in Uncategorized · Leave a comment·Edit

in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSE: DOWN $4.00 to $1637.40

SILVER PRICE CLOSE: DOWN $0.00 to $19.18

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1632.60

Silver ACCESS CLOSE: 19.21

New: early yesterday morning//

Bitcoin morning price: $20,703 UP 127

Bitcoin: afternoon price: $20,369 DOWN 207

Platinum price closing DOWN $15.50 AT $931.00

Palladium price; closing DOWN $49.80 at $1905.05

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: 2225.28 DOLLARS DOWN 7.80 CDN DOLLARS PER OZ

BRITISH GOLD: 1423.53 POUNDS PER OZ UP 10.21 POUNDS PER OZ

EURO GOLD: 1653.17 EUROS PER OZ UP 3.20 EUROS PER OZ.

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX//NOVEMBER

CONTRACT: NOVEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,639.600000000 USD

INTENT DATE: 10/28/2022 DELIVERY DATE: 11/01/2022

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DB AG 379

118 C MACQUARIE FUT 700

190 H BMO CAPITAL 178

323 C HSBC 239

435 H SCOTIA CAPITAL 370

624 H BOFA SECURITIES 245

657 C MORGAN STANLEY 12

661 C JP MORGAN 231 781

690 C ABN AMRO 65

732 C RBC CAP MARKETS 25

737 C ADVANTAGE 40

800 C MAREX SPEC 16

880 H CITIGROUP 7

905 C ADM 72

TOTAL: 1,680 1,680

MONTH TO DATE: 1,680

JPMORGAN STOPPED 781/1600

GOLD: NUMBER OF NOTICES FILED FOR NOV. CONTRACT: 1600 NOTICES FOR 160,000 OZ or 4.9767 TONNES

total notices so far: 1600 contracts for 160000 oz (4.9767 tonnes)

SILVER NOTICES: 11 NOTICE(S) FILED FOR 135000 OZ/

total number of notices filed so far this month 11 : for 550,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $4.00

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////A BIG CHANGE IN GLD INVENTORY: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD// /INVENTORY LOWERS TO 925.20 TONNES

INVENTORY RESTS AT 922.59 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 0 CENTS

AT THE SLV// :/SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF OF .644 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 483.723 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1724 CONTRACTS TO 138,127 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE TINY GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG $0.35 LOSS IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS/HFT WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.35)., AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS, AS WE HAD A VERY STRONG LOSS IN OUR TWO EXCHANGE OF 1634 CONTRACTS. HUGE SPECS CONTINUE TO ADD TO THEIR SHORTFALLS FROM WHICH OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. SOME SPEC LONGS COVERED THEIR SHORT POSITIONS //(CONTINUED SPREADER LIQUIDATIONS)

WE MUST HAVE HAD:

I) CONSIDERABLE SPECULATOR SHORT COVERINGS BUT STRONG SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /// SOME NEWBIE SPEC LONG ADDITIONS ON THE LOWER PRICE. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.045 MILLION OZ / // V) HUGE SIZED COMEX OI LOSS/ (CONTINUED SPREADER LIQUIDATIONS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: — 34

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 23 days, total 58,035 contracts: 29.017 million oz OR 1.2616MILLION OZ PER DAY. (253 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 29.017 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ INITIAL

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1758 WITH OUR $0.35 LOSS IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A VERY SMALL SIZED EFP ISSUANCE CONTRACTS: 140 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR NOV. OF 1.045 MILLION OZ .. WE HAVE A VERY STRONG SIZED LOSS OF 1618 OI CONTRACTS ON THE TWO EXCHANGES FOR 8.090 MILLION OZ..MOST OF THE LOSS WAS DUE TO SPREADER LIQUIDATION.

WE HAD 11 NOTICE(S) FILED TODAY FOR 550,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 7424 CONTRACTS TO 467.769 AND CLOSER TO FROM TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -376 CONTRACTS.

.

THE STRONG SIZED INCREASE IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $19.70//COMEX GOLD TRADING/FRIDAY // ZERO SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION AND CONSIDERABLE SPEC SHORT ADDITIONS BUT MINOR SPEC SHORT COVERINGS. // CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR NOV. AT 12.386 TONNES ON FIRST DAY NOTICE //EXPECT HUGE QUEUE JUMPING BEGINNING ON 2ND DAY NOTICE: (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR FALL IN PRICE OF $19.70 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A VERY STRONG SIZED GAIN OF 8860 OI CONTRACTS 27.558 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1692 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 468,146

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8740 CONTRACTS WITH 7048 CONTRACTS INCREASED AT THE COMEX AND 1692 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 9116 CONTRACTS OR 28.364 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1692) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (7048): TOTAL GAIN IN THE TWO EXCHANGES 9116 CONTRACTS. WE NO DOUBT HAD 1) STRONG SPECULATOR SHORT ADDITIONS// CONTINUED GOOD BANKER ADDITIONS/// ZERO SPEC SHORT COVERINGS// CONSIDERABLE NEWBIE SPEC ADDITIONS WITH THE LOWER PRICE ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR NOV. AT 12.386 TONNES ///NEW STANDING FOR NOV 12.386 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) STRONG SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

NOV

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV. :

57,090 CONTRACTS OR 5,709,000 OZ OR 177.57 TONNES 23 TRADING DAY(S) AND THUS AVERAGING: 2482 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 23 TRADING DAY(S) IN TONNES: 177.57 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 177.57/3550 x 100% TONNES 5.01% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A HUGE SIZED 17758 CONTRACT OI TO 138,127 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 140 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 140 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 140 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1758 CONTRACTS AND ADD TO THE 140 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A VERY STRONG SIZED LOSS OF 1618 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 8.090MILLION OZ//

OCCURRED DESPITE OUR HUGE LOSS IN PRICE OF $0.35

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED DOWN 22.44 PTS OR 0.77% //Hang Seng CLOSED DOWN 176.04 OR 1.18% /The Nikkei closed UP 482.26 PTS OR 1.78% //Australia’s all ordinaires CLOSED UP 1.17% /Chinese yuan (ONSHORE) closed DOWN TO 7.3001 //OFFSHORE CHINESE YUAN DOWN 7.3218// /Oil DOWN TO 856,61 dollars per barrel for WTI and BRENT AT 92.51 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 7048 CONTRACTS TO 467.769 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX INCREASE OCCURRED DESPITE OUR FALL IN PRICE OF $19.70 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (1692 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1692 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 1692 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1692 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 9116 CONTRACTS IN THAT 1692 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI GAIN OF 7424 CONTRACTS..AND THIS STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $19.70//WE HAD CONSIDERABLE SPEC SHORTS ADDITIONS, WITH BANKERS AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD STRONG ADDITIONAL NEWBIE SPECS GOING LONG WITH THE LOWER PRICE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING NOV (12.386),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV.12.386 TONNES/INITIAL

