n Uncategorized · Leave a comment·Edit

by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSE: DOWN $7.40 to $1650.85

SILVER PRICE CLOSE: DOWN $0.05 to $18,68

Access prices: closes

Gold ACCESS CLOSE 1651.50

Silver ACCESS CLOSE: 18.72

New: early yesterday morning//

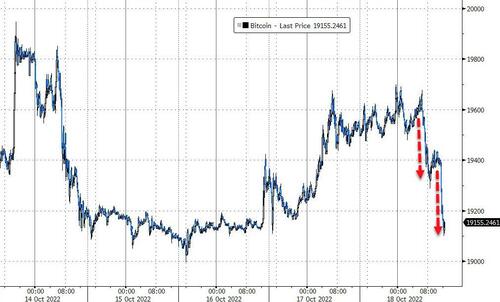

Bitcoin morning price: $19,566 UP 24

Bitcoin: afternoon price: $19,185 DOWN 357.

Platinum price closing DOWN $6.80 AT $912.85

Palladium price; closing UP $9.25 at $2016.20

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD $2268.80 CDN DOLLARS PER OZ UP $3.68 CDN DOLLARS

BRITISH GOLD IN POUNDS: 1457.60 POUNDS PER OZ UP 5.13 BRITISH POUNDS PER OZ/

EURO GOLD: 1675.00 EUROS PER OZ// DOWN 1.78 EUROS PER OZ///

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: OCTOBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,657.000000000 USD

INTENT DATE: 10/17/2022 DELIVERY DATE: 10/19/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 54

323 C HSBC 47

657 C MORGAN STANLEY 4

905 C ADM 3

TOTAL: 54 54

MONTH TO DATE: 22,259

JPMORGAN STOPPED 0/54

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 54 NOTICES FOR 5400 OZ or 0.1617 TONNES

total notices so far: 22,259 contracts for 2,225,900 oz (69.235 tonnes)

SILVER NOTICES: 2 NOTICE(S) FILED FOR 10,000 OZ/

total number of notices filed so far this month 439 : for 2,145,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $7.40

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////A WITHDRAWAL OF 2.03 TONNES INTO THE GLD//

INVENTORY RESTS AT 939.10 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 5 CENTS

AT THE SLV// :/BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A HUGE DEPOSIT OF 1.658 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 487.729 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1021 CONTRACTS TO 135,304 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE GIGANTIC GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.53 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS/HFT WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.53)., BUT UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS. HUGE NUMBERS OF SPECS CONTINUE TO ADD TO THEIR SHORTFALLS FROM WHICH OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS.

WE MUST HAVE HAD:

I) STRONG SPECULATOR SHORT COVERINGS ////CONTINUED BANKER OI COMEX ADDITIONS /// CONSIDERABLE NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING A 415,000 OZ QUEUE JUMP / // V) GIGANTIC SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: +12

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 14 days, total 54,197 contracts: 27.0985 million oz OR 1.935MILLION OZ PER DAY. (387 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 27 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 27.0985 MILLION OZ INITIAL

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1021 DESPITE OUR HUGE $0.53 GAIN IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 950 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /STRONG BANKER ADDITIONS // STRONG SHORT ADDITIONS//CONSIDERABLE NEWBIE SPEC LONG ADDITIONS// /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S 415,000 QUEUE JUMP .. WE HAD A SMALL SIZED LOSS OF 71 OI CONTRACTS ON THE TWO EXCHANGES FOR 0.355 MILLION OZ..

WE HAD 2 NOTICE(S) FILED TODAY FOR 10,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 4392 CONTRACTS TO 432,976 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED — -213 CONTRACTS.

.

THE GOOD SIZED INCREASE IN COMEX OI CAME DESPITE OUR GAIN IN PRICE OF $14.55//COMEX GOLD TRADING/MONDAY // CONSIDERABLE SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE. JUMP OF 12,200 OZ//NEW STANDING 71.284TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $14.55 WITH RESPECT TO MONDAY’S TRADING

WE HAD A SMALL SIZED LOSS OF 4638 OI CONTRACTS 5.095 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2754 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 432,976

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1638 CONTRACTS WITH 4392 CONTRACTS DECREASED AT THE COMEX AND 2754 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1638 CONTRACTS OR 5.095 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2754) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (4392): TOTAL LOSS IN THE TWO EXCHANGES 1425 CONTRACTS. WE NO DOUBT HAD 1) CONSIDERABLE SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS/// STRONG NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 12,200 OZ QUEUE. JUMP ///NEW STANDING 71.284 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) GOOD SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

33,111 CONTRACTS OR 3,311,100 OZ OR 102.989 TONNES 14 TRADING DAY(S) AND THUS AVERAGING: 2365 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAY(S) IN TONNES: 102.989 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 102.989/3550 x 100% TONNES 2.90% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 102.989 TONNES INITIAL ( MUCH SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GIGANTIC SIZED 1021 CONTRACT OI TO 135,304 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 950 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 950 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 950 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 10321 CONTRACTS AND ADD TO THE 950 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED LOSS OF 71 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 0.355 MILLION OZ//

OCCURRED DESPITE OUR GAIN IN PRICE OF $0.53

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED DOWN 3.98 PTS OR 0.13% //Hang Seng CLOSED UP 301.68 OR 1.82% /The Nikkei closed UP 380.35PTS OR 1.42% //Australia’s all ordinaires CLOSED UP 1.78% /Chinese yuan (ONSHORE) closed UP TO 7.1994 //OFFSHORE CHINESE YUAN UP 7.20985// /Oil DOWN TO 85.56 dollars per barrel for WTI and BRENT AT 91.55 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 4392 CONTRACTS TO 432,976 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS GOOD COMEX DECREASE OCCURRED DESPITE OUR RISE IN PRICE OF $14.55 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2754 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2754 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 2754 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2754 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 1638 CONTRACTS IN THAT 2754 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI LOSS OF 4392 CONTRACTS..AND THIS FAIR SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR RISE IN PRICE OF GOLD $14.55//WE HAD SPEC SHORTS COVERING SOME OF THEIR POSITIONS WITH BANKERS ALSO AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD SOME ADDITIONAL NEWBIE SPECS GOING CASHING OUT FOR SOME PROFITS ON THE RISE IN PRICE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (71.284),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 71.284 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $14.55) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS (THEY ADDED TO THEIR POSITIONS) AS WE HAD A FAIR SIZED TOTAL LOSS ON OUR TWO EXCHANGES OF 1638 CONTRACTS // WE HAVE REGISTERED A SMALL LOSS OF 5.095 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (71.284 TONNES)…THIS WAS ACCOMPLISHED WITH A RISE IN PRICE OF $14.55

WE HAD -213 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 1638 CONTRACTS OR 163,800 OZ OR 5.095 TONNES

