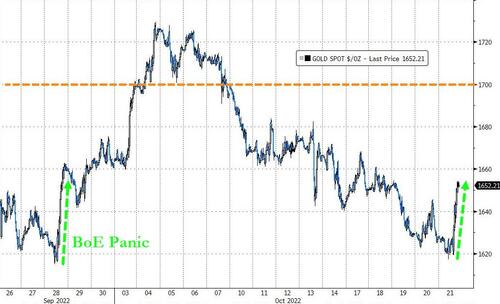

OCT 21//GOLD REVERSES COURSE RISING $19.10 UP TO $1651.50//SILVER UP 43 CENTS TO $19.17//PLATINUM CLOSES UP $17.90 TO $934.60//PALLADIUM IS DOWN $45.07 TO $2018.25//JAPAN CENTRAL BANK CAPITULATES AND INTERVENES TO STOP THE FALL IN THE YEN//A MUST READ: ALASDAIR MACLEOD ON THE LAST STAND FOR FREE MARKETS//YIELDS ON USA 10 YR BOND RISES TO ABOVE 4.33%//UK 10 YEAR GILT RISES TO 4.06%//TURMOIL IN ALL MARKETS FORCES JAPANESE/USA FOR INTERVENTION//PEPE ESCOBAR ON DISCUSSION OF CHINA’S NEW PLENARY AND WATCH FOR CHINA’S ATTACK ON TAIWAN FOR THEIR SEMI CONDUCTORS//COVID UPDATES//VACCINE IMPACT//DR PAUL ALEXANDER//UPDATES ON THE UK FIASCO AND A MUST SEE VIDEO//STOCK MARKETS RISE ON WHISPERER STATING A POSSIBLE USA PAUSE IN INTEREST RATE HIKES//SWAMP STORIES FOR YOU TONIGHT//

323 C HSBC 381 435 H SCOTIA CAPITAL 309 657 C MORGAN STANLEY 13 661 C JP MORGAN 399 255 732 C RBC CAP MARKETS 1 880 H CITIGROUP 43 905 C ADM 15

TOTAL: 708 708 MONTH TO DATE: 23,158

JPMORGAN STOPPED 255/708

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 708 NOTICES FOR 70,800 OZ or 2.2021 TONNES

total notices so far: 23,158 contracts for 2,215,800 oz (72.0311 tonnes)

SILVER NOTICES: 12 NOTICE(S) FILED FOR 60,000 OZ/

total number of notices filed so far this month 444 : for 2,220,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $19.10

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////A WITHDRAWAL OF 1.74 TONNES INTO THE GLD//

INVENTORY RESTS AT 930.99 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 43 CENTS

AT THE SLV// :/BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A SMALL DEPOSIT OF .46 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 486.163 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 657 CONTRACTS TO 137,426 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE GOOD GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.33 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS/HFT WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.33)., AND UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS, AS WE HAD A HUGE GAIN IN OUR TWO EXCHANGE OF 1014 CONTRACTS. HUGE NUMBERS OF SPECS CONTINUE TO ADD TO THEIR SHORTFALLS FROM WHICH OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. SOME SPEC LONGS ADDED TO THEIR POSITIONS

WE MUST HAVE HAD: I) ZERO SPECULATOR SHORT COVERINGS BUT CONSIDERABLE SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /// SOME NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING AN 85,000 OZ QUEUE. JUMP / // V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: –32

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 17 days, total 55,540 contracts: 27.770 million oz OR 1.633MILLION OZ PER DAY. (326 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 27.770 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 27.770 MILLION OZ INITIAL

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 657 WITH OUR $0.33 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 325 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S 85,000 QUEUE JUMP .. WE HAD A HUGE SIZED GAIN OF 1014 OI CONTRACTS ON THE TWO EXCHANGES FOR 5.070 MILLION OZ..

WE HAD 12 NOTICE(S) FILED TODAY FOR 60,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 893 CONTRACTS TO 444,335 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -236 CONTRACTS.

.

THE STRONG SIZED INCREASE IN COMEX OI CAME WITH OUR GAIN IN PRICE OF $2.40//COMEX GOLD TRADING/THURSDAY // CONSIDERABLE SPECULATOR SHORT COVERINGS ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION AND STRONG SPEC SHORT ADDITIONS // CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE. JUMP OF 27,500 OZ//NEW STANDING 73.188TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $2.40 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 2,502 OI CONTRACTS 7.782 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1609 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 444,047

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2,214 CONTRACTS WITH 697 CONTRACTS INCREASED AT THE COMEX AND 1609 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2502 CONTRACTS OR 7.782 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1609) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (605): TOTAL GAIN IN THE TWO EXCHANGES 2,214 CONTRACTS. WE NO DOUBT HAD 1) STRONG SPECULATOR SHORT ADDITIONS// CONTINUED GOOD BANKER ADDITIONS/// MORE SPEC SHORT ADDITIONS// SMALL NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 27,500 OZ QUEUE. JUMP ///NEW STANDING 73.188 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) SMALL SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

40,566 CONTRACTS OR 4,056,600 OZ OR 126.17 TONNES 17 TRADING DAY(S) AND THUS AVERAGING: 2386 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES: 126.17 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 126.17/3550 x 100% TONNES 3.54% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 126.17 TONNES INITIAL ( MUCH SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 605 CONTRACT OI TO 137,426 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 325 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 325 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 325 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 657 CONTRACTS AND ADD TO THE 325 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 982 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 4.910 MILLION OZ//

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

A MUST MUST VIEW

Ep. 96 Live from the Vault

Sinister footprints in Silver to cover SLV shorts

In this week’s Live from the Vault, Andy Maguire takes another deep dive into the smoke and mirror world of COMEX, examining the uncanny resemblance of the current market structure to the 2008 financial crisis-triggered bullish setup.

The London wholesaler explains how the extremely supply-tight physical market draining COMEX liquidity to unsustainable levels can ultimately result in gold and silver arising as safe-haven assets.

SHANGHAI CLOSED UP 3,88 PTS OR 0.13% //Hang Seng CLOSED DOWN 69.10 OR 0.42% /The Nikkei closed DOWN 116.38PTS OR 0.43% //Australia’s all ordinaires CLOSED DOWN 0.71% /Chinese yuan (ONSHORE) closed UP TO 7.2464 //OFFSHORE CHINESE YUAN DOWN 7.2682// /Oil DOWN TO 84,96 dollars per barrel for WTI and BRENT AT 92.69 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 605 CONTRACTS TO 444,047 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS SMALL COMEX INCREASE OCCURRED WITH OUR RISE IN PRICE OF $2.40 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (1609 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1609EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 1609 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1609 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUGE SIZED TOTAL OF 2214 CONTRACTS IN THAT 4273LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI GAIN OF 8516 CONTRACTS..AND THIS HUGE SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR SMALL GAIN IN PRICE OF GOLD $2.40//WE HAD SOME SPEC SHORTS ADDITIONS, WITH BANKERS AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD SOME ADDITIONAL NEWBIE SPECS GOING LONG WITH OUR NEW ATTRACTIVE LOW PRICE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (73.188),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 73.188 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $2.40) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS SPEC SHORT ADDED TO THEIR POSITIONS AS WE HAD A FAIR SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 2,502 CONTRACTS // WE HAVE REGISTERED A FAIR GAIN OF 7.782 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (73.188 TONNES)…THIS WAS ACCOMPLISHED WITH OUR RISE IN PRICE OF $2.40

WE HAD -236 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 2502 CONTRACTS OR 250,200 OZ OR 7.782 TONNES

Total monthly oz gold served (contracts) so far this month

23,158 notices 2,315,800 72.0311 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 2

i)Into Brinks: 96.453 oz

ii) Into HSBC: 13,837.922 oz

total deposits 13,934.425 oz

customer withdrawals:2

i) Out of Manfra: 385.812 oz 12 kilobars

ii) Out of Brinks 64.30 oz (2 kilobars)

total: 450.12 oz

total in tonnes: 0.0139 tonnes

Adjustments: 3// dealer to customer

i)Manfra: 6,036.997 oz

ii) Out of Brinks 9,163.035 oz

iii) Out of JPMorgan: 55,460.403 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 1080 contracts having GAINED 100 contracts . We had 175 contracts

filed on THURSDAY, so we GAINED A STRONG 275 contracts or an additional 27,500 oz will stand in this active delivery month of Oct. From this point

we should gain in total gold standing through to the end of Oct.( This is queue jumping and in reality it is the exercising of London based EFP;s for gold at the comex)

November GAINED 66 contracts to stand at 3567 (WE ARE GOING TO HAVE AN EXTRAORDINARILY LARGE NOV.GOLD DELIVERY)

December LOST 2052 contracts up to 363,302

We had 708 notice(s) filed today for 70,800 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 399 notices were issued from their client or customer account. The total of all issuance by all participants equate to 708 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 255 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (23,158) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 1080 CONTRACTS) minus the number of notices served upon today 708 x 100 oz per contract equals 2,353,000 OZ OR 73.188 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (23,158) x 100 oz+ (1080) OI for the front month minus the number of notices served upon today (708} x 100 oz} which equals 2,353,000 oz standing OR 73.188 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 73.188 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 444 x 5,000 oz = 2,220,000 oz

to which we add the difference between the open interest for the front month of OCT(250) and the number of notices served upon today 12 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 444 (notices served so far) x 5000 oz + OI for front month of OCT (250) – number of notices served upon today (12) x 5000 oz of silver standing for the OCT contract month equates 3,410,000,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

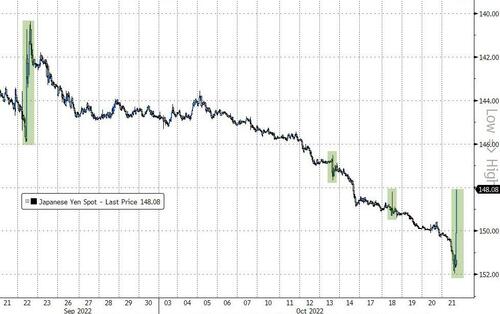

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

GLD INVENTORY: 930.99 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: AWITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

CLOSING INVENTORY 486.163 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

LAWRIE WILLIAMS: Swiss gold exports stay high to China, India,Turkey.

Eastern flows dominate.

