NOV 7/GOLD ROSE BY $2.95 TO $1677.75//SILVER WAS UP $.12 TO $20.74//PLATINUM WAS UP A STRONG $24.15 TO $981.50//PALLADIUM WAS UP $48.65 TO $1901.55//COVID UPDATES//VACCINE IMPACT//DR PAUL ALEXANDER//UKRAINIANS HIT THE KHERSON DAM WITH ONE MISSILE WITH SO AMOUNTS OF DAMAGE SO FAR//FRANCE’S BIGGEST GLASS MANUFACTURER DURALEX SHUTTING DOWN FOR 6 MONTHS BECAUSE OF HIGH ENERGY COSTS//FRANCE ALSO REPORTS LOWER NUCLEAR OUTPUT AND WARNS OF A HARSHER WINTER//ITALY REFUSES TO ALSO MIGRANTS TO ENTER ITS COUNTRY//PEPE ESCOBAR: A MUST READ!!//USA GREENLIGHTS ROCKETS TO FINLAND AND THAT WILL THOROUGHLY UPSET RUSSIA//COMCAST ANNOUNCES IT WILL BEGIN TO LAYOFF EMPLOYEES//SWAMP STORIES FOR YOU TONIGHT//

132 C SG AMERICAS 7 190 H BMO CAPITAL 24 323 C HSBC 15 661 C JP MORGAN 280 83 732 C RBC CAP MARKETS 1 737 C ADVANTAGE 20 20 800 C MAREX SPEC 5 3 880 C CITIGROUP 15 880 H CITIGROUP 136 905 C ADM 1

TOTAL: 305 305

JPMORGAN STOPPED 83/305

GOLD: NUMBER OF NOTICES FILED FOR NOV. CONTRACT: 305 NOTICES FOR 30,500 OZ or 0.9486 TONNES

total notices so far: 4858 contracts for 485,800 oz (15.110 tonnes)

SILVER NOTICES: 7 NOTICE(S) FILED FOR 35,000 OZ/

total number of notices filed so far this month 161 : for 805,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $2.95

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////A BIG CHANGE IN GLD INVENTORY: A WITHDRAWAL OF 1.63 TONNES FROM THE GLD// /INVENTORY LOWERS TO 920.57 TONNES

INVENTORY RESTS AT 909.96 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $0.12

AT THE SLV// :/NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF OF 00.00 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 477.678 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A FAIR SIZED 558 CONTRACTS TO 138,558 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE FAIR LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OU HUGER $1.31 GAIN IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR SHORTERS/HFT WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $1.31)., AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS, AS WE HAD A HUGE GAIN IN OUR TWO EXCHANGES OF 5948 CONTRACTS. WE HAD A CONSIDERABLE ATTEMPT AT SPEC SHORT COVERING THEIR SHORTFALLS BUT TO LITTLE AVAIL.WE HAD NO SPEC SHORT ADDITIONS AS THE PRICE ESCALATED AWAY FROM THEM CAUSING LOTS OF LOSSES. // OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. SOME NEWBIE SPEC LONGS ADDED TO THEIR POSITIONS CAUSING MISERY TO OUR SHORTERS.

WE MUST HAVE HAD: I) CONSIDERABLE ATTEMPTED SPECULATOR SHORT COVERINGS WITH NO SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /// SOME NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A MAMMOTH ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.045 MILLION OZ FOLLOWED BY TODAY’S 80,000 QUEUE JUMP//NEW STANDING:1.485 MILLION OZ/ / // V) FAIR SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -171

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF NOV:

TOTAL CONTRACTS for 5 days, total 9820 contracts: 49.100 million oz OR 9.820MILLION OZ PER DAY. (1964 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 49.100 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 49.100 MILLION

RESULT: WE HAD A FAIR SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 558 DESPITE OUR HUGE $1.31 GAIN IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A MAMMOTH SIZED EFP ISSUANCE CONTRACTS: 6,335 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR NOV. OF 1.345 MILLION OZ FOLLOWED BY TODAY’S 80,000 QUEUE JUMP/ .. WE HAVE AN ATMOSPHERIC SIZED GAIN OF 5948 OI CONTRACTS ON THE TWO EXCHANGES FOR 5.075 MILLION OZ.. THE SILVER SHORTS ARE NOW TRAPPED AS THEY ARE HAVING CONSIDERABLE DIFFICULTY IN COVERING THOSE SHORTS ESPECIALLY WITH THE HUGE GAIN IN PRICE ON FRIDAY.