Estimated gold volume 156,925// poor//

final gold volumes/yesterday 153,085/ poor

INITIAL STANDINGS FOR OCT ’22 COMEX GOLD //OCT 18

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 739.46oz Brinks 23 kilobars |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 1101.154 oz Brinks |

| No of oz served (contracts) today | 54 notice(s) 5400 OZ 0.1679 TONNES |

| No of oz to be served (notices) | 659 contracts 65,900oz 2.049 TONNES |

| Total monthly oz gold served (contracts) so far this month | 22,259 notices 2,225,900 69.235 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals:1

i) Out of Brinks 739.46 oz (23 kilobars)

total: 739.46 oz

total in tonnes: 0.022 tonnes

Adjustments: 4// all dealer to customer

i)HSBC 29,305.136 oz

ii) JPMorgan 65,360.482 oz

iii) Manfra 35,687,610 oz

iv) Brinks 15,461.975 oz

total: 145,815.197 oz moved out of registered to eligible//used for deliveries

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 713 contracts having GAINED 122 contracts . We had 0 contracts

filed on MONDAY, so we GAINED A STRONG 122 contracts or an additional 12,200 oz will stand in this active delivery month of Oct. From this point

we should gain in total gold standing through to the end of Oct.( This is queue jumping and in reality it is the exercising of London based EFP;s for gold at the comex)

November GAINED 182 contracts to stand at 3304

December LOST 4631 contracts up to 357,355

We had54 notice(s) filed today for 5400 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 54 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (22,259) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 713 CONTRACTS) minus the number of notices served upon today 54 x 100 oz per contract equals 2,281,300 OZ OR 71.284 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (22,259) x 100 oz+ (713) OI for the front month minus the number of notices served upon today (54} x 100 oz} which equals 2,281,300 oz standing OR 71.284 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 71.824 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,968,238.247 OZ 61.220 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 25,727,917.721 OZ

TOTAL REGISTERED GOLD: 12,013,196.538 OZ (373.66 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 13,714,721.153 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,044,998 OZ (REG GOLD- PLEDGED GOLD) 312.44 tonnes//rapidly declining

END

SILVER/COMEX

OCT 18//INITIAL OCT SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,212,930.150oz Brinks CNT Loomis HSBC Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 957,251.160 oz CNT HSBC JPM Manfra |

| No of oz served today (contracts) | 2 CONTRACT(S) (10,000 OZ) |

| No of oz to be served (notices) | 235 contracts (1,175,000 oz) |

| Total monthly oz silver served (contracts) | 429 contracts 2,145,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 4 withdrawals out of the customer account

i) out of CNT 4811.612 oz

ii) out of HSBC: 14,601.150 oz

iii) Out of Brinks: 1,173,830.850 oz

iv) Out of Loomis: 9599.140 oz

v) Out of Manfra 10,087.400

Total withdrawals: 1,212,930.152 oz

JPMorgan has a total silver weight: 161.106million oz/307.169million =52.44% of comex

Comex deposits: 0

total withdrawals: nil oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 38.779 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 307.169 MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF OCT OI: 237 CONTRACTS HAVING GAINED 74 CONTRACT(S.)

WE HAD 9 NOTICES FILED ON MONDAY SO WE GAINED 83

SILVER CONTRACTS OR AN ADDITIONAL 415,000 OZ WILL STAND FOR OCT.

NOVEMBER LOST 39 CONTRACTS TO STAND AT 359

DECEMBER SAW A LOSS OF 1348 CONTRACTS DOWN TO 109,616

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 2 for 10,000 oz

Comex volumes:39,674// est. volume today// poor

Comex volume: confirmed yesterday: 54,334 contracts ( poor)

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 429 x 5,000 oz = 2,145,000 oz

to which we add the difference between the open interest for the front month of OCT(237) and the number of notices served upon today 2 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 429 (notices served so far) x 5000 oz + OI for front month of OCT (237) – number of notices served upon today (2) x 5000 oz of silver standing for the OCT contract month equates 3,320,000,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:56,736// est. volume today// poor

Comex volume: confirmed yesterday: 64,896 contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

GLD INVENTORY: 939.10 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLIONOZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

CLOSING INVENTORY 487.729 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

Atlanta Fed President……a crook

(Pam and Russ Martens)

Pam and Russ Martens: Atlanta Fed president hid his trades as Fed rescued Wall Street

Submitted by admin on Mon, 2022-10-17 11:09Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Monday, October 17, 2022

It was one year ago that Wall Street On Parade raised a multitude of red flags about Raphael Bostic, the president of the Federal Reserve Bank of Atlanta. We have published the entirety of that article below so that our readers can see just how long it took both Bostic and the Atlanta Fed to come clean with the American people about his trading on Wall Street.

On Friday, Bostic released a seven-page statement in which he owned up to the following: failing to list a multitude of trades that were conducted on his behalf by trading firms on Wall Street over a period of five years; failing to properly report income on his assets on his financial disclosure forms; trading during blackout periods when trading was barred by the Federal Reserve; and providing inaccurate values on his financial disclosure forms. The upshot was that Bostic had to restate his financial disclosure forms for the entire five-year period he has filed them at the Atlanta Fed, 2017 through 2022

If a publicly-traded company had to restate its earnings and admit that it had lied to the American people for five straight years, you can bet that the CEO and CFO would be fired in short order by the Board of Directors. But the Board of the Atlanta Fed is sticking with Bostic — at least for now. …

… For the remainder of the analysis:

END

3.Chris Powell of GATA provides to us very important physical commentaries

For your interest…

World Gold Council has plan to dematerialize gold market even more

Submitted by admin on Sun, 2022-10-16 12:11Section: Daily Dispatches

A Digital Drive to Reform the $11 Trillion Global Gold Market

By Eddie Spence and Ranjeetha Pakiam

Bloomberg News

Sunday, October 16, 2022

Trading on one of the world’s oldest markets depends on a network of high-security vaults located underneath Greater London. There, some 50,000 gold bars, each worth more than $650,000, change hands every day among the four big banks in charge of processing transactions.

The system, which includes some $500 billion worth of gold stored in locations, has been trundling along with little change for most of the past two decades. David Tait, who heads the World Gold Council, the main lobby group for miners of the metal, thinks it’s time for an overhaul.

The former investment banker is trying to push through changes he hopes will significantly increase demand, including a database using blockchain technology to keep track of almost every gold bar in the world. Once that’s up and running, he says, it should be possible to create a digital token backed by physical gold that can be more easily traded.

Market players gathering for a conference on Oct. 16 are skeptical the proposed overhaul will get off the ground, because previous attempts to make even small changes to the market have fallen flat. But the package of changes, dubbed Gold 247 (for 24/7), has taken on fresh urgency. Post-financial crisis banking reforms began to affect gold this year after market participants were unable to prove that the asset could easily be traded in stressful times.