We always monitor the monthly Swiss customs data for gold imports and exports as they provide an excellent window on the directional global flows of gold bullion given the huge importance of the Swiss gold refineries in this traffic. For the month of September, these have just been released and show that in that month this small European nation, with no domestic gold production of its own, imported some 181 tonnes of gold of refined, semi-refined and scrap gold and exported 176.3 tonnes of ultra-refined gold bullion during the period.

As usual the gold flows were predominantly from gold producing nations and gold holding ones in the West to consuming and hoarding ones in the Middle East and Asia, which recipients are assumed to be stronger holders. Indeed in September 89.6% of Swiss gold exports were destined for these more easterly areas assuming one counts Turkey as a Middle Eastern nation.

A recent report on Bloomberg has highlighted this geographical transference of gold which has led to demand exceeding supply in some areas and price premiums appearing in some markets. Bloomberg comments that rising rates that may be currently making gold less attractive as an investment in the West mean that large volumes of metal are being drawn out of vaults in financial centres like New York and London and heading east to meet demand in Shanghai’s gold market or Istanbul’s Grand Bazaar and as a result, gold and silver are selling at unusually large premiums over the global benchmark price in some Asian markets in particular.

Bloomberg further reports that more than 500 tonnes of gold has poured out of New York and London vaults since the end of April, according to data from the CME Group and London Bullion Market Association. At the same time, shipments are rising into big Asian gold consumers like China, whose imports hit a four-year high in August.

China/Hong Kong continued to occupy top spot for the Swiss gold exports in receiving 45.1 tonnes, with by far the major part (44.5 tonnes) going directly to the Chinese mainland, thus diminishing the importance of Hong Kong even further as a conduit for China’s gold imports. India, which took in 35.3 tonnes looked to be resuming its appetite for gold consumption, closely followed by Turkey which imported 32.2 tonnes. Other significant Middle Eastern and Asian nation recipients of the Swiss gold were Thailand (13.1 tonnes), the United Arab Emirates (11 tonnes), Singapore (9.1 tonnes) and Saudi Arabia (6.7 tonnes).

Swiss gold imports during September were mostly from gold mining nations where it tends to receive doré bullion direct from the mines for re-refining into the ultra high purity kilobars, wafers and coins most in demand on global markets. The refineries also receive larger bars from the major gold vaults in countries like the U.S. and the UK which hold high purity good delivery large gold bars, often on behalf of third party nations, which may need to dispose, or lease them in smaller sizes on global markets and they are geared up to accomplish this too. Historically the Swiss refineries have carved out a substantial business and reputation in this arena, and handle an amount equivalent to perhaps up to 60% of new mined gold annually so comprise an extremely significant part of the global gold market in terms of directional flow patterns.

21 Oct 2022

-END-

-END-

END

3.Chris Powell of GATA provides to us very important physical commentaries

Your weekend reading material: the last stand for free markets

Alasdair Macleod…a must read!!

Alasdair Macleod: The last stand for free markets

Submitted by admin on Thu, 2022-10-20 11:29Section: Daily Dispatches

By Alasdair Macleod GoldMoney, Toronto Thursday, October 20, 2022

The British government’s desperate dash toward free markets has failed, badly bungled. The establishment in Whitehall and Westminster is back and realigned with the international government consensus. The socialist wealth redistributors, the interventionists, and the anti-Brexit Remainers now formulate government policy. In Britain, free markets are dead.

Citizens of other Western nations should take note of these developments. The replacement of Kwasi Kwarteng as chancellor of the exchequer by Jeremy Hunt, an establishment man and deemed to be a safe pair of hands, is set to guarantee the continuing authority of the state over its electors. The underlying problem — that the electorate can no longer afford its government — is lost in the noise.

We must abandon any hope of a reversal of rapacious government policies that continually strip electors of their freedom and personal wealth. With a rapidly approaching financial crisis, which is now widely expected, the UK government will double down on its anti-market, anti-sound money policies. We can expect more price subsidies and price controls — paid for, of course, by yet more currency debasement.

It’s not just the UK. All advanced economies are approaching an endpoint in their governments’ anti-market policies. The global status quo can now be challenged only by markets. Rising interest rates, driven by collapsing purchasing power of the major fiat currencies, are bringing on that challenge, triggering a global financial and currency crisis.

The destiny of financial markets is already becoming evident, with asset values in an intractable decline. The contraction of over-the-counter derivative markets is in its earliest stages, a factor of which the public is generally unaware, but will have enormous consequences. Bank credit for the non-financial sector is in the firing line as well, leading with certainty to a slump in global gross domestic product. And we can be sure that policymakers everywhere will do their utmost to rescue the failing system by new rounds of quantitative easing.

Welcome to an outlook dominated by the accumulated errors of the global establishment, all set to hit us at the same time. As for the return to free markets? Not until considerable volumes of political and intellectual water have flowed under the bridge. …

The Chinese citizens and Indian citizens certainly know the value of gold: Swiss imports of gold rise

Refiners are having great difficulty refining gold/silver due to high costs of electricity and natural gas

(Reuters)

Swiss gold exports to China and India rise as prices fall

Submitted by admin on Thu, 2022-10-20 09:18Section: Daily Dispatches

From Reuters Thursday, October 20, 2022

LONDON — Swiss gold exports to top markets China and India increased in September, while shipments to Turkey rose to the highest since April 2013, Swiss customs data showed on Thursday.

A decline in gold prices from more than $2,000 an ounce in March to around $1,650 has boosted demand for gold bars, coins and jewellery in Asia, where buyers typically take advantage of low prices.

Economic turbulence in Turkey has also encouraged buying of the metal, which is often seen by investors as a safe way to store more money….

