harveyorgan · in Uncategorized · Leave a comment·Edit

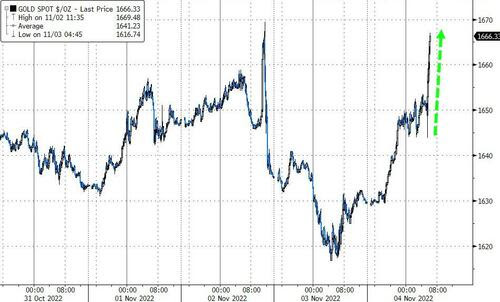

GOLD PRICE CLOSE: UP $44.45 to $1673.30

SILVER PRICE CLOSE: UP $1.31 to $20.74

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1681.00

Silver ACCESS CLOSE: 20.88

New: early yesterday morning//

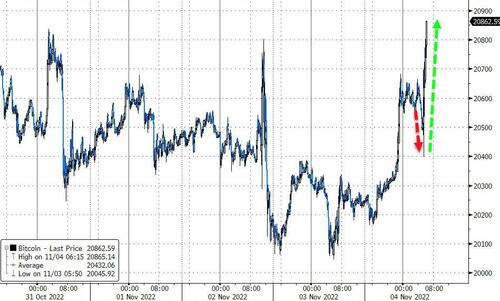

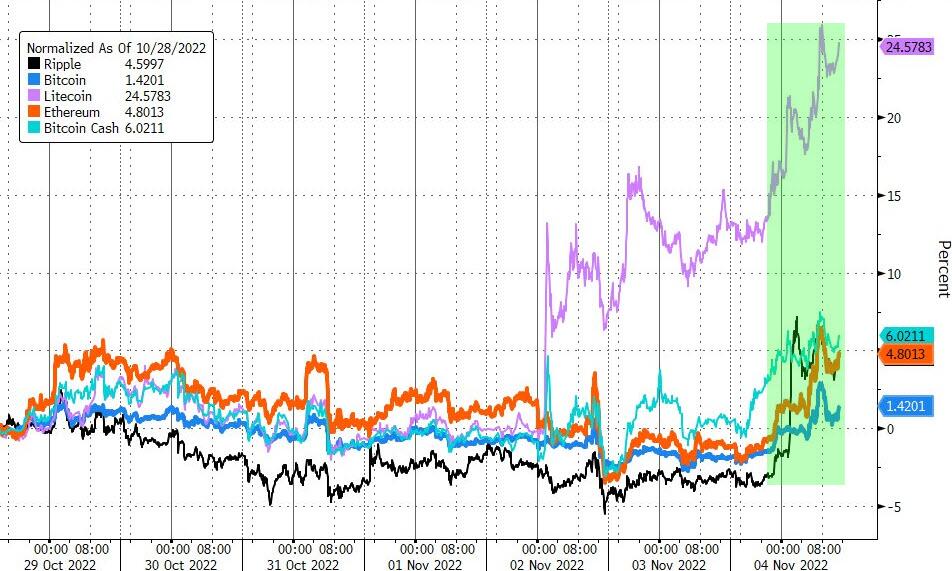

Bitcoin morning price: $20,606 UP 334

Bitcoin: afternoon price: $20,989 UP 637

Platinum price closing UP $34.95 AT $957,45

Palladium price; closing UP $37,35 at $1852.90

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: 2264.08 DOLLARS UP 24.45 CDN DOLLARS PER OZ

BRITISH GOLD: 1476;38 POUNDS PER OZ UP 17.80 POUNDS PER OZ

EURO GOLD: 1686,67 EUROS PER OZ UP 15.03 EUROS PER OZ.

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

DLV615-T CME CLEARING

BUSINESS DATE: 11/03/2022 DAILY DELIVERY NOTICES RUN DATE: 11/03/2022

PRODUCT GROUP: METALS RUN TIME: 20:27:57

EXCHANGE: COMEX

CONTRACT: NOVEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,627.300000000 USD

INTENT DATE: 11/03/2022 DELIVERY DATE: 11/07/2022

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 147 16

190 H BMO CAPITAL 53

323 C HSBC 33

435 H SCOTIA CAPITAL 23

657 C MORGAN STANLEY 2

661 C JP MORGAN 458 189

732 C RBC CAP MARKETS 3

737 C ADVANTAGE 45 20

800 C MAREX SPEC 11 5

880 C CITIGROUP 53

880 H CITIGROUP 311

905 C ADM 3

TOTAL: 686 686

JPMORGAN STOPPED 189/1686

GOLD: NUMBER OF NOTICES FILED FOR NOV. CONTRACT: 686 NOTICES FOR 68,600 OZ or 2.1337 TONNES

total notices so far: 4553 contracts for 455,300 oz (14.1617 tonnes)

SILVER NOTICES: 0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month 154 : for 770,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $44.45

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////A BIG CHANGE IN GLD INVENTORY: A WITHDRAWAL OF 3.48 TONNES FROM THE GLD// /INVENTORY LOWERS TO 920.57 TONNES

INVENTORY RESTS AT 911.59 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $1.31

AT THE SLV// :/SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF OF 4.972 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 477.678 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A FAIR SIZED 376 CONTRACTS TO 139,096 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE SMALL LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.16 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS/HFT WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.16)., AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS, AS WE HAD A HUGE GAIN IN OUR TWO EXCHANGE OF 1015 CONTRACTS. WE HAD ZERO SPEC SHORT COVERING THEIR SHORTFALLS, BUT MASSIVE SHORT ADDITIONS // OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. SOME NEWBIE SPEC LONGS ADDED TO THEIR POSITIONS ESPECIALLY AT THE LOWER PRICES

WE MUST HAVE HAD:

I) ZERO SPECULATOR SHORT COVERINGS BUT HUGE SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /// SOME NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.045 MILLION OZ FOLLOWED BY TODAY’S 85,000 QUEUE JUMP//NEW STANDING:1.305 MILLION OZ/ / // V) FAIR SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: +36

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF NOV:

TOTAL CONTRACTS for 4 days, total 3465 contracts: 17.325 million oz OR 4.331MILLION OZ PER DAY. (866 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 17.325 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 17.325 MILLION

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 340 DESPITE OUR $0.16 LOSS IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 675 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR NOV. OF 1.345 MILLION OZ FOLLOWED BY TODAY’S 85,000 QUEUE JUMP/ .. WE HAVE A HUGE SIZED GAIN OF 1015 OI CONTRACTS ON THE TWO EXCHANGES FOR 5.075 MILLION OZ..

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GIGANTIC SIZED 15,685 CONTRACTS TO 482,745 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -185 CONTRACTS.

.

THE GIGANTIC SIZED INCREASE IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $18.30//COMEX GOLD TRADING/THURSDAY // ZERO SPECULATOR SHORT COVERINGS//HUGE SPEC SHORT ADDITIONS, ACCOMPANYING OUR MONSTER SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD SOME LONG LIQUIDATION // CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR NOV. AT 12.386 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S MONSTER 98,800 OZ QUEUE JUMP //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR FALL IN PRICE OF $18.30 WITH RESPECT TO THURSDAY’S TRADING

WE HAD AN ATMOSPHERIC SIZED GAIN OF 26,875 OI CONTRACTS 83.593 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A MONSTER SIZED 11,190 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 482,743

IN ESSENCE WE HAVE AN ATMOSPHERIC SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 26,875 CONTRACTS WITH 15,685 CONTRACTS INCREASED AT THE COMEX AND 11,190 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 27,060 CONTRACTS OR 84.167 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (11,190) ACCOMPANYING THE GIGANTIC SIZED GAIN IN COMEX OI (15,675): TOTAL GAIN IN THE TWO EXCHANGES 26,875 CONTRACTS. WE NO DOUBT HAD 1) ZERO SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS AS WELL AS HUGE SHORT SPEC GAINS/// // CONSIDERABLE NEWBIE SPEC ADDITIONS AT THE LOWER PRICE ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR NOV. AT 12.386 TONNES FOLLOWED BY TODAY’S MONSTER QUEUE JUMP OF 98,800 OZ //NEW STANDING 20.090 TONNES///3) ZERO LONG LIQUIDATION //// //.,4) GIGANTIC SIZED COMEX OPEN INTEREST GAIN 5) MONSTER ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