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $19.70) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS// SPEC SHORTS ADDED TO THEIR POSITIONS AS WE HAD A VERY STRONG SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 9116 CONTRACTS // WE HAVE REGISTERED A VERY STRONG GAIN OF 30.202 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR NOV. (12.386 TONNES)…THIS WAS ACCOMPLISHED WITH OUR FALL IN PRICE OF $3.80

WE HAD -376 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 8740 CONTRACTS OR 874000 OZ OR 27.105 TONNES

Estimated gold volume 199,696// poor//

final gold volumes/yesterday 204,080/ poor

INITIAL STANDINGS FOR NOVEMBER 2022 COMEX GOLD //OCT 31

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 14,912.718oz Brinks Malca includes 1 kilobar and 2019 kilobars |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 1600 notice(s) 160,000 OZ 4.9767 TONNES |

| No of oz to be served (notices) | 2382 contracts 238.200 oz 7.409 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1600 notices 160,000 4.9767 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals:2

ii) Out of Brinks 32.151 (1 kilobars)

iii) Out of Malca: 14,880.718 oz ( 2019 kilobars

total: 14,912.869 oz

total in tonnes: 0.4638 tonnes

Adjustments: 2// customer to dealer

i)Out of Loomis 18,615.429 oz

ii)Out of Brinks 110,671.591 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR NOVEMBER.

For the front month of NOV. we have an oi of 3982 contracts having LOST ONLY 8 contracts. Thus by definition, the initial amount of gold standing for delivery in this

very inactive month of November is as follows:

3982 notices x 100 oz per notice = 398200 oz

or 12.382 tonnes of gold

This is pretty close to my prediction and it is a whopper which is generally the worst delivery month of the year.

December GAINED 1808 contracts UP to 362,511

February gained 6572 contacts up to 69,645.

We had 1600 notice(s) filed today for 160,000 oz on the first day notice FOR THE NOV. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 231 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1600 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 781 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the NOV. /2022. contract month,

we take the total number of notices filed so far for the month (1600) x 100 oz , to which we add the difference between the open interest for the front month of (NOV 3982 CONTRACTS) minus the number of notices served upon today 1600 x 100 oz per contract equals 398,200 OZ OR 12.3855 TONNES the number of TONNES standing in this non active month of NOV.

thus the INITIAL standings for gold for the NOV. contract month:

No of notices filed so far (1600) x 100 oz+ (3982) OI for the front month minus the number of notices served upon today (1600} x 100 oz} which equals 398,200 oz standing OR 2.3855 TONNES in this NON active delivery month of NOV..

TOTAL COMEX GOLD STANDING: 12.386 TONNES (A HUMONGOUS STANDING FOR NOV (GENERALLY THE POOREST DELIVERY MONTHS FOR A NON ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM TOMORROW ONWARD UNTIL THE END OF THE MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,996,891.215 OZ 62.11 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 24,959,663.661 OZ

TOTAL REGISTERED GOLD: 11,331,325.357 OZ (352.45 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 13,628,338.304 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,334,444 OZ (REG GOLD- PLEDGED GOLD) 290.034 tonnes//rapidly declining

END

SILVER/COMEX

OCT 31//INITIAL NOV. SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 897,179.592 oz Brinks Loomis CNT |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 862,681,985 oz CNT Delaware |

| No of oz served today (contracts) | 11 CONTRACT(S) (55,000 OZ) |

| No of oz to be served (notices) | 198 contracts (990,000 oz) |

| Total monthly oz silver served (contracts) | 11 contracts 55,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 3 withdrawals out of the customer account

i) Out of Brinks 2072,910 oz

ii) out of Loomis: 795,552,070 oz

iii) Out of CNT: 99,554.612 oz

Total withdrawals: 897,179.592 oz

JPMorgan has a total silver weight: 155.891million oz/301.160 million =51.65% of comex .//dropping fast

Comex deposits: 2

i) Into CNT 658,408.230oz

ii) Into Delaware: 254,274.758 oz

total: 862,681.983 oz

adjustments: 4

customer to dealer

i.Brinks 95,048.65 oz

ii) CNT 81,995.699oz

iii) Out of JPM; 560,739.850 oz

iv) Out of Manfra 34,337.569 oz

v) Out of Delaware 14,094.731 iz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 34.741 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 301.160 MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF NOV OI: 209 CONTRACTS HAVING LOST 14 CONTRACT(S.)

THIS IS ALSO AN EXCELLENT SHOWING FOR A NOVEMBER DELIVERY MONTH.

THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER STANDING FOR THIS NON ACTIVE DELIVERY MONTH OF NOVEMBER IS AS FOLLOWS:

209 NOTICES X 5000 OZ PER NOTICE = 1,045,000 OZ

DECEMBER SAW A LOSS OF 1987 CONTRACTS DOWN TO 105.749

JANUARY SAW A GAIN OF 10 CONTRACTS UP TO 1128 CONTACTS.

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 11 for 55,000 oz

Comex volumes:53,927// est. volume today// fair

Comex volume: confirmed yesterday: 59,548 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 11 x 5,000 oz = 55,000 oz

to which we add the difference between the open interest for the front month of NOV(209) and the number of notices served upon today 11 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the NOV../2022 contract month: 11 (notices served so far) x 5000 oz + OI for front month of NOV (209) – number of notices served upon today (11) x 5000 oz of silver standing for the NOV. contract month equates 1,045,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:51,533// est. volume today// poor

Comex volume: confirmed yesterday: 60.788 contracts ( fair)

END

GLD AND SLV INVENTORY LEVELS

OCT 31/WITH GOLD DOWN $4.00; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD//INVENTORY RESTS AT 922.59. TONNES//

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

TONNES

GLD INVENTORY: 922.59 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 31: WITH SILVER FLAT: SMAL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .644 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 483.723 MILLION OZ//

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: AWITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

CLOSING INVENTORY 483.723 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: The Fed Got Everybody Drunk On Cheap Money But The Party Is Over

MONDAY, OCT 31, 2022 – 08:21 AM

A lot of people seem to think that if the Fed had just started fighting inflation a little earlier, we wouldn’t have seen the rapidly rising prices that continue today. The mistake, they say, was thinking inflation was transitory. But as Peter Schiff has pointed out, this problem didn’t start last year, or even with the pandemic. This problem was decades in the making.

And at the root of the problem was year after year of easy money. Wall Street was drunk on cheap money for a decade and it is ultimately going to end in another financial crisis.

The severity of malinvestments, of the misallocations of resources, of the monumental mistakes that have been made throughout this economy by the government, the private sector, corporations, individuals — everybody has made mistakes because of this cheap money.”

Just look at the federal government. It has added trillions of dollars to the national debt over the last decade. It recently eclipsed $31 trillion. A year ago, Janet Yellen was saying the big debt wasn’t a problem because interest rates were low. Well, they’re not low anymore. This is a perfect example of how cheap money incentivized bad decision-making.