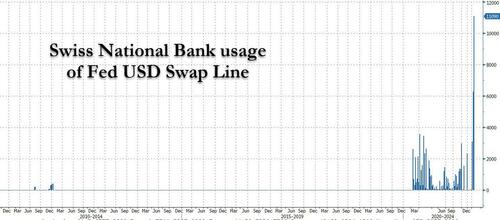

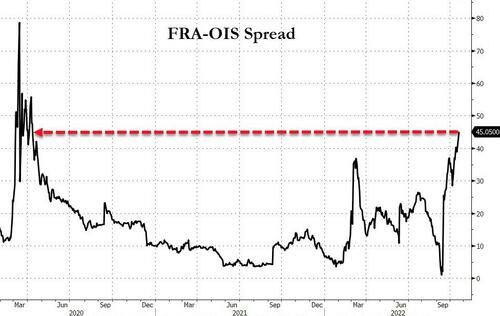

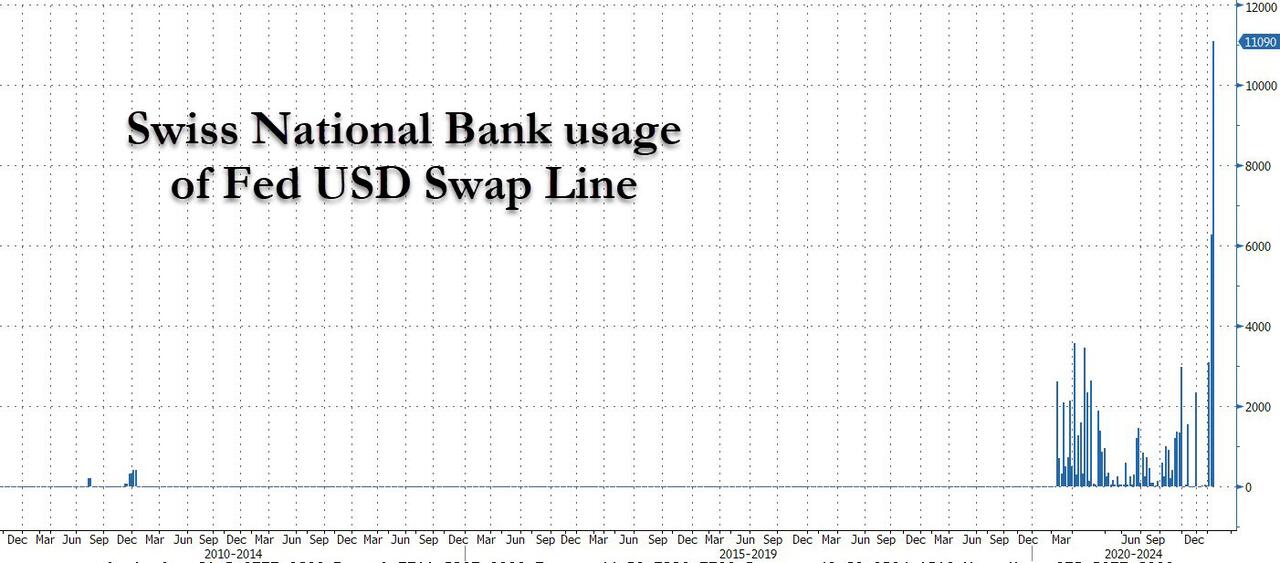

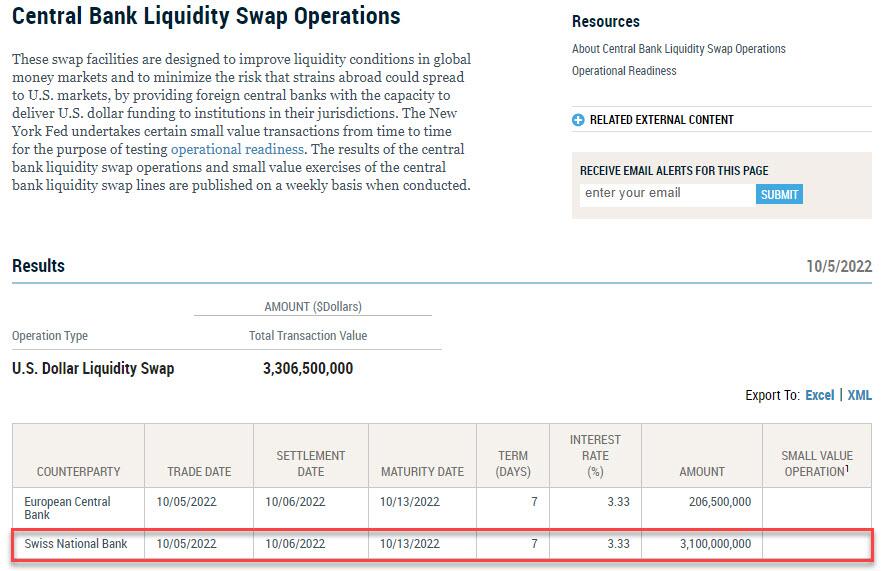

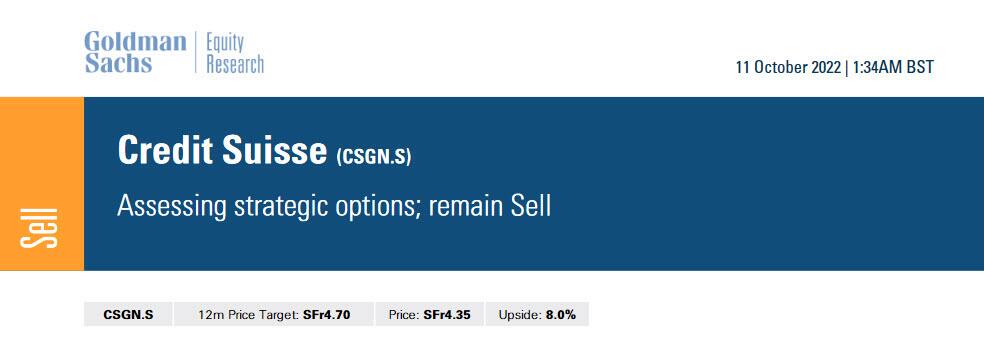

Credit Suisse is in big trouble with their derivative trades. As they short the precious metals, they also borrow massive amounts of USA dollars and it is thses dollars that they are having trouble balancing. They need the Fed to bail them out:

(Bloomberg)

Swiss banks seek most dollars since 2008 in bid for easy profit

Submitted by admin on Wed, 2022-10-19 20:06Section: Daily Dispatches

Why is the Federal Reserve running a scheme to enrich Swiss banks?

* * *

By Bastian Benrath Bloomberg News Wednesday, October 19, 2022

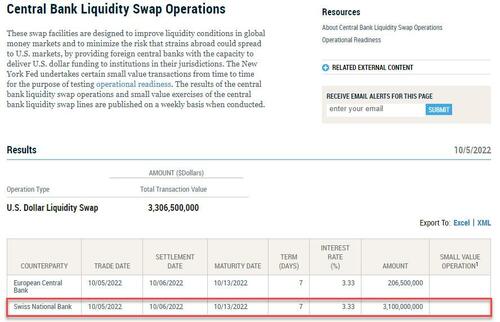

Banks in Switzerland sought the most dollars since 2008 using an emergency dollar swap facility provided by the Federal Reserve in what is likely to be a bid for easy profits.

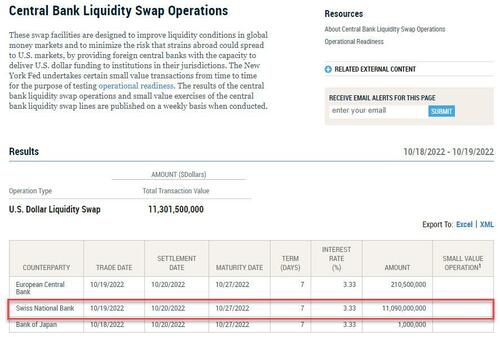

In today’s auction conducted by the Swiss National Bank, 17 institutions took up $11.09 billion. That’s the most since October 2008, when the Global Financial Crisis was raging in the wake of Lehman Brothers’ collapse.

This is the fourth week in a row when banks have accessed the facility. Last Wednesday 15 banks took up $6.27 billion in funds.

According to economists at Credit Suisse, Swiss banks swap the dollars into francs in order to generate a profit. The lenders can even sell the cash back to the Swiss National Bank using its reverse repo auctions, or deposit it at the institution to benefit from a positive interest rate.

“We do not believe that the increased demand for U.S. dollar liquidity by domestic banks reflects any liquidity issues in the Swiss banking system,” Credit Suisse economist Maxime Botteron wrote in a report last week. …

In this week’s Live from the Vault, Andy Maguire takes another deep dive into the smoke and mirror world of COMEX, examining the uncanny resemblance of the current market structure to the 2008 financial crisis-triggered bullish setup.

The London wholesaler explains how the extremely supply-tight physical market draining COMEX liquidity to unsustainable levels can ultimately result in gold and silver arising as safe-haven assets.

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.2464

OFFSHORE YUAN: 7.2682

SHANGHAI CLOSED UP 3.88 PTS OR 0.13%

HANG SENG CLOSED DOWN 69.10 OR 0.42%

2. Nikkei closed DOWN 116.38 PTS OR 0.43%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 113.48/Euro FALLS TO 0.97488

