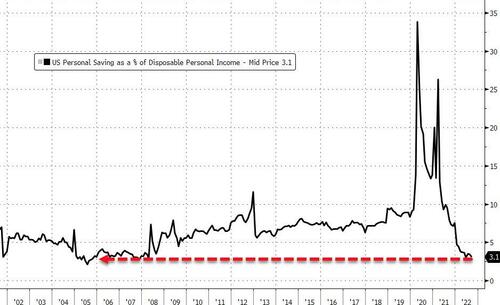

OCT 28/OPTIONS EXPIRY ENDS ON MONDAY AND THUS YOUR USUAL AND CUSTOMARY RAID ON OUR PRECIOUS METALS: GOLD CLOSED DOWN $19.70 TO $1641.70//SILVER WAS DOWN $.35 TO $19.18//PLATINUM WAS DOWN $17.60 TO $946.50//PALLADIUM WAS DOWN $41.85 TO $1902.05//COVID UPDATES: DR PAUL ALEXANDER//VACCINE IMPACT//ELON MUSK TAKES OVER TWITTER AND FIRES THE UPPER ECHELON OVER THERE AND RESTORES ALL OF THOSE WHO HAD A LIFETIME BAN//RUSSIA WARNS THE WEST THAT NON MILITARY SATELLITES ARE NOW LEGITIMATE TARGETS: E.G.MUS’S STARLINK//FINDLAND WILLING TO HOST NUCLEAR WEAPONS ON ITS BORDER WITH RUSSIA (A DUMB MOVE)//ISRAEL ATTACKS IRANIAN ASSETS INSIDE SYRIA AGAIN//USA CITIZENS SAVINGS RATE PLUMMETS//SWAMP STORIES FOR YOU TONIGHT///

132 C SG AMERICAS 16 323 C HSBC 272 435 H SCOTIA CAPITAL 261 624 H BOFA SECURITIES 1055 657 C MORGAN STANLEY 1 661 C JP MORGAN 113 2 732 C RBC CAP MARKETS 57 880 C CITIGROUP 1 880 H CITIGROUP 1195 991 H CME 1

TOTAL: 1,487 1,487

JPMORGAN STOPPED 2/1487

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 1487 NOTICES FOR 148,700 OZ or 4.6251 TONNES

total notices so far: 24,881 contracts for 2,488,100 oz (77.390 tonnes)

SILVER NOTICES: 27 NOTICE(S) FILED FOR 135000 OZ/

total number of notices filed so far this month 716 : for 3,580,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $19.70

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////A BIG CHANGE IN GLD INVENTORY: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD// /INVENTORY LOWERS TO 925.20 TONNES

INVENTORY RESTS AT 928.39 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 35 CENTS

AT THE SLV// :/SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF OF .276 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 484.367 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A TINY SIZED 58 CONTRACTS TO 139,885 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE TINY GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR SMALL $0.03 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS/HFT WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.03)., AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS, AS WE HAD A VERY STRONG GAIN IN OUR TWO EXCHANGE OF 868 CONTRACTS. HUGE SPECS CONTINUE TO ADD TO THEIR SHORTFALLS FROM WHICH OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. SOME SPEC LONGS ADDED TO THEIR POSITIONS

WE MUST HAVE HAD: I) ZERO SPECULATOR SHORT COVERINGS BUT STRONG SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /// CONSIDERABLE NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING A ZERO OZ QUEUE. JUMP / // V) TINY SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: +15

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 22 days, total 57,895 contracts: 28.947 million oz OR 1.315MILLION OZ PER DAY. (263 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 28.947 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 28.947 MILLION OZ INITIAL

RESULT: WE HAD A TINY SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 58WITH OUR $0.03 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A VERY STRONG SIZED EFP ISSUANCE CONTRACTS: 825 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S ZERO OZ QUEUE JUMP .. WE HAD A VERY STRONG SIZED GAIN OF 883 OI CONTRACTS ON THE TWO EXCHANGES FOR 4.415 MILLION OZ..

WE HAD 27 NOTICE(S) FILED TODAY FOR 135,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2992 CONTRACTS TO 460,721 AND CLOSER TO FROM TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -850 CONTRACTS.

.

THE FAIR SIZED INCREASE IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $3.80//COMEX GOLD TRADING/THURSDAY // ZERO SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION AND CONSIDERABLE SPEC SHORT ADDITIONS BUT MINOR SPEC SHORT COVERINGS. // CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 41,100 OZ//NEW STANDING 77.390TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR FALL IN PRICE OF $3.80 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A VERY STRONG SIZED GAIN OF 8860 OI CONTRACTS 27.558 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5868 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 460,721

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8860 CONTRACTS WITH 2992 CONTRACTS INCREASED AT THE COMEX AND 3842 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 8860 CONTRACTS OR 30.202 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5869) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (2992): TOTAL GAIN IN THE TWO EXCHANGES 8860 CONTRACTS. WE NO DOUBT HAD 1) STRONG SPECULATOR SHORT ADDITIONS// CONTINUED GOOD BANKER ADDITIONS/// ZERO SPEC SHORT COVERINGS// CONSIDERABLE NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S HUGE 41,100 OZ QUEUE JUMP ///NEW STANDING 77.390 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

55,398 CONTRACTS OR 5,539,800 OZ OR 172.311 TONNES 22 TRADING DAY(S) AND THUS AVERAGING: 2518 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 22 TRADING DAY(S) IN TONNES: 172.311 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 172.311/3550 x 100% TONNES 4.84% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 172.31 TONNES INITIAL ( MUCH SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A TINY SIZED 58 CONTRACT OI TO 139,885 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 82 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 825 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 82 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 58 CONTRACTS AND ADD TO THE 825 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A VERY STRONG SIZED GAIN OF 883 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 4.414MILLION OZ//

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 66.98 PTS OR 2.25% //Hang Seng CLOSED DOWN 564.88 OR 3.66% /The Nikkei closed DOWN 240.04 PTS OR 0.88% //Australia’s all ordinaires CLOSED DOWN 0.98% /Chinese yuan (ONSHORE) closed DOWN TO 7.2508 //OFFSHORE CHINESE YUAN DOWN 7.2752// /Oil DOWN TO 85.45 dollars per barrel for WTI and BRENT AT 96.35 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2992 CONTRACTS TO 461,571 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS FAIR COMEX INCREASE OCCURRED DESPITE OUR FALL IN PRICE OF $3.80 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (5868 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5868EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 5868 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5868 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 8860 CONTRACTS IN THAT 5868LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 3842 CONTRACTS..AND THIS STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $3.80//WE HAD CONSIDERABLE SPEC SHORTS ADDITIONS, WITH BANKERS AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD STRONG ADDITIONAL NEWBIE SPECS GOING LONG

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (77.390),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $3.80) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS// SPEC SHORTS ADDED TO THEIR POSITIONS AS WE HAD A VERY STRONG SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 8860 CONTRACTS // WE HAVE REGISTERED A VERY STRONG GAIN OF 30.202 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (77.390 TONNES)…THIS WAS ACCOMPLISHED WITH OUR FALL IN PRICE OF $3.80

WE HAD -850 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 8860 CONTRACTS OR 886,000 OZ OR 27.558 TONNES

Total monthly oz gold served (contracts) so far this month

24,881 notices 2,488,100 77.390 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals:2

ii) Out of Brinks 675.17 (21 kilobars)

iii) Out of Loomis 34,533.718.718 oz

total: 35,108.888 oz

total in tonnes: 1.09 tonnes

Adjustments: 2// customer to dealer

i)Out of Loomis 7426.881 oz

ii)Out of Brinks 385.817 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 1487 contracts having GAINED 408 contracts . We had 3 contracts

filed on THURSDAY, so we GAINED A HUGE 411 contracts or an additional 41100 oz will stand in this active delivery month of Oct. We no doubt have resumed queue jumping and gold standing will increase until the end of October.