NOV

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV. :

19,343 CONTRACTS OR 1,934,300 OZ OR 60.16 TONNES 4 TRADING DAY(S) AND THUS AVERAGING: 4835 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY(S) IN TONNES: 60.16 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 60.16/3550 x 100% TONNES 1.69% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 60.16 TONNES//INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A FAIR SIZED 376 CONTRACT OI TO 139.096 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 675 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 650 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 675 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 376 CONTRACTS AND ADD TO THE 650 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 1055 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 5.255MILLION OZ//

OCCURRED DESPITE OUR FALL IN PRICE OF $0.16

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 72.99 PTS OR 2.43% //Hang Seng CLOSED UP 821.65 OR 5.36% /The Nikkei closed DOWN 463.65 OR 1.68% //Australia’s all ordinaires CLOSED UP 0.55% /Chinese yuan (ONSHORE) closed UP TO 7.2467 //OFFSHORE CHINESE YUAN DOWN 7.2300// /Oil UP TO 91,36 dollars per barrel for WTI and BRENT AT 97.79 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GIGANTIC SIZED 15,685 CONTRACTS TO 482,743 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR HUGE FALL IN PRICE OF $18.30 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A POWERFUL SIZED EFP (11,140 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED HUGE NUMBER OF SPECS TO GO MASSIVELY SHORT AND NOW THEY WILL BE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON -ACTIVE DELIVERY MONTH OF NOV.. THE CME REPORTS THAT THE BANKERS ISSUED A POWERFUL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 11,190 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 11,190 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 11,190 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: AN ATMOSPHERIC SIZED TOTAL OF 26,875 CONTRACTS IN THAT 11,190 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GIGANTIC SIZED COMEX OI GAIN OF 15,685 CONTRACTS..AND THIS MONSTROUS SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR HUGE FALL IN PRICE OF GOLD $18.30//WE HAD HUGE SPEC SHORTS ADDITIONS WITH BANKERS AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD STRONG ADDITIONAL NEWBIE SPECS GOING LONG WITH ZERO SPEC SHORT COVERINGS

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING NOV (20.087),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 20.087 TONNES/INITIAL (TOTAL SO FAR THIS YEAR 564.435 TONNES)

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $18.30) AND WERE SOMEWHAT SUCCESSFUL IN KNOCKING OFF SOME SPECULATOR LONGS AS WE HAD AN ATMOSPHERIC SIZED GAIN ON OUR TWO EXCHANGES//// SPEC SHORTS COVERED ZERO OF THEIR POSITIONS, BUT DID ADD A HUGE QUANTITY TO THEIR SHORT SIDE AS WE HAD A MONSTROUS SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 27060 CONTRACTS // WE HAVE GAINED A TOTAL OI OF 84.167 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR NOV. (20.087 TONNES)…THIS WAS ACCOMPLISHED DESPITE OUR FALL IN PRICE OF $0.55

WE HAD -185 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 26,875 CONTRACTS OR 2,687,500 OZ OR 83.593 TONNES

Estimated gold volume 281,811// fair to good//

final gold volumes/yesterday 292,651/ fair to good

INITIAL STANDINGS FOR NOVEMBER 2022 COMEX GOLD //NOV 4

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 66,752.454oz Brinks Delaware Manfra includes 1003 kilobars/Brinks |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 686 notice(s) 68,600 OZ 2.1377 TONNES |

| No of oz to be served (notices) | 1905 contracts 190,500 oz 5.924 TONNES |

| Total monthly oz gold served (contracts) so far this month | 4553 notices 455,300 14.1617TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals:3

ii) Out of Brinks 32,247.460 (1003 kilobars)

ii) Out of Delaware 9963.085 oz

iii) Out of Manfra 24,641.454 oz

total: 66,752.454 oz

total in tonnes: 2.076 tonnes

Adjustments: 4// all dealer to customer

i) Out of Brinks 17,747.352 oz

ii) Out of jPMorgan 12,298.967 oz

iii) out of Loomis: 35,108.892 oz

iv) Out of Manfra: 37,275.848 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR NOVEMBER.

For the front month of NOV. we have an oi of 2591 contracts having LOST ONLY 63 contracts. We had 1050 notices served on THURSDAY so we gained a whopping 987

or an additional 98,700 OZ (3.07 TONNES) will stand in this non active month of November. We will have Nov gold tonnage standing increase daily from this day forth until the end of the month.

This queue jumping originates in London with the exercising of London based EFP’s for comex gold.

December GAINED 1081 contracts UP to 348,168.

JANUARY GAINED 1 contract to stand at 37.

February gained 12,220 contacts up to 94,423.

We had 686 notice(s) filed today for 68,600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 458 notices were issued from their client or customer account. The total of all issuance by all participants equate to 686 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 189 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the NOV. /2022. contract month,

we take the total number of notices filed so far for the month (4553) x 100 oz , to which we add the difference between the open interest for the front month of (NOV 2591 CONTRACTS) minus the number of notices served upon today 686 x 100 oz per contract equals 645,800 OZ OR 20.087 TONNES the number of TONNES standing in this non active month of NOV.

thus the INITIAL standings for gold for the NOV. contract month:

No of notices filed so far (4553) x 100 oz+ (2591) OI for the front month minus the number of notices served upon today (686} x 100 oz} which equals 645,800 oz standing OR 20.087 TONNES in this NON active delivery month of NOV..

TOTAL COMEX GOLD STANDING: 20.090 TONNES (A HUMONGOUS STANDING//NEW RECORD FOR NOV (GENERALLY THE POOREST DELIVERY MONTHS FOR A NON ACTIVE MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,008,987.584 OZ 62.48 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 24,595,130.845 OZ

TOTAL REGISTERED GOLD: 11,228,894.295 OZ (349.265tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 13,367,236.550OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,219,907 OZ (REG GOLD- PLEDGED GOLD) 286.77 tonnes//rapidly declining

END

SILVER/COMEX

NOV 4//INITIAL NOV. SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 24,172.570 oz CNT Brinks |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,200,528.210 oz HSBC Loomis |

| No of oz served today (contracts) | 0 CONTRACT(S) (nil OZ) |

| No of oz to be served (notices) | 107 contracts (535,000 oz) |

| Total monthly oz silver served (contracts) | 154 contracts (770,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 withdrawals out of the customer account

i) Out of Brinks 3950.400 oz

ii) Out of CNT: 20,222.170 oz

Total withdrawals: 24,172.570 oz

JPMorgan has a total silver weight: 154,725million oz/300.390 million =51.51% of comex .//dropping fast

Comex deposits: 2

i) Into HSBC: 600,801.380 oz

ii) Into Loomis: 599,726.830 os

total: 1,200,528.210 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 34.810 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 300.390 MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF NOV OI: 107 CONTRACTS HAVING LOST 46 CONTRACT(S.)

WE HAD 63 NOTICES FILED ON THURSDAY, SO WE GAINED 17 CONTRACTS OR AN ADDITIONAL 85,000 OZ WILL STAND

FOR SILVER IN THIS VERY NON ACTIVE DELIVERY MONTH OF NOVEMBER.

DECEMBER SAW A LOSS OF 1352 CONTRACTS DOWN TO 103,011 (WE WILL HAVE A DANDY DEC. DELIVERY MONTH)

JANUARY SAW A GAIN OF 39 CONTRACTS UP TO 1283 CONTACTS.

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY:0 for NIL oz

Comex volumes:72,926// est. volume today// very good

Comex volume: confirmed yesterday: 68,586 contracts ( good)

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 154 x 5,000 oz = 770,000 oz

to which we add the difference between the open interest for the front month of NOV(107) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the NOV../2022 contract month: 154 (notices served so far) x 5000 oz + OI for front month of NOV (107) – number of notices served upon today (0) x 5000 oz of silver standing for the NOV. contract month equates 1,305,000 oz.