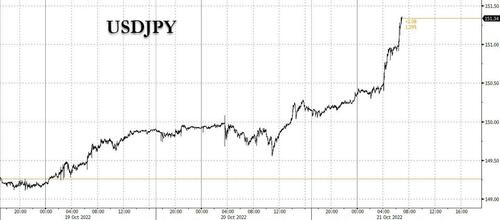

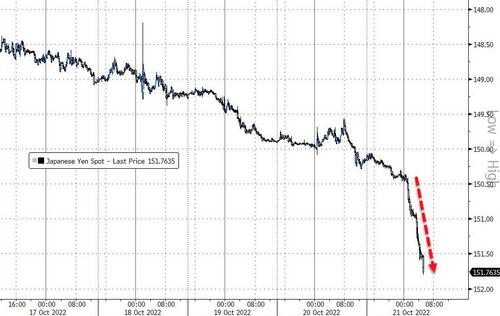

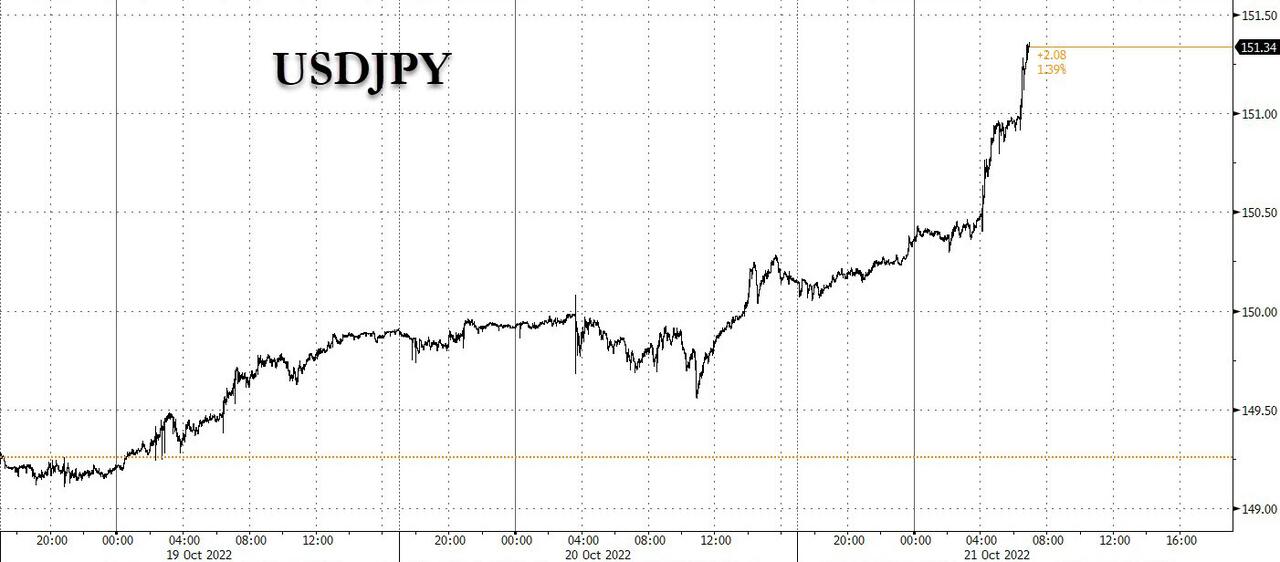

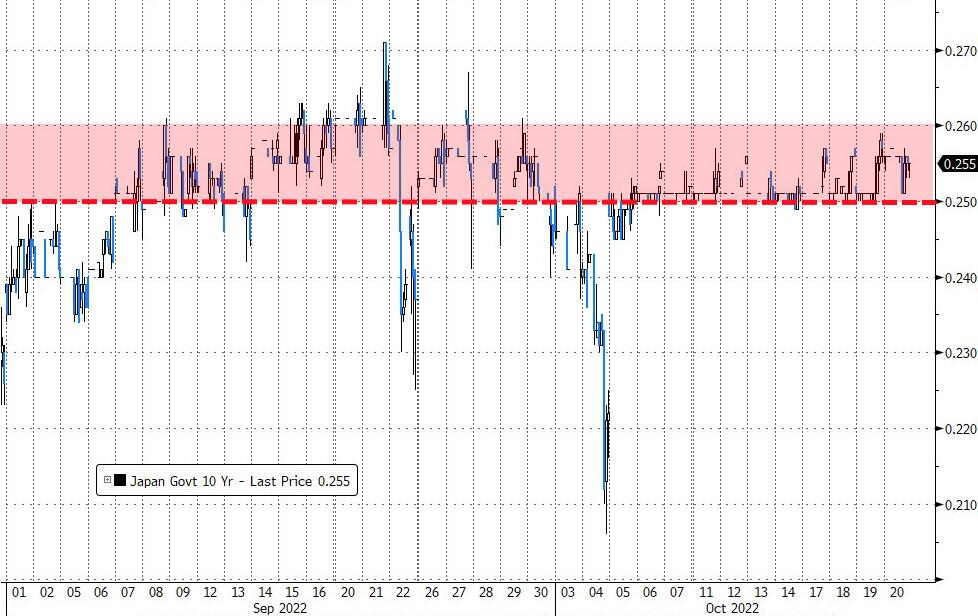

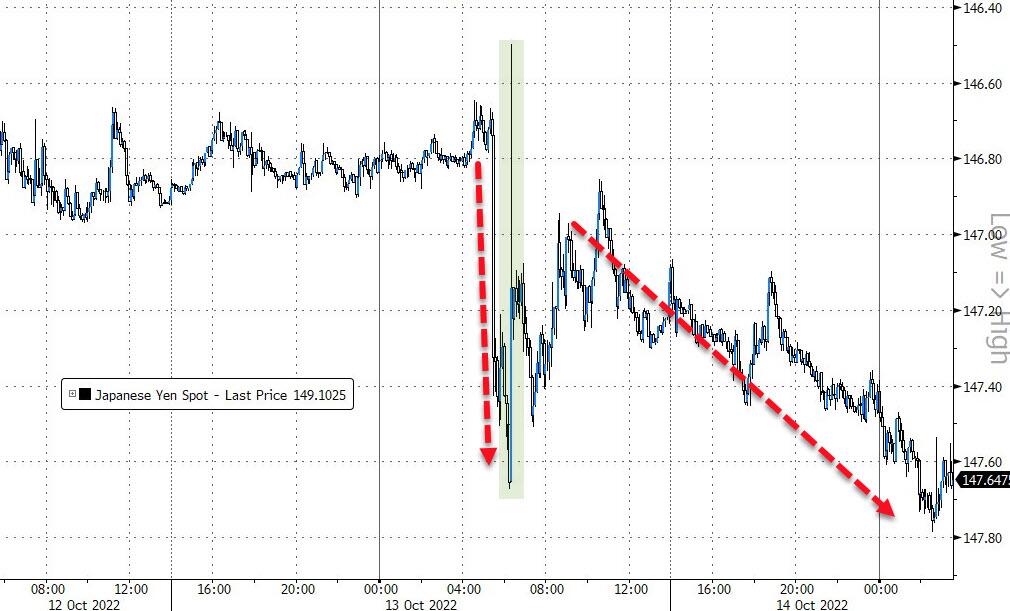

3b Japan 10 YR bond yield: RISES TO. +.249/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 151.52/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.4885%***/Italian 10 Yr bond yield RISES to 4.853%*** /SPAIN 10 YR BOND YIELD RISES TO 3.62%…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 5.064//

3j Gold at $1623.60//silver at: 18.38 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 38/100 roubles/dollar; ROUBLE AT 61.02//

3m oil into the 84 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

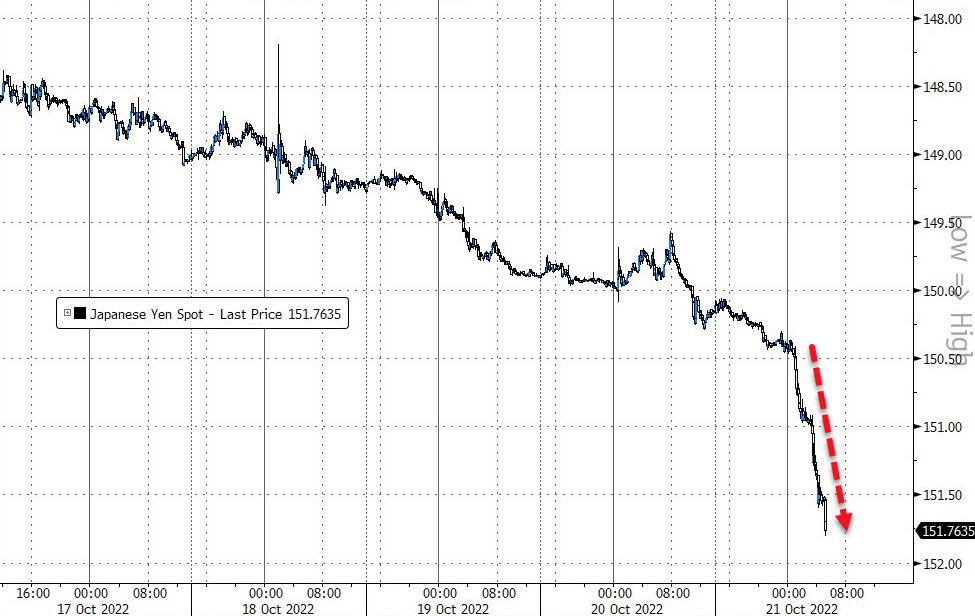

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 151.53DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 1.01149–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.98589well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

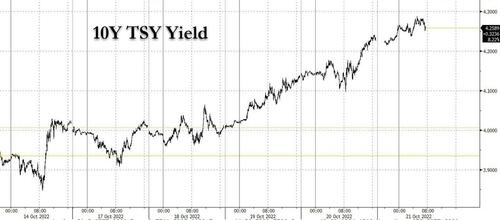

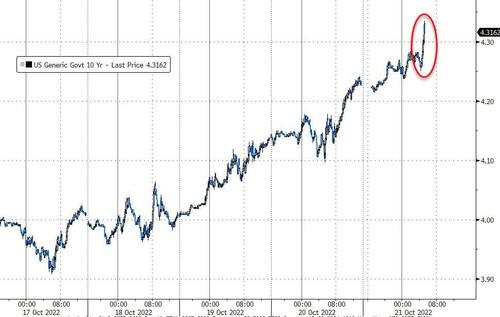

USA 10 YR BOND YIELD: 4.280% UP 5 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 4.299% UP 8 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,60…GETTTING DANGEROUS

GREAT BRITAIN/10 YEAR YIELD: 4.124%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

There is a huge shortage of dollars setting off a huge rise in the dollar and major falls in the Chinese yuan, the Japanese yen, Cdn dollar etc.

We now have a global currency crisis. The lower currency values in all countries cause inflation in their country to skyrocket. This must end

(zerohedge)