WE HAD 7 NOTICE(S) FILED TODAY FOR 35,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 8687 CONTRACTS TO 474,056 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -710 CONTRACTS.

.

THE STRONG SIZED DECREASE IN COMEX OI CAME DESPITE OUR HUGE RISE IN PRICE OF $44.45//COMEX GOLD TRADING/FRIDAY // CONSIDERABLE ATTEMPTED SPECULATOR SHORT COVERINGS//ZERO SPEC SHORT ADDITIONS, ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION WITH CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS. WE WITNESSED DAY ONE OF THIS AS EVERYBODY WISHES TO BUY BUT NO SELLERS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR NOV. AT 12.386 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S GOOD 3200 OZ QUEUE JUMP //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR HUGE RISE IN PRICE OF $44.45 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A SMALL SIZED LOSS OF 3,337 OI CONTRACTS (10.38 PAPER TONNES) ON OUR TWO EXCHANGES..WITH THAT LOSS DUE TO SPECULATORS TRYING TO EXTRICATE THEMSELVES FROM THEIR MESS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5350 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 474,766

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2627 CONTRACTS WITH 7977 CONTRACTS DECREASED AT THE COMEX (SHORT SPECULATORS GETTING OUT OF THEIR MESS) AND 5,350 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 2627 CONTRACTS OR 8.171 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5,350) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (8687): TOTAL LOSS IN THE TWO EXCHANGES 3337 CONTRACTS. WE NO DOUBT HAD 1) CONSIDERABLE ATTEMPTED SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS AS WELL AS ZERO SHORT SPEC ADDITIONS/// // CONSIDERABLE NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR NOV. AT 12.386 TONNES FOLLOWED BY TODAY’S GOOD QUEUE JUMP OF 3200 OZ //NEW STANDING 20.186 TONNES///3) ZERO LONG LIQUIDATION //// //.,4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

NOV

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV. :

24,693 CONTRACTS OR 2,469,300 OZ OR 76.80 TONNES 5 TRADING DAY(S) AND THUS AVERAGING: 4939 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY(S) IN TONNES: 76.80 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 76.80/3550 x 100% TONNES 2.16% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 76.80 TONNES//INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A FAIR SIZED 558 CONTRACT OI TO 138,558 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 6335 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 6335 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 6355 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 558 CONTRACTS AND ADD TO THE 6335 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF 5777 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 28.885MILLION OZ//