We will gain in silver oz standing from this day forth until the end of the month.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:104,869// est. volume today// huge/shorts covered

Comex volume: confirmed yesterday: 77,563 contracts ( good)

END

GLD AND SLV INVENTORY LEVELS

NOV 4/WITH GOLD UP $44.45 TO $1673.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.48 TONNES FROMTHE GLD////INVENTORY RESTS AT 911.59 TONNES.

NOV 3/WITH GOLD DOWN $18.30 TO $1628.85: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.05 TONNES FROM THE GLD////INVENTORY RESTS AT 915.07 TONNES

NOV 2/WITH GOLD UP 55 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 919.12 TONNES.

NOV 1/WITH GOLD UP $9.20 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES FORM THE GLD../INVENTORY RESTS AT 920.57 TONNES

OCT 31/WITH GOLD DOWN $4.00; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD//INVENTORY RESTS AT 922.59. TONNES//

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

GLD INVENTORY: 911.59TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

NOV 4/WITH SILVER UP $1.31 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.972 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 3.WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 566,000 OZ FROM THE SLV////INVENTORY RESTS AT 482.650 MILLION OZ//

NOV 2/WITH SILVER DOWN 9 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 92,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.216 MILLION OZ//

NOV 1/WITH SILVER UP 53 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 415,000 OZ FORM THE SLV////INVENTORY RESTS AT 483.308 MILLION OZ

OCT 31: WITH SILVER FLAT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .644 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 483.723 MILLION OZ//

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: A WITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

CLOSING INVENTORY 477.678 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

–HOW GLOBAL MARKETS FAIL AND GOLD SUCCEEDS: DEBT, DERIVATIVES & POLITICIZED (I.E., DISHONEST) CENTRAL BANKS

Egon von Greyerz..

https:/https://www.youtube.com/watch?v=84toOT7boEI&t=165s

Matterhorn Asset Management’s founding partner, Egon von Greyerz, joins Darryl and Brian Panes of As Good as Gold Australia for an in-depth discussion on the state of global financial markets and the inevitable demise of paper currency and rise of physical gold.

In an alarming backdrop of falling markets, open war, pandemic overreach, record-breaking debt levels and increased supply chain pressures, the Panes ask the obvious question: What and who led to this now undeniable global mess? As indicated by a recent observation in The Economist, the main culprit offered therein is the absolute mismanagement of fiat currencies by central banks around the world. Such mismanagement (living on deficits rather than surpluses) has been the direct cause of equally unprecedented and unsustainable global debt levels of which no intelligent business or family could ever conceive and yet which governments around the world pursue on a daily basis.

Egon, of course, is glad to see more periodicals like The Economist finally addressing such issues, but these central-bank-driven boom and bust cycles engineered by grotesque levels of fantasy/mouse-clicked fiat currencies and unpayable debt levels are forces of which he has been warning for over 20 years. All fault and responsibility easily begins with the money printers in general and the Fed in particular. But as political rather than financial players, central bankers will do what all politicians do—assign blame elsewhere.

Toward that end, the crippling inflation, currency, market, pension, trade and suicidal energy policies pursued by the EU under the misguided pressure of the US will be blamed on Putin today (COVID yesterday and global warming tomorrow) rather than decades of the self-destructive debt-print-and-spend policies of the global central banks.

Turning to gold, Egon draws careful comparison to the DOW/gold ratio and argues for a dramatically falling DOW and equally dramatic rise in the free-pricing of physical gold once paper currencies and futures contracts in the soon-to-implode derivatives markets lose all credibility.

Markets have enjoyed a “stay of execution” by inflationary central bank money printing for far too long, and this has exponentially increased the global debt levels and hence global risk levels. Again, and as Egon reminds, this is a direct result of years of central bank madness. In the end, however, history is a clear guide of the inevitable consequences of such policy insantiy, namely the ruin of paper currencies and the rise of real, physical assets, including monetary metals like gold.

END

3.Chris Powell of GATA provides to us very important physical commentaries

Your weekend reading material: the Great unwind ii

(Alasdair Macleod)

Alasdair Macleod: The Great Unwind, II

Submitted by admin on Thu, 2022-11-03 10:23Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, November 3, 2022

With price inflation rising out of control and interest rates rising strongly, the trading environment for commercial banks has fundamentally changed. With bad debts looming and bond prices in entrenched downtrends, procrastination is now the enemy of bankers.

We are at the beginning of The Great Unwind, and this article elaborates on my first article for Goldmoney on the subject, published here:

https://www.goldmoney.com/research/banking-crisis-the-great-unwind?gmrefcode=gata

The imperative for bankers to respond to these conditions overrides all other matters if their businesses are to survive these changed conditions. We are entering a cyclical downdraft of the bank credit cycle that promises to be cataclysmic. And the monetary policy planners at the central banks can do nothing to stop it.

After outlining the scale of the problems faced by each global systemically important bank, this article looks at the future for the $600 trillion derivatives mountain. It was born out of the long-term decline in interest rates from the mid-1980a, which ended last year. It is almost entirely distributed through banks and shadow banks.

The questions to address are: What is the future for the derivatives mountain now that the long-term trend for falling interest rates is over? And what are the economic consequences? …

… For the remainder of the analysis:

https://www.goldmoney.com/research/the-great-unwind-1?gmrefcode=gata

end

4. OTHER PHYSICAL SILVER/GOLD COMMENTARIES

5.OTHER COMMODITIES:

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 7.2300

OFFSHORE YUAN: 7.2467

SHANGHAI CLOSED UP 72.99 PTS OR 2.43%

HANG SENG CLOSED UP 821.65 OR 5.36%

2. Nikkei closed DOWN 463.65 PTS OR 1.65%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 112.26/Euro RISES TO 0.97954

3b Japan 10 YR bond yield: RISES TO. +.249!!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 147.70/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.286%***/Italian 10 Yr bond yield RISES to 4.451%*** /SPAIN 10 YR BOND YIELD RISES TO 3.345%…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.676//

3j Gold at $1650.95//silver at: 19.95 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 0/100 roubles/dollar; ROUBLE AT 62.10//

3m oil into the 91 dollar handle for WTI and 97 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 147.70DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 1.0063– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9860well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

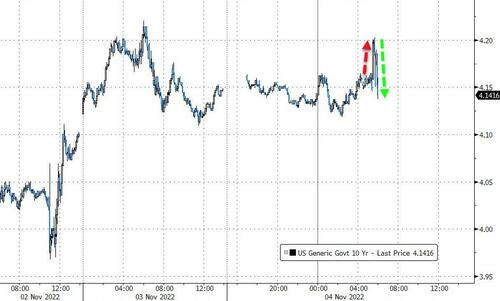

USA 10 YR BOND YIELD: 4.161% UP 4 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 4.200% UP 5 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,62…GETTTING DANGEROUS

GREAT BRITAIN/10 YEAR YIELD: 3.5855%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Jump On China Reopening Rumors Ahead Of Key Jobs Report

FRIDAY, NOV 04, 2022 – 07:58 AM

US futures jumped and the Nasdaq 100 was poised to trim its biggest weekly drop since the start of the year as optimism about China’s reopening boosted Wall Street futures despite the looming risk of another hotter-than-expected payrolls report. As reported earlier, Chinese stocks in Hong Kong headed for their best week since 2015, and the yuan strengthened amid fresh speculation that Beijing was set to ease covid-zero policies. The frenzy was sparked earlier this week on unverified social media posts indicating Beijing could be preparing to exit the strict Covid zero policy. There’s a flurry of new market-friendly headlines adding fuel to the rally, which boosted US-listed Chinese stocks while miners led gains in Europe as commodities rallied, while luxury stocks also got a boost.

After closing at the lowest level since July 2020 on Thursday, as tech stocks fell out of favor this year as the Federal Reserve tightened its monetary policy, Nasdaq 100 contracts rose 0.8% by 5 a.m. in New York after the tech-heavy gauge plunged 7.4% this week, erasing $1.1 trillion in market capitalization. S&P 500 futures gained 0.7%, putting the underlying gauge on track to pare a 4.6% weekly decline — the steepest since September.