November SHOCKINGLY ADDED A MONSTROUS 207 contracts to stand at 3990 (WE ARE GOING TO HAVE AN EXTRAORDINARILY LARGE NOV.GOLD DELIVERY . I AM INCREASING WHAT WILL STAND TO AROUND 12 TONNES OF GOLD.)

December GAINED 151 contracts UP to 360,703

We had 1487 notice(s) filed today for 148700 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 113 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1487 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 2 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (24,881) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 1487 CONTRACTS) minus the number of notices served upon today 1487 x 100 oz per contract equals 2,488,100 OZ OR 77.390 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (24,881) x 100 oz+ (1487) OI for the front month minus the number of notices served upon today (1487} x 100 oz} which equals 2,488,100 oz standing OR 77.390 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 77.390 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM TOMORROW ONWARD UNTIL THE END OF THE MONTH.

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 716 x 5,000 oz = 3,580,000 oz

to which we add the difference between the open interest for the front month of OCT(27) and the number of notices served upon today 27 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 716 (notices served so far) x 5000 oz + OI for front month of OCT (27) – number of notices served upon today (27) x 5000 oz of silver standing for the OCT contract month equates 3,580,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

TONNES

GLD INVENTORY: 925.20 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: AWITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

CLOSING INVENTORY 484.367 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

3.Chris Powell of GATA provides to us very important physical commentaries

Modi’s plan is the exactly how Einstein defines insanity. Try the same modus operandi hoping for a different outcome.

He has tried this several times and each time, he has failed. Indian citizens wil never give up their gold

(Bloomberg./comex)

Modi plan to unlock India’s gold gets new focus amid near-record trade gap

Submitted by admin on Thu, 2022-10-27 23:38Section: Daily Dispatches

By Adrija Chatterjee, Swansy Afonso, and Shruti Srivastava Bloomberg News Thursday, Octrober 27, 2022

India’s wide trade deficit is highlighting a curious government plan to rein in the gap: Getting people to hand over their private stashes of gold jewelry.

Prime Minister Narendra Modi and his government have been trying to convince gold-obsessed citizens — who collectively own the biggest private holding of bullion in the world — to deposit their treasures with banks and earn interest.

The plan, which dates back seven years, has been a resounding flop, luring only about 25 tons of the 25,000 the World Gold Council estimates is held by households and temples in the south Asian nation.

But now, the impetus behind it — to stem India’s massive gold imports and reduce the trade deficit by melting down the metal already in the country and reselling it — is newly relevant as the rupee slumps and the trade gap hovers near the record high it hit in July.

“If you can recycle the existing gold back home, then reliance on gold imports comes down and it will reduce pressure on the current account deficit,” said Madhavi Arora, lead economist with Emkay Global Financial Services Ltd. “And you can also monetize the gold as an instrument to raise funds.” …

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.2508

OFFSHORE YUAN: 7.2752

SHANGHAI CLOSED DOWN 66.98 PTS OR 2.25%

HANG SENG CLOSED DOWN 564.88 OR 3.66%

2. Nikkei closed DOWN 248.04PTS OR 0.88%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 110.64/Euro FALLS TO 0.99613

3b Japan 10 YR bond yield: FALLS TO. +.239!!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 147,42/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.110%***/Italian 10 Yr bond yield FALLS to 4.188%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.15%…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.45//

3j Gold at $1648.95//silver at: 19.28 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 21/100 roubles/dollar; ROUBLE AT 61.51//

3m oil into the 88 dollar handle for WTI and 96 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 147.42DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9961–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9934well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.000% UP 6 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 4.128% UP 3 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,62…GETTTING DANGEROUS

GREAT BRITAIN/10 YEAR YIELD: 3.4850%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Slide After Tech Wreck Goes 0 For 5

FRIDAY, OCT 28, 2022 – 08:05 AM

With the core of tech earnings season now behind us, FAAMG goes 0 for 5 on earnings as lackluster earnings from the group this week dampened sentiment and underscored the impact of the Fed’s tightening regime. While macro data didn’t help the cause – the GDP report showed the US economy rebounded after two quarterly contractions (all driven by net exports)and briefly assuaged concerns of an imminent recession, consumer spending remains under pressure because of persistent inflation – after the bell, AMZN out with an extremely disappointing miss which sent the stock down as much as 21%, followed by AAPL with a low quality beat driven by As such, Goldman’s Michael Nocerino writes that this morning is going to be harder to compartmentalize these prints (like we have with MSFT, GOOG, META) given AMZN and AAPL make up 10% weighting of the S&P.

And sure enough, the Nasdaq 100 was poised to extend a $675 billion wipeout of the past two days as disappointing earnings prompted a liquidation spree amid the deteriorating profit outlook. Nasdaq 100 futures slumped 1% by 7:30 a.m. in New York, set to trade lower for a third day as reports from Amazon.com and Apple hurt sentiment. Contracts on the S&P 500 were down 0.4%, having dropped as much as 1% earlier. And yet, despite recent weakness, the S&P 500 is set for a second week of gains for the first time since August, amid growing speculation the Fed will be forced to pivot soon. The 10-year benchmark Treasury yield surpassed 4% as a rally in government bonds began to fizzle. Government bonds this week were buoyed by hopes that policymakers are preparing a downshift in aggressive rate hikes amid softer economic data. The dollar collapse, which defined much of this week amid speculation of coordinated intervention, has also started to crack and the dollar index is sharply higher today after the yen tumbled following the BOJ’s announcement to maintain YCC and not change monetary policy for a long time, despite some half-baked rumors to the contrary.

Amazon shares plunged 14% in premarket after the tech giant projected its slowest holiday quarter growth in history.

Meanwhile, Apple edged higher after posting weaker-than-expected iPhone and services sales for its latest quarter, marring an otherwise upbeat report. The combination of weaker earnings and higher interest rates is making technology stocks look increasingly unappealing to investors. The sector could face more pressure ahead as valuations continue to look elevated, Mark Haefele, chief investment officer at UBS Global Wealth Management, said in a note.

“There are now two stock markets — it’s increasingly important to look at the equal-weighted S&P as mega-cap tech (which dominates the normal SPX) enters an extended period of underperformance,” Vital Knowledge analyst Adam Crisafulli wrote in a note. “We continue to think tech is entering a period similar to the ‘99/’00 dotcom boom and bust.”

