OCT 20//ANOTHER GOLD AND SILVER MANIPULATIVE DAY: GOLD CLOSED UP $2.40 TO $1632.40//SILVER WAS UP 33 CENTS TO $18.74//PLATINUM CLOSED UP $27.45 TO $916.20//PALLADIUM CLOSED UP $66.50//JAMES TURK; A MUST READ!//COVID UPDATES//DR PAUL ALEXANDER//VACCINE MANDATE//RUSSIA VS UKRAINE UPDATES//IN THE UK: PRIME MINISTER TRUSS RESIGNS//UPDATES ON THE EUROPEAN/UK FINANCIAL/ENERGY MESS//SWAMP STORIES FOR YOU TONIGHT//

323 C HSBC 153 435 H SCOTIA CAPITAL 22 657 C MORGAN STANLEY 5 661 C JP MORGAN 153 1 880 H CITIGROUP 9 905 C ADM 7

TOTAL: 175 175 MONTH TO DATE: 22,450

JPMORGAN STOPPED 1/175

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 175 NOTICES FOR 17500 OZ or 0.5493 TONNES

total notices so far: 22,57 contracts for 2,245,000 oz (69.2828 tonnes)

SILVER NOTICES: 3 NOTICE(S) FILED FOR 15,000 OZ/

total number of notices filed so far this month 432 : for 2,160,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $2.40

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////A WITHDRAWAL OF 6.08 TONNES INTO THE GLD//

INVENTORY RESTS AT 932.73 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 33 CENTS

AT THE SLV// :/BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A HUGE WITHDRAWAL OF 0.921 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 485.703 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 714 CONTRACTS TO 136,769 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.27 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS/HFT WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.27)., BUT UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS. HUGE NUMBERS OF SPECS CONTINUE TO ADD TO THEIR SHORTFALLS FROM WHICH OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. SOME SPEC LONGS ADDED TO THEIR POSITIONS WITH THE VERY ATTRACTIVE PRICE.

WE MUST HAVE HAD: I) SOME SPECULATOR SHORT COVERINGS ////CONTINUED BANKER OI COMEX ADDITIONS /// SOME NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING A 10,000 OZ QUEUE. JUMP / // V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: –70

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 16 days, total 55.215 contracts: 27.608 million oz OR 1.7255MILLION OZ PER DAY. (345 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 27.608 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 27.608 MILLION OZ INITIAL

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 714 DESPITE OUR $0.27 LOSS IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 400 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /STRONG BANKER ADDITIONS // STRONG SHORT ADDITIONS//SOME NEWBIE SPEC LONG ADDITIONS// /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S 10,000 QUEUE JUMP .. WE HAD A HUGE SIZED GAIN OF 1114 OI CONTRACTS ON THE TWO EXCHANGES FOR 5.570 MILLION OZ..

WE HAD 3 NOTICE(S) FILED TODAY FOR 15,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 8741 CONTRACTS TO 443,442 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED 225 CONTRACTS.

.

THE STRONG SIZED INCREASE IN COMEX OI CAME DESPITE OUR LOSS IN PRICE OF $20.65

//COMEX GOLD TRADING/WEDNESDAY // CONSIDERABLE SPECULATOR SHORT COVERINGS ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION AND STRONG SPEC SHORT ADDITIONS // CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE. JUMP OF 4200 OZ//NEW STANDING 72.333TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $20.65 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A HUGE SIZED GAIN OF 13,014 OI CONTRACTS 40.479 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4273 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 443,442

IN ESSENCE WE HAVE A HUGE SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 13,014 CONTRACTS WITH 8741 CONTRACTS INCREASED AT THE COMEX AND 4273 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 12,789 CONTRACTS OR 939.780 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4273) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (8741): TOTAL GAIN IN THE TWO EXCHANGES 13,014 CONTRACTS. WE NO DOUBT HAD 1) STRONG SPECULATOR SHORT ADDITIONS// CONTINUED GOOD BANKER ADDITIONS/// STRONG NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 4200 OZ QUEUE. JUMP ///NEW STANDING 72.303 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) STRONG SIZED COMEX OPEN INTEREST GAIN 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

38,957 CONTRACTS OR 3,895,700 OZ OR 121.17 TONNES 16 TRADING DAY(S) AND THUS AVERAGING: 2434 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES: 107.88 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 121.17/3550 x 100% TONNES 3.40% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 121/17 TONNES INITIAL ( MUCH SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 714 CONTRACT OI TO 136,769 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 400 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 400 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 400 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 714 CONTRACTS AND ADD TO THE 400 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 1114 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 5.570 MILLION OZ//

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 9.33 PTS OR 0.31% //Hang Seng CLOSED DOWN 231.06 OR 1.40% /The Nikkei closed DOWN 250.42PTS OR 0.92% //Australia’s all ordinaires CLOSED DOWN 1.16% /Chinese yuan (ONSHORE) closed UP TO 7.2260 //OFFSHORE CHINESE YUAN UP 7.2448// /Oil UP TO 87.46 dollars per barrel for WTI and BRENT AT 93.65 / Stocks in Europe OPENED MOSTLY GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 8741 CONTRACTS TO 443,442 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX INCREASE OCCURRED DESPITE OUR FALL IN PRICE OF $20.65 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (4273 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4273EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 4273 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4273 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUGE SIZED TOTAL OF 13,014 CONTRACTS IN THAT 4273LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI GAIN OF 8516 CONTRACTS..AND THIS HUGE SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $20.65//WE HAD HUGE SPEC SHORTS ADDITIONS, WITH BANKERS AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD SOME ADDITIONAL NEWBIE SPECS GOING LONG WITH OUR NEW ATTRACTIVE LOW PRICE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (72.333),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 72.333 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $20.65) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS (THEY ADDED TO THEIR POSITIONS) AS WE HAD A HUGE SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 13,014 CONTRACTS // WE HAVE REGISTERED A HUGE GAIN OF 39.780 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (72.333 TONNES)…THIS WAS ACCOMPLISHED DESPITE OUR FALL IN PRICE OF $20.65

WE HAD +225 CONTRACTS COMEX TRADES ADDED. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 13,014 CONTRACTS OR 1301,400 OZ OR 40.473 TONNES

Total monthly oz gold served (contracts) so far this month

22,450 notices 2,245,000 69.828 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals:2

i) Out of HSBC: 56,894.928 oz

ii) Out of Brinks 739.470 oz (23 kilobars)

iii) Out of HSBC 96,318.620 oz

total: 57,634.398 oz

total in tonnes: 1.79 tonnes

Adjustments: 1// dealer to customer

i)Manfra: 2290.173 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 980 contracts having GAINED 26 contracts . We had 16 contracts

filed on WEDNESDAY, so we GAINED A STRONG 42 contracts or an additional 4,200 oz will stand in this active delivery month of Oct. From this point

we should gain in total gold standing through to the end of Oct.( This is queue jumping and in reality it is the exercising of London based EFP;s for gold at the comex)

November GAINED 40 contracts to stand at 3501

December GAINED 6316 contracts up to 365,354

We had 175 notice(s) filed today for 17,500 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 153 notices were issued from their client or customer account. The total of all issuance by all participants equate to 175 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (22,450) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 980 CONTRACTS) minus the number of notices served upon today 175 x 100 oz per contract equals 2,325,500 OZ OR 72.333 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (22,450) x 100 oz+ (980) OI for the front month minus the number of notices served upon today (175} x 100 oz} which equals 2,325,500 oz standing OR 72.333 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 72.333 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 432 x 5,000 oz = 2,160,000 oz

to which we add the difference between the open interest for the front month of OCT(236) and the number of notices served upon today 3 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 432 (notices served so far) x 5000 oz + OI for front month of OCT (236) – number of notices served upon today (3) x 5000 oz of silver standing for the OCT contract month equates 3,325,000,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

GLD INVENTORY: 938.81 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: AWITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