OCCURRED WITH OUR RISE IN PRICE OF $1.31. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED UP 7.02 PTS OR 0.23% //Hang Seng CLOSED UP 434.77 OR 2.69% /The Nikkei closed UP 327.90 OR 1.21% //Australia’s all ordinaires CLOSED UP 0.56% /Chinese yuan (ONSHORE) closed UP TO 7.2282 //OFFSHORE CHINESE YUAN UP 7.2319// /Oil UP TO 92.13 dollars per barrel for WTI and BRENT AT 98.23 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 8,687 CONTRACTS TO 474,766 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED DESPITE OUR HUGE GAIN IN PRICE OF $44.45 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (5350 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED HUGE NUMBER OF SPECS TO GO MASSIVELY SHORT AND NO DOUBT ON FRIDAY THEY HAD CONSIDERABLE TROUBLE TRYING TO COVER. WE HAD MANY BUYERS OF CONTRACTS BUT FEW WILLING TO SELL.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON -ACTIVE DELIVERY MONTH OF NOV.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5,350EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 5,350 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5,350 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: AN FAIR SIZED TOTAL OF 3337 CONTRACTS IN THAT 5,350LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 8.687 CONTRACTS..AND THIS FAIR SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR HUGE RISE IN PRICE OF GOLD $44.45//WE FINALLY HAD HUGE SPEC SHORTS TRYING TO COVER THEIR SHORTFALL WITH LIMITED SUCCESS. BANKERS CONTINUE AS BUYERS OF COMEX GOLD CONTRACTS AS THEY HAVE BEEN NET LONG FOR THE PAST FEW MONTHS. WE ALSO HAD STRONG ADDITIONAL NEWBIE SPECS GOING LONG WITH ZERO SPEC SHORT ADDITIONS TO THEIR SHORT SIDE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING NOV (20.186),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 20.186 TONNES/INITIAL (TOTAL SO FAR THIS YEAR 564.435 TONNES)

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $44.45) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS. HOWEVER WE DID HAVE CONSIDERABLE SPECULATOR SHORTS COVERING THEIR SHORTFALL. WE HAD A FAIR SIZED LOSS ON OUR TWO EXCHANGES OF 3337 CONTRACTS.// WE HAVE LOST A TOTAL OI OF 8.171 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR NOV. (20.186 TONNES)…THIS WAS ACCOMPLISHED DESPITE OUR RISE IN PRICE OF $44.55

WE HAD -710 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 3337 CONTRACTS OR 333,700 OZ OR 10.38 TONNES

Estimated gold volume 223,424// fair to good//

final gold volumes/yesterday 318,063/ good

INITIAL STANDINGS FOR NOVEMBER 2022 COMEX GOLD //NOV 7

Total monthly oz gold served (contracts) so far this month

4858 notices 485,800 15.110TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals:2

ii) Out of Brinks 30,958.750

ii) Out of JPMorgan: 2158,530.275

total: 249,489.025 oz

total in tonnes: 7.760 tonnes

Adjustments: 1// dealer to customer

i) Out of Int. Delaware 12,056.625 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR NOVEMBER.

For the front month of NOV. we have an oi of 1937 contracts having LOST ONLY 654 contracts. We had 686 notices served on FRIDAY so we gained a strong 32

or an additional 3200 OZ (0.09 TONNES) will stand in this non active month of November. We will have Nov gold tonnage standing increase daily from this day forth until the end of the month.

This queue jumping originates in London with the exercising of London based EFP’s for comex gold.

December LOST 13,549 contracts DOWN to 334,619. DEC WILL BE A DILLY OF A DELIVERY MONTH.

JANUARY GAINED 89 contract to stand at 126.

February gained 4,204 contacts up to 98,627.

We had 305 notice(s) filed today for 30,500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 280 notices were issued from their client or customer account. The total of all issuance by all participants equate to 305 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 83 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the NOV. /2022. contract month,

we take the total number of notices filed so far for the month (4858) x 100 oz , to which we add the difference between the open interest for the front month of (NOV 1937 CONTRACTS) minus the number of notices served upon today 305 x 100 oz per contract equals 649,000 OZ OR 20.186 TONNES the number of TONNES standing in this non active month of NOV.

thus the INITIAL standings for gold for the NOV. contract month:

No of notices filed so far (4858) x 100 oz+ (1937) OI for the front month minus the number of notices served upon today (305} x 100 oz} which equals 649,000 oz standing OR 20.186 TONNES in this NON active delivery month of NOV..

TOTAL COMEX GOLD STANDING: 20.186 TONNES (A HUMONGOUS STANDING//NEW RECORD FOR NOV (GENERALLY THE POOREST DELIVERY MONTHS FOR A NON ACTIVE MONTH)

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 161 x 5,000 oz = 804,000 oz

to which we add the difference between the open interest for the front month of NOV(123) and the number of notices served upon today 7 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the NOV../2022 contract month: 161 (notices served so far) x 5000 oz + OI for front month of NOV (123) – number of notices served upon today (7) x 5000 oz of silver standing for the NOV. contract month equates 1,485,000 oz.