“These tech results will likely drive broader sentiment down,” said Columbia Threadneedle’s global equity portfolio manager Natasha Ebtehadj on Bloomberg TV. “Apart from tech, other earnings have held up relatively well so hopefully that will provide some support to markets.”

“We are starting to see some companies’ bleeding in terms of forecasts and unfortunately we’re starting to see the big caps in the market disappointing,” Banque Syz CIO Charles-Henry Monchau said in an interview with Bloomberg TV. “Earnings for us is still a headwind.”

Besides the tech rout, bank stocks were also lower in premarket trading Friday, putting them on track to snap a five-day winning streak. In corporate news, Binance, the world’s largest cryptocurrency exchange, confirmed that it’s an equity investor in Elon Musk’s $44 billion acquisition of Twitter. Despite – or perhaps thanks to – Marko Kolanovic’ latest ringing endorsement of all things China, Hong Kong-listed peers plummeting and on course to end a three-day winning streak. Here are some other premarket movers:

Intel rises as much as 5.6% in premarket trading on Friday, after the chipmaker said it was aggressively addressing costs, with a target of $3 billion of reductions in 2023. The chipmaker, and fellow tech companies like Amazon and Meta, are being pressed to wind back spending after years of bulking up.

Pinterest jumped almost 10% in US premarket trading, as the social media company’s results offered analysts respite amid the “wreckage” in the advertising sector demonstrated this week by disappointing earnings from Meta Platforms and Alphabet. Analysts raised their price targets on the stock following Pinterest’s revenue beat and outlook for the fourth-quarter, despite threats from a darkening macroeconomic environment.

US cloud stocks could come under pressure on Friday, after Amazon reported sales for its AWS cloud unit that missed analyst estimates, stoking worries that other providers could also see weakness as enterprise customers pull back on spending.

Core Scientific shares slide 4.9% in US premarket trading, after the bitcoin miner slumped 78% on Thursday in its worst day on record after saying it may seek bankruptcy protection. Barclays downgraded the stock to equal- weight from overweight on solvency worries.

Gilead Sciences shares gain 4.8% in premarket trading after the biopharmaceutical company boosted its guidance for adjusted earnings per share and its 3Q earnings came ahead of analyst estimates. Analysts noted the strong performances from Gilead’s core HIV and oncology businesses, as well as the company’s Covid drug Veklury.

Mullen Automotive drops as much 10% in US premarket trading, with shares in the electric car startup set to ease further after surging more than 40% this week amid heavy mentions on social media and positive sentiment around its I-GO electric vehicle.

In Europe, the Stoxx 50 fell 1.1% with France’s CAC 40 outperforming peers, dropping 0.7%, FTSE MIB lags, dropping 1.4%. Miners, tech and real estate are the worst performing sectors in Europe. Here are some of the biggest European movers today:

OMV shares rise as much as 10%, hitting the highest since July as analysts say 3Q results looks robust operationally.

Kongsberg gains as much as 7.4% after it reported Ebitda for the third quarter that beat the average analyst estimate.

Danske Bank A/S shares rise as much as 5.5%, the most in more than a decade after the lender said it’s close to resolving its money- laundering scandal at an estimated cost of 15.5 billion kroner ($2.1 billion).

Electrolux rises as much as 5.5%, flipping from earlier losses of as much as 5.9%, after the Swedish appliance maker published 3Q results weighed down by poor sales in North America, but offset by a new cost-savings package that includes cutting up to 5,000 staff.

Credit Suisse shares gained as much as 4.7% in Zurich after a record one-day drop on Thursday, when it slumped 19% following the presentation of its new strategic plan including a capital raise and a carve out of its investment banking business.

Natwest fell as much as 9.4% after reporting costs that were higher than expected in the latest hit to the sector as a mortgage crisis looms and a recession looks likely.

Universal Music shares drop as much as 8.5%, the most since June, with analysts saying there were some “weak spots” in the record company’s results and positives around its outlook may already have been priced in.

Valeo shares fall as much as 8% with analysts flagging underperformance for the auto-parts firm.

STMicro shares fall as much as 6.6%, the most since May, after the chipmaker guided fourth-quarter revenue slightly below average analyst estimates.

Earlier in the session, Asian equities were poised for a third weekly drop as Chinese shares slumped, offsetting an earlier reprieve from declines in US Treasury yields and the dollar. The MSCI Asia Pacific Index fell as much as 1.8% on Friday, on track to end the week with losses. Chinese stocks traded in Hong Kong plunged again to 2008 lows, snapping a three-day rally, after the party congress dashed hopes for more market-friendly policies. Read: China Stocks in Worst Ever Post-Congress Rout as Gloom Persists President Xi Jinping’s tighter grip on China has “caused some investors to finally throw in the towel, with the most dramatic impact on the technology stocks,” saidJonathan Pines, head of Asia ex-Japan at Federated Hermes in a note. Meanwhile, Japanese stocks edged lower after the Bank of Japan stood by its ultra-low interest

rates. Singapore bucked the region’s trend to rise more than 1%. Friday marked the busiest day for Asia earnings this results season. Chinese automaker BYD Co., Industrial & Commercial Bank of China Ltd. — the world’s largest bank by assets — and Japanese electronics firm Keyence Corp. are among the 239 MSCI Asia Pacific Index members that reported earnings. Stocks have rebounded this week after a slew of dovish signals from central bankers revived hopes that the pace of policy tightening will slow. Traders will watch for more clues at the Federal Reserve’s meeting next week, where it is expected to deliver a fourth-straight 75 basis point hike.

Japanese equities closed lower after the Bank of Japan maintained its easy monetary policy. Stocks had opened lower amid concern over tech earnings at home and in the US, but were trading little changed around midday before the BOJ’s announcement. The Topix fell 0.3% to close at 1,899.05, while the Nikkei declined 0.9% to 27,105.20. The yen was trading around 146.4 per dollar, swinging between gains and losses. Volume on the Prime market jumped to 5.77 trillion yen, the highest since the market reorganization, as passive funds adjusted holdings on the latest rebalancing of the Topix. Hoya Corp. contributed the most to the Topix decline, decreasing 4.4% after disappointing earnings. Out of 2,166 stocks in the index, 641 rose and 1,448 fell, while 77 were unchanged. The BOJ again maintained its ultra-low rates even as other central banks are tightening. While this divergence had driven the yen’s weakness this year, the currency has rallied almost 4% since last week, from a three-decade low that triggered suspected intervention from Japan. “If the BOJ is lucky, the dollar will weaken from current levels, and the depreciation in the yen will remain at a reasonable level,” Ipek Ozkardeskaya, a senior analyst at Swissquote Group Holdings, wrote in a note. “Otherwise, we could see the dollar-yen spike above the 150 level despite the BOJ’s direct interventions, which do nothing more than burning money.”