The new rules, in effect, made it more expensive for banks to hold bullion, compressing the already meager returns they make trading the commodity, and raising concerns the market will shrink. And in the past decade, gold has faced growing competition from cryptocurrencies for the attention of investors looking for alternatives to stocks, bonds, and cash—with some boosters even calling Bitcoin “digital gold.” …

… For the remainder of the report:

END

Why is this a surprise? G7 fail to reach an intervention deal to ease the pain on emerging and other markets on the soaring dollar

(Reuters/Kihara)

G7 fails to reach intervention deal to ease pain of soaring dollar

Submitted by admin on Sun, 2022-10-16 20:56Section: Daily Dispatches

By Leika Kihara

Reuters

Sunday, October 16, 2022

WASHINGTON — Japan and other countries facing the fallout from a soaring U.S. dollar found little comfort from last week’s meetings of global finance officials, with no sign that joint intervention along the lines of the 1985 “Plaza Accord” was on the horizon.

With a strong push from Japan, finance leaders of the Group of Seven advanced economies included a phrase in a statement on Wednesday saying they will closely monitor “recent volatility” in markets.

But the warning, as well as Japanese Finance Minister Shunichi Suzuki’s threat of another yen-buying intervention, failed to prevent the currency from sliding to fresh 32-year lows against the dollar as the week came to a close.

While Suzuki may have found allies grumbling over the fallout from the U.S. central bank’s aggressive interest rate hike path, he conceded that no plan for a coordinated intervention was in the works. …

… For the remainder of the report:

END

Chinese state banks intervene trying to stem the fall of the renminbi (yuan) by selling dollars

(London’s Financial Times/Lockett)

China state banks step up dollar sales to support renminbi

Submitted by admin on Mon, 2022-10-17 10:58Section: Daily Dispatches

By Hudson Lockett

Financial Times, London

Monday, October 17, 2022

China’s state banks stepped up selling of the dollar today, supporting the renminbi against the surging U.S. currency as the Chinese Communist Party’s 20th congress got under way in Beijing.

Traders in China said large state-run banks were swapping renminbi for U.S. dollars in the country’s forwards market, then selling the dollars in the country’s onshore markets in an intervention to bolster the domestic currency.

The renminbi was trading 0.2% lower against the dollar at about Rmb7.2. But the Chinese currency has fallen almost 12% against the dollar this year, with weakness becoming more pronounced after regulators relaxed informal foreign exchange trading limits in late September.

That move was followed by warnings from authorities discouraging bets on sharper falls to avoid runaway depreciation — part of an effort to slow the pace of depreciation rather than mount a strong defence of any specific level for the renminbi’s dollar exchange rate.

“This kind of intervention won’t usually have too big of an impact in the long term, but it will have an immediate, short-term impact,” said one Shanghai-based foreign exchange trader with a western investment bank. …

… For the remainder of the report:

https://www.ft.com/content/b4a75f35-ccf1-4bec-8596-f3ed4ec6de6

end

4. OTHER PHYSICAL SILVER/GOLD

Turkey bought 3.9 tonnes of gold into the country last month as citizens knew that their currency, the lira was worthless.

special thanks to Milan S for providing this for us;

Report: Turkey’s September Gold Imports up by 1,700% as Individuals Swap Falling Lira With the Precious Metal

Turkey’s gold imports of just over 39,000 kilograms in September 2022 are more than 16 times the quantity that was brought into the country in September 2021. The surge in Turkey’s gold imports is reportedly being spurred by the rise in demand for the precious metal by individuals and entities using it in foreign currency transactions.

‘Gold Instead of Turkish Lira’

According to data from Borsa Istanbul’s Precious Metals and Diamond Markets, the quantity of gold imported into inflation-stricken Turkey in September 2022 was over 1,700% more than the quantity brought into the country during the same period last year.

The country’s September haul of 39,000 kilograms (kg) takes the total quantity of the precious metal imported by Turks in 2022 to 140,126 kg. As noted in a report published by the Hurriyet Daily News, Turkey’s January 2010 import figure of 44,210 kg remains the country’s largest.

Explaining why Turkey is seeing a surge in the quantity of gold brought into the country, Tuna Çetinkaya, the deputy general manager at Info Investment, reportedly linked the surge in demand to identity requirements for buying forex. He said:

This regulation led people or entities with large FX [foreign exchange] demand to use gold instead of Turkish Liras in foreign currency transactions.

The Lira’s Depreciation

Since January 2020, when its official exchange rate stood at just under 5.50 lira for every dollar, the Turkish currency has depreciated by over 300%. At the time of writing, one dollar buys 18.58 lira. The currency’s depreciation, together with the surging inflation rate, which stood at 83.45% in September 2022, is forcing Turks to demand alternative stores of value.

In addition to gold, Turks also imported large quantities of silver during the same period — just over 68,000 kg. The latest figure is nearly double the 36,417 kg imported in September 2021. Besides demanding precious metals, Turks also use digital currencies like bitcoin and the stablecoin tether.

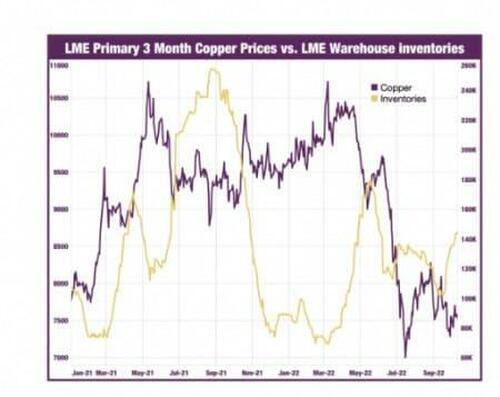

5.OTHER COMMODITIES: COPPER

They say that Copper holds a PhD in Economics. As the economy flourishes so does copper

Here is an in depth look at copper this year.

Miner/OilPrice.com

Copper Remains Range-Bound As Bears And Bulls Duke It Out

TUESDAY, OCT 18, 2022 – 03:30 AM

By Ag Metal Miner via OilPrice.com

The October Copper Monthly Metals Index (MMI) fell 5.59% from September to October, with all components experiencing declines. Still, future copper prices face a wide range of challenges.

Copper prices continue to show signs of short-term consolidation following a brief rebound that stalled in late August. Meanwhile, the bottom found in mid-July and the peak of the subsequent rebound created a short-term trading range for the current sideways trend.

Fed Remains Hawkish, Splits on Rate Hike Pace

Accumulating rate hikes from the Federal Reserve and central banks worldwide added significant weight to copper prices over the past few months. The Fed, in particular, has increased interest rates at the steepest pace in modern history. In September, it issued its third consecutive 75 basis point hike. Even so, Fed officials showed no hesitation in continuing the approach until prices stabilize. That said, officials have started to split on whether to continue on pace or shift to a softer trajectory.

For one, the collective impact of global rate hikes will prove a substantial drag on demand and, therefore, inflation. Indeed, two officials recently voiced the need for restraint going forward. In their opinion, the effect of the Fed’s efforts to date may simply be slow to materialize. In an early October speech, Fed Vice Chairwoman Lael Brainard noted, “it will take time for the cumulative effect of tighter monetary policy to work through the economy and to bring inflation down.” She continued, “the moderation in demand due to monetary-policy tightening is only partly realized so far.”