We will gain in silver oz standing from this day forth until the end of the month.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:104,869// est. volume today// huge/shorts covered

NOV 7/WITH GOLD UP $2.95: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.63 TONNES FROM THE GLD//INVENTORY RESTS AT 906.96. TONNES

NOV 4/WITH GOLD UP $44.45 TO $1673.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.48 TONNES FROMTHE GLD////INVENTORY RESTS AT 911.59 TONNES.

NOV 3/WITH GOLD DOWN $18.30 TO $1628.85: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.05 TONNES FROM THE GLD////INVENTORY RESTS AT 915.07 TONNES

NOV 2/WITH GOLD UP 55 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 919.12 TONNES.

NOV 1/WITH GOLD UP $9.20 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES FORM THE GLD../INVENTORY RESTS AT 920.57 TONNES

OCT 31/WITH GOLD DOWN $4.00; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD//INVENTORY RESTS AT 922.59. TONNES//

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

GLD INVENTORY: 906,96TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

NOV 7/WITH SILVER UP 12 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 4/WITH SILVER UP $1.31 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.972 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 3.WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 566,000 OZ FROM THE SLV////INVENTORY RESTS AT 482.650 MILLION OZ//

NOV 2/WITH SILVER DOWN 9 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 92,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.216 MILLION OZ//

NOV 1/WITH SILVER UP 53 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 415,000 OZ FORM THE SLV////INVENTORY RESTS AT 483.308 MILLION OZ

OCT 31: WITH SILVER FLAT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .644 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 483.723 MILLION OZ//

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: A WITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

CLOSING INVENTORY 477.678 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Last week, the Federal Reserve delivered a 75-basis point rate hike, but Fed Chair Jerome Powell failed to deliver the more doveish rhetoric that many expected. The messaging did not indicate much softening in the stance on the future trajectory of rate hikes, despite an apparent “soft pivot” the week before.

In his podcast, Peter broke down Powell’s messaging and pointed out a number of very scary admissions that came out of the Fed meeting.

Peter said the Fed did do a soft pivot but was able to back off when the bond market stabilized.

I believe the Fed was forced into making that pivot because it stood on the precipice of a bond market crash, which was in the process of happening. And I think the only way the Fed was able to stop that slow-motion crash from playing out accelerating was by throwing a bone to the markets and indicating through the Wall Street Journal that there was going to be some type of statement that was going to go along with the rate hike that would indicate that maybe there was going to be a pause in the pace, a slowdown in the pace, that the Fed was going to take a step back and reflect and assess, and maybe acknowledge the progress that had been made without indicating complete victory, but at least acknowledging that victory was at least in sight and that the Fed could take a more cautious approach going forward. … Something to that effect was expected.”

However, the Fed didn’t deliver anything close to that.

Initially, the markets thought the Fed was going more doveish. The statement released by the FOMC left some wiggle room for a slowdown in hiking or even a pause with language about monetary policy “lags” and “cumulative” effects.

In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

By acknowledging the lag between rate hikes and inflation, the Fed gave itself the leeway to pause.

Initially, the stock market rallied. But during his prepared marks, Fed Chairman Jerome Powell spooked the markets, saying that price stability is essential and the historical record strongly cautions against prematurely loosening policy. Powell emphasized that the central bank was committed to “staying the course” until the job is done.

As he moved through the Q&A, Powell dropped a number of what Peter called “unexpected bombshells” that the markets were not expecting.

First, he reiterated the Fed’s commitment to positive real interest rates. Right now, the Fed interest rate sits at 4%, but CPI remains over 8%. Powell implied that we will get to positive real rates as CPI falls. But what if CPI doesn’t fall? That would mean interest rates have to go much higher than the markets anticipate.