In premarket trading, US-listed Chinese stocks like Alibaba Group Holdings Ltd., JD.com Inc., and Baidu Inc. surged as China-linked sentiment got a lift after Bloomberg News reported China is working on plans to scrap a system that penalizes airlines for bringing virus cases into the country, a sign that authorities are looking for ways to ease the impact of the Covid Zero policy. Cloud software stocks dropped in premarket trading after revenue forecasts from peers Atlassian and Twilio fell short of expectations, triggering analyst downgrades. Atlassian falls 23% in premarket trading, the stock is set for its biggest drop since its debut; Twilio fell as much as 27% in premarket trading; the stock is set for its biggest drop since May 3, 2017. Here are some of the other notable premarket movers:

- The conservative-targeting money processor PayPal fell 8.3% in premarket trading after the payments platform cut its forecast for annual revenue amid a slowdown in spending. Analysts note that a strong dollar and other macroeconomic headwinds are weighing on the company’s forecast.

- Block Inc. shares surge 14% in US premarket trading after the digital payments company’s adjusted Ebitda beat expectations and boosted optimism that the company can weather a slowdown in the economy. Brokers in particular singled out the performance of the firm’s Cash App business, saying its potential isn’t fully recognized by investors.

- DoorDash jumps 11% in premarket trading after the food delivery platform topped revenue estimates, driven by strong appetite for takeout. Analysts noted that demand remained resilient and the company does not seem to be affected by inflationary and macro headwinds.

- Coinbase shares rallied as much as 9.1% in US premarket trading, with analysts saying that the cryptocurrency platform provider’s growth in subscription revenue and a narrower loss were reasons for optimism. These positives showed that the company’s efforts to control costs were working, even as trading volume was underwhelming as expected due to the slump in prices of digital currencies this year.

- Kratos forecast adjusted Ebitda for the fourth quarter that missed the average analyst estimate, as the defense and security company faces hiring challenges and supply-chain disruptions. Shares declined 9.3% in US postmarket trading..

- Twilio fell as much as 22% in premarket trading, after the infrastructure software company gave a fourth-quarter revenue forecast that came in below estimates. Analysts noted that the company’s analyst day left them wanting as it “raised new concerns” instead of extinguishing existing ones.

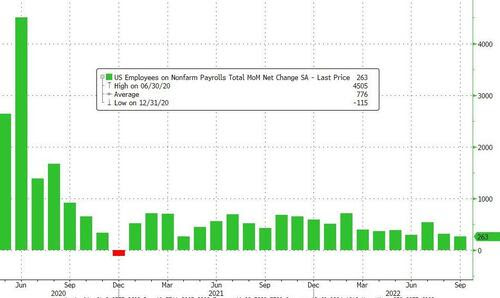

Focus next will turn to US payrolls data at 830am ET on Friday, where 195,000 jobs are expected for October, compared with 263,000 in September. Unemployment rate projected at 3.6% (our payrolls preview is here). The US two-year yield topped 4.75% for the first time since 2007 after a key segment of the curve reached an extreme of inversion not seen since the 1980s, an anomaly that historically preceded economic downturns.

“Key focal point could be the US NFP release tonight which could provide a better sense of tightening trajectory and the eventual peak of terminal rates,” said Fiona Lim, senior currency analyst at Malayan Banking Berhad in Singapore. “Investors chase that flickering light at the end of the Covid-Zero tunnel,” said Stephen Innes, a managing partner at SPI Asset Management.

“Today’s numbers need to be viewed in the light of other labor market statistics that shows labor demand holding up,” said Stuart Cole, head macro economist at Equiti Capital. “The concerns over still strong inflationary pressures will be trumping any meaningful easing that the labor market might be pointing to.”

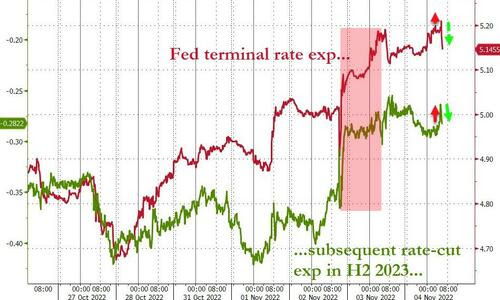

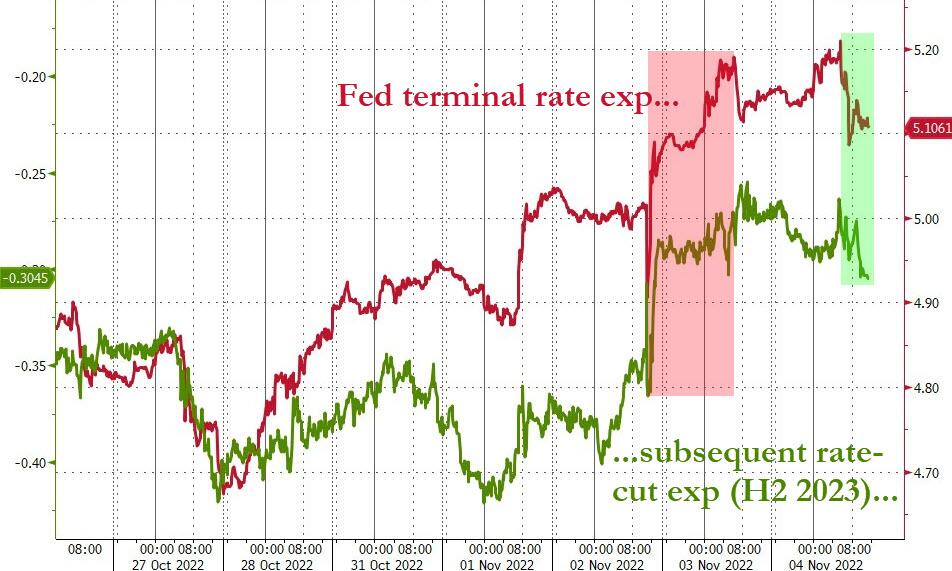

Chair Jerome Powell left little doubt that he’s prepared to push interest rates as high as needed to stamp out inflation after the Fed raised rates by 75 basis points for the fourth time in a row. Traders will parse jobs data due later on Friday for signs of a slowing labor market, which could convince the bank to adopt a less hawkish stance. Swaps that reference future Federal Reserve meetings indicate an expected peak policy rate above 5.14% around mid-2023.

“We think the Fed is much closer to pausing than the market is pricing and much closer than what they’re trying to convey,” said Isaac Poole, chief investment officer at Oreana Financial Services, who expects the US central bank to end hiking by December or January. “Maybe we’ll see a bit more near-term volatility, but I think there are real opportunities for upside in equities over the next 12 months,” he told Bloomberg TV.

European stocks rallied for the first time in the past three sessions on optimism about China’s reopening. Euro Stoxx 50 rallies 1.6%. CAC 40 outperforms peers, adding 1.7%, IBEX lags. Miners, consumer products and chemicals are the strongest performing sectors. Shares with high business exposure to China rallied the most on Friday as authorities were said to be making efforts to ease the impact of their Covid-Zero policy. Europe’s automobile and parts subsector outperformed the Stoxx 600 index, rising as much as 2.0%. Volkswagen, Mercedes-Benz, Ferrari are among the biggest contributors to the sector advance. European luxury stocks also jumped as key market China is said to be preparing a plan to end a system that penalizes airlines for bringing virus cases into the country. Swatch Group is among the best performing rising as much as 3.6%, Richemont +3.3%, Hermes International +2.3%, Burberry +1.3%, Christian Dior +2%, LVMH +1.7%, Pandora +2.6% Italian luxury stocks also jumped with Moncler +2.7%, Tod’s +1.6% and Salvatore Ferragamo +2.6%. Here are some of the biggest European movers:

- Europe’s basic resources sector is the best-performing subindex in the Stoxx 600 benchmark as iron ore heads for its first weekly gain in two months, with traders buying on speculation China may be planning to remove some Covid Zero restrictions. KGHM leads advances, rising 10%, Anglo American +9.4%, Rio Tinto +7%

- Andritz shares jump as much as 11%, the most since July, after results from the hydropower station equipment supplier that analysts said were “excellent” and show the company’s resilience to a tough macro environment

- GN Store Nord climbs as much as 15% after company notified that William Demant Invest has increased its aggregate holding of shares to above 10% of the share capital and voting rights in company.