Australian stocks also fell: the S&P/ASX 200 index dropped 0.9% to close at 6,785.70, ending a four-day winning streak, dragged by iron ore miners including BHP Group after the steelmaking raw material extended its rout to the lowest in more than two years. Materials, technology and healthcare sectors led the benchmark index’s drop on Friday. Still, the index made a weekly gain of 1.6%. In New Zealand, the S&P/NZX 50 index climbed 0.3% to 11,129.53

Stocks in India advanced for the second consecutive week, moving closer to their record levels seen last year, helped by a rally in financial companies amid robust earnings. The S&P BSE Sensex Index rose 0.3% to 59,959.85 in Mumbai, its highest level since Sept. 14. The NSE Nifty 50 Index advanced by an equal measure. For the week, the indexes have risen more than 1% and are about 3% short of their record levels seen a year ago. Twelve of the 19 sector sub-gauges compiled by BSE Ltd. declined, led by metal companies. For the week, auto firms were among best performers as vehicle sales picked-up during the ongoing festive season. Corporate earnings for September quarter have been supportive of the rally in Indian markets. Out of the 23 Nifty companies, which have so far reported earnings, 16 have either matched or beat the consensus view, while five missed. Top lenders including ICICI Bank and Axis Bank, have reported higher-than-expected profits, helped by rising credit demand.

In FX, the Bloomberg Dollar Spot Index extended yesterday’s bounce from a five-week low as the greenback advanced 0.4$ versus all of its Group-of-10 peers ahead of US inflation data. EUR and DKK are the strongest performers in G-10 FX, JPY and AUD underperform; yen trades at ~147 per dollar.

The yen was the worst G-10 performer, snapping a three-day advance, as the Bank of Japan stood by its ultra-low interest rates amid fresh government support, pushing back against lingering market speculation it will adjust policy as it continues to predict inflation will cool below 2% next year

Australia’s dollar was also among the worst performers as commodity prices slumped. The nation’s sovereign bonds rallied as it caught up with events in Europe and the US on Thursday

The euro fell for a second day on the back of broad-based US dollar strength. European bonds extended a drop after French inflation data for October came in hotter than expected. Front-end bund yields rose by around 10bps, while the long end added around 7bps. BTPs added 10-12 bps across the curve.

In rates, the Treasury curve bear-flattened, pushing yields 2-7bps higher as yields trade near session highs after erasing late-Thursday gains that coincided with Amazon’s after-market plunge. Treasuries track bigger losses in bunds, where German curve aggressively bear-flattens as ECB hike premium is added into front-end. Economic data are focal point of US session, including personal income/spending inflation gauge and University of Michigan sentiment. US yields are cheaper by as much as 10bp in belly of the curve, flattening 5s30s by 7bp to as low as -6.2bp; 10-year yields around 4%, cheaper by 8bp on the day with bunds cheaper by additional 6bp in the sector. German curve bear-flattens as 10-year yields rise 14bps to 2.1%; 2s10s, 5s30s spreads are tighter by 2bp and 3bp on the day as front- end and belly yields are cheaper by 17bp on outright basis. Italian BTP spread widens to Germany; Italy inflation hit an all-time high of 12.8% in October.

In commodities, oil pared its weekly gain as investors shied away from risky assets on a dimming outlook for China and the wider global economy. West Texas Intermediate slid below $88 a barrel. Moving to metals, the complex is once again under USD-induced pressure with precious metals unable to derive any substantial allure from their traditional haven status; base metals hit on sentiment, particularly APAC weakness in China. Spot gold falls roughly $12 to trade near $1,651/oz.

Bitcoin is under modest pressure though resides in narrow ranges and despite the DXY reclaiming 111.00, Bitcoin still holds onto the USD 20k handle.

Looking ahead, today’s data line up in the US will include Q3 employment cost index, which as Nikileaks just informed us…

… will be closely watched by the Fed so a big beat here and futures will tumble even more. We also get, September personal income, personal spending, PCE deflator and pending home sales. In Europe, Germany and France will release Q3 GDP and October CPI figures, with the latter also due for Italy. Other indicators will include consumer spending and PPI for France, PPI and hourly wages for Italy and economic and industrial confidence for the Eurozone. The earnings list will be lighter than in previous days but will feature key commodity companies like Exxon Mobil, Chevron, Equinor and Eni. Other notable reporters will include AbbVie, NextEra Energy, Sanofi, Porsche, Airbus, Volkswagen, Colgate-Palmolive, BBVA and LyondellBasell.

Market Snapshot

S&P 500 futures down 0.8% to 3,790.50

STOXX Europe 600 down 0.6% to 406.72

MXAP down 1.7% to 135.55

MXAPJ down 1.9% to 432.30

Nikkei down 0.9% to 27,105.20

Topix down 0.3% to 1,899.05

Hang Seng Index down 3.7% to 14,863.06

Shanghai Composite down 2.2% to 2,915.93

Sensex little changed at 59,792.78

Australia S&P/ASX 200 down 0.9% to 6,785.72

Kospi down 0.9% to 2,268.40

Brent Futures down 0.7% to $96.30/bbl

Gold spot down 0.7% to $1,651.18

U.S. Dollar Index up 0.31% to 110.93

German 10Y yield up 4% to 2.04%

Euro down 0.2% to $0.9946

Top Overnight News from Bloomberg

As China’s hovers near the weak end of a daily 2% trading band against the dollar, the specter of extreme measures — however unlikely — is growing. Already, there are signs that China is intervening in foreign-exchange markets, like Japan has done. A one-time revaluation and restricting the yuan’s range are other major tools

The ECB’s monetary policy will have to move into restrictive territory to get inflation under control, Governing Council member Peter Kazimir said

The ECB is under no obligation to repeat the 75 basis-point interest-rate increases enacted at the last two meetings, Governing Council member Francois Villeroy de Galhau said

The ECB will continue to lift borrowing costs as it steps up its battle against record euro-area inflation, and remain flexible about the magnitude of individual steps, according to Governing Council member Bostjan Vasle

The ECB needs to deliver a “substantial” increase in interest rates at its final meeting of the year in December, despite a strong likelihood of a technical recession in the euro area, according to Governing Council member Gediminas Simkus

Hopes that the euro zone can stave off a recession got a boost as Germany defied expectations by reporting another quarter of economic growth, though momentum slowed dramatically in France and Spain

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks traded mostly lower but off worst levels following a mixed lead from the US. ASX 200 was pressured by its IT sector following the Meta-induced losses seen on Wall Street. Nikkei 225 drifted off worst levels heading into the BoJ announcement but saw little action on the return from lunch break after the BoJ maintained its policy unchanged whilst upping its inflation forecasts across the board. KOSPI conformed to the broader risk tone, although losses were shallower than peers. Hang Seng and Shanghai Comp opened lower with the tech sector underperforming after the downbeat sectoral lead from the US, whilst NY Times reported that the Biden administration is weighing further controls on Chinese technology. Agricultural Bank of China (1288 HK) Q3 2022 (CNY): Net 68.5bln, NIM 1.96%, NPL ration 1.40%. ICBC (1398 HK) 9M 2022 (CNY): net profit 265.82bln, NPL 1.4% at end-Sept.