I think the fact that Powell had to acknowledge that ultimately we have to have a positive real interest rate — that is very scary for the markets.”

Powell also admitted they don’t know what the actual underlying inflation rate is.

Now, that is a very scary admission by the Fed. Because if the Fed is committed to fighting inflation, but it doesn’t even know how big the monster that it has to slay is, then how does it know how many rate hikes are going to be necessary? How does he know how high rates have to be in order for there to be a positive real rate of interest if he doesn’t even understand what the underlying rate of inflation is? And if he doesn’t understand it now, why will he understand it at some point in the future? The Fed has no clue. All it’s looking at is the same headline number as everybody else. And based on that, the Fed is still way behind the inflation curve and has a long way to go. And that, again, should scare anybody who is counting on the Fed to ease up on its current trajectory of tightening.”

When asked if inflation has become entrenched, Powell didn’t say no. In fact, Powell said the Fed has no way of knowing when inflation becomes entrenched.

That’s another scary admission by the Fed. Because if it doesn’t know, it’s just kind of flying blind, and it has to err on the side of caution to make sure inflation doesn’t become entrenched.”

Of course, as Peter pointed out, inflation is entrenched. It’s not a matter of psychology. It is a matter of monetary policy.

The Fed has created so much inflation for so long — it didn’t even start with COVID. It didn’t even really start with QE. The Fed was creating inflation even before it upped the ante to quantitative easing and then upped it again in the aftermath of COVID.”

Powell also admitted that inflation was a lot higher and has lasted a lot longer than anybody at the Fed had expected.

This is tantamount to saying, ‘We got this wrong. We made a mistake. And now we need to correct that mistake by staying tighter for longer or going higher than markets expect.’”

Powell said the real risk was in doing too little tightening, not doing too much. He said he would prefer to overtighten. Powell said if the central bank tightens too much, it has the tools to support economic activity if necessary. In other words, it can always go back to monetary stimulus.

Again, those are very scary comments, especially if you were expecting the Fed to adopt a softer tone.”

But it also reveals the fatal flaw in the Fed’s thinking.

Powell is wrong to think that if they just tighten too much, meaning they tighten so much that the economy really weakens into a severe recession, that the Fed has the tools to prop it back up and stimulate it to support economic activity. It doesn’t. Because if the fight against inflation drives the economy into recession, if the Fed then uses those very tools to support the economy, well then, inflation is going to take off and get much worse. You see, if the Fed is really committed to fighting inflation, then those tools are no longer at its disposal. The fact that Powell is so quick to admit that he’s going to use those tools if the inflation fight does too much damage to the economy really reveals that the Fed is not as committed to fighting inflation as it maintains, or as the markets believe. Because, as I’ve said many times, the Fed’s commitment to fighting inflation stops if it brings about a severe recession or a financial crisis.”

The Fed is willing to tolerate a “hard landing” and a mild, short recession. But if it gets worse than that, it will use its tools. Peter said he thinks it will use those tools long before inflation gets near 2%.

But even in the extremely unlikely situation where the Fed got inflation back down to 2% because of its tightening and then, with inflation at 2%, the Fed then used those tools to stimulate the economy, anything it had achieved in reducing inflation will be lost and the inflation rate will spike back up again. So, even if inflation does go to 2%, the Fed still can’t use those tools.”

Peter said when the economy really starts to fall apart, the Fed will make a hard pivot. He also said despite Powell’s rhetoric, he believes the Fed did recently do a soft pivot to rescue the bond market.

It’s just that Powell didn’t follow through in the Q&A. I think that pivot was, in fact, written into the prepared remarks, but Powell went off script and went back to his newfound hawkishness.”

The rally in the bond market after the soft pivot made that possible.