CLOSING INVENTORY 485.703 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

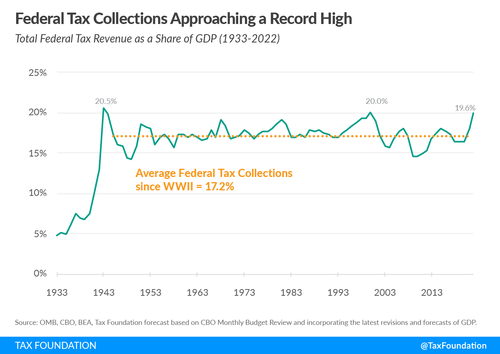

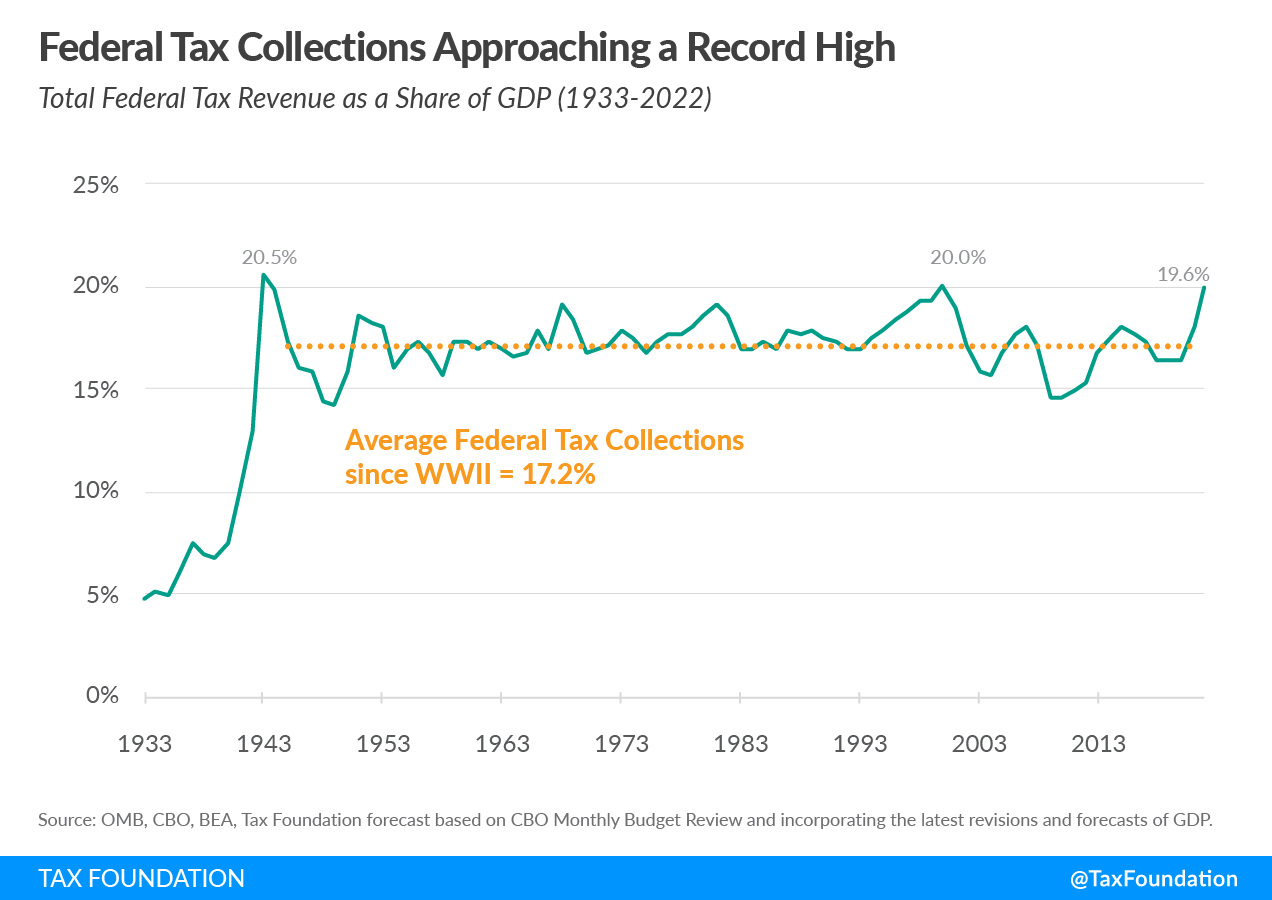

Federal Tax Receipts Near Record-High Share Of GDP

US tax receipts have surged this year. Through August, the US Treasury had collected over $4.4 trillion in revenue for fiscal 2022 with one month left to go. That was already 10% higher than receipts in 2021. The US government took in $303.73 billion in August alone. That was up 23% from August 2021.

According to a Tax Foundation analysis of Congressional Budget Office data, federal tax collections were up 21% in the 2022 fiscal year that ended on Sept. 30.

The US government isn’t just making a windfall in absolute terms. Tax collection is at a multi-decade high of 19.6% as a share of GDP. That is up from 17.9% in fiscal 2021 and is approaching the last peak of 20% set during the dot-com bubble in FY 2000.

Besides the dot-com bubble, federal tax receipts have only represented a higher share of GDP in two other years, both during World War II. In 1943, federal tax collections reached 20.5% of GDP before falling to 19.9% in 1944.

Compared to average federal tax collections in the post-war era of 17.2% of GDP, 2022 collections are set to exceed that level by 2.4 percentage points.

Individual income tax collections surged the most, up 29% from $2.0 trillion last year to $2.6 trillion this year.

The Question

This raises a question: if the government is taking in near-record levels of taxes, how is it running massive deficits month after month?

The answer is simple: Uncle Sam has a spending problem.

History shows that over a long period of time government will spend whatever the tax system raises plus as much more as it can get away with. That’s why we’ve had universal deficits.”

The US government has spent money at roughly a half-trillion per month clip all year. In August, Uncle Sam blew through another $523.3 billion. This brought total spending for fiscal 2022 to just over $5.35 trillion.

According to the Committee for a Responsible Federal Budget, policies enacted by the Biden administration will add more than $4.8 trillion to deficits between 2021 and 2031.

On top of increased spending, rising interest rates will balloon the debt even more.

Every increase in interest rate raises the federal government’s interest expense. So far in fiscal 2022, the US Treasury has forked out $471 billion just to fund the government’s interest payments.

Individual income tax receipts are projected to decline as a share of GDP over the next few years because of the expected dissipation of some of the factors that caused their recent surge. For example, realizations of capital gains (profits from selling assets that have appreciated) are projected to decline from the high levels of the past two years to a more typical level relative to GDP. Subsequently, from 2025 to 2027, individual income tax receipts are projected to rise sharply because of changes to tax rules set to occur at the end of calendar year 2025. After 2027, those receipts remain at or slightly below the 2027 level relative to GDP.”

As the economy spins deeper into a recession as the Fed tightens monetary policy to fight raging inflation, you can expect revenue to tank further, meaning even bigger budget shortfalls.

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

LAWRIE WILLIAMS: No let up for gold and silver

Contrary to our expectations, gold and silver prices continued to weaken Wednesday as the dollar strengthened again and U.S. Treasury yields picked up again after dropping back a little on Tuesday. This choppy nature for the principal precious metals seems more or less set to continue for as long as the U.S. Fed appears to be committed to its current aggressive approach to raising interest rates to try and counteract the current high levels of inflation that are currently afflicting U.S. retail markets. The 0.4% rise in the core inflation level demonstrated by the October 13th Consumer Price Index (CPI) data from the Bureau of Labor Statistics made at least a 75 basis point Federal Funds rate rise at the early November FOMC meeting a virtual certainty, and a year-end interest rate level of between 4.5 and 4.75% is now the predicted outcome. This will almost certainly lead to an even stronger U.S. dollar and potentially even weaker gold and silver prices as U.S. Treasury and 10-year TIPS yields rise accordingly making non-interest-generating assets like gold ever increasingly less favourable investment assets.

The only real hope now it seems for the precious metals investor is that the FOMC participants will become aware of the damage that the high interest rates are likely to do to the U.S. economy – they will certainly drive it into recession, if it is not there already, which some reckon it is. At some stage they may thus ease off the pressure and start to reduce the levels of the rate rises as inflation begins to come down, but perhaps not as quickly as the Fed would like, towards the 2% target rate. Again, looking at the Fedwatch Tool, some market observers see this happening by mid 2023, but others still see the Fed maintaining its aggressive approach for longer.