Top Asian News

China Names Beijing Mayor Chen Jining As Shanghai Party Boss

BOJ Keeps Ultra-Low Rates as Team Japan Sticks to Policy Path

BOJ Changes Bond Purchase Plan for First Time During a Quarter

Russia Export Windfall Finds Sanctions Haven in Yuan, Quasi-Bank

Iron Ore on Track for Longest Run of Weekly Losses Since 2014

European bourses are pressured across the board, Euro Stoxx 50 -0.9%, deriving direction from downbeat APAC and US after-market trade. Within the region, sectors are predominantly in the red with Tech dented amid US after-market updates while Basic Resources slips after Glencore’s downbeat production report. Stateside, the NQ -1.3% is the clear underperformer amid pressure from the below after-market earnings; ES -0.8%, pressured though magnitudes a touch more contained ahead of key US price data. Amazon.com Inc (AMZN) – Q3 2022 (USD): EPS 0.28 (exp. 0.22), Revenue 127.1bln (exp. 127.45bln); Q4 22 revenue view 140-148bln (exp. 155.150bln). AWS: 20.54bln (exp. 21.191bln). Click here for details. CFO said the Co. is preparing for what could be a slower growth period. Co. is being very careful on its hiring and is seeing weakness in Europe relative to the US. -13% in the pre-market. Apple Inc (AAPL) Q4 2022 (USD): EPS 1.29 (exp. 1.27), Revenue 90.15bln (exp. 88.90bln) Q4 product sales: iPhone: 42.63bln (exp. 43.21bln) iPad: 7.17bln (exp. 7.94bln). Mac: 11.51bln (exp. 9.36bln). Click here for details. CFO says total company revenue will decline in Q4; sees nearly 10ppt negative Y/Y impact from FX. +0.5% in the pre-market. Intel Corp (INTC) – Q3 2022 (USD): Adj. EPS 0.59 (exp. 0.32), Revenue 15.3bln (exp. 15.25bln). Click here for details. +4.5% in the pre-market

Top European News

European Stocks Fall Amid Earnings Flurry as Tech, Miners Drop

UK Lenders Face Biggest Mortgage Test Since Financial Crisis

Appliance Maker Electrolux to Cut Up to 8% of 50,000 Staff

Saab Ramping Up Capacity Ahead of Sweden’s NATO Membership

DXY extends recovery gains to probe 111.000 and this time thanks in large part to the Yen as BoJ sticks to ultra-accommodation, dovish guidance and passive role in terms of intervention; USD/JPY eyes 148.00 from around 146.00 at one stage and near 145.00 yesterday

Aussie and Kiwi rattled by risk aversion and their US rival’s revival, AUD/USD just over 0.6400 and NZD/USD under 0.5800

Euro cushioned by strong inflation data and some hawkish ECB rhetoric, but capped at parity vs the Buck and more hefty option expiries

Yuan undermined by a weak PBoC fix and losses in Chinese tech stocks on reports of further US controls

PBoC set USD/CNY mid-point at 7.1698 vs exp. 7.1638 (prev. 7.1570); weakest Yuan fix since Feb 2008.

China’s CBIRC says those who sell the Yuan now will regret it, via Bloomberg citing a report. China has a resilient economy and its positive long-term trend will continue.

Fixed Income

EGBs are under broad pressure as ECB speakers come out in full hawkish force alongside hotter than expected regional CPI data, ex-Spain.

Specifically, the Bund has been pushed below 139.00 and the accompanying 10yr yield to above 2.10% while BTPs are similarly pressured though the spread vs. Germany has narrowed to around 200bps.

Gilts are bucking the trend somewhat and retain a slight positive bias, with attention turning to next week’s BoE where the magnitude is centered around 75bp vs 100bp+ in recent weeks.

Stateside, USTs are in-fitting with EGBs ahead of their own price metrics via PCE Price Index this afternoon, with yields elevated as such though the curve is a touch flatter.

Commodities

The complex looks set to end the week with another session of relatively limited explicit newsflow and as such participants focus remains on broader macro developments and pricing.

Currently, the crude benchmarks are pressured by around 1% or just shy of USD 1.00/bbl on the session though are still set to end the week with upside of just over USD 2.00/bbl, at the time of writing.

Moving to metals, the complex is once again under USD-induced pressure with precious metals unable to derive any substantial allure from their traditional haven status; base metals hit on sentiment, particularly APAC weakness in China.

Central Banks

BoJ maintained its policy unchanged as expected with rates at -0.10% and QQE with yield curve control maintained to target 10yr JGB yield at around 0%, via a unanimous vote, whilst also maintaining dovish forward guidance, as expected.

BoJ Quarterly Outlook Report saw Core CPI upgraded across the board, but the FY23 and FY24 forecasts were below the BoJ’s 2% target, both at 1.6% (upgraded to 1.4% and 1.3% respectively), whilst warning that the risks to prices are skewed to the upside. Real GDP growth was downgraded for FY22 and FY23 but upgraded for FY24. The BoJ said there is a need to watch FX and its impact on the economy. The central bank also said it will make changes to the way it buys ETFs from Dec 1st, the Bank will take now into account the holding cost of each ETFs and select those with the lowest trust fee ratio in making purchases.

BoJ Governor Kuroda (post-meeting press conference) says must be vigilant to the impact of FX moves; CPI to undershoot 2% from next year; will not hesitate to ease monpol. if needed. Click here for full details.

BoJ Quarterly Schedule of Outright Purchases of Japanese Government Bonds; to increase frequency of purchases in November.

ECB’s Simkus says QT discussion in December should be about start dates and amounts, via Reuters.

ECB’s Villeroy says the ECB will bring inflation back to 2% in 2-3 years; no obligation to raise rates by 75bps at the December meeting.

ECB’s Kazmir says rates will rise in December and in early 2023, crossing neutral like a ‘runaway train’, must get rates into restrictive territory. A risk that Eurozone inflation will remain higher for longer, and remains above target. Risk of a recession in the Eurozone are growing.

ECB’s Muller says they must decide on how to gradually cut bond holdings, via Bloomberg; rates will continue to increase in the near term, they are still now and are not restrictive.

Geopolitcs

US will soon provide additional military assistance to Ukraine, according to the White House spokesperson, US is not seeing any signs of Russia making preparations to use a “dirty bomb”, via CNN.

Biden administration is weighing further controls on Chinese technology, according to NYT.

France and Germany “agreed that recent American state subsidy plans represent market-distorting measures that aim to convince companies to shift their production to the US… and that is a problem they want the EU to address.”, according to Politico sources.

North Korea fired two short-range ballistic missiles that landed outside of Japan’s Exclusive Economic Zone, according to South Korea.