But now that Powell has returned to his hawkish rhetoric, the market crash that the Fed interrupted is going to resume. And I think when faced with those circumstances again, especially if it’s the bond market and not just the stock market, I think Powell is going to have to come back and clarify his remarks. And by clarify, I mean do a complete 180

END

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards: A Bodyguard Of Lies

The all-important midterm elections are just one week away. I’ve said a lot about them, and will have more to say about them in the days to come.

But today, I want to talk about something even more important: truth vs. official lies. More specifically, I want to talk about truth and propaganda.

It’s said that truth is the first casualty of war. And Churchill once said that in wartime, truth is so precious that it needs to be surrounded by a bodyguard of lies.

That’s why propaganda plays such a large role in modern warfare.

The fact is wars are conducted in part through lies and propaganda. For example, in the early days of World War I, the British cut the undersea communications cables that ran from Germany to the U.S.

The British wanted to control the flow of information and issue what we call today “misinformation.” And so they created inflammatory accounts of German atrocities to sway public opinion, like German soldiers skewering Belgian babies on bayonets.

While there will always be individual acts of atrocity in wartime, these reports were largely propaganda.

Here in the U.S. itself, President Wilson had special police forces who arrested anyone reporting negative news on the progress of the war. Sound familiar?

It’s like the social media companies today canceling or censoring anyone who reports that the vaccines don’t work or masks don’t work. The media call it “misinformation” (even though it’s scientifically valid) and move on.

The same is true with the war in Ukraine. The propaganda machine kicked into overdrive early on.

Bodyguard of Lies

The CIA and MI6 leaked a steady stream of anti-Russian lies to prop up morale. These lies were reprinted in warmonger media outlets like The Washington Post, The New York Times and NBC News.

That means it’s almost impossible for U.S. citizens to get the real story through mainstream media outlets. Still, there is some honest reporting going in if you know where to find it.

You just have to filter the sources and find those with good pipelines of information (including inside the government) who do not have a hidden agenda and are willing to speak the truth.

It’s not necessary to rely on Russian sources (the Russians are certainly not above propaganda, although they’re generally more truthful than the U.S. media, believe it or not). There are excellent analyses to be found among Swiss sources, German experts who are not in favor of the war and some on-the-ground reporting from the front lines on specialist websites.

Get Ready for the Russian Counteroffensive

Some of the best sources are found among retired U.S. military officers who are experts on warfare, still have good contacts inside the military and intelligence communities, and who consider the war in Ukraine to be highly detrimental to U.S. national security and the economy.

One top commentator who fits this description is Colonel (Ret.) Douglas Macgregor, who wrote a recent commentary about the war. Macgregor points out that Russia is preparing for a full-scale counterattack to roll-back recent Ukrainian gains near the Donbas and Kherson.

The Russians have been consolidating their positions: resupplying, mobilizing troops, and preparing for winter warfare at which they excel. It’s just a matter of waiting for the ground to freeze so trucks and armor can maneuver without getting bogged down.

The attack could come as early as November or December at the latest. Yet, that is not Macgregor’s main concern.

Is the 101st Airborne Division Being Used as Bait?

His fear is that the U.S. will double down in the face of this attack and deploy U.S. troops to the battle. The Pentagon recently deployed units of the 101st Airborne Division to Romania, just miles from its border with Ukraine.

Airborne forces are generally light infantry that lack the firepower of, say, armored units or mechanized infantry.

But if these forces did get directly involved in the fighting, heavier reinforcements would be on the way. From there, it could be a short step to nuclear war with Russia.

To some, that might sound unrealistic or even paranoid. They’ll say it’s just scare-mongering. But this is a legitimate possibility, and there’s a real chance of it happening. The fact is, we’ve been on the path of escalation with Russia since 2008 and the tempo of escalation has accelerated since the war began in February.

All experts on nuclear warfighting agree that if a nuclear war begins, it will be the result of escalation to the point that one side feels it is cornered and has no choice but to use nukes. That point is getting closer by the day.

Macgregor calls on Congress to stop the White House, but he’s not optimistic that’ll happen.