After the 2008 financial crisis, George Bush pointed out that Wall Street got drunk. Peter said Bush was correct.

Why was everybody on Wall Street drunk? Where did they get the alcohol? Who liquored them up? That was the Federal Reserve. That was Alan Greenspan. He was the bartender. He kept serving the drinks. That’s why Wall Street was drunk.”

But Wall Street wasn’t drinking alone. Main Street was also three sheets to the wind.

The whole nation was drunk on cheap money, and while they were drunk, they did a lot of stupid things, just like a lot of people do when they’re drunk.”

Peter compared it to a favorite Warren Buffet quote: when the tide goes out, we see who’s swimming naked. Peter said, “Basically, everybody has been naked.”

And everybody is going to be exposed when the tide goes out, which is what’s happening right now.”

As Peter said in a prior podcast, it goes back even further than the last decade. You can trace the Fed’s inflationary monetary policy all the way back to 1998 and the Long-Term Capital Management bailout.

That’s when the Fed really started printing money. And then it printed even more money in advance of Y2K. And then even more money after the NASDAQ bubble popped in 2000. And even more money after the real estate bubble popped in 2008. So, it’s not just one year of excess money printing. The Fed has been too loose for almost 25 years, flooding the economy with cheap money.”

Peter said he knew 2008 wasn’t the real crash. The reckless monetary policy in the response to the Great Recession simply papered things over and kicked the looming crisis down the road.

Well, the real crash is the one we’re headed for right now. And we were going to have that crash regardless of the mistakes the Fed made in 2021. We were going to have it because of all the mistakes it made — not just going back to 2008 — but going all the way back to 1998.”

https://www.zerohedge.com/markets/peter-schiff-fed-got-everybody-drunk-cheap-money-party-over

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

EGON VON GREYERZ

$2 Quadrillion Debt Precariously Resting On $2 Trillion Gold

SUNDAY, OCT 30, 2022 – 08:35 AM

Authored by Egon von Greyerz via GoldSwitzerland.com,

A Lehman squared moment is approaching with Swiss banks and UK pension funds under severe pressure.

But let’s first look at another circus –

The global travelling circus is now reaching ever more nations just as expected. This is right on cue at the end of the most extraordinary financial bubble era in history.

It is obviously debt creation, money printing and the resulting currency debasement which creates the inevitable fall of yet another monetary system. This has been the norm throughout history so “the more it changes, the more it stays the same”.

It started this time with the closing of the gold window in August 1971. That was the beginning of a financial and political circus which continuously added more risk and more lethal acts to keep the circus going.

An economic upheaval always causes political chaos with a revolving door of leaders and political parties going and coming. Remember, a government is never voted in but invariably voted out.

What was always clear to a few of us was that the circus would end with all of the acts crashing virtually simultaneously.

And this is what is starting to happen now.

We have just seen a political farce in the UK. Even the most talented playwright could not have created such a wonderful merry-go-round of characters who we have seen coming in and out of Downing Street.

Just look at the UK Prime Ministers. First there was David Cameron who had to resign in 2016 due to mishandling Brexit. Then the next PM Theresa May had to go in 2019 since she couldn’t get anything done, including Brexit. Then Boris Johnson won the biggest Conservative majority ever but was forced out in 2022 due to Partygate during Covid.

In came Liz Truss as PM in September this year but she only lasted 44 days due to her and her Chancellor’s (Finance Minister) mishandling of the mini budget. They managed to crash the pound and UK gilts (bonds) on the international markets leading to the Bank of England having to step in. Both gilts, derivatives and UK pension funds were at the point of implosion.

And now the carousel has gone full circle with Rishi Sunak the ex-Chancellor taking the helm as Boris bailed out. Boris clearly decided that speeches and other private engagements would be more fruitful than being part of the circus. But he will most certainly attempt to come back.

What a circus!

It just shows that at the end of an economic era, we get the worst leaders who always promise but never deliver.

In a bankrupt global system, you reach a point when the value of printed money dies and whatever a leader promises can no longer be bought with fake money which will always have ZERO intrinsic value.

No one must believe that this is only happening in the UK. The US has a leader who sadly is too old and not in command. He has a deputy who is not respected by anyone. So if Biden, as many believe, doesn’t make it to the end of his period, the US is likely to have a real leadership circus. Also, the US economy is chronically ill having run deficits for 90 years. What keeps the US alive temporarily is the dollar which is strong because it is the least ugly horse in the currency stable.

Scholz in Germany was given a very bad hand by Merkel but has certainly not improved it since he took charge and Germany is on the verge of collapse.

Most countries are the same. Macron doesn’t have a majority in France and strikes are paralysing his country on a daily basis. And his new Italian counterpart, PM Georgina Meloni certainly doesn’t shred her words. Just watch her having a very aggressive go at Macron (poor video quality).

But for people (like myself) who have difficulty accepting the current wave of Wokeism in the world, Meloni’s attack on this fad and her strong defence of family values is a “must watch” (video link). So there is still hope when leaders dare to express views that most media including social media censor today.

DEBT BONDAGE

History has dealt with punishment of non payment of debt in a variety of ways.

In the early Roman Republic around 2,500 years ago, there was a debt bondage called Nexum. In simple terms, a borrower pledged his person as collateral. If he didn’t pay his debt he was enslaved often for an undetermined period.

Jumping quickly to modern times, it would mean that the majority of people, especially in the West would all be debt slaves today. The big difference today is that most people are debt slaves but they have physical freedom. Since virtually nobody, individuals, companies or sovereign states, neither has the intention nor the ability to repay debt, the world now has a chronic debt slavery.

It is even worse than that. The playing field is totally skewed in favour of the banks, big business and the wealthy. The more money you can play with, the more money you can make risk free.

UNLIMITED PERSONAL LIABILITY

No banker, no company management or business owner ever has to take the loss personally if he makes a mistake. Losses are socialised and profits are capitalised. Heads I win, Tails I don’t lose!

But there are honourable exceptions. A smaller number of Swiss banks still work with the principle of unlimited personal liability for the partners/owners. If the global financial system and governments applied that principle, imagine how different the world would look not just financially but also ethically.

With such a system, we wouldn’t just adore the golden calf but put human values first. And whenever we evaluate an investment proposal or granting someone a loan, we wouldn’t just look at how much we could gain personally but if the transaction was sound both economically and ethically and if the risk of loss was minimal.

But I can hear many people protesting and arguing that the world could never have grown as fast without this massive amount of debt. That is of course correct in the short term. But rather than fast growth and then a total implosion of assets and debt, we would then have a much more stable system.