Experts on The Fence Over the Federal Reserve’s Actions

Mirroring Brainard’s comments, Chicago Fed President Charles Evans warned of the risks associated with “overshooting” the Fed’s goal. Evans noted that between limited inflation reports and the Fed’s actions to date, “puts us at somewhat greater risk of responding overly aggressive.”

Other officials appear far less concerned about the Fed’s aggressive tactics. In response to the current level of inflation, Governor Christopher Waller commented, “this is not the inflation outcome I am looking for to support a slower pace of rate hikes or a lower terminal policy rate.” Beyond that, a still robust labor market will likely outweigh the concerns of more cautious officials. Although growth eased from the previous month, the Labor Department reported that the U.S. added 263,000 jobs in September. This total proved larger than expected, contradicting the Fed’s goal to cool labor demand.

Supply Constraints, Chinese Demand Add Counterweight

As the Fed pressures demand, several factors have added a bullish counterweight. For one, Chinese copper demand remains strong, holding copper prices up. In fact, refined copper imports through August saw a 9.8% year-over-year rise. This is primarily due to heavy increases throughout the summer months. Meanwhile, infrastructure spending, specifically on renewable energy projects, helped lift demand after the Q1 slump.

Secondly, copper production in South America remains pressured. For example, Peruvian copper production fell 1.5% in August, according to the Ministry of Energy and Mines (MINEM). Meanwhile, production in Chile fell even more drastically. According to Cochilco, total Chilean output in August dropped 10.2% from 2021. Both Peru and Chile have faced numerous mining disruptions throughout the year, including protests and reduced mining activity.

LME Actions Could Impact Copper Prices

Copper deliveries face new and potential restrictions from the LME. Indeed, the most recent announcement added significant upward pressure to copper prices. First, the LME announced the immediate restriction of new metal (including copper) from Russia’s Ural Mining & Metallurgical (UMMC). Therefore, any new material delivered to the LME must be proven not to breach the UK’s sanctions against the company’s co-founder, Iskandar Makhmudov.

Separately, the LME requested member input regarding a total ban on Russian metal. The statement noted, “the LME believes it is appropriate, in the absence of general sanctions against Russian metal brands, to seek market views on the expected accessibility of Russian metal in 2023.” While these actions could challenge historically low warehouse inventories, stocks have nonetheless continued to grow since early September. Beyond that, inventory levels do not necessarily impact copper prices. As of 2011, the two continue to display a low inverse correlation of just 17%.

Overall Impacts on Copper Prices

For copper prices, widespread monetary tightening will continue to squeeze long-term demand. Despite the internal division, the Federal Reserve continues to dampen any hopes of a dovish pivot. Indeed, so far, no officials have gone on record to call for a rate hike pause. At this point, most investors expect another 75 basis point rate hike come November.

For now, supply-side constraints and strong Chinese demand have proven enough to halt the macro downtrend. Current copper prices appear resistant to creating either a higher high or lower low. Instead, they continue to move sideways within a tight range.

end

COMMODITIES IN GENERAL/

END

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 7.1993

OFFSHORE YUAN: 7.2085

SHANGHAI CLOSED DOWN 3.98 PTS OR 0.13%

HANG SENG CLOSED UP 301.68 OR 1.82%

2. Nikkei closed UP 301.68 PTS OR 1.82%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 112.13/Euro FALLS TO 0.98339

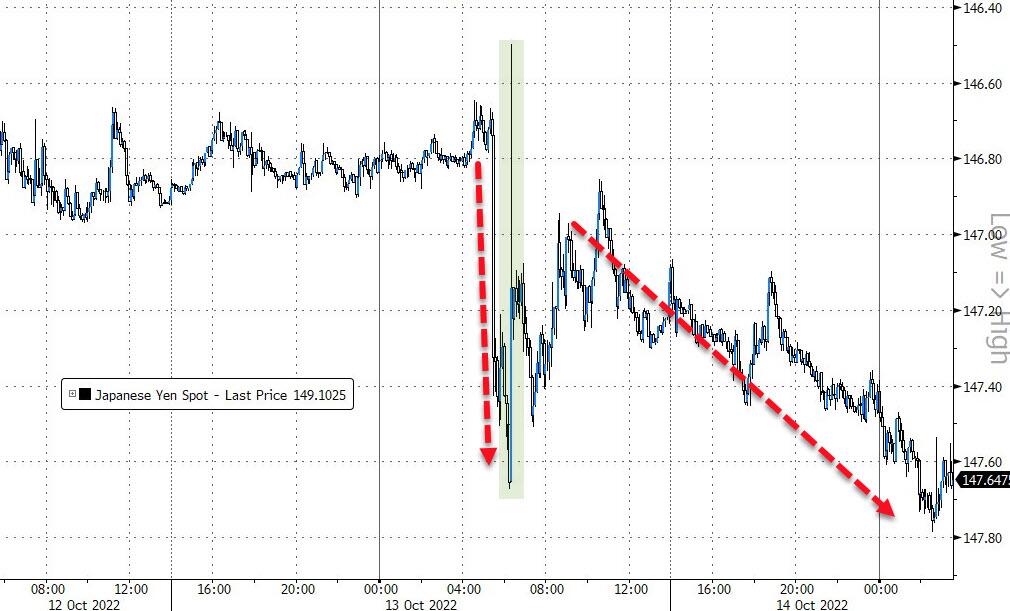

3b Japan 10 YR bond yield: RISES TO. +.249/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 149.10/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: UP -// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.252%***/Italian 10 Yr bond yield RISES to 4.698%*** /SPAIN 10 YR BOND YIELD RISES TO 3.429%…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.966//

3j Gold at $1652.85//silver at: 18.79 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 15/100 roubles/dollar; ROUBLE AT 61.69//

3m oil into the 85 dollar handle for WTI and 91 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 149.10DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 1.0022– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9757well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

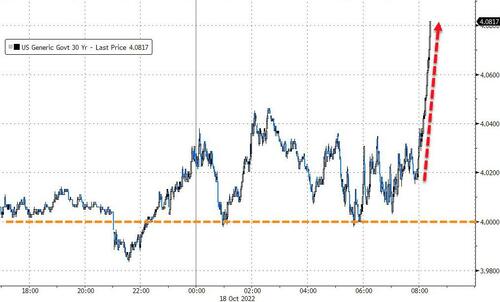

USA 10 YR BOND YIELD: 3.998% DOWN 2 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 4.030% UP 2 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

USA DOLLAR VS TURKISH LIRA: 18,59…GETTTING DANGEROUS

GREAT BRITAIN/10 YEAR YIELD: 4.05%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