- Rovi slides as much as 13% with Jefferies flagging that the Spanish pharmaceutical company’s guidance for 2023 as well as 9-month Ebitda missed consensus estimates.

- Leonardo declines as much as 8.4% as worries over inflation overshadow the Italian aerospace technology company’s beat on 3Q Ebita and revenue and its strong orders.

- Kering jumps as much as 5.5% after a report that the French company is in advanced talks to buy Tom Ford.

- Enel falls as much as 3.5% after the Italian power utility cut its adjusted net guidance for the year, partly reflecting a decline in hydroelectric power generation.

Meanwhile, European Central Bank President Christine Lagarde said interest rates may need to be lifted to restrictive levels to drag inflation back to the 2% target. Bank of England Chief Economist Huw Pill said the BOE is trying to strike a balance between bringing inflation back to target and preventing an unnecessarily deep recession by raising interest rates too aggressively.

“Our view has been for a while that the only way central banks can credibly tame inflation is through tighter financial conditions and slower growth,” Barclays analysts wrote in a note. “Chairman Powell made it clear that over tightening may be a less costly option over the long run than doing too little. So as it stands, we find few reasons to stop worrying about a hard landing.”

Earlier in the session, Asian stocks rebounded as China and Hong Kong staged a strong comeback amid speculation that China is poised to exit its stringent Covid-zero policy. The MSCI Asia Pacific Index gained as much as 1.6%, lifted by consumer discretionary and financial shares. Chinese stocks in Hong Kong capped their best week since 2015 as shares linked to reopening jumped amid fresh signs of easing Covid restrictions. Hong Kong’s benchmark Hang Seng Index saw the biggest weekly jump since 2011 and China’s CSI 300 Index capped its best week since mid-2020. The rally follows days of speculation on the back of unverified social media posts detailing a reopening plan. While similar Chinese rallies have all fizzled in recent months, bulls are now betting that some of the world’s lowest valuations have left the nation’s shares primed to surge on any hint of good news. Separately, Chinese President Xi Jinping told German Chancellor Olaf Scholz he opposed the use of nuclear force in Europe, in his most direct remarks yet on the need to keep Russia’s war in Ukraine from escalating.

Part of China’s gains were also spurred by tech companies, with a gauge of tech stocks listed in Hong Kong surging more than 7% after Bloomberg News reported progress in efforts to prevent delisting of hundreds of Chinese stocks from US exchanges. US audit officials completed their first on-site inspection round of Chinese companies ahead of schedule.

But the recent gains might not sustain, according to market watchers. “Market dynamics remain relatively subdued despite some short-lived excitement over chatter around Covid-Zero policy changes,” Morgan Stanley strategists including Laura Wang wrote in a note. She expects near-term volatility to “stay high with complexity around Covid relaxation.” Gains in other Asian markets were relatively subdued, with Japanese shares underperforming the region as the market returned from a holiday. The Asian stock benchmark was poised for a weekly gain of more than 2%, the first in four weeks, as the reopening boost in China offset downside risks from further monetary tightening by the Federal Reserve. Still, the gauge is down about 28% this year

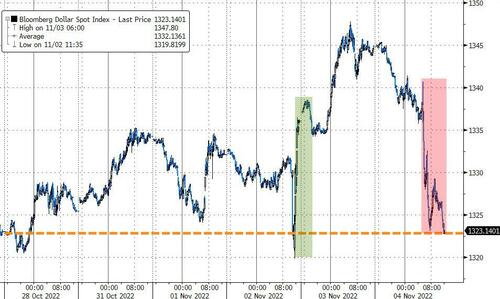

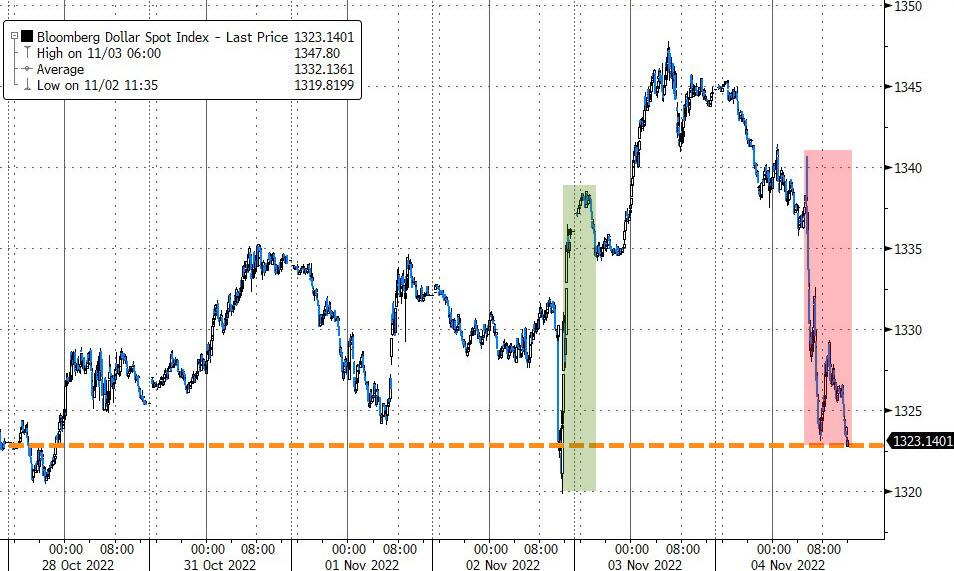

In FX, the Bloomberg Dollar Spot Index slipped 0.5% after rising 0.7% Thursday and the dollar weakened against all of its Group-of-10 peers, in a commodity-currency led advance. DKK and EUR are the weakest performers in G-10 FX, AUD and NZD outperform.

- The euro advanced after slumping all other trading days this week. Bunds were steady while Italian bonds inched up

- The pound rebounded from a two-week low of 1.1150 per dollar and gilts inched up, led by the belly. Money markets pared pricing for BOE hikes by up to 10bps. BOE Chief Economist Huw Pill said the Bank of England is trying to strike a balance between bringing inflation back to target and preventing an unnecessarily deep recession by raising interest rates too aggressively. Pill speaks again later on Friday

- The Australian dollar was the best G-10 performer. The currency rose by as much as 1.2% versus the dollar, and snapped six straight days of declines as Chinese stocks and iron ore prices surged amid China reopening speculation. Australia’s bonds bounced back with RBA’s quarterly monetary policy statement underscoring the central bank’s expectation it will soon reach peak rates even at a modest pace of hikes

In rates, the Treasury curve flattened as yields were between 3bps lower and 2bps higher from yesterday’s close while Germany’s 5y30y yield curve inverts for the first time since late September. Treasury yields slightly cheaper vs Thursday’s close with front-end underperforming — 2-year touched 4.75%, new multiyear high — as market braces for the October jobs report at 8:30am New York time. 2-year yield rose as much as 3.7bp, lagging rest of the curve; 10-year little changed near 4.16% with bunds slightly outperforming and gilts slightly lagging. Front-end underperformance continues to flatten 2s10s spread, which reached -61.9bp, new generational extreme; in Europe, German 5s30s curve inverts for the first time since end of September. Estoxx50 higher by almost 2% into early US session while S&P 500 futures climb 0.8%, paring Thursday’s drop; WTI futures up 3.5%. October jobs report expected to print 195k headline number (whisper number is 231k) with unemployment rate at 3.6%. Price action rangebound in the overnight session, also across core European bonds, while stocks have rallied, led by Estoxx50.

UK bonds fell after Andrew Hauser, executive director for markets at the BOE, said the central bank will outline how it will unwind its recent emergency gilt purchases “shortly.”