Either way, gold has something of a chequered history as an inflation hedge. Over the long term it tends to come out fairly well as a wealth protector but short term, as now, the performance tends to be rather more mixed. It does tend to perform better – or perhaps that should be less poorly – than most other asset classes though which is some consolation for the gold holder. Silver, on the other hand, tends to be altogether more speculative and, as at present, can seriously underperform its yellow sibling. At one point last week the Gold:Silver ratio (GSR) slipped back to 90 (a high GSR is bad for silver- out and out silver bulls reckon it should be around 16-20) and it is currently sitting above 88 as I write).

Equities performed rather better over the past week than we might have expected from the overall global recessionary trend. U.S. earnings performance was, perhaps, a little stronger than might have been anticipated but the equity indexes were all beginning to turn downwards again towards the week’s end, although had not given back all the gains made earlier – but give them time! Recessions are negative for stock prices and we could well see some severe falls as economies continue to suffer from the inflationary trends and the consequent economic downturns worldwide. U.S. markets tend to be ever optimistic though so they could buck the likely pattern as we see it developing.

20 Oct 2022

-END-

END

3.Chris Powell of GATA provides to us very important physical commentaries

This is interesting: Russian central bank sees no need to raise gold holdings despite sanctions. It looks like China and Turkey will be the only guys that will buy this sanctioned gold

(zerohedge)

Russian central bank sees no need to raise gold holdings

Submitted by admin on Wed, 2022-10-19 09:06Section: Daily Dispatches

By Anastasia Lyrchikova and Elena Fabrichnaya Reuters via Nasdaq.com Tuesday, October 18, 2022

MOSCOW — Russia’s central bank sees no need to raise gold holdings in its gold and foreign exchange reserves, its deputy governor, Alexei Zabotkin, said Tuesday, shrugging off a plea from gold miners to increase state purchases amid Western sanctions.

The association of the Russian gold producers told a meeting of officials at Russia’s upper house of the parliament on Tuesday that the government should support the industry with purchases amid sanctions on the Russian banks and disrupted exports.

“In terms of accumulating gold in gold and foreign exchange reserves, this is something that is not advisable at the moment, because it would create additional impetus to the growth of the money supply,” Zabotkin told the same meeting.

He said that Russia’s central bank made gold purchases on the domestic market in March and April, but those “were small volumes.”

Sergei Kashuba, the head of Russia’s Gold Industrialists’ Union, told the meeting that the central bank’s purchases in the spring were carried out with a 12-15% price discount to London gold prices. …

With huge dollar shortages occurring across the globe, we find Swiss banks ever so eager to pick up these dollars and use them to lend to needy nations in desperate need of them.

(Bloomberg)

Swiss banks seek most dollars since 2008 in bid for easy profit

Submitted by admin on Wed, 2022-10-19 20:06Section: Daily Dispatches

Why is the Federal Reserve running a scheme to enrich Swiss banks?

* * *

By Bastian Benrath Bloomberg News Wednesday, October 19, 2022

Banks in Switzerland sought the most dollars since 2008 using an emergency dollar swap facility provided by the Federal Reserve in what is likely to be a bid for easy profits.

In today’s auction conducted by the Swiss National Bank, 17 institutions took up $11.09 billion. That’s the most since October 2008, when the Global Financial Crisis was raging in the wake of Lehman Brothers’ collapse.

This is the fourth week in a row when banks have accessed the facility. Last Wednesday 15 banks took up $6.27 billion in funds.

According to economists at Credit Suisse, Swiss banks swap the dollars into francs in order to generate a profit. The lenders can even sell the cash back to the Swiss National Bank using its reverse repo auctions, or deposit it at the institution to benefit from a positive interest rate.

“We do not believe that the increased demand for U.S. dollar liquidity by domestic banks reflects any liquidity issues in the Swiss banking system,” Credit Suisse economist Maxime Botteron wrote in a report last week. …

“The Earth speaks to us through the elements of nature. In every natural thing, we can find a hidden, powerful message.”

– Ralph Waldo Emerson

Every natural element with which the earth has been endowed has a usefulness—a purpose. If we listen to gold, its message is loud and clear—gold is money. To serve as natural money is gold’s highest purpose.

The advance of civilization demonstrates that nature throughout the ages, to our good fortune, has provided everything humanity needs to progress, including money. Few today, however, understand money as it has existed from prehistory and as it was perceived up until the dawn of the twentieth century. Since the commencement of the First World War in 1914, time-honored principles have been abandoned. Humanity has become enthralled with money substitutes like national currencies and, more recently, cryptocurrencies circulating in place of money, and people have subsequently lost sight of natural money itself.

Gold Is Natural Money

Although gold these days rarely circulates as currency because of government imposed restrictions and impediments, gold still retains all the features that explain why humanity in prehistory chose it to be money. Gold is natural money, or stated another way, nature’s money is gold, which is well illustrated by the following chart that presents the price of crude oil measured in four different currencies from a base of 100.

A gram or an ounce of gold buys essentially the same amount of crude oil today as it has at any time over the past seven decades. I have purposefully chosen oil because the energy it provides is essential to our standard of living.

Using gold to measure the price of other commodities has a similar result, but not the price of manufactured products. They tend to fall over time because advances in technology lead to increasing production efficiencies. An obvious example is computer chips, whose price has fallen dramatically in recent decades, yet which are still profitable to the companies that make and sell them.

Gold preserves purchasing power, which is one of the key requisites of money. As illustrated by the above chart, it is an outcome that no national currency can match.

Another requisite of money is the enablement of sound economic calculation, which is only possible when using a consistent, unchanging unit of account to measure prices over time. Gold serves this role perfectly because it is the only element in the known universe that is eternal and not subject to decay or degradation. A gram of gold today is identical to a gram of gold mined by the Romans.

Gold’s natural features that fulfil the two requisites of money stated above explain why gold is accumulated. Commodities are consumed and disappear, but because it is money, all the gold mined throughout history still exists in its aboveground stock, except for the inconsequential weight lost in shipwrecks and from coin abrasion.

The Gold Stock

A gold stock of 297 tons is estimated to have existed in 1492, when generally reliable record keeping of production and stocks began. That weight of gold when visualized comprises a cube of 4.3 feet (131cm) per side for a total of 79.5 cubic feet, which equals the volume of space encompassed by a small kitchen table. Today’s cube would just about slide under the arches of the Eiffel Tower.

Gold is not valuable because it is rare. Plenty of gold exists that has yet to be mined on land, under the oceans, and even extracted from ocean water when the technologies become available to make that mining possible. Gold is valuable because it is useful but mined—produced—only when it is profitable to do so, which depends on how gold has been dispersed in the earth’s crust when combined with humanity’s ability, financial capacity, and available technology needed to discover, mine, and refine it.

Growth of the Gold Stock Compared to the Stock of Dollars

Over the centuries gold becomes harder to find and mine, yet its aboveground stock has grown about the same annual rate. The average annual rate over the last 529 years is 1.2 percent. Since 1960 it is 1.8 percent, ranging from 1.4 percent to 2.2 percent.

The annual growth rates of the stock—the total quantity—of dollars since 1960 varies from a low of 1 percent in 1993 to a high of 19.1 percent in 2020. This inconsistency results in swings in the dollar stock that in turn causes volatility in prices expressed in dollars because there are not enough or too many dollars circulating relative to the prevailing level of economic activity.

Gold comes closer than any central bank managed currency in achieving Milton Friedman’s k-percent rule that the quantity of currency should increase by a constant percentage rate every year, irrespective of bank credit cycles. The gold stock grows at approximately the same rate as world population and new wealth creation. Consequently, the purchasing power arising from the interaction of gold’s supply—its aboveground stock—and the unfailing inelastic demand for gold that exists because it is money, make gold uniquely useful to accurately calculate the price of goods and services throughout time. It is a feature that the dollar and other national currencies fail to match because their annual growth rates are not consistent, causing fluctuations in their “aboveground” stock. Since 1950 the weight of the gold stock has grown 3.5 times, but a gram of gold still purchases the same amount of crude oil.

What is more, the growth rate of the dollar stock since 1960 has averaged 7.1 percent, which is four times greater than the average growth rate of the gold stock over this period. This more rapid increase in the dollar stock is debasing the dollar relative to gold, a reality clearly illustrated in the above chart of crude oil prices, which raises an important point.

The stock of dollars is controlled by the managers of the banking system. Recurring bank and currency crises throughout history result from human error and other human frailties that inevitably destroy fiat currency, like the unwillingness to “take away the punchbowl” after a period of prolonged credit expansion. Gold is different.