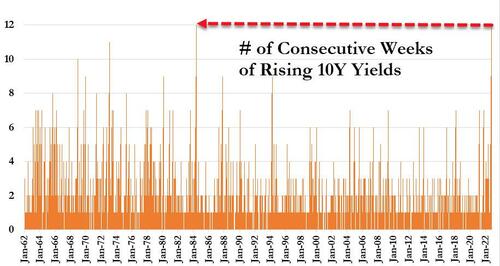

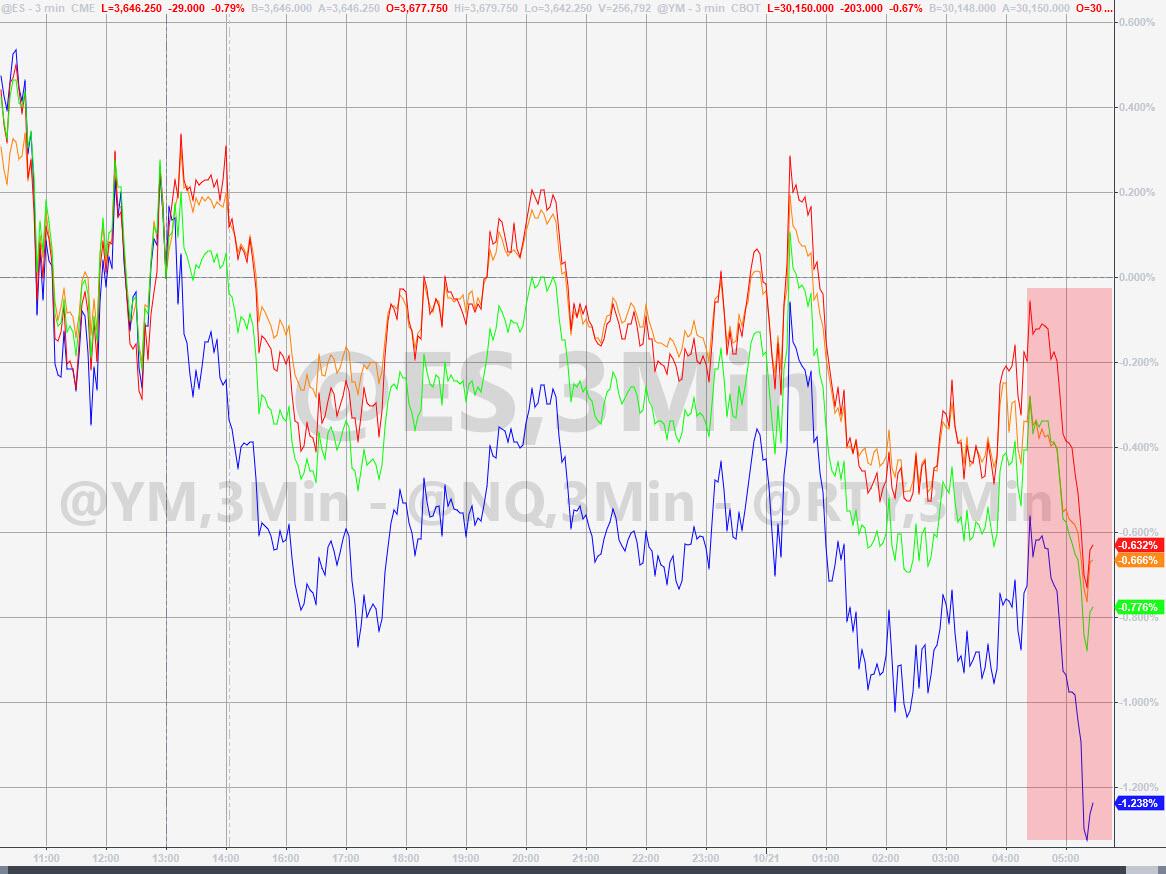

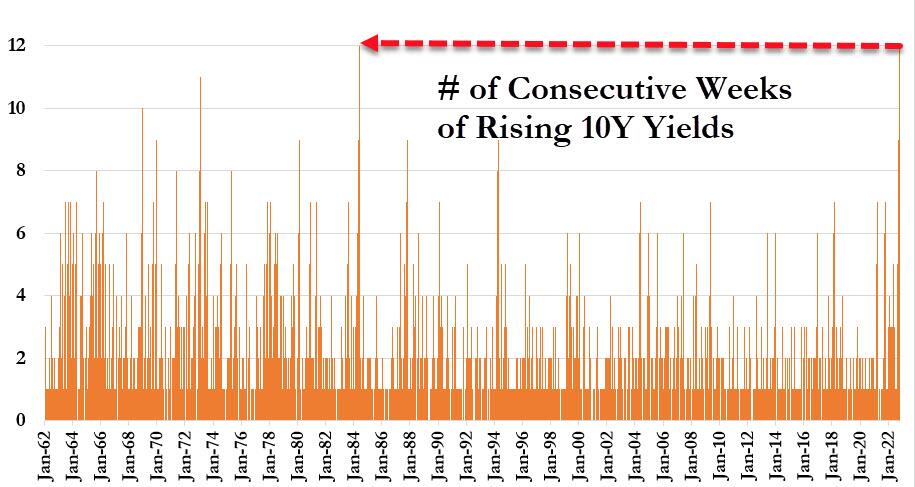

Futures Slide As Global Yields Soar, Pushing Bond Markets To Edge Of Breaking

FRIDAY, OCT 21, 2022 – 08:02 AM

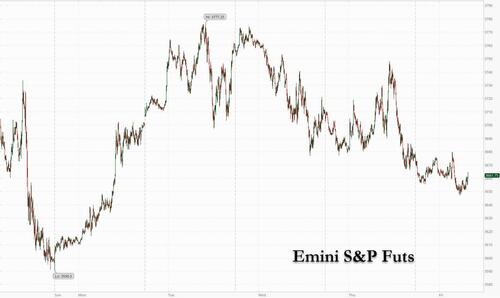

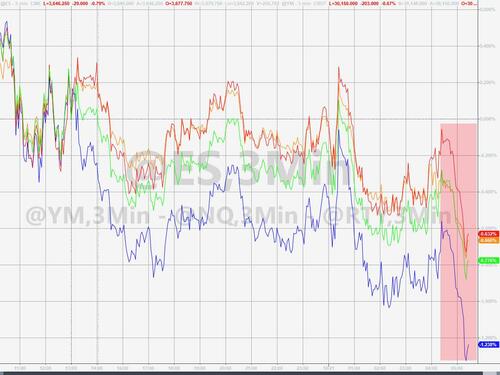

US equities extended their recent slump, set to trim their modest weekly advance even further as soaring bonds yields and poor earnings renewed the gloom that’s sent stocks into a bear market this year. Contracts on the S&P 500 dipped 0.4% at 7:30 a.m. ET, putting the underlying index on track to sharply pare this week’s 2.3% gain…

… as the yield on the 10-year Treasury rose to 4.29%, the highest since 2007 and as Treasuries dropped for a 12th consecutive week, which would match longest stretch since 1984. Fed swaps price in a 5% peak policy rate in 2023 after Philly Fed President Patrick Harker said that the Fed is likely to raise interest rates to “well above” 4% this year and hold them at restrictive levels to combat inflation,

“The global inflation bogeyman continues to scare the bond markets,” said strategists at Societe Generale SA including Ninon Bachet. “Central banks have additional big moves to make in their tightening process, so we remain short duration.”

Nasdaq 100 futures fell 0.9% after the tech-heavy gauge advanced 3.3% from Monday through Thursday. Surging yields also pushed the dollar sharply higher, with USDJPY soaring above 151.50 and the yuan falling to the weakest level since 2008.

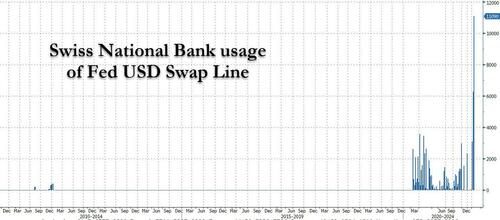

At this point, absent a Fed short-circuit of the soaring dollar (in the form of a major liquidity injection), a global currency crisis is all but assured; one look at the latest record weekly usage in the SNB swap line with the Fed confirms without a doubt that there is now a global currency shortage which is becoming more systemic by the week if not day.

In premarket trading, Twitter shares tumbled, falling as much as 16% and well below Elon Musk’s offer price, on concern the deal may be terminated by the government. Earnings from appliance maker Whirlpool and social-media platform Snap disappointed investors after the market closed Thursday. Snap plunged 27% in premarket trading Friday after its slowest quarterly sales growth ever. This sets the stage for what investors can expect when bigger players like Alphabet and Meta Platforms report next week. Earlier this week, firms among AT&T as well as IBM had beaten expectations earlier this week. Here are some of the biggest US movers today:

Whirlpool shares drop 4% in US postmarket trading after the company cut its FY ongoing EPS guidance; shares of Swedish peer Electrolux also fall.

CSX gained 3% in premarket trading. It’s unchanged FY guidance comes as a relief after peer Union Pacific cut its forecast for volume growth, Morgan Stanley analysts write after the freight transportation firm reported 3Q earnings that beat estimates.

Opendoor Technologies slides 2.5% in premarket trading after Truist Securities cut the price target to $5 from $8 as the analyst trims their margin estimates for the real estate firm.

Autoliv shares rise as much as 5.9% in premarket trading after the firm said it expects to see full-year organic revenue growth of about 15%, higher than the 14.5% that analysts had been expecting.

Under Armour shares decline 3.2% in premarket trading after Telsey Advisory Group downgrades the sportswear brand to market perform from outperform, expecting high inventory rates from Nike and Adidas to weigh on FY23 and for the company to once again cut its 2022 outlook again when it reports on November 3.

Immunic shares sink 71% in premarket trading after interim analysis of the biopharma company’s Phase 1b clinical trial of IMU-935 patients with moderate-to-severe psoriasis showed a placebo rate that Piper Sandler says was “surprisingly high.”

SVB Financial dropped 17% in premarket trading after lowering its full-year forecast for net interest income growth.

Tenet drops 18% in premarket trading after the health care company narrowed its operating revenue guidance to a level below Wall Street estimates.

As Bloomberg notes, the S&P 500 hasn’t been able to hold onto gains for more than a week since early August, a sign of persistent economic headwinds as the Federal Reserve continues raising interest rates. The earnings season will be key to dictating the direction of equities until the US central bank meets next month. Ironically, so far it is nowhere near as bad as some had suspected with 74% of companies have exceeded earnings expectations versus the long-term, prepandemic average of 72%, according to Bloomberg analysts Gina Martin Adams and Gillian Wolff.

“History tells us that markets don’t find a bottom until investors begin to anticipate rate cuts, leading indicators point to better growth, or valuations price a bear case scenario. That’s not the case today,” UBS Global Wealth Management strategists led by Mark Haefele wrote in a note. “Equity valuations, despite falling in absolute terms, don’t yet fully discount a bear case.”

Investor sentiment has turned deeply pessimistic but that’s not yet being reflected in equity flows and “final capitulation” remains elusive, according to strategists at Bank of America Corp. US funds had a second straight week of inflows at $12 billion in the week through Oct. 19, according to a note from the bank citing EPFR Global data.

European stocks fell amid the broader risk-off mood. Euro Stoxx 50 slumps 1.6% as retailers, consumer products and construction are the worst-performing sectors as all industry groups in Europe fall. Here are some of the biggest European movers today:

L’Oreal’s 3Q sales showed “hairline fractures appearing,” according to Morgan Stanley, with volumes sequentially softening, pockets of weaker demand and changing consumer behavior. The stock fell as much as 5.5%, biggest intraday drop in more than two years.

Adidas shares plunge as much as 10%, the most since March 7, after the German sportswear maker cut its outlook for the year flagging slowing demand, partly due to a weakening in footfall in China, and also because of inventory build-up, providing further warning about the consumer slowdown.

Sika shares drop as much as 5.1% despite maintaining its FY guidance, as Jefferies says a third-quarter Ebit miss may trigger mild downgrades.

Telia shares fall as muchy as 8.9% to their lowest level since 2003, as a steep increase in energy costs prompts a cut to its profit outlook, with operational free cash flow for 2022 set to be below the minimum dividend level.

PostNL declines as much as 12%, the most since May 9, after the Dutch mail carrier withdrew its FY guidance, citing rising inflation and a drop in consumer confidence which has led to 3Q under performance, particularly in parcel delivery.

Grifols shares dropped as much as 8.8% to their lowest level in 10 years following a media report that it could face legal claims in the US for as much as $270m. Banco Santander notes potential fine size could represent about 1% to 4% of plasma firm’s market cap.

Deliveroo shares rise as much as 6.2%. The food delivery firm lifted its adjusted Ebitda margin guidance for the year, making progress on plans to improve profitability amid slowing growth.

Borregaard shares climb as much as 3.7% after the specialized biochemicals supplier reports 3Q results that may push earnings per share estimates for 2023 and 2024 higher by 2%-3%, DNB analyst says in note.

Earlier in the session, Asian stocks fell, set to cap a second week of declines, as recession worries weighed on sentiment amid hawkish central-bank remarks and stringent China Covid restrictions. The MSCI Asia Pacific Index dropped as much as 1.2% Friday, with most of the markets in the region marking losses. The Hong Kong benchmark hit its lowest since April 2009, while gauges in Singapore and the Philippines declined more than 1%. China’s pandemic rules continued to weigh on regional investor sentiment amid additional lockdowns. Risk sentiment was also hurt by higher Treasury yields after a Federal Reserve official said he expects interest rates to be “well above” 4% this year.

“I think the risks for recession in the region are pretty high,” David Chao, Asia Pacific market strategist at Invesco, said in an interview with Bloomberg TV. Still, Chao believes Asia Pacific is “relatively more attractive” than Europe and the US as the region is somewhat insulated from high levels of inflation and central bank tightening. Traders will be on the watch for earnings reports in the coming days to understand the impact of high inflation and China’s virus restrictions on corporate health and growth. Down about 30% this year, the key Asian stock gauge is trading near its lowest level since April 2020.

Japanese stocks fell, as losses in chemical makers and railways offset gains in electronics makers. Japan’s core inflation reached 3% for the first time in over three decades excluding tax-hike impacts. The Topix fell 0.7% to close at 1,881.98, while the Nikkei declined 0.4% to 26,890.58. The yen slightly extended its loss after falling through 150 per dollar Thursday. Sony Group Corp. contributed the most to the Topix Index decline, decreasing 1.5%. Out of 2,166 stocks in the index, 442 rose and 1,626 fell, while 98 were unchanged

Australian stocks also slid as banks, property shares weigh; the S&P/ASX 200 index fell 0.8% to close at 6,676.80, with banks and real estate stocks leading the declines. All sectors slumped except for energy as oil gained. The benchmark notched a second week of declines, down 1.2%. In New Zealand, the S&P/NZX 50 index fell 0.5% to 10,782.36.