In commodities, crude futures rally. WTI up 3% to trade near $91. Brent rises 2.6% to top $97 amid optimism a China will boost oil demand; Commodities are also bolstered by the USD’s pullback and. Saudi Arabia set December Arab light crude OSP to Asia at Oman/Dubai + USD 5.45/bbl, while it set OSP to NW Europe at ICE Brent + USD 1.70/bbl and to the US at ASCI + USD 6.35/bbl. Spot gold has struggled to surpass the USD 1650/oz mark where its 21-DMA lies just above at USD 1651.7/oz, while base metals are deriving broad support on the China/COVID narrative.

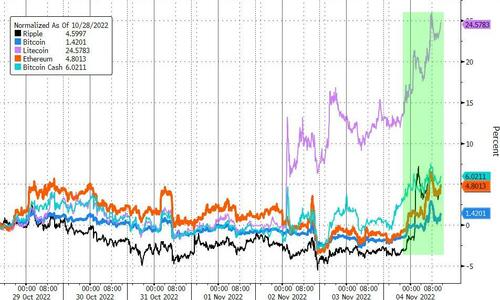

Bitcoin has broken out of the last few sessions tight parameters and resides towards the top end of this range just above the USD 20.5k mark.

Looking to the day ahead now, the main highlight will be the US jobs report for October. Meanwhile in Europe, there’s data on German factory orders, French industrial production and Euro Area PPI for September, alongside the final services and composite PMIs for October. Central bank speakers include ECB President Lagarde, Vice President de Guindos, Bundesbank President Nagel, the Fed’s Collins and BoE Chief Economist Pill.

Market Snapshot

- S&P 500 futures up 0.3% to 3,740.50

- STOXX Europe 600 up 0.7% to 412.46

- MXAP up 1.2% to 139.46

- MXAPJ up 2.3% to 449.33

- Nikkei down 1.7% to 27,199.74

- Topix down 1.3% to 1,915.40

- Hang Seng Index up 5.4% to 16,161.14

- Shanghai Composite up 2.4% to 3,070.80

- Sensex down 0.2% to 60,727.51

- Australia S&P/ASX 200 up 0.5% to 6,892.46

- Kospi up 0.8% to 2,348.43

- German 10Y yield down 1% to 2.22%

- Euro up 0.3% to $0.9774

- Brent Futures up 2% to $96.54/bbl

- Gold spot up 1.1% to $1,647.66

- U.S. Dollar Index down 0.36% to 112.52

Top Overnight News from Bloomberg

- ECB President Christine Lagarde said interest rates may need to be lifted to restrictive levels to drag inflation back to its 2% target

- Inflation in the euro zone will likely remain above the European Central Bank’s target for an extended period, raising the risk of a price-wage spiral, ECB Vice-President Luis de Guindos said in a speech

- German factory orders continued to decline in September, adding to concerns that Europe’s largest economy is slipping into recession as it struggles with surging energy costs. Demand fell 4% from the previous month, a steeper drop than the 0.5% median estimate in a Bloomberg poll of economists and accelerating from a revised 2% decrease in August

- A Federal Reserve Bank of New York experiment has found that a central bank digital currency using distributed ledger technology could reduce the time it takes to settle foreign exchange transactions from two days to under 10 seconds, a top New York Fed official said

- Cash is king, with investors fleeing to the safety of cash funds at the fastest pace since the coronavirus pandemic as the Federal Reserve remains firmly hawkish, according to strategists at Bank of America Corp

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mixed with Chinese stocks rallying on unverified reopening rumours, although the rest of the region was contained after the wave of central bank rate hikes and ahead of the NFP jobs data. ASX 200 was kept afloat by strength in the commodity-related sectors although gains were limited by weakness in defensives and the top-weighted financial sector, while the RBA’s quarterly Statement on Monetary Policy provided little in the way of fresh insight and included a downgrade to growth projections. Nikkei 225 was hit on return from holiday and reacted to the recent FOMC and Powell’s hawkish remarks. Hang Seng and Shanghai Comp rallied with the Hong Kong benchmark spearheaded by tech and with EV makers boosted following a jump in BYD’s new energy vehicle sales, while sentiment was also boosted as US audit inspectors finished on-site China work ahead of schedule and amid unverified rumours of China reopening.

Top Asian News

- US audit inspectors finished on-site China work ahead of schedule, according to Bloomberg.

- Chinese President Xi met with German Chancellor Scholz and said as big nations with influence, China and Germany should work together all the more in times of change and turmoil to make a greater contribution to world peace and development, according to state media.

- German Chancellor Scholz said his meeting with Chinese President Xi is at a time of big tension and that the Russian war on Ukraine brings big problems for rule-based order, while they will talk about Europe-China relations and the fight against climate change and world hunger. Scholz added they will also talk about how to develop economic relations and on topics where their perspectives are different.

- Japan’s government is said to issue JPY 22.8tln in bonds for the extra budget with total issuance for FY22/23 revised upward to a record JPY 62.5tln, according to Reuters.

- RBA Statement on Monetary Policy said the board expects rates will need to increase further and policy is not on a pre-set path, while they will hike in larger steps or pause if considered necessary. Furthermore, the RBA cut economic growth forecasts in which it sees GDP at 2.9% in December 2022, 1.4% in December 2023 and 1.6% in December 2024, while it lifted the inflation forecast which it sees at 8.0% in December 2022, 4.7% in December 2023 and 3.2% in December 2024.

- China is working on a plan to scrap COVID flight suspensions, according to Bloomberg.

- China’s Health Authorities are to hold a presser on targeted COVID prevention on November 5th at 15:00 local time (07:00GMT/03:00ET).

European bourses are firmer across the board as the complex benefits from further rumours around an easing of China’s COVID policy, with a presser on prevention due on the weekend; Euro Stoxx 50 +1.4%. Additional upside occurred in wake of upward revisions to the regions PMI metrics; however, the magnitude of this was limited as internal commentary remained downbeat and the metrics are still in contractionary territory. Stateside, futures are firmer across the board with magnitudes a touch more contained vs Europe, ES +0.7%, as the region awaits the NFP print.

Top European News

- Rolex Lifts Prices Again in Europe as US Dollar Stays Strong

- German Factory Orders Accelerate Drop as Recession Looms

- EU’s Breton Urges Carmakers to Keep Producing Combustion Engines

- Paschi Completes Full Rights Offer Subscription, Shares Fall

- GN Store Nord Shares Soar as Demant Invest Raises Holding

- Naspers Surges in Johannesburg on China Reopening Hopes

FX

- DXY has pulled back from overnight peaks, where it tested but failed to attain 113.00; a pullback in the context of constructive overall sentiment amid China-COVID rumours/reports and upward PMI revisions.

- Antipodeans outperform given base metal action on the mentioned COVID rumours, a narrative which has also buoyed the Yuan which itself was subject to a firmer-than-expected Yuan midpoint.

- EUR/USD has been unable to reclaim 0.98 despite favorable PMI revisions and the USD’s pullback; note, substantial OpEx lies between 0.9790-0.9800.

- Cable was unreactive to the BoE’s Chief Economist reiterating lines from Bailey in pushing-back on market pricing; nonetheless, the Pound has eclipsed 1.12 and is among the outperformers following Thursday’s underperformance.

Fixed Income

- Core benchmarks are little changed overall with USTs essentially flat on the session and yields holding within recent parameters as we count down to the NFP print.

- Bund has trimmed initial 50 tick upside following remarks from ECB’s Lagarde which incl. hawkish undertones on the wage front, German benchmark now little changed overall.

- In contrast, Gilts continue to slip and are lower by 50 ticks around 101.50 post-Pill highlighting that recent turmoil has not distracted them from their QT goals.

Commodities

- Commodities are bolstered amid the USD’s pullback and on further reopening rumours re. China

- WTI and Brent front-month futures are firmer on the day with the former just under USD 91/bbl and the latter around USD 97.00/bbl.

- Saudi Arabia set December Arab light crude OSP to Asia at Oman/Dubai + USD 5.45/bbl, while it set OSP to NW Europe at ICE Brent + USD 1.70/bbl and to the US at ASCI + USD 6.35/bbl.

- MMG said it has been forced to commence a progressive slow-down of its Las Bambas operation amid disruptions due to blockades by communities, while it continues to work with the government of Peru and communities along the site’s logistic route.