Gold does not need management by a central bank or government. Gold is money that manages itself because growth in the gold stock is controlled by two immutable forces—nature and profitable mining. Together they impose discipline on the production of gold that prevents the money punchbowl from overflowing, which is a key factor explaining why gold preserves purchasing power over time.

The Essential Nature of Honest Money

The timeless reliability in the interconnection of gold’s supply and demand sets gold apart from national currencies as does its essential nature. Gold is tangible; national currencies are an intangible financial promise with counterparty risk. This risk arises because promises do get broken, as was demonstrated in the 2008 financial crisis and countless other banking and fiat currency crises.

Gold is natural money that has served humanity well throughout history by enabling people to achieve an ever-higher standard of living. We can ponder whether this outcome results from fortuitous chance or from the intelligent design of a creator endowing the earth’s resources providentially to equip humanity with natural money. Regardless of gold’s origin, which is unknowable, it cannot be denied that gold is money and is as useful today as any time in history.

end

From Nicholas B

a must read…

After a period of some twenty years of being a very keen student of all matters relating to precious metals and in recent times engaging in deep immersion in a proliferation of podcasts etc., I think I am in a position to proffer some meaningful comments.

Many commentators stress that physical gold and silver have been a store of value for several millennia and the absence of any counterparty risk has been a major factor in differentiating physical precious metals from fiat currencies, which rarely have a life span (or supremacy) of more than four decades. Absolutely. On the other hand ,paper gold and silver contracts, with a potential backing of underlying physical metal at 100 to one (or is it 500) have only been in existence since the first COMEX gold futures contract was traded in 1974.In that time, the advances perfected in the techniques of trading algorithms and high frequency trading capacity have become normative market manipulation practices.

Remember this 2009 story? Sergey Aleynikov, a naturalized US citizen who emigrated from Russia, was arrested on Friday night as he arrived at Newark Liberty International Airport and charged with trade-secret theft. On four occasions since June 1, the 39-year-old programmer downloaded a total of 32 megabytes of data from Goldman Sachs servers in New Jersey, according documents filed in federal court in Manhattan. The allegedly pilfered software used “sophisticated mathematical formulas to place automated trades in the market,” the documents alleged. Such trades typically generate “many millions of dollars.” The documents didn’t identify Aleynikov’s former employer, but during a court hearing on Saturday, prosecutors revealed it was Goldman Sachs.

Therefore it is probably a reasonable postulation that manipulative gold and silver paper trading has been magnificently perfected in the last decade to the point where seeking to extrapolate projected future price movements based on historical chart patterns is meaningless and futile. I listen carefully to the Live from the Vault podcasts, since Andrew Maguire is the supreme commentator on the physical wholesale precious metal market (matched only by Andy Schectman’s commentaries on the retail markets). Sometimes I have to listen repeatedly to Andrew’s wonderfully crafted words in order to fully comprehend (as far as possible) the full significance of what he is saying. So many times in the last few years I have felt a warm glow after listening to Andrew and come to the conclusion that ‘it won’t be long now’-before the precious metal markets explode as the manipulation and fractional reserving become completely unsustainable. But the headline price of the precious metals continues to spiral downwards.

This is my interpretation of what is currently transpiring. The COMEX disclosed inventories are now (comparatively) so gossamer that they are almost of no consequence (and there is also the relatively final option of exercising force majeure clauses.) There is much informed commentary as to the relatively favourable positioning of the trading desks of the large investment banks in the event that the headline paper price of the precious metals was ever to be released from the stranglehold and consequence of serial and perpetual creation of infinite numbers of naked short paper contracts. For many years, MIDAS has serially invoked the principle of Occam’s Razor by blaming the cabal for the daily grotesque and blatantly manifest manipulation of the paper price of the precious metals. I believe that the orders that the cabal execute come from a higher authority than the trading desks of certain large investment banks, who may not even be briefed as to the bigger picture.

The problem with a ‘blow-up’ in the paper precious markets and the invocation of fiat settlement options (as hidden in the contractual small print) would be that the whole western world would then realize that possession and ownership of physical precious metals is all that matters. (How much physical do you have?) Remember that:

* After adjustment for BOE vault holdings and ETF physical inventors stored in loco London, there is ,again ,a gossamer amount of physical bullion available to satisfy the claims of not only ‘unallocated investors’ but also ‘allocated investors’ and no one knows whether criminal fractional reserving policies and blatant theft (termed re hypothecation) has resulted in more or less than 500 claims to every ounce of residual loco London vault precious metal.

* The thousands of tonnes of precious metal obligations that have been miraculously ‘settled’ by Exchange for Physical (EFPs) sourced from the LBMA may in fact have been serially rolled forward and thus remain as future delivery obligations on the counter parties (the cabal)

* If circumstances demand, the reported physical vault precious metal holdings of some ETFs can increase overnight by tonnage that logistically would take several weeks to deliver in the real world.

* The reported gold reserves of the IMF at 2,814 tonnes are merely quota allocations of gold from the IMF’s founding members back in 1944, and these allocations have always been double counted as both IMF gold and vault gold held by the quota allocating central bank

* The BOE and Federal Reserve have almost certainly rehypothecated many times over the physical gold that should constitute the gold reserves of so many nations who disclose bullion reserves that are not held physically within their own domain. There is a camp of informed commentators who postulate that the Federal Reserve has virtually no physical gold in its custody. The quantum of tonnage of physical gold transferred from West to East in the last few decades makes no sense if such rehypothecation is denied.

The grotesque manipulation of the paper gold price cannot end without the unravelling of a story that is far too big to ever see the light of day. For how long will the principal protagonists in the East v West confrontation be prepared to delay unveiling the ‘nuclear’ option of moving to a physical gold standard, which will devastate the West almost to the same extent as a nuclear option without the inverted commas?

Regards

Nicholas

END

5.OTHER COMMODITIES:

end

COMMODITIES IN GENERAL/

END

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 7.2260

OFFSHORE YUAN: 7.2448

SHANGHAI CLOSED DOWN 9.33 PTS OR 0.31%

HANG SENG CLOSED DOWN 231.06 OR 1.40%

2. Nikkei closed DOWN 250.42 PTS OR 0.92%

3. Europe stocks SO FAR: MOSTLY GREEN

USA dollar INDEX DOWN TO 112.41/Euro RISES TO 0.98131

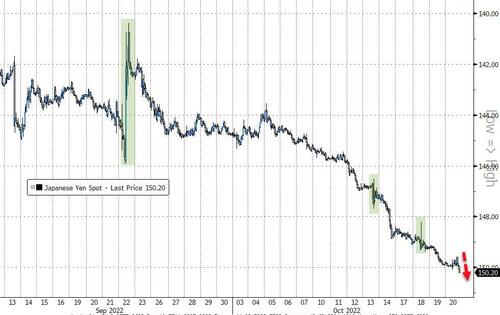

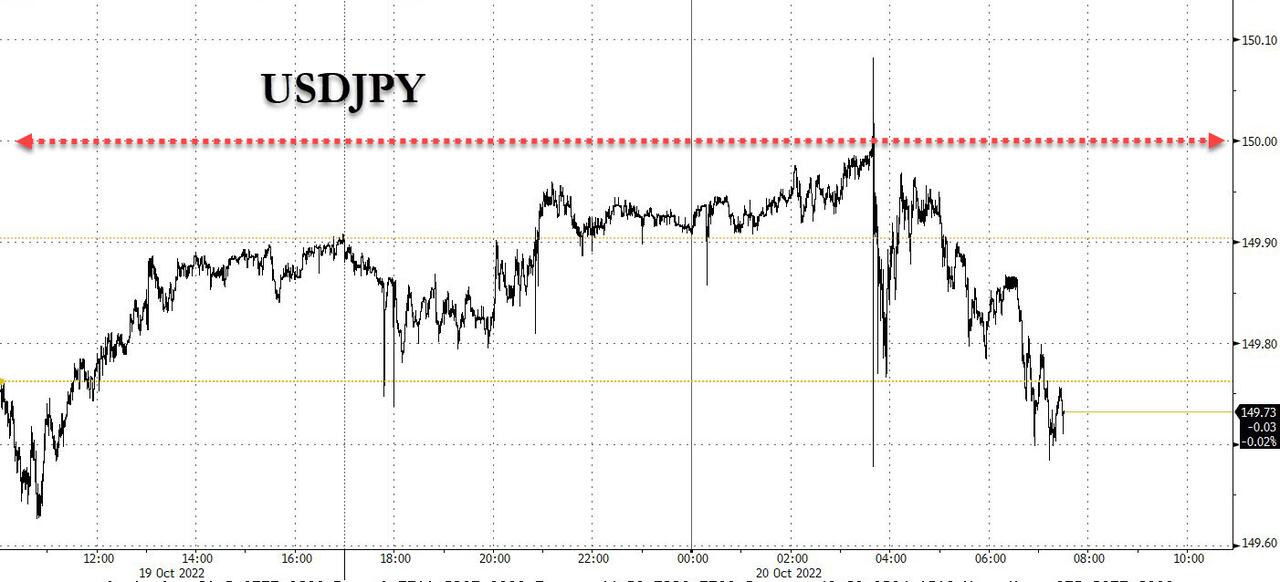

3b Japan 10 YR bond yield: FALLS TO. +.247/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 149.79/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.392%***/Italian 10 Yr bond yield RISES to 4.754%*** /SPAIN 10 YR BOND YIELD RISES TO 3.53%…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 5.024//

3j Gold at $1637.70//silver at: 18.71 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 52/100 roubles/dollar; ROUBLE AT 61.22//

3m oil into the 87 dollar handle for WTI and 93 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 149.79DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 1.0023–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.98365well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.138% UP 1 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 4.148% UP 2 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,57…GETTTING DANGEROUS

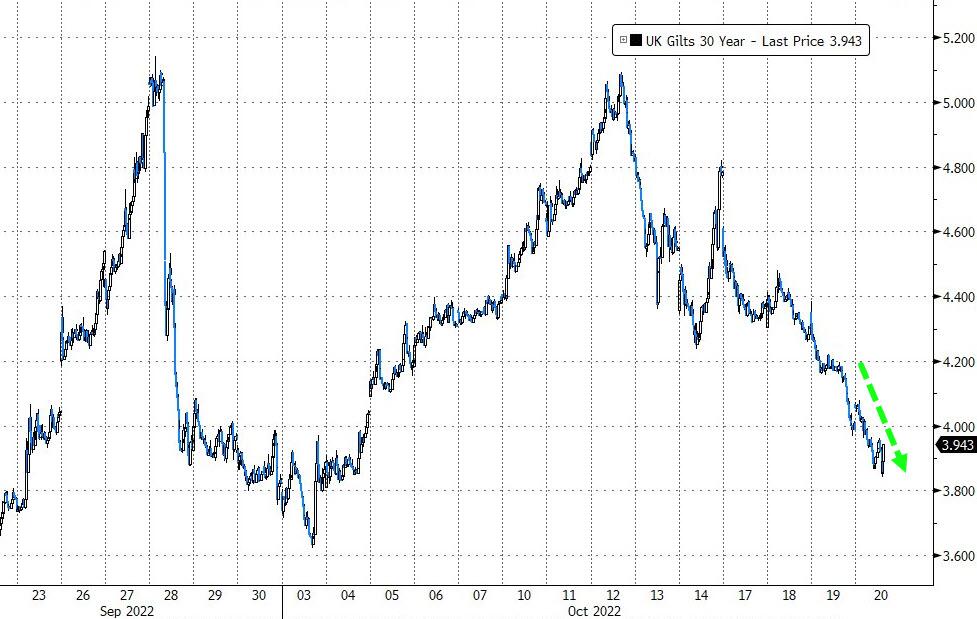

GREAT BRITAIN/10 YEAR YIELD: 3.875%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Green After Bouncing From Session Lows As Overnight Swings Turn Violent

THURSDAY, OCT 20, 2022 – 07:49 AM

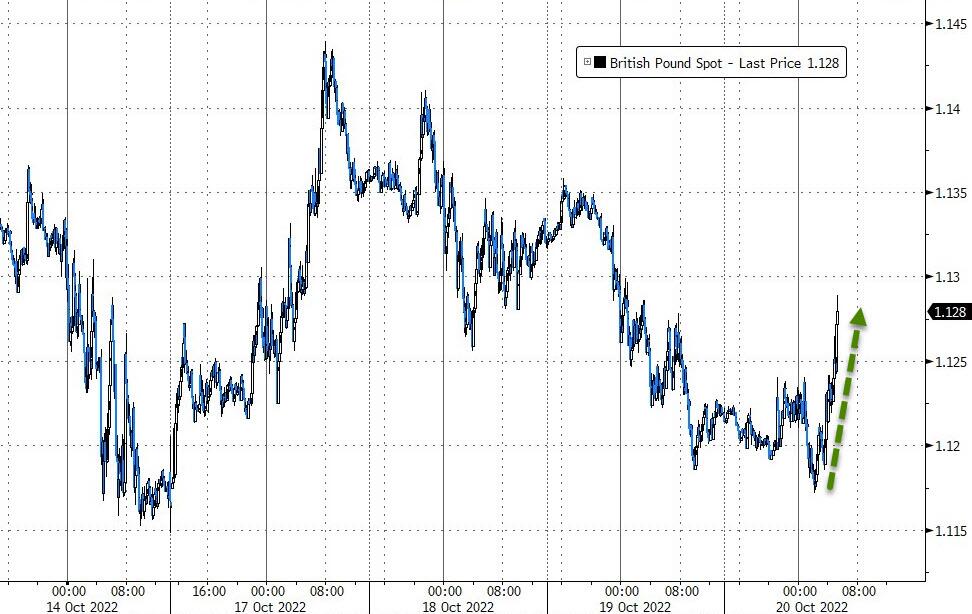

US equity-index futures have swung wildly in the illiquid, overnight session, and after earlier dropping as much as 0.5% following the rapid move higher in US Treasurys and UK gilts, they have since erased all losses to trade near session highs, up 0.3% with Nasdaq futures also up 0.2%, as investors the surge in yields fizzled and as investors assessed disappointing earnings from Tesla against resilient reports from AT&T and IBM. Oil jumped, Chinese stocks spiked (but then fizzled) and both the offshore and onshore yuan rose after a Bloomberg report sparked market optimism that Chinese officials are mulling shortening the amount of time people coming into the country must spend in mandatory quarantine, an implicit tempering of the country’s much maligned coved zero policies. The US dollar slumped as sterling spiked as UK Prime Minister Liz Truss began meetings with a key Conservative party official, stoking speculation that a change in leadership may be afoot. US 10-year yield holds steady at about 4.12%.

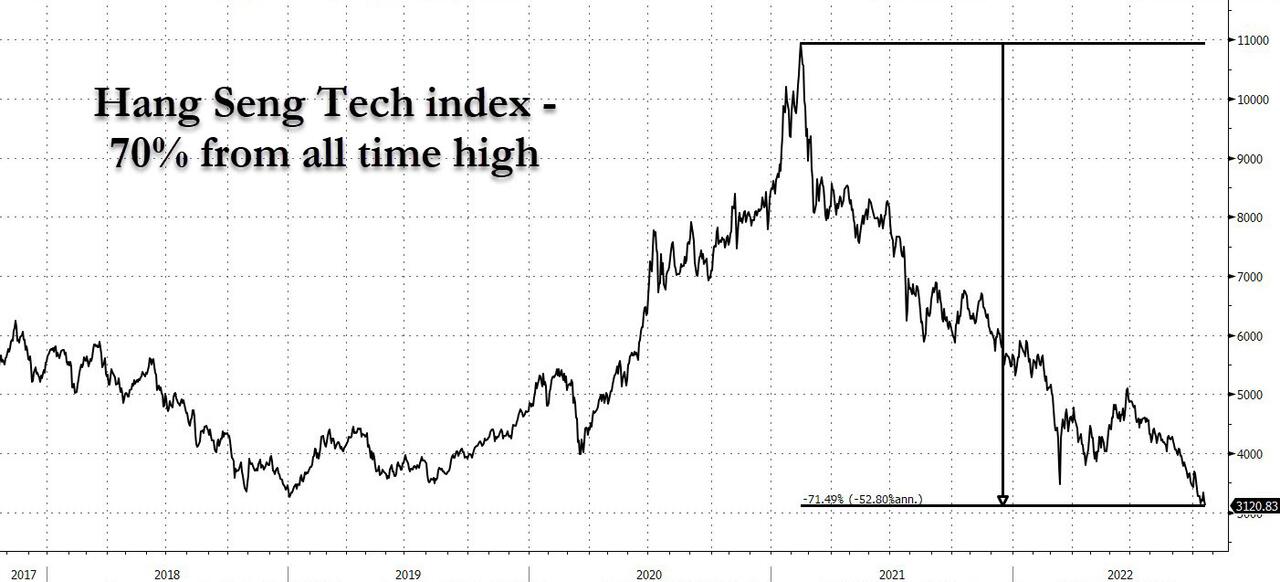

In other notable overnight developments, Hong Kong’s Hang Seng index tumbled to the lowest level since 2009 amid continued liquidations and outflows from China…

… while the yen finally weakened past the closely watched 150 per dollar level, marking a 32-year low and keeping investors on high alert for further intervention to support it. And sure enough, the BOJ promptly jumped in sparking a big move lower in the pair. The move followed a surge in US Treasury yields to multi-year highs that widened the gap with Japanese equivalents.