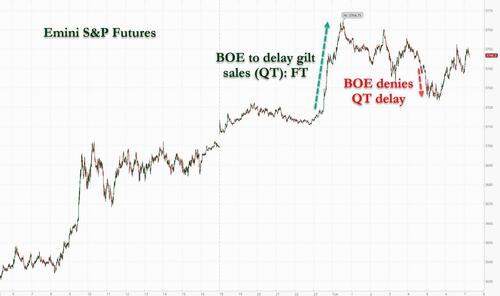

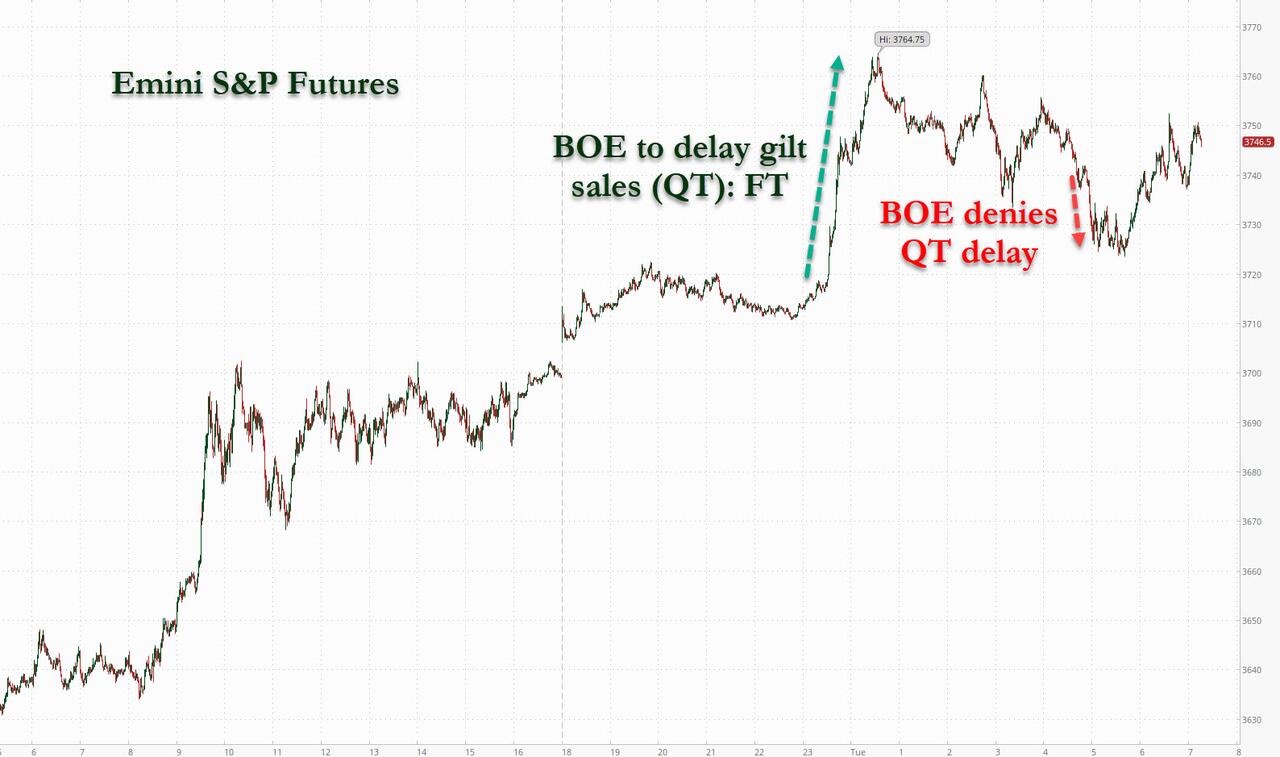

Futures Soar Despite Latest UK Newsflow Rollercoaster Fiasco

TUESDAY, OCT 18, 2022 – 08:00 AM

It was another overnight emotional and markets rollercoaster session thanks to the constant chaos of newsflow and confusion out of the UK.

Just around midnight ET, the Financial Times reported that the Bank of England would delay the start of its gilt-sale program (i.e. Q.T.), sending UK gilts, sterling and US equity futures sharply higher. Those gains, however, turned to losses when the central bank denied the report in a statement just around 5am ET, pushing the yield on the UK 10-year bond seven basis points higher to 4.05% while cable dumped 0.5%. That said, the BOE didn’t rule out the prospect of the BOE announcing a delay at a later time. The central bank has already delayed the start of the sales once, during the fallout from the government’s fiscal plan last month

Despite the reversal by the BOE, the huge meltup which we said would be triggered on Monday by Friday’s massive shorting, extended for a second day, encouraged by the reversal of uber-bear Michael Wilson who as we noted yesterday, expects a bear market rally pushing the S&P as high as 4,150, and helping the S&P to close above a key technical level on Monday. Nasdaq 100 futures rose 1.8%, while S&P 500 futures advanced 1.6% at 7:30 a.m. in New York, as tech giants Amazon and Microsoft led major technology and internet stocks higher in premarket trading, while the 10-year Treasury yield holds steady at about 4% and the Bloomberg dollar index was flat.

In premarket trading, bank stocks traded higher as Goldman Sachs becomes the last of the big six US lenders to report earnings this quarter, beating on the top and bottom line (a more detailed report to follow). In corporate news, Credit Suisse is exploring a sale of its US asset-management operations and moving closer to securing financing for other businesses. Amazon and Microsoft lead major US technology and internet stocks higher in premarket trading, set to extend their gains for a second straight session. Nvidia (NVDA US) +2.7%, Amazon (AMZN US) +2.3%, Alphabet (GOOGL US) +2%, Meta (META US) +2%, Apple (AAPL US) +1.7% and Microsoft (MSFT US) +1.7%. Here are some other premarket movers:

- AVEO (AVEO US) shares jump 38% in US premarket trading hours to $14.43 after LG Chem said it will buy the biotech for $15 per share in an all-cash transaction with an implied equity value of $566m on a fully diluted basis.

- Target (TGT US) stock rises 2.7% in US premarket trading after it was upgraded to buy from hold at Jefferies, which says the combination of a subdued valuation and improvements in the supply chain and inventory positioning supports a bullish stance on the retailer.

- FuboTV (FUBO US) shares rise as much as 11% in premarket trading, with analysts saying the firm’s decision to end operations of its Fubo Sportsbook betting unit will help its bottom line.

- Juniper (JNPR US) shares gain as much as 2.6% in US premarket trading after Piper Sandler upgraded the internet infrastructure company to neutral from underweight with the expectation that management can continue to increase product revenue numbers in full-year 2023 by around 10% year-on-year.

- Keep an eye on MongoDB (MDB US) after its shares were raised to neutral at Redburn as the stock is trading 20% below 2020 valuation lows and the brokerage sees no further downside that justifies a sell rating.

- Watch US timber stocks as RBC reshuffles ratings in the sector ahead of the third-quarter earnings season, which analysts say will mark a “sharp return” to normalized pricing, while downgrading Resolute (RFP US) and Western Forest Products (WEF CN) to sector perform from outperform.

“Investors keep pushing stock indices higher following the rebound over the annual lows at the end of last week, and growing risk appetite can now be seen across different asset classes,” said Pierre Veyret, a technical analyst at ActivTrades. As risks including high inflation, slower growth and the energy crisis still remain, “this is still seen as a technical correction,” he added.