- US and allies have reached agreement on which sales of Russian oil will be subject to a price cap, WSJ reports; “Each load of seaborne Russian oil will only be subject to the price cap when it is first sold to a buyer on land, meaning resales of the same oil won’t have to fall under the cap”, according to WSJ sources.

- Spot gold has struggled to surpass the USD 1650/oz mark where its 21-DMA lies just above at USD 1651.7/oz, while base metals are deriving broad support on the China/COVID narrative

Geopolitics

- US officials have no clear timing for when North Korea might conduct a nuclear test and would like to see China and Russia use their leverage on North Korea to head off a nuclear test. Furthermore, the US is prepared to engage directly with North Korea and has sought to communicate with North Korea in private channels and through third parties, while it rejects the notion that the international community should treat North Korea as a nuclear power, according to a senior US administration official.

- At least 180 North Korean warplanes take off in apparent show of force, via Yonhap; subsequently, South Korean has scrambled around 800 jets.

- Taiwan Defence Ministry says 12 Chinese air force planes crossed the Taiwanese Strait Median Line on Friday, via Reuters.

US Event Calendar

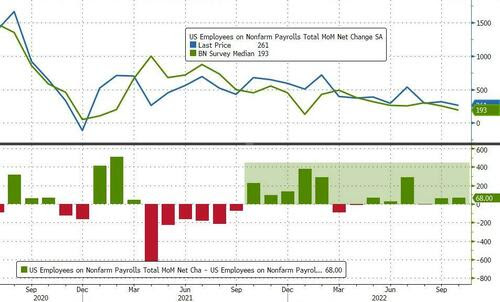

- 08:30: Oct. Change in Private Payrolls, est. 200,000, prior 288,000

- 08:30: Oct. Change in Nonfarm Payrolls, est. 195,000, prior 263,000

- 08:30: Oct. Change in Manufact. Payrolls, est. 12,000, prior 22,000

- 08:30: Oct. Unemployment Rate, est. 3.6%, prior 3.5%

- 08:30: Oct. Underemployment Rate, prior 6.7%

- 08:30: Oct. Labor Force Participation Rate, est. 62.3%, prior 62.3%

- 08:30: Oct. Average Hourly Earnings MoM, est. 0.3%, prior 0.3%

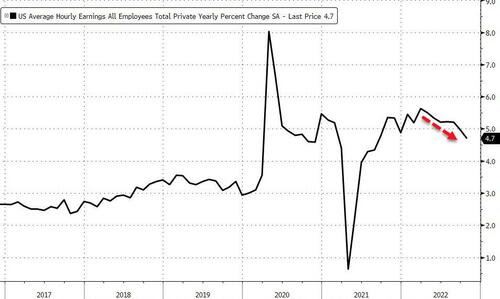

- 08:30: Oct. Average Hourly Earnings YoY, est. 4.7%, prior 5.0%

- 08:30: Oct. Average Weekly Hours All Emplo, est. 34.5, prior 34.5

DB’s Jim Reid concludes the overnight wrap

It’s been another rough 24 hours in markets, with risk assets continuing to struggle after Fed Chair Powell’s Wednesday statement that “the ultimate level of interest rates will be higher than previously expected”. Indeed, fed funds futures are now pricing in their most hawkish expectations to date, with terminal rate expectations closing above 5.1% for the first time.

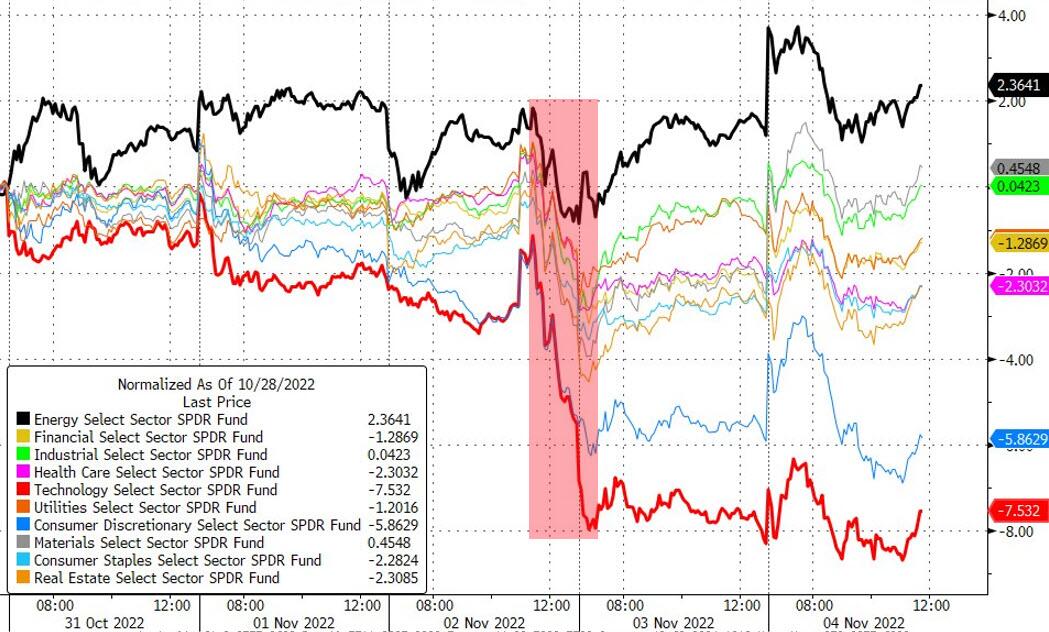

This fresh bout of hawkishness served to knock equities yet again, with the S&P 500 (-1.06%) building on the previous day’s losses to fall for a 4th consecutive session. That brings its losses for the week to -4.64%, and the effects have been particularly pronounced among the more interest-sensitive sectors like tech. For example the NASDAQ (-1.73%) is now on track for its second-worst weekly performance since March 2020, having lost -6.84% over the last four days. Furthermore, the FANG+ index of megacap tech stocks fell a further -1.53% yesterday, meaning that it’s now down by over -48% since its peak exactly a year ago today.

If that wasn’t bad enough, a number of recessionary indicators were flashing with increasing alarm yesterday, and the 2s10s Treasury yield curve flattened by another -5.0bps to -57.3bps. That’s the most inverted that curve has been since 1982, and bear in mind that it’s inverted prior to every single one of the last 10 US recessions, so a concerning sign if you value the yield curve as a recession indicator. That push even deeper into inversion territory came as the 2yr yield rose by +9.4bps yesterday, hitting a fresh post-2007 high of 4.71%. In the interests of balance however, we should point out that the Fed’s preferred yield curve (the 18m forward 3m yield minus the spot 3m yield) did steepen +11.9bps yesterday to 46.0bps, moving it yet further away from its near-inversion last week, when it closed at a new low for this cycle of 3.2bps.

When it comes to expectations of future rate hikes, the big event today will be the US jobs report for October, which will feed into the debate as to whether the Fed might slow down their pace of hikes at the December meeting. In terms of what to expect, our US economists are forecasting that nonfarm payrolls will have risen by +225k, which they think should be enough to keep the unemployment rate steady at 3.5%. Nevertheless, there’s still next month’s jobs report as well as a further two CPI prints ahead of the next Fed meeting, so there’s plenty to digest before they have to make that decision.

Here in the UK, the focus was also on central banks yesterday after the BoE delivered a 75bps rate hike as expected, thus taking Bank Rate to a post-2008 high of 3%. But even though it was the biggest single hike in decades, several details leaned in a dovish direction. First, although a majority of the MPC said that further hikes might be required if the economy progressed in line with their forecasts, they also said it would be “to a peak lower than priced into financial markets.” That was evident from their forecasts too, since their inflation projection which was conditioned on market interest rate expectations showed inflation falling below the 2% target in a couple of years. Separately, two of the nine MPC members were also in favour of a smaller hike, with one wanting a 50bps move and another preferring a 25bps move.