India stocks posted their biggest weekly gain since July as investor sentiment was buoyant ahead of a key festival next week while corporate earnings season gathers steam. The S&P BSE Sensex rose 0.2% to 59,307.15 in Mumbai, while the NSE Nifty 50 Index was little changed. Both the gauges rose at least 2.3% this week. All but three of BSE Ltd.’s 19 sector sub-indexes declined, led by capital goods companies. For the week, banking stocks were the best performers, thanks to strong earnings performances by top lenders including HDFC Bank. After a stronger-than-expected quarterly performances by technology and banking companies, earnings were starting to reflect worries over elevated costs. Of 17 Nifty 50 Index firms, which have posted results so far, 11 have either met or surpassed the consensus view while five have missed.

In FX, the Bloomberg Dollar Spot Index roared higher after whipsawing in early European hours; the greenback rose against all its Group-of-10 peers. Long-dated Treasuries fell, driving the 10-year benchmark yield to a 15-year high, as traders bet the Federal Reserve will press ahead with rate hikes to defeat inflation.

The euro reversed an early European session gain and bonds from the region fell across the board. Germany’s 10-year yield climbed above 2.5% for first time since 2011.

The pound fell against all of its G-10 peers and tumbled as much as 1.2%, while gilts sold off as markets entered another bout of uncertainty amid a truncated leadership contest following the resignation of Liz Truss. The next leader could be decided as soon as Monday. The UK budget deficit in September exceeded estimates

The yen fell beyond 151 per dollar as the disparity between US and Japanese yields continued to grow, putting the currency on track for a 10th straight weekly loss. The relative premium to own exposure in short-term dollar-yen options rose to levels not seen for more than six years due to the risk of intervention as realized volatility remains in defensive mode. The Bank of Japan will keep conducting monetary easing to support the economy and sustainably and stably achieve its price target accompanied by wage growth, Governor Haruhiko Kuroda said in a speech in Tokyo. Finance Minister Shunichi Suzuki told reporters that Japan is firmly confronting forex speculators in the market now.

The onshore yuan fell to the weakest level since 2008 as the greenback surged on hawkish comments from a Federal Reserve official.

In rates, Treasuries dropped for 12th week, which would match longest stretch in 38 years. BOJ boosted bond purchases to hold 10-year yield at 0.25% ceiling, while Australian bonds drop. Longer-dated Treasuries extended Thursday’s declines, steepening 2s10s and 5s30s spreads by at least 4bp into early US session. Bigger bear-steepening move grips German curve as 10-year yields top 2.5% for first time since 2011. US yields were cheaper by nearly 7bp across long-end of the curve with 2s10s, 5s30s spreads steeper by about 4.5bp and 6.5bp on the day. German long-end yields are cheaper by 11.5bp on the day while Gilts 10-year yield rose 8bps, trading around 4% as traders add BOE and ECB rate-hike premium.

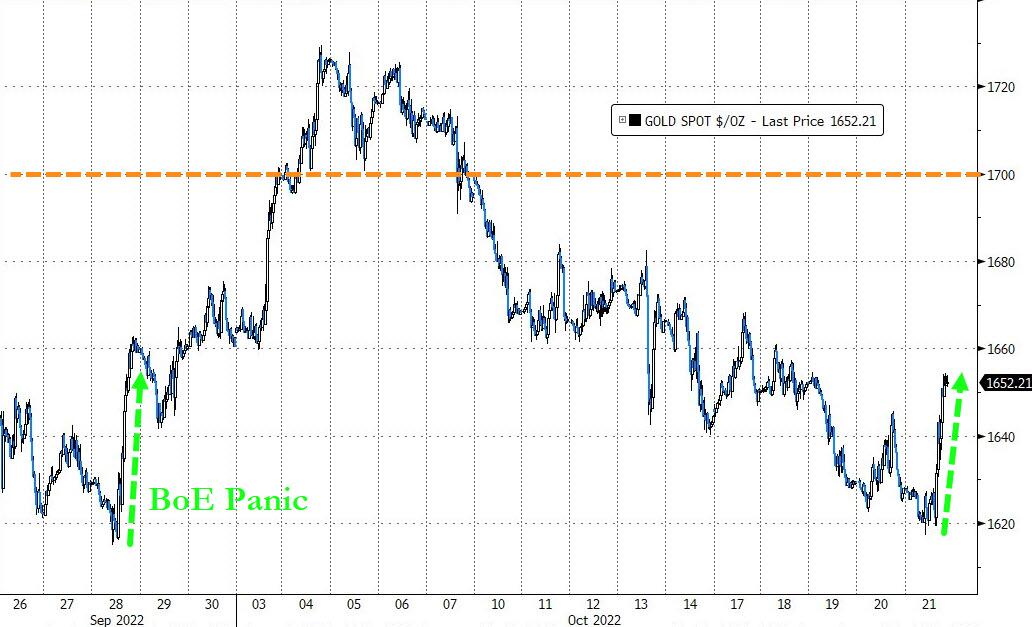

In commodities, WTI drifts 1.6% lower to trade near $83.19, but off lows amid the firmer Dollar and deterioration of broader risk sentiment. Saudi and China are said to be ready to cooperate oil market stability; Saudi remains the most trusted China oil supplier, according to a joint statement cited by Bloomberg. LME metals are lower across the board with 3M copper also weighed on by the risk mood – the red metal trades on either side of USD 7,500/t. Spot gold posts modest losses and remains under USD 1,650/oz after dipping below yesterday’s lows.

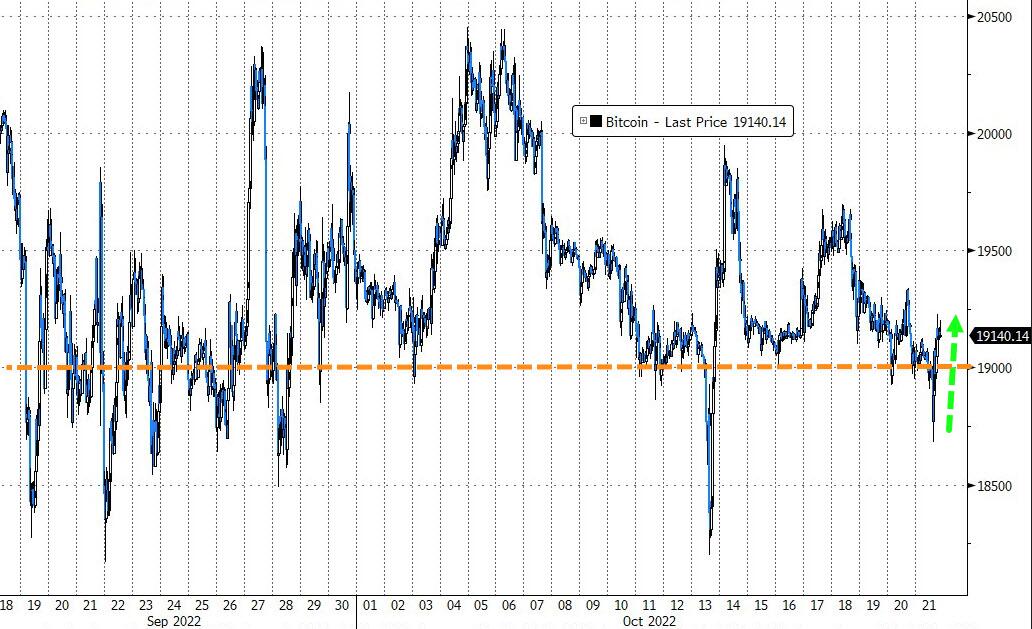

Bitcoin is under pressure and has lost the USD 19k handle and lies at the lower-end of a circa USD 700 range for the session.

Looking to the day ahead now, data releases include UK retail sales for September and the US Monthly budget statement. From central banks, we’ll hear from New York Fed President Williams. Finally, earnings releases include Verizon Communications and American Express.

Market Snapshot

S&P 500 futures down 0.6% to 3,653.00

STOXX Europe 600 down 1.4% to 393.11

MXAP down 1.1% to 135.34

MXAPJ down 0.9% to 438.50

Nikkei down 0.4% to 26,890.58

Topix down 0.7% to 1,881.98

Hang Seng Index down 0.4% to 16,211.12

Shanghai Composite up 0.1% to 3,038.93

Sensex up 0.2% to 59,347.19

Australia S&P/ASX 200 down 0.8% to 6,676.76

Kospi down 0.2% to 2,213.12

German 10Y yield up 3.7% at 2.49%

Euro down 0.2% at $0.9758

Brent Futures down 1% to $91.45/bbl

Gold spot down 0.4% to $1,621.21

U.S. Dollar Index up 0.42% to 113.357

Top Overnight News from Bloomberg

Giorgia Meloni clinched a mandate from her coalition on the path to becoming Italy’s first female premier, after weeks of political stasis following her right-wing alliance’s election win

The UK Treasury may be forced to delay its long-awaited Oct. 31 fiscal plan because of the resignation of Prime Minister Liz Truss, adding a layer of political risk to an event that had become crucial for markets and the Bank of England

The Conservative Party is desperate to draw a line under Truss’s disastrous premiership, with a rapid leadership contest aimed at trying to give the winner a shot at overturning an unprecedented deficit in the polls

Regardless of who wins the race to succeed Truss as UK Prime Minister, one thing is clear: the pound is set to keep falling. That’s the prognosis of market players who see sterling continuing its descent as economic headwinds and the Bank of England’s policy stance act as a drag

Traders in UK government bonds helped topple Truss. Now they’re setting their sights on the next goal: ensuring her successor will stick to the fiscal discipline required to shore up the country’s fragile finances

UK retail sales fell more than expected last month after the death of Queen Elizabeth II curtailed activity and cost-of- living pressures hit harder. The volume of goods sold in shops and online dropped 1.4% in September after a revised 1.7% decline the month before. Economists had expected an 0.5% drop

ECB officials are considering whether to add a new overnight interest rate to co-exist with its three existing levers to manipulate the cost of money, Expansion reported, citing people familiar with the matter