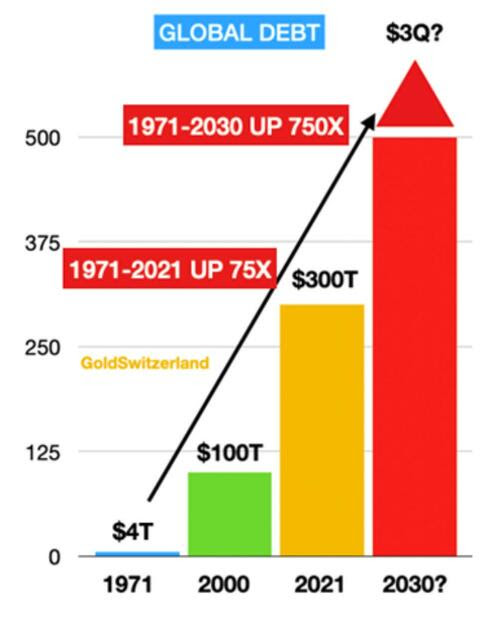

GLOBAL DEBT $300 TRILLION PLUS $2.2 TRILLION OF DERIVATIVES & LIAB.

Just look at the last 50 years since 1971. Globally governments and central banks have contributed to the creation of almost $300 trillion of new money plus quasi money in the form of unfunded liabilities and derivatives of $2.2 quadrillion making £2.5 trillion in total.

As debt explodes, the world could easily face a debt burden of $3 quadrillion by 2025-2030 as the derivatives and unfunded liabilities become debt.

DERIVATIVES – THE MOST DANGEROUS FINANCIAL WEAPON CREATED

Derivatives is not a new instrument. For example during the Tulipomania bubble in Holland in the 17th century, it was possible to trade options on tulip bulbs.

Today the financial system has developed derivatives to become such a sophisticated instrument that virtually no financial transaction can take place without involving some form of derivatives.

But the biggest problem with derivatives is that the quants that create them don’t understand the consequences of their actions. And senior management, including boards of directors, haven’t got a clue of the massive risk derivatives represent.

The collapse in 1998 of LTCM (Long Term Capital Management), set up by Nobel Prize winners and the 2007-9 Sub-Prime crisis is a clear proof of the ignorance of the risk of derivatives.

As an aside, it seems that anyone can receive a Nobel Prize today. Just take Bernanke, he has been awarded the Nobel Prize in economics. Remember that Bernanke, when he was Head of the Fed, printed more money than anyone in history!

What we have to understand is that the committee which chooses the winner of the Nobel economy prize is the Swedish Riksbank (central bank), filled with Keynesian money printers!

Need I say more?

Derivatives have been a massive profit earner for all banks involved. They were initially created as defensive hedge instruments but today they are the most dangerous and aggressive financial instrument of destruction.

Just over 10 years ago, global derivatives were $1.2 quadrillion. Then the Bank of International Settlements (BIS) in Basel decided to halve the values to $600 trillion overnight by changing the basis of calculation. But the $1.2Q risk was still remained at the time.

Since then Over The Counter (OTC) derivatives have seen an explosive growth just like all financial assets. The beauty of OTC derivatives, from the issuers point of view, is that they don’t need to be declared like derivatives traded on exchanges.

And today there are not just interest rate and forex derivatives. No, these instruments are involved in virtually every single financial transaction. Every stock and bond fund involves derivatives. And today most of these funds consist of only synthetic instruments and contain none of the virtual stocks or bonds they represent.

CENTRAL BANKS RESCUING UK AND SWISS BANKS

Just a couple of weeks ago, the UK and thus the global financial system was under severe pressure due to pension funds’ interest derivatives collapsing in value after the UK Budget. Pension funds are globally on the verge of collapse due to rising interest rates and insolvency risk. In order to create cash flow, the pension funds have acquired interest rate swaps. But as bond rates surged these swaps collapsed in value, requiring either liquidation or margin injection.

And thus the Bank of England had to support the UK pension funds and financial system to the extent of £65 billion to avoid default.

In the last couple of weeks we have seen a dismal situation in Switzerland. Swiss banks, through the Swiss National Bank (SNB) have received $11 billion ongoing support through currency swaps (a form of dollar loans) from the Fed.

No details have been revealed of the Swiss situation except that 17 banks are involved. It could also be international banks. But most certainly the ailing Credit Suisse is involved. Credit Suisse just announced a 4 billion Swiss francs loss.

What is clear is that these UK and Swiss situations are just the tip of the iceberg.

The world is now on the verge of another Lehman moment which could erupt at any time.

CENTRAL BANKS NEED TO VACUUM $2 QUADRILLION DERIVATIVES

These derivatives which some of us now estimate to be over $2 quadrillion (not $600b reported by BIS) are what will bring the financial system down.

Every derivative includes an interest element. And the construction of all derivatives did not foresee the major and rapid rise in interest rates that the world has seen. Remember Powell and Lagarde calling inflation transitory just a year ago!

WITH OVER $ 2 QUADRILLION DEBT, PROTECTION IS CRITICAL

This article is not directly about gold. No, it is about the disastrous consequences of governments’ deceitful mismanagement of the economy and of your money. But based on history, gold has been the best protection or insurance against such mismanagement.

Why do 99.5 % of all investors in financial assets avoid the investment that is continuously backed and supported by every government and every central bank globally.

Investors own $600 trillion in stocks, bonds and property which have all enjoyed a 50 year (40 years for bonds) explosion in value.

But why do they only hold $2.3 trillion of an asset that without fail and for 5,000 years has always appreciated and never gone to zero or even gone down substantially over time?

It is the simplest asset to understand and appreciate. It looks good, even shiny and you don’t have to understand the technology behind it nor the balance sheet.

All you need to understand is that every day and every year your government does whatever it can to increase the value of this asset.

So this asset that only gets 0.5% of world financial investments and is continuously supported by governments through their constant creation of money is obviously gold.

What very few investors know, partly because governments are suppressing it, is that gold is the only money that has survived throughout history. Every other currency has without fail gone to ZERO and become extinct.

With this perfect 100% record for gold, it certainly is surprising that virtually nobody owns it!

Investors don’t understand gold or its relevance. There are many reasons for this.

Governments hate gold in spite of the fact that all their actions make gold appreciate considerably over time.

They are of course totally aware of the fact that their totally inept management of the economy and of the monetary system, destroys the value of fiat money.

This is why it is in their interest to conceal their mismanagement of the economy by suppressing the value of gold in the paper market.

But investors ignorance of gold and reluctance to buy it will very soon go through a tectonic change.

OVER $2 QUADRILLION OF LIABILITIES RESTING ON $2 TRILLION OF GOLD

Total gold ever produced in the world is $10.5 trillion. Most of this gold is in jewellery. Central banks around the world hold $2 trillion. That includes $425 billion that US allegedly hold. Many people doubt this figure.

So with over $2 quadrillion (2 and15 ZEROS) of debt and liabilities resting on a foundation of $2 trillion of government owned gold that makes a gold coverage of 0.1% or a leverage of 1000X!