Those dovish implications meant that sterling fell significantly in response, and in fact was the worst-performing G10 currency with a -2.04% decline against the dollar. That said, sterling’s weakness did support the FTSE 100 (+0.62%), which was the only major equity index to close in positive territory yesterday. In his recap (link here), our UK economist sticks to his view that Bank Rate will peak at 4.5%, but sees more downside risks to the call as a result of the more dovish message from yesterday. In the meantime, the focus on the UK economy will now shift to the fiscal side, as the government’s fiscal statement is set to be delivered on November 17.

When it came to gilts, the 10yr yield was up +11.1bps on the day, but that was basically in line with other European countries, with yields on 10yr bunds (+10.9bps), OATs (+10.0bps) and BTPs (+12.2bps) seeing similar increases. That followed remarks from an array of ECB officials, including President Lagarde who said that there was “still a way to go” when it came to raising rates. As with the Fed, market expectations of future ECB interest rates have ticked up again over recent days, but unlike the Fed they remain beneath their recent highs over the last month or so.

Overnight in Asia we’ve seen a massive surge in Hong Kong and mainland Chinese stocks, driven by continued speculation about a potential shift in their zero-Covid strategy. That’s helped the Hang Seng to gain a massive +7.46% on the day, whilst the CSI 300 (+3.53%) and the Shanghai Comp (+2.76%) have also seen sizeable gains. And unlike the US, tech stocks are surging even faster, with the Hang Seng Tech index up by +10.87%. Elsewhere in Asia we haven’t seen a surge on that scale, with the Kospi up by a more modest +0.61%, and the Nikkei (-1.81%) experiencing a decent loss as it reopens following the holiday during the previous session. Looking forward however, equity futures in the US and Europe are pointing higher this morning, with those on the S&P 500 up +0.25%.

Overnight we’ve also heard from the Reserve Bank of Australia, who released their quarterly Statement on Monetary Policy and upgraded their forecasts for inflation, which they now see peaking at 8% this year. Meanwhile on the data front, Japan’s composite and services PMI both hit a 4-month high in October, climbing to 51.8 and 53.2 respectively.

Looking at yesterday’s other data, the US weekly initial jobless claimed fell to 217k (vs. 220k expected) over the week ending October 29, and the 4-week moving average also ticked lower for the first time in 5 weeks. However, the ISM services came in somewhat beneath expectations, and the 54.4 reading (vs. 55.3 expected) was the worst month since May 2020 during the pandemic contraction, and the employment component also moved back into contractionary territory with a 49.1 reading. Finally, the Euro Area unemployment rate fell to 6.6% in September, which is the lowest since the formation of the single currency, since the August number was revised up a tenth to show a 6.7% reading.

To the day ahead now, and the main highlight will be the US jobs report for October. Meanwhile in Europe, there’s data on German factory orders, French industrial production and Euro Area PPI for September, alongside the final services and composite PMIs for October. Central bank speakers include ECB President Lagarde, Vice President de Guindos, Bundesbank President Nagel, the Fed’s Collins and BoE Chief Economist Pill.

end

AND NOW NEWSQUAWK (EUROPE/REPORT)

Sentiment firmer pre-NFP amid further rumours regarding China’s COVID policy – Newsquawk US Market Open

FRIDAY, NOV 04, 2022 – 06:49 AM

- European bourses are firmer across the board as the complex benefits from further rumours around an easing of China’s COVID policy, Euro Stoxx 50 +1.4%

- Stateside, futures are firmer across the board with magnitudes a touch more contained vs Europe pre-NFP

- DXY has pulled back from overnight peaks, where it tested but failed to attain 113.00, Antipodeans & Yuan outperform

- Core fixed benchmarks are little changed overall with USTs essentially flat while Gilts lag post-Pill

- Commodities are bolstered amid the USD’s pullback and on further reopening rumours re. China

- Looking ahead, highlights include US & Canadian Labour Market Reports, Speech from Fed’s Collins.

- Click here for the Week Ahead preview.

View the full premarket movers and news report.

Or why not try Newsquawk’s squawk box free for 7 days?

EUROPEAN TRADE

EQUITIES

- European bourses are firmer across the board as the complex benefits from further rumours around an easing of China’s COVID policy, with a presser on prevention due on the weekend; Euro Stoxx 50 +1.4%.

- Additional upside occurred in wake of upward revisions to the regions PMI metrics; however, the magnitude of this was limited as internal commentary remained downbeat and the metrics are still in contractionary territory.

- Stateside, futures are firmer across the board with magnitudes a touch more contained vs Europe, ES +0.7%, as the region awaits the NFP print.

- Click here for more detail.

FX

- DXY has pulled back from overnight peaks, where it tested but failed to attain 113.00; a pullback in the context of constructive overall sentiment amid China-COVID rumours/reports and upward PMI revisions.

- Antipodeans outperform given base metal action on the mentioned COVID rumours, a narrative which has also buoyed the Yuan which itself was subject to a firmer-than-expected Yuan midpoint.

- EUR/USD has been unable to reclaim 0.98 despite favorable PMI revisions and the USD’s pullback; note, substantial OpEx lies between 0.9790-0.9800.

- Cable was unreactive to the BoE’s Chief Economist reiterating lines from Bailey in pushing-back on market pricing; nonetheless, the Pound has eclipsed 1.12 and is among the outperformers following Thursday’s underperformance.

- Click here for more detail.

Notable FX Expiries, NY Cut:

- EUR/USD: 0.9650 (260M), 0.9750 (615M), 0.9790-00 (1.62BLN), 0.9825-35 (902M), 0.9870 (254M), 0.9900 (1.28BLN), 0.9925-30 (348M), 0.9950-55 (487M), 1.0000 (2.48BLN) USD/JPY: 146.00 (607M), 147.00 (1.05BLN), 148.00 (680M), 149.00 (583M), 150.00 (940M)

- Click here for more detail.

FIXED INCOME

- Core benchmarks are little changed overall with USTs essentially flat on the session and yields holding within recent parameters as we count down to the NFP print.

- Bund has trimmed initial 50 tick upside following remarks from ECB’s Lagarde which incl. hawkish undertones on the wage front, German benchmark now little changed overall.

- In contrast, Gilts continue to slip and are lower by 50 ticks around 101.50 post-Pill highlighting that recent turmoil has not distracted them from their QT goals.

- Click here for more detail.

COMMODITIES

- Commodities are bolstered amid the USD’s pullback and on further reopening rumours re. China

- WTI and Brent front-month futures are firmer on the day with the former just under USD 91/bbl and the latter around USD 97.00/bbl.

- Saudi Arabia set December Arab light crude OSP to Asia at Oman/Dubai + USD 5.45/bbl, while it set OSP to NW Europe at ICE Brent + USD 1.70/bbl and to the US at ASCI + USD 6.35/bbl.

- MMG said it has been forced to commence a progressive slow-down of its Las Bambas operation amid disruptions due to blockades by communities, while it continues to work with the government of Peru and communities along the site’s logistic route.

- US and allies have reached agreement on which sales of Russian oil will be subject to a price cap, WSJ reports; “Each load of seaborne Russian oil will only be subject to the price cap when it is first sold to a buyer on land, meaning resales of the same oil won’t have to fall under the cap”, according to WSJ sources.

- Spot gold has struggled to surpass the USD 1650/oz mark where its 21-DMA lies just above at USD 1651.7/oz, while base metals are deriving broad support on the China/COVID narrative

- Click here for more detail.

NOTABLE EUROPEAN HEADLINES

- BoE’s Pill says we still think there is more to do on inflation pressures, via CNBC; not for BoE to tell market how to price assets. Thinks lag in transition of monetary policy to activity is about a year. We need to raise bank rate and shrink QT portfolio, recent disturbances have not distracted us from key goal.

- ECB President Lagarde says we must not let high inflation become entrenched, rate path ahead will look different depending on the contingencies ECB faces. We are likely to see wages ‘catching up’ to some extent with higher inflation.

- BoE’s Hauser (non-MPC) says we must execute a timely and orderly unwind of the assests accumulated as part of financial stability purchase operations. Need to remain sensitive to and if necessary respond appropriately to still-febrile market conditions.

- UK Chancellor Hunt is mulling an increase in the headline rate of Capital Gains Tax, according to The Telegraph.

NOTABLE EUROPEAN DATA