Nuclear War? It’s Not the End of the World

The possibility of nuclear war between the U.S. and Russia is a shocking development after thirty years, during which nuclear weapons and nuclear war between superpowers were almost forgotten.

What is as disconcerting is the fact that the discussion of nuclear war is casual, almost flippant, and carries none of the seriousness with which the topic was formerly addressed. It also carries no comprehension of the existential consequences and sheer horror that the use of nuclear weapons entails.

It’s almost as if the warmongers in and around the White House were playing a game of chicken without realizing the other driver had no intention of changing course.

Now the U.S. elites have started psychological operations (psyops) aimed at Putin with nuclear weapons as the bait. They claim that Putin has threatened to use tactical weapons in Ukraine and possibly other parts of Eastern and Central Europe.

That’s a lie; Putin never said that.

When asked, both Putin and Prime Minister Dmitri Medvedev said that if attacked, Russia would defend itself by all means necessary, including the possible use of nuclear weapons. That’s not news. That has been Russian or Soviet policy since the early 1950s. It has also been U.S. policy since then. Neither side has ever renounced the first use of nuclear weapons.

Putin’s expected answer to a question posed has been turned into a threat he never made. This is U.S. and UK propaganda at its worst (and most dangerous). This lie about Putin’s intentions quickly morphed into another psyop about a “false flag” operation.

That’s when you stage an attack disguised to look like an attack by your enemy in order to justify your own “retaliation,” which you were planning all along. Recently, the narrative that Putin would use nukes or conduct a false flag operation morphed into a related narrative that Putin would use a “dirty bomb.”

He Said, He Said

In effect, Putin would detonate a dirty bomb and then blame the Ukrainians and Americans. A dirty bomb is not a nuclear weapon, but it does employ radioactive material wrapped around conventional explosives. When detonated, the radioactive material is dispersed and can poison or kill any people or livestock in the area.

Not to be outdone, the Russians countered by saying the U.S. or Ukraine would conduct the false flag by detonating a dirty bomb and then blaming the Russians as an excuse to escalate Western involvement in Ukraine.

At this point, we have both sides warning the other side will conduct a false flag with a dirty bomb in order to justify their own pre-planned escalation. If a dirty bomb does go off, each side will blame the other and the truth will be a casualty of war.

Meanwhile, a senior Russian foreign ministry official has warned that U.S. satellites, which have been providing critical targeting information to Ukraine’s armed forces, may be “legitimate” targets of Russian forces.

How would the U.S. respond if Russia starts taking out its satellites? We may soon find out.

Is Your Portfolio Ready for Nukes?

By the way, I’m not apologizing for Putin or defending his invasion of Ukraine. I’m just looking at the current situation and objectively analyzing where things could go next, based upon the facts.

And I’m not making a specific prediction; I’m just giving you a warning because the media doesn’t seem to want to.

It might seem like an inappropriate question given the potential for widespread death and destruction, but is your portfolio ready for nukes?

In a nuclear confrontation, stocks and bonds could become worthless as exchanges are closed around the world. At best, they will retain some value as illiquid private equity tokens.

The best assets in this catastrophic scenario are land, gold, silver, food, water, and heat for your home.

Nothing else will matter much.

END

LAWRIE WILLIAMS: Week closes with gold and silver trending sharply higher

Precious metals volatility following last week’s FOMC meeting, and the announcement of yet another 75 basis point rise in the Federal Funds interest rate was nothing if not volatile in the extreme. The immediate reaction was for the gold price to surge to well above $1,670 an ounce and silver to around the $20 mark, only to see both precious metals fall back heavily, gold to around its lowest point in over 2 years, on Fed chair Powell’s rather more hawkish post-meeting follow-on presentation to the assembled media. In it he seemed to suggest that the Fed was not necessarily done with its aggressive approach to interest rate rises to combat inflation and bring it down to the target 2% level. It was better, he averred, to over-tighten, and subsequently reverse course, than to under-correct and for inflation potentially to become endemic.