So that is clearly an inverse pyramid with a very weak foundation. A sound financial system needs a very solid foundation of real money. Quadrillions of debt and liabilities can not survive resting on this feeble amount of gold. If gold went up 100X to say $160,000, the coverage would be 10% which is still hardly acceptable.

So the $2 quadrillion financial weapon of mass destruction is now on the way to totally destroy the system. This is a global house of cards that will collapse at some point in the not too distant future.

Obviously Central Banks will first print unlimited amounts of money, buying up to $2 quadrillion of outstanding derivatives, turning them to on balance sheet debt. This will create a vicious circle of more debt, higher interest rates and higher inflation, with probable hyperinflation as debt markets default.

No government and no central bank can solve the problem that they have created. More of the same just won’t work.

So these are the gigantic risks that the world is now facing.

Obviously there is no certainty in these kind of forecasts. But what is certain is that risk of this magnitude must be protected.

There is no reason to believe that gold this time will play a different role to what is has done throughout history.

Gold stands as the sole protector of a sound currency system and the only money which has survived throughout the ages.

3.Chris Powell of GATA provides to us very important physical commentaries

Andy Schectman is perfectly correct; he explains why the physical price of gold and silver is moving away from the paper price

(Andy Schectman/Andrew Maguire)

Miles Franklin’s Andy Schectman explains ‘price as misdirection’ in gold and silver

Submitted by admin on Fri, 2022-10-28 23:26Section: Daily Dispatches

11:27p ET Friday, October 28, 2022

Dear Friend of GATA and Gold:

This week’s “Live from the Vault” from program Kinesis Money, a conversation between London metals trader Andrew Maguire and coin and bullion dealer Andrew Schectman of the Miles Franklin distributorship, examines the incongruity of falling gold and silver futures prices amid overwhelming demand for real metal.

Schectman says he has never seen such a divergence between the prices between “paper” and real metal. This divergence, Schectman says, reflects a “price as misdirection” scheme by large players in the metals markets by which they can obtain the last remaining supplies before a big change in the financial world.

That change, Schectman says, is a revolt against Western hegemony, which is already underway.

The interview is 48 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Ted Butler

a must read..

Ted Butler: Silver’s coming move to $50, and beyond

Submitted by admin on Fri, 2022-10-28 10:27Section: Daily Dispatches

By Ted Butler

SilverSeek.com

Thursday, October 27, 2022

Twice over the past 42 years, the price of silver has risen to $50; once back in 1980 and again 11 years ago, in 2011. Obviously, no one would argue that something that occurred twice already is not capable of happening again. On both prior silver price peaks, prices then fell sharply and quickly. But the next coming move to $50 in silver is much more likely to not only exceed the past two highs, but also remain far higher for far longer than previously.

In 1980 the price of silver rose from $7 to $50 in little more than a year, driven, essentially, by the concerted buying, both in futures and physical metal by interests associated with the Hunt Brothers from Texas and then fell even more sharply as a result of exchange and regulatory actions to unwind the Hunts’ buying. But the epic price run up did show, conclusively, that speculative investment buying could drive silver prices sharply higher. …

… For the remainder of the analysis:

https://silverseek.com/article/coming-move-50-silver-and-beyond

The Coming Move to $50 Silver (and beyond)

October 27, 2022

Ted Butler

Butler Research

750Shares

Twice over the past 42 years, the price of silver has risen to $50; once back in 1980 and again 11 years ago, in 2011. Obviously, no one would argue that something that occurred twice already is not capable of happening again. On both prior silver price peaks, prices then fell sharply and quickly. But the next coming move to $50 in silver is much more likely to not only exceed the past two highs, but also remain far higher for far longer than previously.

In 1980, the price of silver rose from $7 to $50 in little more than a year, driven, essentially, by the concerted buying, both in futures and physical metal by interests associated with the Hunt Brothers from Texas and then fell even more sharply as a result of exchange and regulatory actions to unwind the Hunt’s buying. But the epic price run up did show, conclusively, that speculative investment buying could drive silver prices sharply higher.

In 2011, silver hit near $50 again, but this time there wasn’t the slightest hint of excessive speculative buying in silver futures, an area I monitor closely. Instead, the price surge was due to the physical buying of silver, mainly by way of the silver ETFs (investment vehicles that didn’t exist in 1980). The sharp price fall, starting in May 2011, was engineered by interests associated with JPMorgan and did succeed in persuading the silver ETF investors who drove prices higher to sell.

The coming silver price surge to $50 (and beyond) will be driven by both physical and paper buying and will occur against a backdrop far more bullish than existed in either 1980 or 2011. For one thing, there is far less silver in the world than existed in 1980, as a result of a deficit consumption pattern that prevailed for at least 25 years (to 2005). And while there is just as much (or more) physical silver in the world today than existed in 2011, that silver is now owned by investors (including JPMorgan) in the world’s silver ETFs to an extent never witnessed.

Of the 2 billion oz of silver that exist in 1000 oz bar form (the form that matters most to price), more than 1.1 billion oz (or 55%) is owned by the world’s silver ETFs. (Another 300 million oz are held in the COMEX warehouses, making the total amount of silver bullion in recorded form a remarkable 70% of all the silver in the world). Back in 2011, there was less than half that amount in the world’s silver ETFs. In 1980, investors held no silver in the world’s silver ETFs, since they were only introduced in 2006 and later. The key point here is that there is demonstrably less physical silver available today than in 1980 and 2011. Yet, at the same time, there are many trillions or more investment dollars sloshing around and looking for an investment home.

One important consideration often overlooked is that the first price run up to $50 in 1980 resulted in a literal avalanche of silver coming to market, in the form of old coins, as well as silver artifacts of every type imaginable, including silverware and serving pieces. Quite literally, hundreds of millions of ounces came to market in the Great Silver Melt of 1980. After all, silver’s price had been, essentially, fixed at little more than a dollar an ounce for many decades before 1980. It mattered little that discounts of 50% and greater were received for the silver artifacts melted – the price advance was great enough to provide a windfall for the sellers.

In addition, the US Government would come to sell the remaining hundreds of millions of silver ounces it still held in 1980 over the next 20 years, either by auctions or in coinage for the American Silver Eagle program started in 1986. In the silver run up to $50 in 2011, there was a second wave of melting, but nowhere near as large as the melt in 1980. The striking thing about the Great Melt in 1980 and its minor sequel in 2011, is that once someone sells his or her unwanted silver artifacts, they can’t be sold again. The unmistakable conclusion is that the next run to $50 will not bring great supplies of silver to the market because there is not that much left remaining to be melted. And just like in 2011, the US Government can’t dispose of silver since it doesn’t own any – a far cry from the 5 billion oz it held in 1940.