Another reason for the continued meltup is because JPMorgan’s inhouse permabull, Marko Kolanovic, who has been long and wrong all year, appears to have thrown in the towel and late on Monday the Croat trimmed the extent of equities overweight in his model portfolio this month, citing “increasing risks around central banks making a hawkish policy error and geopolitics.” As we have said before, the bear market won’t end until Marko turns bearish, so that was another piece of the puzzle falling into place.

Meanwhile, the Bank of America monthly global fund manager survey “screams macro capitulation, investor capitulation, start of policy capitulation,” opening the way to an equities rally in 2023 the bank’s Chief Investment Strategist, Michael Hartnett wrote in a note on Tuesday. They expect stocks to bottom in the first half of 2023 after the Federal Reserve pivots away from raising interest rates.

“There’s still a strong feeling of a bear market rally about trading over the course of the last week,” said Craig Erlam, senior market analyst at Oanda Europe Ltd. “The economic landscape looks treacherous and we don’t even know if we’re at peak inflation and interest rate pricing yet. Those are substantial headwinds that will make any stock market rebound extremely challenging.”

In Europe, stocks rose for a fourth day, with most industry groups in the green. Risk sentiment was firmly bullish, with cyclical stocks leading the rally, while technology shares also outperformed. Autos, tech and financial services lead gains in Europe as Euro Stoxx 50 rallies 1.4%. FTSE MIB outperforms peers, adding 1.8%. Here are the most notable European movers:

- AZA SS: Avanza shares jump as much as 17%, the most since Oct. 2019, after the Swedish retail trading and savings platform reported what Handelsbanken called a “strong beat” on net interest income.

- THG LN: THG shares surge as much as 12% after SoftBank sold its stake in the British online shopping firm. The sale removes an overhang on the stock and it could help sentiment that existing investor Qatar Investment Authority bought the majority of the stake, according to Bloomberg Intelligence analysts.

- TIT IM: Telecom Italia shares rise as much as 9.6% in Milan trading on speculation reported by Italian newspaper MF regarding potential interest for the company by CVC.

- PUB FP: Publicis shares rise as much as 4.7% after the advertising agency lifted FY organic growth guidance for a second straight quarter.

- GALP PL: Portuguese oil co. Galp falls as much as 6.8% as it says it received a force majeure notice from Nigeria LNG following flooding that caused a “substantial reduction” in the production and supply of LNG and natural gas liquids, according to a regulatory filing.

- N91 LN: Ninety One shares drop as much as 5.3% after the investment manager reported a decline in assets under management during the second quarter.

- ERF FP: Eurofins Scientific shares drop as much as 6.0%, the most since July 28, after the provider of testing services reported third-quarter revenue that fell year-on-year.

- ROG SW: Roche shares slide as much as 1.6% after the Swiss pharmaceutical group slightly missed consensus 3Q expectations on overall sales, but focus remains on its outlook and pipeline, analysts say.

Earlier in the session, Asian equities rebounded, led by advances in tech stocks following a rally on Wall Street, as possible delays in bond sales by the Bank of England bolstered investor sentiment. The MSCI Asia Pacific Index rose as much as 1.5%, buoyed by TSMC, Tencent and Alibaba. All sub-gauges except real estate climbed. The Financial Times reported that the BoE may delay selling billions of pounds of government bonds, easing investor angst after the UK’s botched fiscal plan. The UK central bank denied the report after most markets in the region were closed. Tech stocks listed in Hong Kong climbed after the Nasdaq 100 index had its best day since July. Most benchmarks advanced, with notable gains in Australia, Japan, Hong Kong, and South Korea. Concerns that China is delaying the release of its 3Q GDP report amid the on-going party congress failed to quell the mood. The prospect of the BoE postponing QT “offers the potential for a decline in global rates volatility, a pre-condition for a broader improvement in cross-asset risk sentiment,” Stephen Innes, managing partner at SPI Asset Management, said before the bank’s denial. It’s been almost a year since Bitcoin hit a record. Even after Tuesday’s gain, the key Asian stock benchmark still trades close to its early-2020 low, as China’s virus lockdowns and property crisis weigh on growth. Asian stocks have underperformed their US and European peers this year as the Fed’s rate hikes pressure emerging market currencies, triggering an exodus of foreign funds

Japanese stocks rose, following a rebound in US peers as the S&P 500 was seen pointing toward a technical recovery. Electronics makers were the biggest boost. The Topix rose 1.2% to close at 1,901.44, while the Nikkei advanced 1.4% to 27,156.14. Recruit Holdings Co. contributed the most to the Topix gain, rising 5.1% after announcing a buyback. Out of 2,166 stocks in the index, 1,809 rose and 279 fell, while 78 were unchanged.

Australia stocks rebounded with tech and real estate shares leading; the S&P/ASX 200 index rose 1.7% to close at 6,779.20. The climb tracks a regional rally, buoyed after gains on Wall Street and a report of a possible delay in the Bank of England’s quantitative tightening. In New Zealand, the S&P/NZX 50 index rose 0.6% to 10,847.34.

In rates, Treasuries edged higher in early US trading after paring declines. Losses persist in gilts, where UK curve bear-flattens, with bunds also under pressure amid auctions by Germany, UK and Finland. US yields remain within 2bp of Monday’s closing levels, 10-year yields just under 4% with bunds and gilts trading cheaper by 6bp and 8bp in the sector. Gilt price action has been choppy; Long-end gilts take a breather, 10-year yield about 1bp higher after FT reported that Bank of England is set to delay quantitative tightening until gilt markets calm which the BOE later denied; UK sells 30-year notes later.

In FX, the Bloomberg Dollar Spot Index pared losses to trade marginally lower; yen settles at around the 149 handle while the pound trades lower toward $1.13.

- New Zealand’s dollar led G-10 gains after quarter-on-quarter inflation exceeded forecasts, fueling bets the central bank will need to keep raising interest rates

- The euro moved in a narrow range around $0.950, while the German 10- year yield reversed earlier losses to gain 6bps to 2.32%

- The pound weakened against all of its G-10 peers and fell below $1.13, following in an advance of as much as 0.5% to $1.1410. The long-term outlook for the pound has started to improve. At least, that’s what the options market is saying.

- The yen briefly rallied sharply versus the dollar after dropping to 149.29 per dollar, the lowest level since August 1990. Bank of Japan Governor Haruhiko Kuroda said that while the interest-rate differential with US has been a driving factor for the yen to weaken recently, the currency doesn’t move in parallel with the difference over the longer term

- The yuan stayed near 7.2 per dollar as the central bank kept the currency’s reference rate near 7.1 level in the last few sessions, a move that’s expected to slow the currency’s decline. USD/CNY falls 0.1% to 7.2000. It droped as much as 1.2% in early trade, close to the central bank’s fixing. USD/CNH little changed at 7.2075.