In premarket trading, bank stocks were mostly higher following their worst day in more than a month. In corporate news, the world’s biggest banks have already had to use about $30 billion of their own cash this year to fund loans for acquisitions and buyouts that they weren’t able to offload to investors. US-listed Chinese stocks bounced in premarket trading, a day after Wednesday’s selloff sent the Nasdaq Golden Dragon China Index down to its lowest closing level since July 2013. The KraneShares CSI China Internet Fund ETF rises 2.1% as of 7:20 a.m. in New York. Here are the other notable premarket movers:

Tesla (TSLA US) falls 5.5% in premarket trading after the world’s most valuable automaker missed third-quarter revenue estimates as it struggled to get its cars to customers. Fellow EV firms lower in premarket trading include: Nikola (NKLA US) -2%, Faraday Future (FFIE US) -2%, Rivian (RIVN US) -1.8%, Canoo (GOEV US) -0.7%

Alcoa (AA US) drops 9.3% in premarket trading after the aluminum giant reported worse-than-expected results for the third quarter, putting pressure on its global peers.

International Business Machines (IBM US) shares rise 3.1% in premarket trading after the IT services company reported third-quarter revenue that beat expectations.

Ally Financial (ALLY US) shares drop 2.5% in premarket trading as Morgan Stanley downgraded the car-finance company to equal-weight from overweight following Wednesday’s third-quarter results.

Sunrun (RUN US) shares slump 4.1% in premarket trading after Wolfe downgrades the stock in a note to peer perform, citing headwinds from a rising interest-rate environment.

Las Vegas Sands (LVS US) shares rise 1% in US premarket trading after posting better- than-expected 3Q adjusted property Ebitda. That was driven by a solid performance in Singapore while uncertainty remains around Macau.

US stocks slipped on Wednesday after a two-day rally saw the S&P 500 reclaim $1.2 trillion in market capitalization amid support from technical levels and optimism about earnings. Higher bond yields and Tesla’s sobering report provided reminders of the tough macroeconomic backdrop as costs for companies remain high and the Federal Reserve pushes forward with interest rate hikes.

“We continue to see plenty of macroeconomic headwinds,” said Marija Veitmane, a senior strategist at State Street Global Markets. “As central banks tighten financial conditions, earnings will crack. So we are very much in the sell-the-rally camp.”

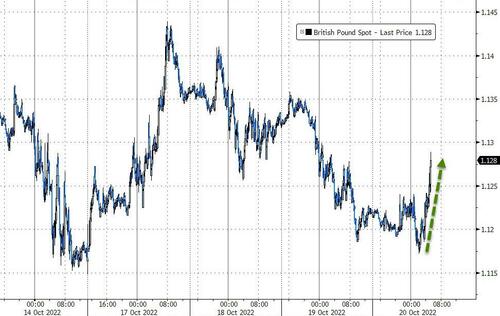

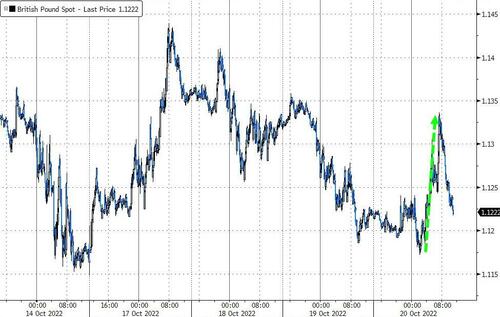

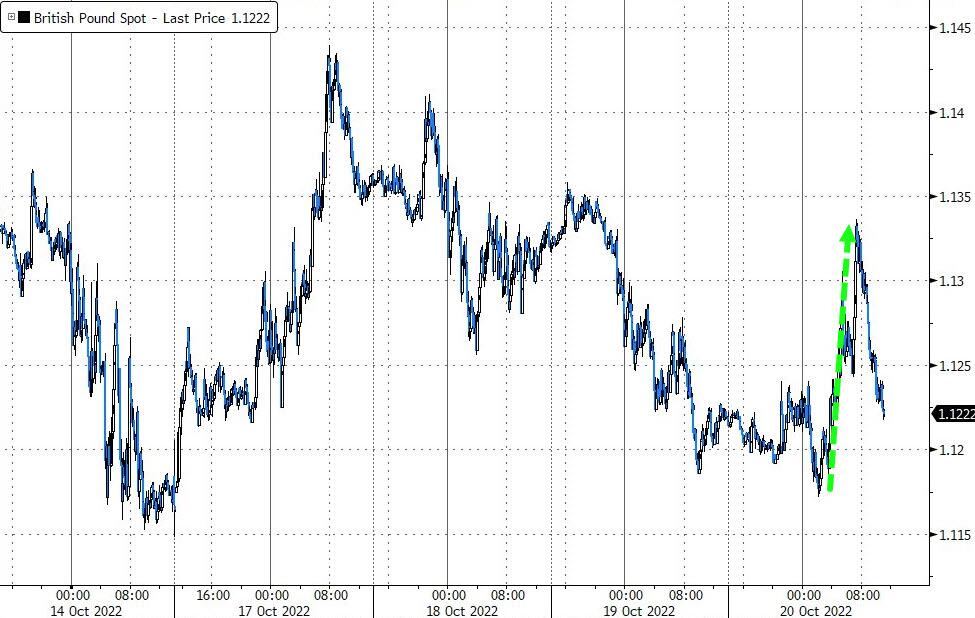

Investors continue to closely monitor events in the UK where Liz Truss’s chaotic premiership looked close to imploding as backbench Conservative lawmakers openly said she should resign and even Cabinet ministers discussed her future. The pound weakened and 10-year UK bond yields climbed, but were off their highs.

A generally strong start to the third-quarter earnings season has bolstered sentiment toward equities. But investors are having to balance signs of corporate resilience against fears about the impact of persistent inflation, hawkish moves by the Federal Reserve and other central banks and threats to the economy. “I think the market now is looking at 2023 and baking some kind of mild downturn into the price,” Hugh Gimber, global market strategist at JPMorgan Asset Management, said on Bloomberg Television. “The key is that inflation number coming down, because if it does, 5% for the Fed looks to me roughly as the right figure and then the market can have a clearer picture.”