All the while, the physical industrial demand for silver, from 1980 or 2011, has increased, while since 2011, mine production has been static, due to the ongoing price manipulation on the COMEX. Remarkably and owing to silver’s great industrial versatility, the former main use of silver in photography almost disappeared (due to digital photography), only to be replaced by demand for new uses, such as for solar panels, a use that didn’t exist in 1980 and that has grown by leaps and bounds since 2011. Take a look around and try to deny that the modern world isn’t becoming more electronic and electrical every day and that the world’s best electrical conductor, silver, won’t play a vital and expanding role.

The absolute key to the coming silver price surge to $50 and beyond is the same force in play in 1980 and 2011, namely, investment demand. But whereas investment demand suddenly exploded in 1980 and 2011, silver investment demand has been surging for years to this point – not only growing as prices have remained stagnant, but engendering such a rabid belief in the higher prices to come that any thought of liquidation on lower prices seems absurd. There’s even a grassroots Internet movement that has sprung up over the past less than two years that is devoted to promoting the buying of silver that numbers in the hundreds of thousands. No such movement exists in any other commodity, not even gold.

Perhaps the biggest difference between the two past runs to $50 in silver and the coming run is the state on the ongoing COMEX price manipulation, orchestrated by large traders classified as commercials, but in reality, are mostly banks which are just speculators masquerading as legitimate hedgers. In fact, the origins of the long-running COMEX price manipulation had its roots in the Hunt Bros bust in 1980 and began in earnest in 1982, 40 years ago. On second price run up to $50 in 2011, the COMEX price manipulators (at this time lead by JPMorgan) bent, but did not break and succeeded in turning prices sharply lower, starting on May 1, 2011.

But the near-financial death to JPMorgan and other large short sellers into April 2011, taught the bank a lesson that could only be learned by first-hand experience. It was the unexpected surge to $50 in 2011 that taught JPM of the critical balance between how much physical silver existed in the world and how easily an increase in investment demand would send prices sharply higher. Being the criminal masterminds that I believe JPMorgan to be, it put this sudden realization into practice by continuing the downward price manipulation with selective and concentrated short sales of COMEX futures contracts to keep silver prices as cheap as possibly, but with a criminal genius new twist, namely, accumulating as much physical silver (and gold) as it could, while keeping prices artificially depressed.

And it worked like a charm over the next decade, with the result that JPMorgan and its hidden interests accumulated more than a billion oz of silver and over 30 million oz of physical gold. If anything, I believe my estimates may be too low, rather than too high. Sure, it cost JPMorgan some regulatory frictional expenses over the years, including a $920 million settlement with the Justice Dept and CFTC, but what’s hundreds of millions of dollars when the potential payday is in the many tens of billions of dollars?

Therefore, the biggest difference between the two prior run ups to $50 in silver and the coming run to $50 and beyond is that the coming run will mark the end of the long-running COMEX price manipulation. To be blunt, the COMEX silver manipulation has been the longest-running price manipulation in history and the principal manipulators, a series of large banks and financial institutions, made a boatload of money for nearly the entire 40-year episode, up until mid-2019 or so, as JPMorgan began its-long awaited exit from the short side of COMEX contracts and fully-completed by the spring of 2020. Abandoned by their former ringleader on the short side, the remaining large commercial shorts began to suffer large losses for the first time in nearly 4 decades.

More recently, since March 8, the remaining big commercial shorts on the COMEX, no doubt sensing the coming end to the long-running manipulation, resorted to the only true remedy for closing out as many of their COMEX silver (and gold) short positions as possible, namely, by arranging what I believe to be the final selloff and tricking the commercials’ main counterparties, the managed money traders to sell heavily so that the commercials could buyback and rid themselves of as many COMEX short positions as possible. And it certainly appears that the commercial manipulators have succeeded in doing just that, as the commercial-only concentrated short positions in both COMEX silver and gold have reached historically-low levels of late. Throw in an unmistakable developing physical silver shortage – the inevitable result of a long-term downward price manipulation – and the ingredients for the next price run to $50 and beyond appear firmly in place.

Today, there are more people than ever that understand that silver has been artificially depressed in price and that are putting their money behind that understanding. This was not the case at all in 1980 or 2011 and just about guarantees that silver will soon lift off in price to the former peak levels and beyond. There has never been a set up like this before and it would be a shame not to take advantage of it.

Ted Butler

October 27, 2022

END

4. OTHER PHYSICAL SILVER/GOLD COMMENTARIES

5.OTHER COMMODITIES: URANIUM/ENERGY

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.3001

OFFSHORE YUAN: 7.3208

SHANGHAI CLOSED DOWN 22.44 PTS OR 0.77%

HANG SENG CLOSED DOWN 176.04 OR 1.18%

2. Nikkei closed UP 482.26PTS OR 1.78%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 111.07/Euro FALLS TO 0.99281

3b Japan 10 YR bond yield: FALLS TO. +.239!!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 148.65/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.140%***/Italian 10 Yr bond yield RISES to 4.221%*** /SPAIN 10 YR BOND YIELD RISES TO 3.187%…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.571//

3j Gold at $1640.75//silver at: 19.16 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 12/100 roubles/dollar; ROUBLE AT 61.40//

3m oil into the 86 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 148.65DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 1.0006– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9933well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

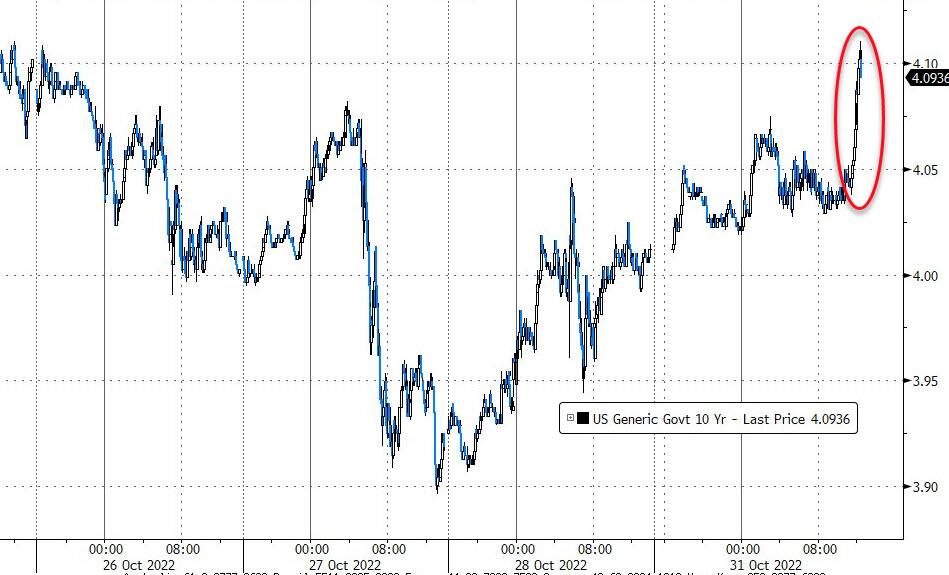

USA 10 YR BOND YIELD: 4.068% UP 4 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 4.148% UP 2 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,62…GETTTING DANGEROUS