US Event Calendar

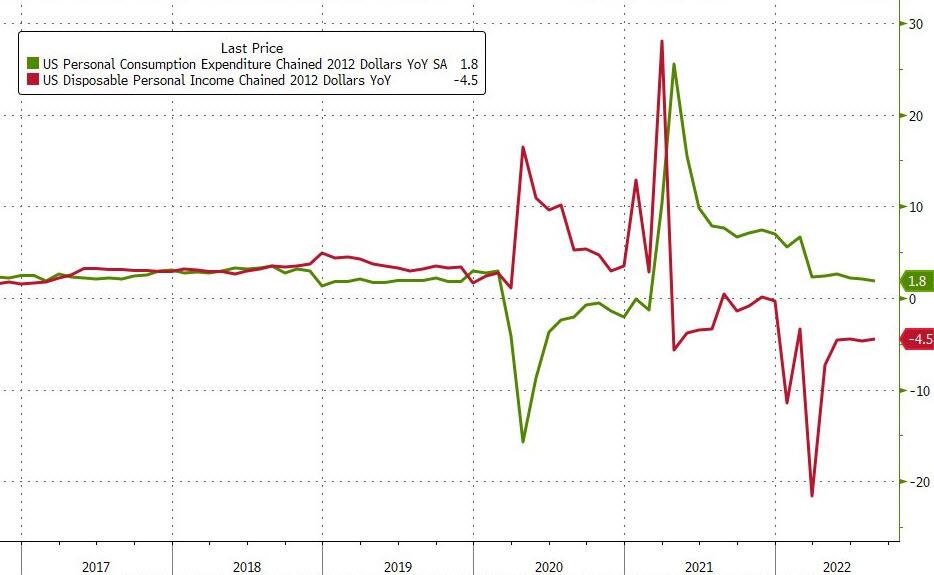

08:30: 3Q Employment Cost Index, est. 1.2%, prior 1.3%

08:30: Sept. Real Personal Spending, est. 0.2%, prior 0.1%

Sept. Personal Income, est. 0.4%, prior 0.3%

Sept. Personal Spending, est. 0.4%, prior 0.4%

Sept. PCE Deflator MoM, est. 0.3%, prior 0.3%

Sept. PCE Deflator YoY, est. 6.3%, prior 6.2%

Sept. PCE Core Deflator YoY, est. 5.2%, prior 4.9%

Sept. PCE Core Deflator MoM, est. 0.5%, prior 0.6%

10:00: Sept. Pending Home Sales (MoM), est. -4.0%, prior -2.0%

Pending Home Sales YoY, prior -22.5%

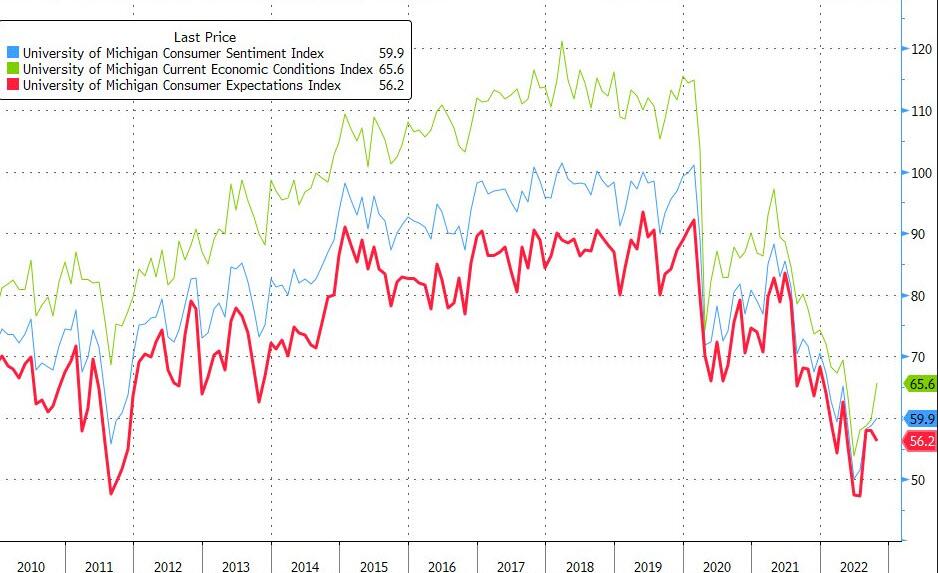

10:00: Oct. U. of Mich. Sentiment, est. 59.6, prior 59.8

Oct. U. of Mich. Current Conditions, est. 65.0, prior 65.3

Oct. U. of Mich. Expectations, est. 56.0, prior 56.2

Oct. U. of Mich. 1 Yr Inflation, est. 5.1%, prior 5.1%

Oct. U. of Mich. 5-10 Yr Inflation, est. 2.9%, prior 2.9%

DB’s Jim Reid concludes the overnight wrap

I think we can now officially call this the 6th pivot anticipation trade over the last 12 months. What started out as a WSJ Timiraos tweet last Friday, got momentum from weaker housing data, moved onto a dovish BoC, and then reached the ECB yesterday. Although they hiked 75bps, they signalled a more dovish tone than expected. So much so that our economists now think they will hike 50bps in December relative to their previous 75bps forecasts. They still think the terminal rate will hit 3% but the profile is much more uncertain now. Their base case is a further 50bps in February and then two successive 25bps hikes to get to 3%. The BoJ maintained the dovish flavour of the last week, as expected, keeping policy rates unchanged and its yield curve control program in place.

Back to the ECB, to quote DB’s Mark Wall from his review piece “the press conference had elements that leaned dovish”. These included the increased probability of recession, the lagged impact of rapid monetary tightening and the absence of reference to “several” more hikes. Other comments pushed back as too dovish an interpretation, such as the emphasis on uncertainty, the more inflationary wording on wages and the fact that even after this hike the Governing Council was no closer to defining the terminal rate.” There’s lots more in the piece including on all the TLTRO news.

All in all, this further amplified the dovish rates trade since Friday. If only I had a fraction of the power to move global markets as WSJ’s Nick Timiraos. In terms of the highlights yesterday, markets took around 25bps of cuts out of terminal ECB rates to now around 2.6%. This put pressure on the euro (-1.16%) which fell below parity again as 2y yields weakened across major European markets, including Germany (-17.0bps), France (-9.8bps) and Italy (-31.0bps). 10y yields fell as well, with periphery bonds (BTPs -32.1bps) outperforming the ones in Western Europe (Bunds -15.1bps and OATs -18.3bps). In their recap of the meeting (link here) our European rates strategists tied the Italian outperformance to the communications that principles around QT would be pursued in December, and that ahead of any implementation, which was more dovish than what was anticipated going into the meeting. They also note that BTPs outperformed from the generally dovish tone that defined the entire meeting.

So this sets us up very nicely for Powell and the Fed next week. What could have been a bog standard incremental 75bps now becomes a “will they or won’t they” endorse the pivot party? I’d imagine the most dovish Powell could be is to say that December’s decision between 75bps and 50bps will be data dependent. I’m not sure he can go further than that with two CPI and NFP reports in the interim.

This dovish global move this week has taken the headline pressure off a poor week for US tech earnings with Meta falling -24.56% yesterday after the prior night’s results. Last night it was the turn of Apple and Amazon. The former slightly disappointed analysts on weaker iPhone and services revenues and, after flitting between gains and losses, actually managed to finish after-hours trading +0.38% higher on offsetting strength in other business lines including Mac sales. Apple is proving a stand out, however, as the latter was a bit of a shocker with company forecasts for the lucrative holiday period much lower than expected. Shares fell a dramatic -12.98% after hours. If sustained today that would drop it to a market cap of below $1tn. In November last year we were as high as $1.9tn, so quite a fall to say the least. This has left S&P and Nasdaq futures down -0.44% and -0.69% overnight.

Another big macro event yesterday was the release of Q3 GDP in the US and the print came in at +2.6%, above the 2.4% consensus estimate and a strong rebound from -0.6% in Q2. However, the lion’s share of gains in growth came from net exports and demand-related components showed muted growth. In other data releases, a downbeat tone came from a miss on durable goods orders (+0.4% vs +0.6% expected) although initial jobless claims came in a touch lower than expected (217k v 220k). This morning, all eyes will be on GDP and inflation data from Germany and France along with Italian CPI data.