In Europe, the Stoxx 50 fell 0.5% with Spain’s IBEX flat but outperforming peers; the DAX lags, retreating 0.8%. Telecoms, financial services and retailers are the worst-performing sectors. Oil and gas shares are the only rising sector in Stoxx Europe 600 index on Thursday as crude extended gains amid a report that China debates easing some Covid restrictions, while European gas advanced after a five-day losing run. The Stoxx Energy sub-index advanced 1.3% as of 10:45 a.m. in London, while the broader equity benchmark declined 0.5%. Here are some of the biggest European movers today:

Oil and gas shares are the only rising sector in Stoxx Europe 600 index on Thursday as crude extended gains amid a report that China is debating easing some Covid restrictions, while European gas advanced after a five-day losing run. BP gained 1.5%, Shell +1.4% and TotalEnergies +1.5%

Saipem soars as much as 13% in Milan, the most intraday since July 14, after winning a $4.5 billion engineering and construction contract from Qatargas. Jefferies upgraded the stock to buy after the “material” award

Yara shares gain as much as 7.2% after fertilizer maker’s 3Q adjusted Ebitda beat analyst estimates and was seen as very strong in an uncertain quarter. Declining gas prices are also pointing toward restarting fertilizer capacity in Europe as demand is rising

Brunello Cucinelli shares soar as much as 11.5%, the most since March, after it delivered a significant beat in its 3Q results as well as a major uptick in FY guidance

Nokia shares fall as much as 6.8% after a mixed set of results, with sales beating consensus estimates while profit and margin lagged. The bottom-line was dragged down by the network equipment maker’s Technologies segment, which continued to be hobbled by a delay in patent contract renewals

Ericsson shares slide as much as 16%, the most since Oct. 2016, after reporting third-quarter operating profit and margin that missed analyst estimates. While the Swedish telecom equipment maker pledges to change pricing and cut costs, analysts still see margin pressure persisting into the next year

Volvo shares fall as much as 5.9% in Stockholm trading, the most intraday since May 2, as analysts highlight that focus for 3Q results is on the weaker Truck division margin, which is driving a miss at Ebit level

GB Group shares plummet as much as 20%, hitting the lowest since September 2017, after identity verification company published a first-half trading update. Davy said the revenue was below consensus expectations

Earlier in the session, Asian equities headed for a second day of declines, as the recent selloff in Hong Kong shares deepened amid investor concerns on China’s zero-Covid approach. The MSCI Asia Pacific Index dropped as much as 1.6%, as tech shares faced fresh losses after bond yields spiked overnight. The gauge pared some of its earlier losses after a report that Chinese authorities were considering a shorter quarantine for inbound travelers. Hong Kong led declines in the region, with its benchmark falling to the lowest since 2009 as Chief Executive John Lee’s maiden policy speech left investors disappointed. Traders remained concerned about consumer demand in China amid lockdowns and rising Covid cases, as well as the spillover into earnings for the region.

“History suggests it is hard for stocks to rally in the face of EPS cuts,” said Stephen Innes, managing partner at SPI Asset Management in a note. “While stock prices should trough before EPS estimates bottom, there is still a lot of wood to chop.” Benchmarks in Taiwan, South Korea and Australia also fell, with the latter extending declines after government data showed that Australian hiring almost stalled in September. Japan’s gauges slid even as the yen weakened past the closely-watched 150 per dollar. Indexes in Indonesia and Malaysia defied the broader gloom to gain more than 1%.

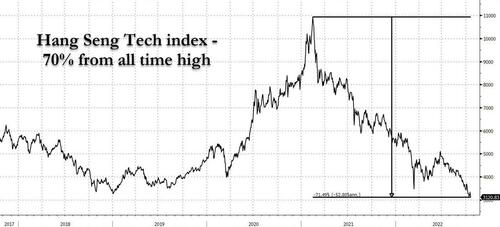

The Hang Seng Tech index has now tumbled more than 70% from its Jan 2021 high.

China’s possible cut in quarantine period for inbound travelers is a small step in the right direction but a lot more is needed to lift investor sentiment dented by the country’s Covid Zero policy. US futures pared losses after the Bloomberg report on the news. The offshore yuan briefly gained as much as 0.5% to 7.2353 against the dollar. According to Amir Anvarzadeh, a strategist at Asymmetric Advisors: “A cut to quarantine rules for inbound travelers will not be enough for the Chinese market to rebound”

Japanese stocks slid as investors refocused on the impact of higher US interest rates and a looming global recession after a two-day rally. The Topix fell 0.5% to close at 1,895.41, while the Nikkei declined 0.9% to 27,006.96. Hoya Corp. contributed the most to the Topix decline, decreasing 3.5%. Out of 2,166 stocks in the index, 596 rose and 1,454 fell, while 116 were unchanged.

Australian stocks declined with global growth fears in focus; the S&P/ASX 200 index fell 1% to 6,730.70, in step with most markets in Asia and on Wall Street amid worries of a global slowdown. Miners contributed the most to the gauge’s retreat as investors weighed quarterly production reports. They also assessed jobs data that suggest the RBA will continue to slow the pace of interest rate increases. In New Zealand, the S&P/NZX 50 index fell 0.8% to 10,832.03.

Key Indian stock gauges gained for a fifth straight day, their longest run of advances in two months, before a key festival next week and as robust corporate earnings boost investor sentiment. The S&P BSE Sensex gained 0.2% to 59,202.90 in Mumbai, while the NSE Nifty 50 Index advanced 0.3%. The indexes overcame decline of as much as 0.5% as weekly derivative contracts expired Thursday. The key benchmarks have risen more than 2% this week and were trading near their highest level since Sept. 21. Twelve of 19 sector sub-gauges compiled by BSE Ltd. advanced, led by oil & gas companies while consumer durables were the worst performers. For the week, information technology stocks are the best performers, helped by stronger-than-expected earnings. Out of 11 Nifty 50 companies, which have so far reported earnings, eight have either met or exceeded average estimates, while three have trailed. Asian Paints’ quarterly results trailed estimates, dragged by weaker revenue growth and rising costs, while Bajaj Finance’s numbers matched consensus

In rates, 10-year TSY yields trade near session lows at around 4.12%, richer by 1bp on the day after earlier rising 5bps to 4.17% while German 10-year yield rises 5.5bps to 2.43%. Treasuries pared losses in the early US session, rising with gilts which stretch to fresh session highs and outperform on the day as Bank of England Deputy Governor Ben Broadbent says UK rates may not rise as much as markets foresee. Gilts outperformed by 4bp while bunds lag Treasuries by 2bp; belly outperformance tightens 2s5s30s fly by 4bp on the day. Dollar issuance slate empty so far and expected to be light; Wednesday saw three borrowers price $6.5b. Three-month dollar Libor +4.70bp at 4.32457%

In FX, the Bloomberg Dollar Spot Index hovered as the greenback traded mixed against its Group-of-10 peers, though most pairs consolidated recent moves. Treasury yields rose by as much as 2bps, led by the short end.

The euro erased a modest loss to near $0.98. Bunds fell for a third session as traders continued to digest Wednesday’s unexpected German Finance Agency decision to increase its own securities holdings for repo purposes, with schatz swap spreads narrowing for a sixth day, the longest streak since December

UK bonds pared an earlier loss and traders cut bets on BOE tightening after Deputy Governor Ben Broadbent said it’s not clear that UK interest rates need to rise as much as the market expects. The pound fell below $1.12 as Liz Truss’s premiership looks close to imploding after she fired one minister over a security breach and two others were heard resigning amid the fallout from a chaotic parliamentary vote before agreeing to stay in their posts

The yen fluctuated in a tight range, and briefly rose above 150 per dollar. Japanese Finance Minister Shunichi Suzuki said excessive and sudden moves in the foreign exchange market triggered by speculation can’t be tolerated. Japan’s benchmark yield climbed above the central bank’s policy ceiling and monetary authorities announced unscheduled bond purchases to rein it back in. Demand for long gamma in dollar-yen gains traction as spot breaches the psychologically-key 150 level

Australia’s dollar slid as much as 0.7% amid a weak jobs print, before reversing following a report that Chinese officials were debating whether to shorten quarantine for inbound travelers. Bonds fell. Australia’s employment rose by just 923 people in September, below the forecast of 25,000, government data showed

In commodities, WTI and Brent December contracts are firmer intraday with the former around USD 86/bbl (84.49-86.27 range) whilst the latter resides around USD 93.50/bbl (91.95-93.92 range). The crude complex is buoyed by the pullback in the Dollar after receiving a boost from source reports that China is considering easing its COVID rules for travellers. Spot gold sees some support from the DXY remaining under 113.00, although remains well off recent highs, with the yellow metal still around the USD 1,630/oz mark (vs yesterday’s 1,654.50/oz high). LME metals are mixed but 3M copper receives a boost from the Buck alongside the aforementioned China source reports, but the red metal remains under USD 7,500/t.

Overall, Bitcoin is contained and essentially unchanged on the session around USD 19.1k with specific updates relatively limited and participants focused on broader market action.