In commodities, oil switched between gains and losses as traders weighed a tight market against concerns over a global economic slowdown. WTI and Brent December contracts are softer on the session and gave up earlier gains as the DXY creeps higher throughout the European morning. Spot gold is flat around the USD 1,650/oz mark in a USD 10/oz range – but still under its 10 and 21 DMAs at 1,673.56/oz and 1,668.63/oz. LME metals are mostly lower amid the recent rise of the Dollar, whilst Rio Tinto forecasted annual iron ore shipments at the lower end of guidance and sees further downside risks to demand as the global economy slows. White House is reportedly planning an oil reserve release announcement this week with a release of another 10mln-15mln bbls in an effort to balance markets and keep prices from climbing, according to Bloomberg.

EU financial services chief McGuiness called on the US to create new crypto rules and said any regulation imposed on the industry would need to be global for it to work, according to FT.

Looking to the day ahead now, and data releases from the US include industrial production and capacity utilisation for September, as well as the NAHB housing market index for October. Central bank speakers include the ECB’s Makhlouf and Schnabel, as well as the Fed’s Bostic and Kashkari. Finally, earnings releases include Goldman Sachs, Netflix, Johnson & Johnson, and Lockheed Martin.

Market Snapshot

- S&P 500 futures up 1.4% to 3,741.00

- MXAP up 1.4% to 138.93

- MXAPJ up 1.6% to 450.98

- Nikkei up 1.4% to 27,156.14

- Topix up 1.2% to 1,901.44

- Hang Seng Index up 1.8% to 16,914.58

- Shanghai Composite down 0.1% to 3,080.96

- Sensex up 1.0% to 58,966.61

- Australia S&P/ASX 200 up 1.7% to 6,779.22

- Kospi up 1.4% to 2,249.95

- STOXX Europe 600 up 1.1% to 402.75

- German 10Y yield up 3% at 2.337%

- Euro up 0.1% to $0.9852

- Brent Futures down 0.6% to $91.05/bbl

- Gold spot up 0.1% to $1,651.42

- U.S. Dollar Index up 0.1% at 112.187

Top Overnight News from Bloomberg

- Just 10% of Britons have a favorable opinion of Liz Truss, a YouGov survey found, piling further woes on the beleaguered prime minister a day after she was forced to row back on the bulk of her economic vision for Britain

- UK trade unions have called on millions of workers to protest against any return to austerity after Britain’s new chancellor of the Exchequer warned that “some areas of spending will need to be cut.”

- There’s scope for a Polish central bank hike by as much as 100bps in November, Monetary Policy Council member Joanna Tyrowicz says in ISB News interview

- French rail, energy and other key workers are striking on Tuesday to demand a bigger share of corporate profits, raising pressure on President Emmanuel Macron to take further steps to ease the impact of surging inflation

- ECB policy maker François Villeroy de Galhau expects the central bank to continue to “go quickly” until its deposit rate reaches 2% at the end of the year, Financial Times reports, citing an interview

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were positive with the region inspired by gains in global counterparts following the UK Chancellor’s reversal of most of the measures of the ‘mini-Budget’ and with a report later suggesting a delay of QT by the BoE. ASX 200 was led by strength in tech and with the top-weighted financials sector also notching firm gains, while commodity-related stocks were somewhat varied with Rio Tinto choppy after a mixed quarterly activity report. Nikkei 225 reclaimed the 27,000 level to the upside, but was off highs with officials continuing to pledge to take action to address excess FX moves. Hang Seng and Shanghai Comp. gained although the mainland lagged amid COVID woes after Nanjing halted certain indoor venues due to rising cases, while the postponement of key Chinese data releases including Q3 GDP has led to some speculation that the data could be disappointing, although it was also suggested that the delay could be so that officials can concentrate on the Chinese Communist Party Congress.

Top Asian News

- China’s Nanjing halted certain indoor venues including bars, KTVs and gyms, while it also halted dine-in services due to an increase in coronavirus cases.

- RBA Minutes from the October 4th Meeting stated the decision to raise rates by only 25bps was finely balanced with the smaller move warranted by the scale of hikes already delivered and lags in policy. RBA added that the uncertain outlook argued for slower hikes for a time but noted further increases in rates are likely over the period ahead and that rates are not especially high, while the board emphasised the importance of keeping inflation expectations anchored and RBA said monthly CPI data confirmed broad-based pick-up in inflation, rents and utilities are expected to increase.

- RBA Deputy Governor Bullock said the board expects to increase interest rates further over the coming months with the pace and timing to be determined by data, while she added that as the board meets more frequently than most peers, it can achieve a similar tightening with smaller individual rate increases.

European equity bourses traded with gains across the board but are off best levels. Sectors are mostly firmer with no overarching theme; Autos & Parts, Financial Services, and Industrial Goods lead the charge whilst Healthcare, Optimised Personal Care, Energy and Basic Resources sit at the bottom of the pile. US equity futures are firmer to a greater magnitude than their European counterparts, with the ES trading on either side of 3,750 whilst the NQ outperforms its peers. Intel’s (INTC) MobilEye IPO is set to be priced between USD 18-20/shr, according to Bloomberg. Renault (RNO FP) and Nissan (7201 JT) are moving towards a “landmark” deal to reshape their alliance, according to Bloomberg; subsequently echoed by the Renault CEO in a Nikkei interview.

Top European News

- BoE is reportedly expected to further delay quantitative tightening until gilt markets calm, according to FT. Subsequently, the BoE labelled this report as “inaccurate”.

- UK PM Truss said she wants to accept responsibility and apologise for the mistakes made, while she added that she will lead the Tories into the next general election and is sticking around because she was elected to deliver for the country. PM Truss also stated the most vulnerable will be protected into next winter regarding household energy bills and that they are looking at exactly how they can do that, according to a BBC interview.

- ECB’s Villeroy said the UK crisis shows the risk of a vicious loop and that the pensions turmoil underscored the need for non-banks to build liquidity buffers, according to FT.

- European Commission to unveil proposal of further emergency energy measures for coming winter (including joint purchasing & alternative benchmark) at 14:30BST/09:30EDT, according to journalist Keating.

FX

- Kiwi elevated as stronger than expected NZ CPI metrics lift RBNZ rate outlooks, NZD/USD probes 0.5700 before pullback

- Sterling underperforming after making stellar gains on Monday as BoE says FT’s QT delay report is inaccurate; Cable sub-1.1300 from just over 1.1400 at one stage

- Loonie lags within a 1.3771-1.3657 range as crude prices sag

- Euro pivots 0.9850 vs Buck as DXY holds around 112.000 and Fib resistance at 0.9858 hampers EUR/USD

- Yen pares some losses from under 149.00 against Dollar amidst some unsubstantiated talk of intervention

- The CBRT’s move to raise the required level of bond holdings for FX deposits means that banks must hold an additional TRY 80-100bln of bonds, via Reuters citing bankers.

- BoJ and FSA are to hold 17th cooperation on financial stability, according to reports.

Fixed Income

- Gilts saw an initial bounce at the open on overnight FT reporting around a potential delay to QT; however, this was modest in nature and has since given way to marked pressure following BoE labelling it as “inaccurate”.

- The overall complex is pressured, with Gilts lagging though Bunds are in close proximity and below 136.00 post poor 7yr-supply and ahead of ECB speak.