For US bonds, stronger-than-expected economic rebound didn’t fully outweigh the passthrough from the dovish ECB, with yields declining by -13.0bps on the 2y and -8.4bps on the 10y. Net net that took out -10.7bps off the peak Fed Funds futures rate priced in for next May and -27.7bps since Timiraos’ tweet when terminal pricing had breached 5%. Nevertheless, the dollar index was still up +0.81% for the day as the Fed is currently being out-pivoted by other global central banks.

Heading into big tech earnings after the close, stocks gyrated between gains and losses, but ultimately slumped into the close with the S&P 500 finishing down by -0.61%. Meta’s outsized impact on tech was seen in Nasdaq’s underperformance (-1.63%) after the stock lost -24.56% during trading hours and the share price closed at its worst level since early 2016. Sector-wise, industrials led the pack (+1.14%) on strong earnings (Caterpillar gained +7.71% and Honeywell climbed +3.27%) with financials close behind (+0.75%) on a steeper curve whilst, on the other hand, IT (-1.52%) and communications (-4.12%) weighed down on the S&P 500. It was thus unsurprising that despite a big loss on the day for the index, 55% of its members actually finished higher by the close since the two sectors together take up nearly a third of the index by weight. Along with Caterpillar and Honeywell, we got an earnings beat from McDonald’s, who’s share price climbed +3.31%.

In Europe, the Stoxx 600 (-0.03%) closed nearly flat ahead of today’s major data releases and despite the tailwinds from falling European yields. Showing growth concerns, cyclical sectors like IT (-1.76%), materials (-0.87%) and industrials (-0.47%) were a major drag on performance together with healthcare (-1.13%) and consumer discretionary stocks (-0.65%). So energy (+3.76%), real estate (+2.56%) and utilities (+1.07%) did most of the heavy lifting to keep the index afloat for the day. In data, we also had a tailwind from an upward surprise in Germany’s consumer confidence, which rose to -41.9 from -42.5 (vs consensus of -42.3). Data from Italy was more mixed, with a miss on consumer confidence (90.1 vs 93.5 expected) but a beat on the manufacturing gauge (100.4 vs 100).

Asian equity markets are mostly trading lower this morning due to weaker earnings posted by Wall Street’s tech giants. As I type, the Hang Seng (-1.91%) is the largest underperformer followed by the CSI (-1.27%), the Shanghai Composite (-0.83%) and the Nikkei (-0.35%). Elsewhere, the KOSPI (-0.09%) is swinging between gains and losses.

As mentioned, the Bank of Japan (BOJ) continued its dovish tone, keeping interest rates unchanged due to weak growth prospects, while keeping YCC in place. In its quarterly review of its projections, the BOJ mentioned that it sees core consumer inflation to hit 2.9% for FY2022 and 1.6% the following year. It projects inflation to hit 1.6% in fiscal 2024.

Ahead of the BOJ’s rate announcement, Japan’s Prime Minister Fumio Kishida unveiled a new economic stimulus package that will include 29.1 trillion yen ($199 billion) in government spending. The overall size of the package will likely reach 71.6 trillion yen, when spending by municipalities and companies is taken into account.

Staying on Japan, Tokyo CPI inflation rose sharply to +3.5% y/y in October (v/s +3.3% expected), picking up from +2.8% increase in September. At the same time, the core inflation hit +3.4%, the highest level since 1989 while sharply accelerating from September’s +2.8% gain, indicating broadening inflationary pressure. Separately, Japan’s jobless rate surprisingly rose to 2.6% in September from previous month’s 2.5% while the Job-to-applicant ratio improved for the ninth consecutive month to a 2-1/2-year high of 1.34 in September from 1.32 in August.

Looking ahead, today’s data line up in the US will include Q3 employment cost index, September personal income, personal spending, PCE deflator and pending home sales. In Europe, Germany and France will release Q3 GDP and October CPI figures, with the latter also due for Italy. Other indicators will include consumer spending and PPI for France, PPI and hourly wages for Italy and economic and industrial confidence for the Eurozone. The earnings list will be lighter than in previous days but will feature key commodity companies like Exxon Mobil, Chevron, Equinor and Eni. Other notable reporters will include AbbVie, NextEra Energy, Sanofi, Porsche, Airbus, Volkswagen, Colgate-Palmolive, BBVA and LyondellBasell.

end

AND NOW NEWSQUAWK (EUROPE/REPORT)

Sentiment slips following a downbeat APAC session with AMZN -13% post-earnings – Newsquawk US Market Open

FRIDAY, OCT 28, 2022 – 06:33 AM

European bourses are pressured across the board, Euro Stoxx 50 -0.9%, deriving direction from downbeat APAC and US after-market trade.

Stateside, the NQ -1.3% is the clear underperformer amid pressure from after-market earnings; AMZN -13%

DXY extends recovery gains to probe 111.000 and this time thanks in large part to the Yen; EUR cushioned by inflation prints

EGBs are under broad pressure as ECB speakers come out in full hawkish force alongside hotter-than-expected regional CPI data

Commodity complex is once again being dictated by broader market action amid relatively light-specific newsflow

Looking ahead, highlights include German CPI Prelim., US PCE. Earnings from Chevron, Exxon, AbbVie, Colgate-Palmolive, LyondellBasell

European bourses are pressured across the board, Euro Stoxx 50 -0.9%, deriving direction from downbeat APAC and US after-market trade.

Within the region, sectors are predominantly in the red with Tech dented amid US after-market updates while Basic Resources slips after Glencore’s downbeat production report.

Stateside, the NQ -1.3% is the clear underperformer amid pressure from the below after-market earnings; ES -0.8%, pressured though magnitudes a touch more contained ahead of key US price data.

Amazon.com Inc (AMZN) – Q3 2022 (USD): EPS 0.28 (exp. 0.22), Revenue 127.1bln (exp. 127.45bln); Q4 22 revenue view 140-148bln (exp. 155.150bln). AWS: 20.54bln (exp. 21.191bln). Click here for details. CFO said the Co. is preparing for what could be a slower growth period. Co. is being very careful on its hiring and is seeing weakness in Europe relative to the US. -13% in the pre-market

Apple Inc (AAPL) Q4 2022 (USD): EPS 1.29 (exp. 1.27), Revenue 90.15bln (exp. 88.90bln) Q4 product sales: iPhone: 42.63bln (exp. 43.21bln) iPad: 7.17bln (exp. 7.94bln). Mac: 11.51bln (exp. 9.36bln). Click here for details. CFO says total company revenue will decline in Q4; sees nearly 10ppt negative Y/Y impact from FX. +0.5% in the pre-market

Intel Corp (INTC) – Q3 2022 (USD): Adj. EPS 0.59 (exp. 0.32), Revenue 15.3bln (exp. 15.25bln). Click here for details. +4.5% in the pre-market

Over 300 US groups have warned that rail strikes could shut down the entire freight rail system and have urged President Biden’s involvement, according to a letter cited by Reuters.