To the day ahead now, and data releases from the US include the weekly initial jobless claims and existing home sales for September, whilst in Germany there’s the PPI reading for September. Central bank speakers include the Fed’s Harker, Jefferson, Cook and Bowman, the ECB’s de Cos and BoE Deputy Governor Broadbent. Earnings releases include Danaher, Philip Morris International, Union Pacific, AT&T and Blackstone. Finally, EU leaders will gather for a summit in Brussels.

Market Snapshot

S&P 500 futures down 0.5% to 3,690.25

MXAP down 0.8% to 136.26

MXAPJ down 0.9% to 440.36

Nikkei down 0.9% to 27,006.96

Topix down 0.5% to 1,895.41

Hang Seng Index down 1.4% to 16,280.22

Shanghai Composite down 0.3% to 3,035.05

Sensex down 0.3% to 58,948.91

Australia S&P/ASX 200 down 1.0% to 6,730.73

Kospi down 0.9% to 2,218.09

STOXX Europe 600 down 0.5% to 395.57

German 10Y yield up 3% to 2.45%

Euro little changed at $0.9777

Brent Futures up 0.9% to $93.26/bbl

Gold spot little changed at $1,630.01

U.S. Dollar Index down -0.1% at 112.86

Top Overnight News from Bloomberg

Giorgia Meloni, the right-wing leader poised to form a new Italian government, said she’d give up on the fledgling coalition if her allies can’t commit to supporting Ukraine along with Italy’s European Union and NATO partners

France’s Economy & Finance minister Bruno Le Maire targets inflation of 4% by the end of 2023, AFP reports, stressing these are “objectives, not forecasts”

Turkey’s central bank is poised to take another step toward cutting interest rates into single digits this year, a gamble masterminded by President Recep Tayyip Erdogan to power economic growth ahead of elections next June

German Chancellor Olaf Scholz warned that a proposal to introduce a European Union-wide cap on gas prices could backfire as the region seeks to offset a drastic supply cut from Russia.

A more detailed look at global markets courtesy of Newquawk

Asia-Pacific stocks were pressured following the weak handover from Wall Street owing to the higher yield environment and as global inflationary headwinds offset the recent earnings momentum. ASX 200 was led lower by the underperformance in tech and following disappointing jobs data, although the energy sector bucked the trend after gains in oil prices and strong quarterly output updates from Woodside Energy and Santos. Nikkei 225 briefly fell beneath 27,000 with participants on intervention watch, while stronger-than-expected Exports and Imports failed to spur risk appetite as the data also contributed to a record trade deficit for the fiscal first half. Hang Seng and Shanghai Comp. declined from the open with the former on course for its lowest close since 2009 amid heavy losses in tech and with the mainland also downbeat after the lack of surprises from the PBoC which maintained its benchmark lending rates unchanged as widely expected, although news of China mulling shortening its quarantine eventually lifted the Shanghai Comp into the green.

Top Asian News

PBoC 1-Year Loan Prime Rate (Oct) 3.65% vs. Exp. 3.65% (Prev. 3.65%); 5-Year Loan Prime Rate (Oct) 4.30% vs. Exp. 4.30% (Prev. 4.30%)

China reportedly held emergency talks with chip firms after US curbs, according to Bloomberg.

China is reportedly mulling cutting inbound quarantine to 7 days from 10 days which will be presented to the top leaders, according to Bloomberg.

Indonesian 7-Day Reverse Repo (Oct) 4.75% vs. Exp. 4.75% (Prev. 3.75%); will intervene in FX to prevent imported inflation.

Japanese Finance Minister Suzuki provides no comment on FX levels; cannot tolerate speculative moves; will take action against any speculative, excessive and sudden moves, via Reuters. Japanese currency diplomat Kanda says excessive and disorderly FX moves have a negative impact on the economy, will not comment on whether Japan is intervening now or has intervened today

European cash bourses trade mixed with the breadth of the market narrow (Euro Stoxx 50 -0.2%; Stoxx 600 -0.4%). Sectors in Europe are mostly negative with no overarching theme – Energy and Banks outperform amid price action in underlying crude and yields respectively. Meanwhile, Telecom names sit at the bottom of the pile as Ericsson (-14%) and Nokia (-5.3%) slide following red flags on margins. US equity futures are softer across the board but to varying degrees, with the NQ (-0.9%) lagging the ES (-0.5%) and RTY (-0.4%), with Tesla carrying a larger weight in the NDX (circa. 4.0%) than the SPX (circa. 1.8%). Tesla Inc (TSLA) – Q3 2022 (USD): Adj. EPS 1.05 (exp. 1.00), Revenue 21.45bln (exp. 21.96bln). Q3 FCF USD 3.30bln (exp. 2.89bln). Q3 Automotive gross margin +27.9% (exp. +28.4%). Tesla sees initial phase of semi deliveries begin in December 2022. Tesla still sees 50% avg. annual growth in vehicle deliveries. Raw material cost inflation impacted quarterly profitability along with ramp inefficiencies from Gigafactory Berlin-Brandenburg, Gigafactory Texas, 4680 cell production. Battery supply constraints will be main limiting factor. CEO Musk said looking forward to a record-breaking Q4 and the Co. is gaining rapid traction in 4680 cell production. -5.0% in the pre-market

Top European News

BoE’s Broadbent says the MPC is likely to respond relatively promptly to news about fiscal policy. Remains to be seen if rates need to rise as much as currently priced in by markets, via BoE. The justification for tighter policy is clear. If government support mitigates the effect of import costs, there is more at the margin for monetary policy to do. If Bank Rate really were to reach 5.25%, the cumulative impact on GDP of the entire hiking cycle would be just under 5% – of which only around one quarter has already come through

UK Tory 1922 Committee officers are expected to meet on Thursday to discuss the leadership crisis in the Tory party, according to The Telegraph’s Editor. However, recent reporting indicates the Committee will not be meeting today.

UK PM Truss’s office noted that the Tory party’s chief whip and deputy chief whip remain in their posts.

ITV’s Peston, citing a member of UK Cabinet, that it is clear there is a will among ministers to attempt to keep PM Truss in office until October 31st (when the budget will be announced). A view that contrasts the recent update from ITV’s Brand, citing a 1922 member, that the “odds are against” PM Truss surviving the day as PM

FX

Pound precarious as pressure continues to build against UK PM Truss and BoE’s Broadbent infers that market expectations on rates may be too hawkish, Cable pivots 1.1200

Yen slips under 150.00 mark vs Dollar as yields continue to rally, but rebounds amidst further Japanese verbal, if not actual intervention

Franc remains on the backfoot due to as a funding currency, but Euro gleans traction from data and EGB/UST spread convergence, USD/CHF straddles 1.0050 and EUR/USD bounces ahead of 0.9750 to reclaim 10 and 21 DMAs

Aussie labours after payrolls miss consensus by some distance and before recovery in tandem with Yuan on reports that China may relax some Covid rules for inbound travellers, AUD/USD eyes 0.6300 from sub-0.6250 and USD/CNH off peaks near 7.2800

Riksbank’s Ingves, to Swedish parliament, says easing mortgage repayment rules would be inappropriate.

RBI is continuing spot USD sales and receiving December forwards, according to traders cited by Reuters.

Fixed Income

Debt remains depressed though notably off worst levels after dovish remarks from BoE’s Broadbent lifted Gilts to the mid-98.00 region.

In turn, both USTs and Bunds have climbed off lows of 109.19+ and 134.86 respectively, though still post downside of circa. 3 and 50 ticks respectively.

The complex looks to US data and Fed speak while BTPs await updates out of Italy as potential PM Meloni is set to begin constructing her cabinet, with particular focus on the Berlusconi’s Foreign Minister nominee.

Commodities

WTI and Brent December contracts are firmer intraday with the former around USD 86/bbl (84.49-86.27 range) whilst the latter resides around USD 93.50/bbl (91.95-93.92 range).

The crude complex is buoyed by the pullback in the Dollar after receiving a boost from source reports that China is considering easing its COVID rules for travellers.

Spot gold sees some support from the DXY remaining under 113.00, although remains well off recent highs, with the yellow metal still around the USD 1,630/oz mark (vs yesterday’s 1,654.50/oz high).

LME metals are mixed but 3M copper receives a boost from the Buck alongside the aforementioned China source reports, but the red metal remains under USD 7,500/t.

MMG’s (1208 HK) Las Bambas copper mine in Peru reportedly halted copper transportation due to protests.