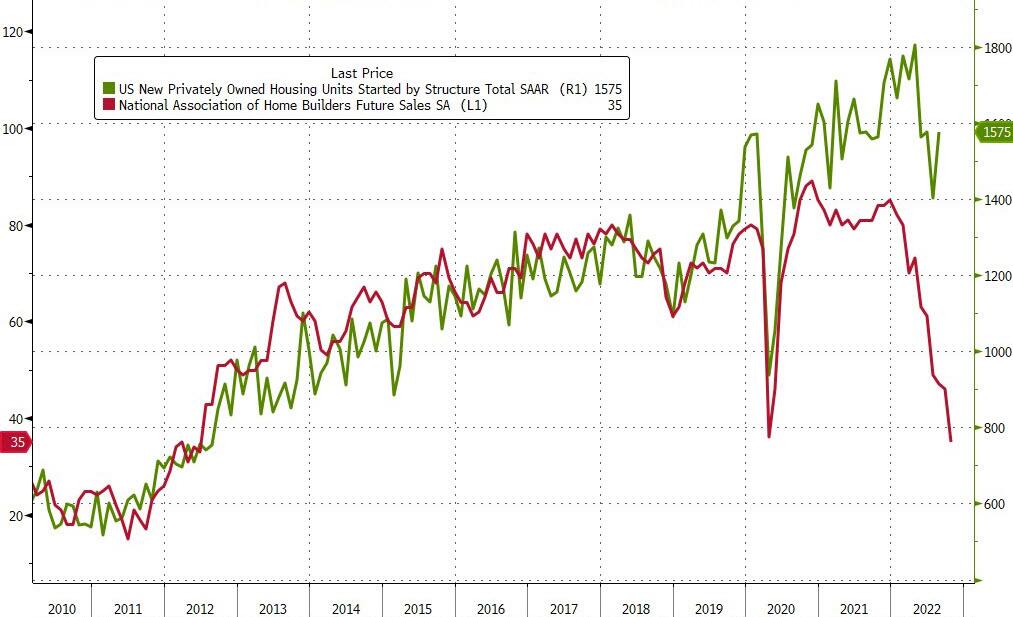

Looking to the day ahead now, data releases include the UK and Canadian CPI readings for September, along with US housing starts and building permits for September. From central banks, the Fed will release their Beige book, and we’ll also hear from the Fed’s Kashkari, Evans and Bullard, the ECB’s Centeno and Visco, and the BoE’s Cunliffe and Mann. Finally, earnings releases include Tesla, Procter & Gamble and Abbott Laboratories.

Market Snapshot

S&P 500 futures down 0.2% to 3,726.50

STOXX Europe 600 down 0.4% to 398.38

MXAP down 0.8% to 137.80

MXAPJ down 1.1% to 445.81

Nikkei up 0.4% to 27,257.38

Topix up 0.2% to 1,905.06

Hang Seng Index down 2.4% to 16,511.28

Shanghai Composite down 1.2% to 3,044.38

Sensex up 0.2% to 59,077.34

Australia S&P/ASX 200 up 0.3% to 6,800.06

Kospi down 0.6% to 2,237.44

German 10Y yield up 3% to 2.354

Euro down 0.3% to $0.9826

Brent Futures up 0.6% to 90.59

Gold spot down 0.7% to $1,640.03

U.S. Dollar Index up 0.25% to 112.42

Top Overnight News from Bloomberg

Embattled UK Prime Minister Liz Truss faces a brewing parliamentary rebellion if she is forced to abandon a key Conservative manifesto commitment on pensions as part of a frantic austerity drive

Record-low demand for German bonds at a government auction suggests investors are getting picky as countries ready a wall of sales and speculation mounts that the ECB will start reducing the bonds it’s amassed on its balance sheet over the years

Bank of Japan Board Member Seiji Adachi reinforced the central bank’s message that it won’t adjust policy in response to the rapid weakening of the yen, pushing back against persistent market speculation

The value of US Treasuries owned by Japanese investors slid by almost 3% in August to the lowest level in three years as a slump in global debt markets hammered down prices

A number of hedge funds are starting to come around to the idea that it may be time to buy the beaten-up pound and gilts. Others say investors should remain cautious. Great Hill Capital in New York sees opportunities to go long sterling after the currency’s recent wild ride. Blue Edge Advisors Pte sees positives in longer- maturity gilts as global growth slows

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mixed following the choppy performance stateside where the major indices wobbled on news that Apple cut iPhone 14 Plus production less than two weeks after its debut, but then recovered heading into the close and with futures underpinned after-hours after strong earnings and subscriber additions from Netflix. ASX 200 gained with outperformance in defensive sectors although the upside was contained by a lacklustre mood in miners after BHP’s quarterly output update which included higher iron output but also a severe drop in coal production. Nikkei 225 was led higher by notable strength in blue-chip names including SoftBank and Fast Retailing and with firm gains also in utilities and power stocks, while the latest commentary from BoJ board member Adachi echoed the central bank’s dovish message as he warned against a shift towards tightening and pushed back on responding to short-term FX moves with monetary policy. Hang Seng and Shanghai Comp. remained pressured amid COVID concerns and data uncertainty, while Hong Kong Chief Executive John Lee’s first annual Policy Address failed to inspire a turnaround despite the announcement of measures to support property, tech start-ups and attract foreign talent.

Top Asian News

Hong Kong Chief Executive John Lee said in his first annual Policy Address that national sovereignty and security are top priorities, while he also noted Hong Kong faces a “new chapter” of development and warned Hong Kong faces risks from global turmoil and Covid. Lee added that they will allow overseas talent to refund extra stamp duty on home purchases and will introduce a bill this year to exempt the stamp duty payable for transactions conducted by dual-counter market makers. Lee also stated the HKEX will revise main board listing rules next year to facilitate fundraising of advanced tech enterprises that have yet to meet the profit and trading record requirements, according to Reuters.

BoJ’s Adachi said monetary policy does not directly control FX and there are times FX moves rapidly short-term, while he added that responding to short-term FX moves with monetary policy would heighten uncertainty over BoJ’s guidance which is not good for the economy. Adachi also stated that inflation is starting to increase but he is not convinced yet that the BoJ’s target will be achieved in a stable and sustained manner. Furthermore, he said they must be cautious about shifting toward monetary tightening as downside risks to the economy are increasing and a shift to monetary tightening would weaken demand and heighten the risk Japan will revert to deflation, while the best approach now is to maintain easy monetary policy.

Coal Miner Left With Retiring Plants in Indonesia Green Push

Taiwan Central Bank Sees Severe Economic Challenges Next Year

Billionaire Ambani Splurges $163 Million on Priciest Dubai Villa

Singapore’s COE Category B Bidding Rises to S$110,000