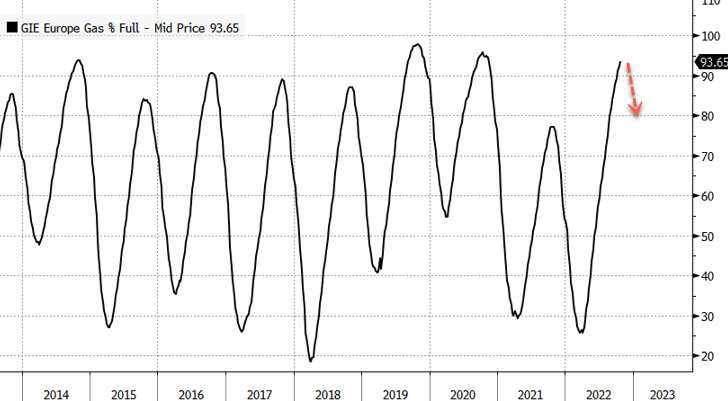

The EU agreed to press ahead with a set of emergency actions to address the bloc’s energy crisis, with Germany yielding to pressure from other member states to pave the way for a temporary price cap on natural gas. European natural gas prices fell after the accord

US Treasuries have entered the longest sustained slump in 38 years, as policy makers signal their determination to keep raising rates until they are sure inflation is under control

The Communist Party’s list of Central Committee members released Saturday will be scrutinized by economists for what it means for the People’s Bank of China. Governor Yi Gang, 64, and Guo Shuqing, 66, who is party chief and deputy governor at the central bank, are around the official retirement age, fueling speculation over whether they’ll remain in their posts

China’s yuan is expected to weaken further after the Communist Party Congress ends this weekend, as the central bank loosens its grip on the currency, according to market watchers

A More detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded cautiously with the region lacking firm direction following the weak lead from Wall Street where stocks reversed initial gains amid mixed data releases and continued upside in yields. ASX 200 was dragged lower by underperformance in industrials and the top-weighted financials sector, while the Australian Treasurer also flagged a 25bps hit to Q4 GDP from recent floods. Nikkei 225 was slightly softer after mostly inline inflation data which showed Core CPI at its fastest pace of increase since 2014 and as participants remained on alert for intervention after the JPY weakened beyond the 150.00 level for the first time since 1990. Hang Seng and Shanghai Comp. were indecisive heading towards the conclusion of the Communist Party Congress and pending release of delayed key data. Furthermore, Chinese press reports noted analysts see room for an LPR cut by year-end, although there was also the threat of further tech restrictions with the US eyeing expanding its China tech ban to quantum computing and A.I. products.

Top Asian News

US is reportedly eyeing expanding its China tech ban to quantum computing and AI products, according to Bloomberg.

Australian PM Albanese said he is concerned about a delay to the implementation of the UK-Australia trade agreement amid UK political instability, according to Reuters.

Australian Treasurer Chalmers said the latest floods are to cut 25bps from GDP growth in the December quarter, while floods will add 10bps to inflation in December and March quarters, according to Reuters.

India Rate-Setter Wants RBI to Focus on Softening Core Inflation

China Market Revival Hopes in Tatters as Congress Disappoints

Hong Kong Cancels Screening of Batman Film Shot in the City

Chinese City Plans Offshore Wind Farm That Could Power Norway

Asian Development Bank Approves $1.5 Billion Loan for Pakistan

Cash bourses in Europe started the session with losses which then extended to the downside as market sentiment further deteriorated. Sectors in Europe are in a sea of red, but defensive sectors are faring better than cyclical peers, with Healthcare, Food & Beverages, Optimised Personal Goods, and Utilities towards the top of the bunch, whilst Retail, Consumer Products, Construction, Real Estate, and Basic Resources reside on the other end of the spectrum. US equity futures are also softer across the board with the NQ (-0.9%) lagging its peers (ES -0.6%, RTY -0.5%, YM -0.4%) as bond yields continue to climb. SNAP (SNAP) – Q3 2022 (USD): Adj. EPS 0.08 (exp. 0.00), Revenue 1.128 (exp. 1.14bln). Daily active users rose 19% Y/Y to 363mln (exp. 358.7mln), sees Q4 DAU of about 375mln. Quarterly sales growth was slowest on record. Authorized a stock repurchase program of up to USD 500mln of its Class A common stock. Not providing formal Q4 guidance and sees it as highly likely that Y/Y revenue growth will decelerate as we move through Q4, due in large part to the fact that Q4 has historically been relatively more dependent on brand-oriented advertising revenue, which declined slightly on a Y/Y basis in the most recent quarter. Estimate adj. EBITDA would be about USD 200mln under about flat Y/Y revenue growth assumption for D4. (businesswire) -25% in the pre-market. US government is reportedly mulling a security review regarding Elon Musk’s deal to acquire Twitter (TWTR), according to Bloomberg. Additionally, Elon Musk is said to have told prospective investors that he planned to cut almost 75% of Twitter (TWTR) workers, according to documents cited by Washington Post. CATL slows battery investment plans in N. America, according to Reuters sources; due to concern that new US rules around sourcing battery material will increase costs.

Top European News

German Parliament votes to approve the suspension of the debt brake, via Reuters.

Italy’s Meloni says she has been proposed by the rightist coalition as PM to President Mattarella, via Reuters.

The ECB is planning to create a new interest rate, according to Expansion.

Adidas’s Unsold Sneakers and Problems Are Piling Up for Next CEO

Renault Slips as Inflation Worries Offset Revenue Gains

French Central Banker Warns Against Algos in Currency Trading

Credit Suisse Set to Settle Criminal Tax Case in France

FX

DXY has continued to benefit from further yield upside with the 10-yr eclipsing 4.25% and the index to a 113.50+ best.

As such, peers across the board are hampered with GBP lagging and approaching 1.11 amid the latest bout of political turmoil.

EUR/USD seemingly found support as it neared the 0.97 mark and conscious of multiple chunky OpEx for the NY Cut.

Traditional havens are also dented despite risk sentiment given differentials weighing; USD/JPY has risen to a test of 151.00, with participants attentive for any BoJ/MoF reaction.

Antipodeans are unable to escape the USD’s ascendance with CAD similarly dented, but off worst, amid the most recent paring of crude losses.

China’s major state-owned banks are seen selling USD in the onshore spot market to stabilise the Yuan, according to Reuters sources; meant to prevent the spot price from weakening past 7.25.

Fixed Income

Debt has extended on initial downbeat performance amid Germany approving the debt brakes suspension to fund their EUR 200bln energy support scheme.

As such, Bunds are subdued by over a full point; though, amid ongoing political turmoil, Gilts remain the laggard and briefly lost the 97.00 handle sending the corresponding yield back above 4.0%.

Stateside, USTs are similarly pressured though a touch more contained ahead of Fed’s Williams as we near the blackout period.

Elsewhere, the periphery has been unreactive to the as-expected announcement that the Italian coalition has put Meloni forward to become PM.

Commodities

WTI and Brent December contracts are lower intraday but off lows amid the firmer Dollar and deterioration of broader risk sentiment.

Spot gold posts modest losses and remains under USD 1,650/oz after dipping below yesterday’s lows.

LME metals are lower across the board with 3M copper also weighed on by the risk mood – the red metal trades on either side of USD 7,500/t.

Saudi and China are said to be ready to cooperate oil market stability; Saudi remains the most trusted China oil supplier, according to a joint statement cited by Bloomberg.

EU Council President Michel said the European Council reached an agreement on energy and agreed to work on measures to contain energy prices, according to Bloomberg.

Belgium PM says it will take 2-3 weeks for energy ministers to come up with how to implement the gas price cap, via FT’s Bounds; two energy ministers summit will probably be needed to agree energy package, via WSJ’s Norman.

Hungary’s PM Orban said an agreement was reached that even if the EU imposes a gas price cap, long-term supply agreements will be exempt, according to a Facebook post.

US Treasury Official estimates that Russia has sufficient tankers and services to trade about 80-90% of its oil, following the December 5th sanctions; circa. 1-2mln BPD of Russian crude and refined products could be shut in if they resist the price cap, via Reuters.

Geopolitcs

US Secretary of State Blinken said they take the Russian threat to use nuclear weapons seriously but have not yet seen a reason to change our nuclear status, according to Al Jazeera.

EU could reinforce sanctions on Iran if support for Russia isn’t wound back; “Several leaders said they’d be open to additional sanctions this morning.”, according to WSJ’s Norman.

US Secretary of State Blinken said they place great emphasis on making sure the differences between China and Taiwan are resolved peacefully and not through coercion or force, according to Al Jazeera.

US Event Calendar

3:15 p.m. ET: President Joe Biden delivers remarks on student debt relief in Dover, Delaware

Central Bank Speakers

09:10: Fed’s Williams Makes Opening Remarks at Careers Event

09:40: Fed’s Evans Speaks at Community Banking Symposium

DB’s Jim Reid concludes the overnight wrap

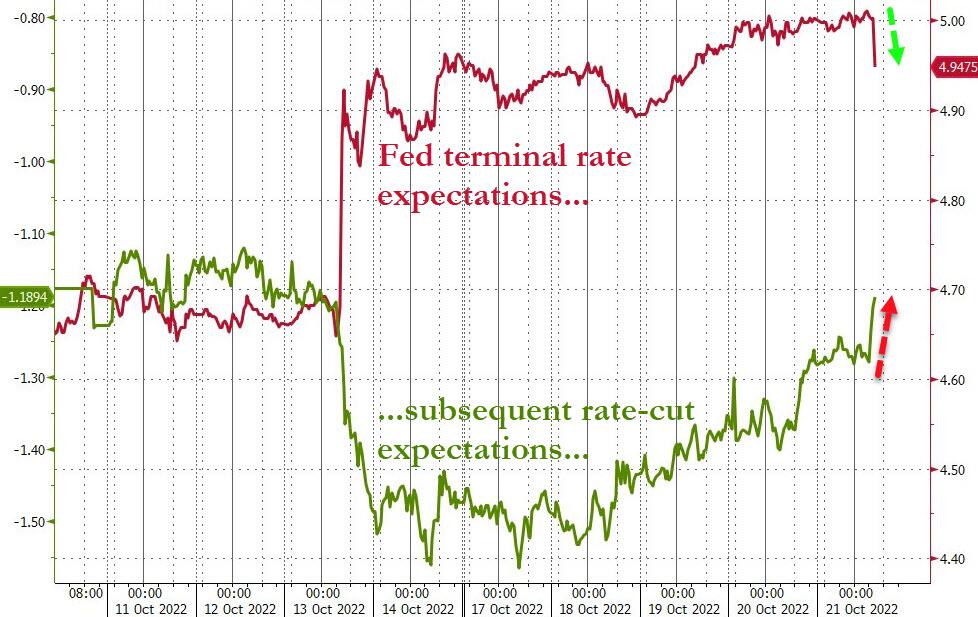

Risk assets struggled and sovereign bond yields hit fresh multi-year highs yesterday as investors moved to price in the most aggressive path for central bank rate hikes so far. In fact, there was a notable milestone for Fed funds futures, since by the close they expected the Fed to take rates above 5% next year, which is the first time that futures for an upcoming meeting have closed that high in this cycle so far. Bear in mind that on the day of Chair Powell’s hawkish Jackson Hole speech in late-August they closed at 3.78% for the March meeting, so the stronger-than-expected inflation prints over the last couple of months have led to a big reappraisal in how hawkish the Fed and other central banks are expected to be.