GREAT BRITAIN/10 YEAR YIELD: 3.5205%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Rally Fizzles As Fed Looms

MONDAY, OCT 31, 2022 – 08:05 AM

US futures were mixed at the start of another busy week of earnings and key central bank decisions, after posting their best two-week rally since November 2020, with investors bracing for the Federal Reserve’s meeting and another busy earnings week. S&P 500 futures were down 0.4 as of 7:30 a.m. in New York, having dipped as much as 0.7% earlier, after the index closed 2.4% higher on Friday, while Nasdaq 100 futures fell 0.7%. Both gauges are set to pare gains for October, which has been the best month since July. The market drop was led by chipmakers and Chinese stocks. The 10-year Treasury yield hovered around 4.04% after surging by nine basis points on Friday, but has receded from about 4.25% in the past week; yields on UK gilts were steady ahead of what could be the Bank of England’s biggest interest-rate hike in more than 30 years. The dollar rose as the yen and pounds reversed much of last week’s gains. Crypto unexpectedly spiked.

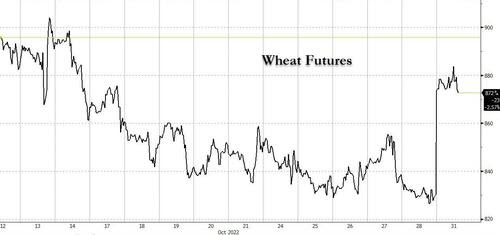

Wheat soared after Russia pulled out of a grain-export deal even as vessels continued to depart from Ukraine.

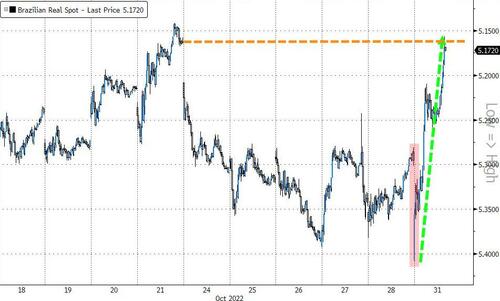

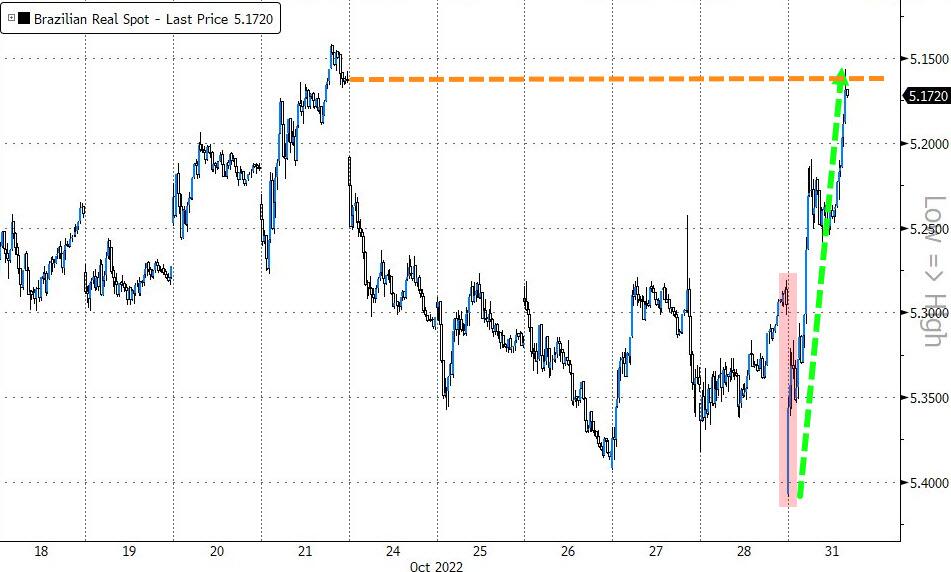

Brazilian assets are set to weaken on Monday after Luiz Inacio Lula da Silva won the presidential election. The extent of the market drop will depend on whether President Jair Bolsonaro will concede as a contested election would likely trigger larger losses.

In premarket trading, U.S-listed shares of Brazilian oil firm Petrobras tumbled as much as 11% after Luiz Inacio Lula da Silva won the presidential election, amid concerns about how the left-wing politician will impact the firm. In other premarket moves, Chinese stocks listed in the US declined after Covid cases spiked across the country while factory and services activity weakened more than expected. US chipmakers fell after Foxconn Technology Group, the world’s largest maker of iPhones, said it may boost capacity at alternative sites to mitigate potential disruption at its main Covid-stricken plant in China. Other notable premarket movers:

- Y-mAbs Therapeutics (YMAB US) shares slumped as much as 38% in US premarket trading, as the stock was downgraded by Kempen and JPMorgan analysts after the drug developer’s cancer drug omburtamab failed to win a nod from an FDA panel, with Kempen not expecting the treatment to win FDA approval and Cowen calling the vote outcome “unfortunate.”

- Chinese stocks listed in the US decline in premarket trading after Covid cases spiked across the country while factory and services activity weakened more than expected.

- Alibaba (BABA US) falls 1.9%, Baidu (BIDU US) -2.8%, Pinduoduo (PDD US) -1.5%, Li Auto (LI US) -4.2%, Nio (NIO US) -1.4%

- Selina Hospitality (SLNA US) rises 36% in US premarket trading. Shares have been volatile since they debuted on Thursday following merger with BOA Acquisition Corp. Stock closed down 63% on Friday after a first session ended with the stock rising 348% from the price BOA closed at.

- Hanesbrands (HBI US) falls 3.6% in premarket trading after Wells Fargo double- downgrades to underweight based on rising risks from the macro outlook and the company’s balance sheet.

- Keep an eye on Ceridian (CDAY US) as Barclays raised the recommendation on the stock to equal-weight from underweight, citing the company’s international expansion strategy, shift to more cloud and product investments.

- Watch Gilead Sciences (GILD US) stock as it was raised to equal-weight from underweight at Barclays, which sees strong commercial execution justifying higher estimates. Meanwhile, the brokerage cut its rating on Amgen (AMGN US) to underweight from equal-weight.