DXY extends recovery gains to probe 111.000 and this time thanks in large part to the Yen as BoJ sticks to ultra-accommodation, dovish guidance and passive role in terms of intervention; USD/JPY eyes 148.00 from around 146.00 at one stage and near 145.00 yesterday

Aussie and Kiwi rattled by risk aversion and their US rival’s revival, AUD/USD just over 0.6400 and NZD/USD under 0.5800

Euro cushioned by strong inflation data and some hawkish ECB rhetoric, but capped at parity vs the Buck and more hefty option expiries

Yuan undermined by a weak PBoC fix and losses in Chinese tech stocks on reports of further US controls

PBoC set USD/CNY mid-point at 7.1698 vs exp. 7.1638 (prev. 7.1570); weakest Yuan fix since Feb 2008.

China’s CBIRC says those who sell the Yuan now will regret it, via Bloomberg citing a report. China has a resilient economy and its positive long-term trend will continue.

EGBs are under broad pressure as ECB speakers come out in full hawkish force alongside hotter than expected regional CPI data, ex-Spain.

Specifically, the Bund has been pushed below 139.00 and the accompanying 10yr yield to above 2.10% while BTPs are similarly pressured though the spread vs. Germany has narrowed to around 200bps.

Gilts are bucking the trend somewhat and retain a slight positive bias, with attention turning to next week’s BoE where the magnitude is centered around 75bp vs 100bp+ in recent weeks.

Stateside, USTs are in-fitting with EGBs ahead of their own price metrics via PCE Price Index this afternoon, with yields elevated as such though the curve is a touch flatter.

The complex looks set to end the week with another session of relatively limited explicit newsflow and as such participants focus remains on broader macro developments and pricing.

Currently, the crude benchmarks are pressured by around 1% or just shy of USD 1.00/bbl on the session though are still set to end the week with upside of just over USD 2.00/bbl, at the time of writing.

Moving to metals, the complex is once again under USD-induced pressure with precious metals unable to derive any substantial allure from their traditional haven status; base metals hit on sentiment, particularly APAC weakness in China.

BoJ maintained its policy unchanged as expected with rates at -0.10% and QQE with yield curve control maintained to target 10yr JGB yield at around 0%, via a unanimous vote, whilst also maintaining dovish forward guidance, as expected.

BoJ Quarterly Outlook Report saw Core CPI upgraded across the board, but the FY23 and FY24 forecasts were below the BoJ’s 2% target, both at 1.6% (upgraded to 1.4% and 1.3% respectively), whilst warning that the risks to prices are skewed to the upside. Real GDP growth was downgraded for FY22 and FY23 but upgraded for FY24. The BoJ said there is a need to watch FX and its impact on the economy. The central bank also said it will make changes to the way it buys ETFs from Dec 1st, the Bank will take now into account the holding cost of each ETFs and select those with the lowest trust fee ratio in making purchases.

BoJ Governor Kuroda (post-meeting press conference) says must be vigilant to the impact of FX moves; CPI to undershoot 2% from next year; will not hesitate to ease monpol. if needed. Click here for full details.

BoJ Quarterly Schedule of Outright Purchases of Japanese Government Bonds; to increase frequency of purchases in November.

ECB’s Simkus says QT discussion in December should be about start dates and amounts, via Reuters.

ECB’s Villeroy says the ECB will bring inflation back to 2% in 2-3 years; no obligation to raise rates by 75bps at the December meeting.

ECB’s Kazmir says rates will rise in December and in early 2023, crossing neutral like a ‘runaway train’, must get rates into restrictive territory. A risk that Eurozone inflation will remain higher for longer, and remains above target. Risk of a recession in the Eurozone are growing.

ECB’s Muller says they must decide on how to gradually cut bond holdings, via Bloomberg; rates will continue to increase in the near term, they are still now and are not restrictive.

UK PM Sunak reportedly explores tax rises and spending cuts of up to GBP 50bln, according to FT. The Telegraph says that the Chancellor Sunak is drawing up plans to expand the windfall tax on energy companies in an attempt to balance the books.

NOTABLE EUROPEAN DATA

German North Rhine-Westphalia State CPI YY (Oct) 11.0% (Prev. 10.1%); MM (Oct) 1.2% (Prev. 1.8%)

Italian CPI (EU Norm) Prelim. YY (Oct) 12.8% vs. Exp. 9.9% (Prev. 9.4%); MM (Oct) 4.0% vs. Exp. 1.4% (Prev. 1.6%)

Bitcoin is under modest pressure though resides in narrow ranges and despite the DXY reclaiming 111.00, Bitcoin still holds onto the USD 20k handle.

GEOPOLITICS

RUSSIA-UKRAINE

US will soon provide additional military assistance to Ukraine, according to the White House spokesperson, US is not seeing any signs of Russia making preparations to use a “dirty bomb”, via CNN.

OTHER

Biden administration is weighing further controls on Chinese technology, according to NYT.

France and Germany “agreed that recent American state subsidy plans represent market-distorting measures that aim to convince companies to shift their production to the US… and that is a problem they want the EU to address.”, according to Politico sources.

North Korea fired two short-range ballistic missiles that landed outside of Japan’s Exclusive Economic Zone, according to South Korea.

APAC TRADE

EQUITIES

APAC stocks traded mostly lower but off worst levels following a mixed lead from the US.

ASX 200 was pressured by its IT sector following the Meta-induced losses seen on Wall Street.

Nikkei 225 drifted off worst levels heading into the BoJ announcement but saw little action on the return from lunch break after the BoJ maintained its policy unchanged whilst upping its inflation forecasts across the board.

KOSPI conformed to the broader risk tone, although losses were shallower than peers

Hang Seng and Shanghai Comp opened lower with the tech sector underperforming after the downbeat sectoral lead from the US, whilst NY Times reported that the Biden administration is weighing further controls on Chinese technology.

Agricultural Bank of China (1288 HK) Q3 2022 (CNY): Net 68.5bln, NIM 1.96%, NPL ration 1.40%.

ICBC (1398 HK) 9M 2022 (CNY): net profit 265.82bln, NPL 1.4% at end-Sept.

NOTABLE APAC HEADLINES

IMF cuts China’s 2022 growth outlook to 3.2% (prev. 4.4%), sees 4.4% growth in 2023 and 4.5% in 2024.

PBoC injects CNY 98bln via 7-day reverse repos at a maintained rate 2.00% for a daily injection of CNY 88bln

Japanese PM Kishida announces JPY 29.1tln extra budget for stimulus, via Bloomberg.

DATA RECAP

Japanese CPI, Overall Tokyo (Oct) 3.5% (Prev. 2.8%); Ex fresh food YY (Oct) 3.4% vs. Exp. 3.1% (Prev. 2.8%)

Japanese Unemployment Rate (Sep) 2.6% vs. Exp. 2.5% (Prev. 2.5%); Jobs/Applicants Ratio* (Sep) 1.34 vs. Exp. 1.33 (Prev. 1.32)

Australian PPI QQ (Q3) 1.9% (Prev. 1.4%); YY (Q3) 6.4% (Prev. 5.6%)

i)FRIDAY MORNING// THURSDAY NIGHT