Those increasingly hawkish expectations drove a fresh selloff in US Treasuries, with the 10yr yield up +9.5bps to close at 4.23%. That’s their highest level since 2008, and came as the 10yr real yield (+4.0bps) hit a post-2009 high of its own at 1.74%. And those rises have continued overnight, with 10yr yields up another +2.7bps to a new high of 4.26% as we go to print. Those moves have been partly supported by stronger-than-expected data, with the weekly initial jobless claims for the week ending October 15 unexpectedly falling to 214k (vs. 233k expected), which was seen as giving the Fed more space to keep hiking rates. But we also had a fresh round of speakers from the Fed, including Philadelphia Fed President Harker, who said that he expected rates to be “well above” 4% by the end of the year. In the meantime, Governor Cook reiterated the message from Chair Powell that the Fed would “keep at it until the job is done”, and that this would “likely will require ongoing rate hikes and then keeping policy restrictive for some time.” Remember that today is the last we’ll hear from any FOMC members, as the Fed will then be entering its blackout period ahead of the next meeting a week on Wednesday.

Central bank hawkishness had a knock-on effect on equities too, with the S&P 500 (-0.80%) losing ground for a second day running, reversing course from its early gains when it had been on track to hit a 2-week high. Those declines were led by the more cyclical sectors, but it was a broad-based move that saw over three-quarters of the index’s members lose ground on the day. Small-cap stocks underperformed in particular, with the Russell 2000 down -1.24%, whereas the Dow Jones only shed -0.30%. European equities had a comparatively better performance though, having closed before the US selloff, and the STOXX 600 advanced +0.26%.

Whilst markets are gearing up for the next round of central bank decisions, here in the UK we’re also set to have another Prime Minister by the end of next week after Liz Truss announced her resignation yesterday after just 44 days in office. That’ll mean she’s the shortest-serving PM in UK history, and caps off a brief but tumultuous period in office, with the turning point occurring on September 23 when the government’s mini-budget triggered market turmoil that eventually led the government to U-turn on most of what they announced that day. The mini-budget also led to a sharp decline in the Conservatives’ polling position against the backdrop of large rises in mortgage rates, with the opposition Labour Party seeing their largest poll leads since the late-1990s. As such, we saw growing numbers of Conservative MPs withdraw their support from Truss over recent days, ultimately leading to her resignation yesterday.

In terms of what happens next, there’s now going to be another Conservative leadership election to select the next Prime Minister, in a short contest that’ll conclude by Friday October 28 at the latest. Candidates will require nominations from 100 MPs by Monday afternoon to go onto the ballot, which means there can only be a maximum of three anyway. MPs will then vote on Monday to take that down to two candidates for grassroots Conservative members to vote on. But unlike before, MPs will also hold an indicative vote between the final two, and it’s certainly possible that the losing candidate comes under significant pressure to drop out, so we could potentially know the next PM by Monday.

When it comes to who’ll be the next PM, the bookmakers’ favourite is former Chancellor Rishi Sunak, who was the runner-up to Liz Truss over the summer. But speculation is also swirling around former PM Boris Johnson, who the Times newspaper reported is expected to stand in the contest, and who a number of Conservative MPs have already publicly endorsed.

In terms of the market reaction, there weren’t any discernible moves in response to Truss’ resignation. Sterling only saw a small movement of +0.14% against the US Dollar, and the moves in 10yr gilt yields (+2.9bps) echoed those in other European countries. However, one development that led investors to dial back the amount of rate hikes priced in for the coming months was a speech by BoE Deputy Governor Broadbent, who said that “Whether official interest rates have to rise by quite as much as currently priced in financial markets remains to be seen”.

As with gilts, sovereign bonds elsewhere in Europe lost ground, with yields on 10yr bunds (+2.8bps) rising to a post-2011 high of 2.39%. That followed growing expectations that the ECB were set to maintain their hawkish stance over the coming months, with the deposit rate priced in by overnight index swaps for the March meeting up a further +4.5bps to a new high of 2.76%, and this morning it’s up another +6.2bps to 2.82%. That rise in yields was driven by higher inflation breakevens yesterday rather than real rates, which wasn’t helped by the fact that natural gas futures rebounded by +13.01% to €127 per megawatt-hour, ending a run of 5 consecutive daily declines.

Overnight in Asia, the major equity indices have been struggling overnight as bond yields continue to rise. That’s seen the Nikkei (-0.33%), the Hang Seng (-0.17%) and the Kospi (-0.33%) all lose ground, although the CSI 300 (+0.15%) and the Shanghai Comp (+0.50%) have both made gains. US and European equity futures have similarly fallen back, with contracts tied to the S&P 500 (-0.23%) and the NASDAQ 100 (-0.57%) are both lower. Snap reported their weakest sales ever quarterly sales growth, up just 6% in Q3.

Elsewhere in Asia, the other big piece of news was that the Japanese Yen weakened through 150 per dollar for first time since 1990 just after we went to press yesterday. It’s now currently trading at 150.40, putting it well on track for a 10th consecutive weekly decline against the dollar. In response, finance minister Suzuki said that there had been “absolutely no change to our thinking that we’ll take an appropriate response against excessive moves”. The moves also came as Japanese inflation remained strong, with CPI staying at +3.0% (vs. +2.9% expected), and CPI excluding fresh food up to +3.0% as expected. Apart from the jump in 2014 following the sales tax hike, that’s the highest that core measure has been since 1991.

Looking at yesterday’s other data, US existing home sales fell to an annualised rate of 4.71m in September (vs. 4.70m expected), which is their lowest level in a decade if you exclude the pandemic months of April and May 2020. Meanwhile in Germany, producer price inflation remained at +45.8% year-on-year in September (vs. +45.4% expected).

To the day ahead now, and data releases include UK retail sales for September. From central banks, we’ll hear from New York Fed President Williams. Finally, earnings releases include Verizon Communications and American Express.

AND NOW NEWSQUAWK

Sentiment slips & NQ lags while DXY climbs and USD/JPY breaches 151.00 – Newsquawk US Market Open

FRIDAY, OCT 21, 2022 – 06:43 AM

Equities began the session on the backfoot and have extended to the downside, with the NQ lagging stateside post-SNAP.

SNAP -25% in the pre-market; TWTR -8%, with the US reportedly to review Musk’s deal

USD continues to climb with the index above 113.50 at best while USD/JPY tests 151.00 and Cable near 1.11

Debt has extended on initial downbeat performance amid Germany approving the debt brakes suspension; UK 10yr back above 4.00%

Crude complex is softer on the session but off worst levels amid reports that China and Saudi are to cooperate on oil market stability

Looking ahead, highlights include Sovereign Debt Ratings for the UK, Germany, Czech and Italy, Speech from Fed’s Williams

Cash bourses in Europe started the session with losses which then extended to the downside as market sentiment further deteriorated.

Sectors in Europe are in a sea of red, but defensive sectors are faring better than cyclical peers, with Healthcare, Food & Beverages, Optimised Personal Goods, and Utilities towards the top of the bunch, whilst Retail, Consumer Products, Construction, Real Estate, and Basic Resources reside on the other end of the spectrum.

US equity futures are also softer across the board with the NQ (-0.9%) lagging its peers (ES -0.6%, RTY -0.5%, YM -0.4%) as bond yields continue to climb.

SNAP (SNAP) – Q3 2022 (USD): Adj. EPS 0.08 (exp. 0.00), Revenue 1.128 (exp. 1.14bln). Daily active users rose 19% Y/Y to 363mln (exp. 358.7mln), sees Q4 DAU of about 375mln. Quarterly sales growth was slowest on record. Authorized a stock repurchase program of up to USD 500mln of its Class A common stock. Not providing formal Q4 guidance and sees it as highly likely that Y/Y revenue growth will decelerate as we move through Q4, due in large part to the fact that Q4 has historically been relatively more dependent on brand-oriented advertising revenue, which declined slightly on a Y/Y basis in the most recent quarter. Estimate adj. EBITDA would be about USD 200mln under about flat Y/Y revenue growth assumption for D4. (businesswire) -25% in the pre-market

US government is reportedly mulling a security review regarding Elon Musk’s deal to acquire Twitter (TWTR), according to Bloomberg. Additionally, Elon Musk is said to have told prospective investors that he planned to cut almost 75% of Twitter (TWTR) workers, according to documents cited by Washington Post.

CATL slows battery investment plans in N. America, according to Reuters sources; due to concern that new US rules around sourcing battery material will increase costs.

DXY has continued to benefit from further yield upside with the 10-yr eclipsing 4.25% and the index to a 113.50+ best.

As such, peers across the board are hampered with GBP lagging and approaching 1.11 amid the latest bout of political turmoil.

EUR/USD seemingly found support as it neared the 0.97 mark and conscious of multiple chunky OpEx for the NY Cut.

Traditional havens are also dented despite risk sentiment given differentials weighing; USD/JPY has risen to a test of 151.00, with participants attentive for any BoJ/MoF reaction.

Antipodeans are unable to escape the USD’s ascendance with CAD similarly dented, but off worst, amid the most recent paring of crude losses.

China’s major state-owned banks are seen selling USD in the onshore spot market to stabilise the Yuan, according to Reuters sources; meant to prevent the spot price from weakening past 7.25.

Debt has extended on initial downbeat performance amid Germany approving the debt brakes suspension to fund their EUR 200bln energy support scheme.