- Stateside, UTS have been following their peers directionally though magnitudes are more contained overall pre-data/Fed speak; yield curve mixed, overall.

Commodities

- WTI and Brent December contracts are softer on the session and gave up earlier gains as the DXY creeps higher throughout the European morning.

- Spot gold is flat around the USD 1,650/oz mark in a USD 10/oz range – but still under its 10 and 21 DMAs at 1,673.56/oz and 1,668.63/oz.

- LME metals are mostly lower amid the recent rise of the Dollar, whilst Rio Tinto forecasted annual iron ore shipments at the lower end of guidance and sees further downside risks to demand as the global economy slows.

- White House is reportedly planning an oil reserve release announcement this week with a release of another 10mln-15mln bbls in an effort to balance markets and keep prices from climbing, according to Bloomberg. Note, this would come from part of a previously announced 180mln bbl sale announced earlier in the year

- UAE supports Saudi Foreign Ministry’s statement regarding the OPEC+ decision and fully stands with Saudi Arabia in its efforts to support energy stability and security, according to the state news agency cited by Reuters.

Geopolitics

- US Commerce Department issued a temporary denial order against Ural Airlines for operating in apparent violation of US export controls on Russia, according to Reuters.

- Ukraine President Zelenskiy says there is no space left for negotiations with Russian President Putin, via Reuters.

- Russia’s Kremlin, when asked if Russia’s nuclear umbrella extends to annexed territories, says all the territories are parts of Russia and their security is provided as with all other Russian territories, via Reuters.

- Japanese Chief Cabinet Secretary Matsuno said Japan is to impose additional sanctions against North Korea, according to Reuters.

- Officials revealed that China recruited dozens of former British military pilots to teach Chinese armed forces how to defeat western warplanes and helicopters in a “threat to UK interests”, according to Sky News’s Deborah Haynes.

US Event Calendar

- 09:15: Sept. Capacity Utilization, est. 80.0%, prior 80.0%

- 09:15: Sept. Manufacturing (SIC) Production, est. 0.2%, prior 0.1%

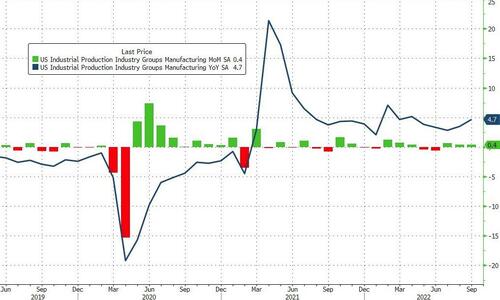

- 09:15: Sept. Industrial Production MoM, est. 0.1%, prior -0.2%

- 10:00: Oct. NAHB Housing Market Index, est. 43, prior 46

- 16:00: Aug. Total Net TIC Flows, prior $153.5b

- 16:00: Aug. Net Foreign Security Purchases, prior $21.4b

Central bank speakers

- 14:00: Fed’s Bostic Takes Part in Workrise Panel Discussion

- 17:30: Fed’s Kashkari Discusses the Economy

DB’s Jim Reid concludes the overnight wrap

We’ve discussed recently how we shouldn’t underestimate just how much the UK’s recent woes have impacted global markets. Correlation doesn’t equal causality, but the UK news has again seemed to heavily influence global markets over the last 24 hours after the UK government officially announced one of the biggest U-turns in political history and ditched the bulk of what remained of their mini-budget. However the risk momentum was also helped by a view that earnings season has starting relatively well versus beaten up expectations. Even overnight the UK is moving global markets again as reports from the FT that the BoE is going to delay QT at around 5am this morning have pushed equities futures over a percent higher with S&P 500 (+1.95%) and NASDAQ 100 (+2.17%) contracts soaring.

This follows a big session yesterday with the S&P 500 (+2.65%) and the STOXX 600 (+1.83%) both posting strong advances that were led by the more cyclical sectors. Tech stocks were one of the big outperformers, with the NASDAQ (+3.43%) and the FANG+ Index (+4.83%) seeing even stronger advances, whilst banks were another outperformer with those in the S&P 500 up +3.48% in their 4th consecutive advance. The moves were also supported by some positive corporate news, with Lufthansa raising their full-year forecasts whilst Bank of America saw trading revenue beat expectations and net interest income rise to a record in Q3, a common theme among banks benefitting from heightened market volatility and rising policy rates. Bank of America joins the other large US banks to report with JPMorgan (+5.94% since releasing earnings), Citi (+1.44% since), Wells Fargo (+3.68%), and Morgan Stanley (-2.75%) all having reported the last few days. That comes as earnings season is moving into full flow, with today’s releases including Netflix, Goldman Sachs and Johnson & Johnson. We’ve had 38 S&P companies report so far, and while major financials have grabbed a lot of the headlines there have been a number of key corporate reporters including consumer staples Walgreens (+3.32% since their earnings), health care provider United Health Group (+2.38% since reporting), food and beverage retailer PepsiCo (+6.24% since reporting), and airline Delta (+6.61%). The breadth of reporters should expand with the major US banks largely now in the rear-view mirror.

Back to the UK and there was an increasing sense of what was coming yesterday, with the first reversal happening two weeks ago as they U-turned on the abolition of the top 45% rate of income tax. Then on Friday we had a second reversal as PM Truss announced that corporation tax would go up after all, in line with the previous government’s plans. But yesterday saw Chancellor Hunt announce that almost everything else would be going as well, including the planned cut in the basic rate of income tax to 19% from April 2023, which will instead be kept at 20% indefinitely.

It’s clear the UK are now desperately trying to claw back their market credibility, as not only have the government reversed course on most of the tax cuts, but they also said they’d revisit the scale of their energy support package as well. Previously, energy prices were set to be capped at £2,500 per year for the average household over the next two years. But the government are now saying that will only go up until April 2023, and after that they’d review what support would be given instead, and were aiming to “design a new approach that will cost the taxpayer significantly less than planned”. Furthermore, the government’s statement implied there was more to come in the fiscal statement on October 31, as it said that government departments “will be asked to find efficiencies within their existing budgets”, and that there’d be “further changes” on fiscal policy “to put the public finances on a sustainable footing”.

UK assets surged on the back of the announcements, with sterling +1.66% higher versus the US dollar after having been as much as +2.38% up, just as yields on 10yr UK gilts tumbled by -35.7bps to 3.96%. In fact, apart from September 28 when the Bank of England began their intervention, that’s the largest daily decline in the 10yr gilt yield since the Conservatives won a surprise victory in the 1992 general election, so we are still experiencing unprecedented volatility. Meanwhile, sterling (+0.31%) is trading higher again this morning ($1.1393) on the FT story that QT is set to be delayed. Back to yesterday and the declines in real yields were even more pronounced than nominals, with the 10yr real yield down by -47.9bps on the day, which again is the largest daily move since the BoE intervention began. That said, even with the recent declines, the spread of UK 10yr yields over German bunds is still wider than it was prior to the mini-budget at +169bps, which points to the fact that investors are still charging a larger premium for holding gilts, even with the recent U-turns.