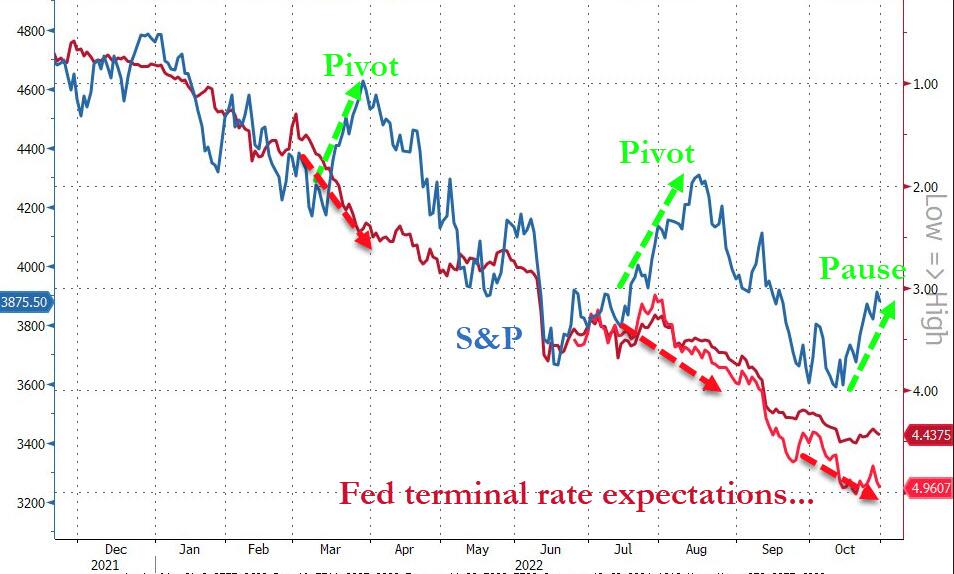

Sparking debate about another split between fundamentals and technicals, US stocks ended last week with sizeable gains despite very disappointing earnings from tech giants including Meta, Amazon and Microsoft. That said, overall earnings season has been quite positive (thanks to sharp estimate cuts in recent weeks), with a majority of companies beating estimates, although fewer than in the past few seasons. Meanwhile, some economic data, including plunging home sales, indicated the Federal Reserve’s fight against inflation is working, fueling hopes of a sooner than expected pivot in rate policy.

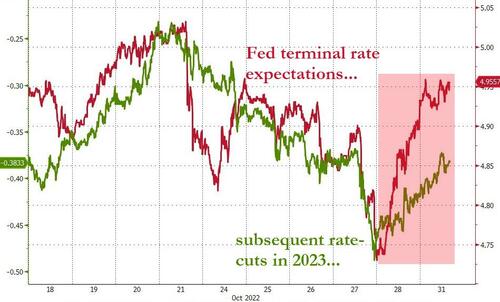

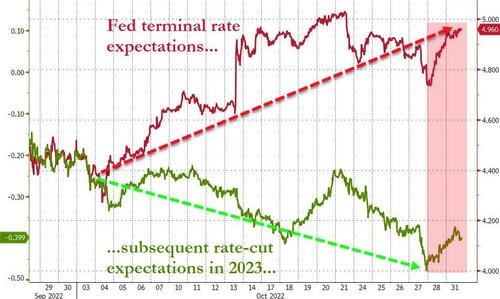

“The market is pricing in by next spring a 5% Fed fund rate — this is a massive tightening cycle, one of the fastest in history, and I think essentially, it’s in the price right now,” said Yves Bonzon, Julius Baer Group CIO on Bloomberg TV, warning that even if the Fed pauses, the quantitative tightening actually continues.

Hopes for a Fed pivot rose after a lower-than-expected rate hike from the Bank of Canada last week and a perceived change of tone from the European Central Bank. Tweets from Nick Timiraos last Friday also sparked a dovish sentiment reversal. The WSJ’s Fed mouthpiece sought to reverse some of the euphoria over the weekend, however, as we discussed here.

“This week’s Fed meeting is critical for the rally to continue, pause or even end completely,” Morgan Stanley strategists led by Michael Wilson wrote in a note on Monday, noting macro-economic indicators “support a Fed pivot sooner rather than later.”

In Europe, the Stoxx 600 was little changed, with travel and financials outperforming, while consumer and commodities sectors fell. In Asia, stocks advanced, boosted by Hong Kong technology shares, with gains also seen from Japan to Australia.

Fed Chairman Jerome Powell “should be a bit less hawkish”at his press conference on Wednesday compared to after the last meeting, according to Yardeni Research. With the expectation that another 75 basis points is penciled in this week, “Powell will have to acknowledge that the federal funds rate is now further into restrictive territory and will be even more so come the FOMC’s December meeting,” it said in a note.

In Europe, the Stoxx 600 was little changed, with travel and financials outperforming, while consumer and commodities sectors fell. Mining and energy stocks underperformed in Europe, where the benchmark fluctuated.Here are some of the biggest European movers:

- International Distributions Services rises as much as 8.7%, the most intraday in almost a year, after the UK government said it won’t take any further action under a national security law in relation to a potential stake increase by Czech billionaire Daniel Kretinsky’s Vesa Equity Investment.

- Credit Suisse shares climb as much as 5% after it announced expected terms for its capital increase and after the Saudi National Bank ruled out raising its stake further for the time being.

- UK bank stocks including NatWest and Lloyds rise after the Sunday Times reported that the UK government is unlikely to seek more windfall taxes on bank profits.

- Know IT gains as much as 7.8%, extending gains into a third day, after Swedish business daily Dagens Industri labeled the IT consultancy’s shares a “bargain,” saying the company will benefit greatly from “megatrends” such as the shift to digitalization.

- Loomis falls as much as 6.7%, before paring the drop, after Carnegie cut its recommendation for the Swedish cash handling firm to hold from buy after strong year-to-date performance, saying the shares are approaching fair value.

- Pandora falls as much as 2.7% after the Danish jeweler on Oct. 30 said a fire has affected its European distribution center in Hamburg, Germany.

- Exmar shares drop as much as 11%, erasing a post-earnings gain on Friday, after an analyst at ING writes that the total potential book gain on a divestment by the gas transporter may be lower than expected.

- Verbund falls as much as 5.3% after Credit Suisse says it expects the power firm to be negatively impacted by rising interest rates, as well as the risk of adverse political intervention and falling power prices.

- Fresenius SE gains as much as 4.6% after the German health care company published a better-than-feared quarterly figure.

- EMS-Chemie fell as much as 4.8% after Berenberg cut the stock to hold from buy, saying the chemicals firm’s valuation is “too expensive.”

Euro-area inflation surged to a fresh all-time high, while the bloc’s economy lost momentum — reinforcing fears that a recession is now all-but unavoidable. That’s after a core gauge of US inflation accelerated in September, bolstering the case for more tightening.

In Asia, stocks advanced, boosted by Hong Kong technology shares, with gains also seen from Japan to Australia, as optimism on corporate earnings and a lift from Apple offset disappointment with Chinese economic data. The MSCI Asia Pacific Index climbed as much as 1.1% before halving the advance in afternoon trading. Tech-heavy markets of South Korea and Taiwan saw indexes rise more than 1%, while key gauges in China and Hong Kong extended last week’s rout. Samsung, TSMC and other Apple suppliers in Asia staged a rally after the iPhone maker jumped nearly 8% Friday, fueling gains on Wall Street. Apple’s results were seen as positive in contrast with disappointing recent announcements from other tech giants.