But there were also signals that a reduction in the size of interest rate impositions might be under consideration too – a position seemingly supported by some other Fed officials in subsequent statements. This could even be as soon as at the December FOMC meeting. And this latter premise gave some possibly unwelcome encouragement to the equity markets late in the day Friday.

The Chicago Mercantile Exchange’s Fedwatch Tool is certainly also moving in this direction with the latest prediction now showing a 52% likelihood of a slightly reduced 50 basis point rate rise at the December meeting as opposed to 48% favouring a 75 basis point increase – a reversal of the position of only a day earlier. We suspect the next Consumer Price Index (CPI) data release due out on Thursday from the Bureau of Labor Statistics will thus set the scene for the next phase in precious metals and equity price movements. It will give the markets further ammunition for second guessing the Fed’s next likely interest rate move and affect the direction in which equity and precious metals prices may progress.

We suspect Thursday’s CPI data may well again be largely inconclusive, though, with regard to whether inflation has yet peaked. Inflation is likely still to remain higher than the Fed would like regardless, although whether it may come down sufficiently enough, if at all, to justify a reduction in the Fed’s aggressive rate increase programme remains to be seen. But even a reduction to a 50 basis point rate increase will leave year end rates at an eye-watering 4.25- 4.5%, and probably 4.75-5.0% by end Q1 next year, which will certainly be a dampener on corporate earnings in any case.

Thus the recent late recovery in equity prices on Friday, in a volatile day’s trading, is to our minds, unjustified. We suspect further falls are in the pipeline as GDP again drifts into negative territory quite probably before the end of the current year, and almost certainly in 2023, and a possibly extended period of recession begins to take hold.

We suspect the U.S. mid-term elections this week may well make life more difficult for the Biden administration and the U.S. dollar will suffer to the benefit of gold and silver. The UK and Europe are also heading for even deeper economic troubles than the U.S. which could counter the dollar’s comparative fall to an extent, though, but perhaps also help bring home the perceived benefits of safe haven investments. $1,700 gold or higher before the year’s end certainly no longer looks unlikely, and the way markets have been behaving recently a considerably higher level cannot be considered impossible. But markets have been, to say the least, unpredictable for most of the current year and with possible geopolitical or geo-economic shocks potentially continuing to build up, anything could happen.

John Williams of U.S. site Shadowstats fame reckons the Fed’s ongoing series of rate hikes, even if future ones are going to be at a slightly reduced level, are all designed to intensify an already ongoing and rapidly deepening, but not yet formally recognised, recession. Or perhaps even an unfolding depression, with purported expectations of killing extraordinary economic inflation pressures, which he considers are monetary by nature. With headline inflation driven by explosive money supply growth and various pandemic issues, not by the Fed’s “overheating” economy scapegoat, the U.S. economy already is in what should become recognised as a deepening recession, and that applies to much of the rest of the world too. Hold on tight for a bumpy ride ahead.

06 Nov 2022

3.Chris Powell of GATA provides to us very important physical commentaries

Agnico Eagle just could not let GoldFields have the remaining stub of Malartic.

(GATA)

Gold Fields target Yamana catches eyes of Agnico Eagle and Pan American

Submitted by admin on Fri, 2022-11-04 18:31Section: Daily Dispatches

By Helen Reid and Mrinalika Roy Reuters Friday, November 4, 2022

Agnico Eagle Mines Ltd.and Pan American Silver Corp swooped in Friday with a joint bid for Yamana Gold in an attempt to scupper Gold Fields’ planned acquisition of the Canada-listed gold miner.

The cash and stock offer, valuing Yamana at around $4.8 billion, would see Agnico and Pan American split Yamana’s mines between them. Yamana shareholders would receive $1.0406 in cash, 0.0376 of an Agnico Share, and 0.1598 of a Pan American Share for each share held.

South Africa’s Gold Fields had agreed to take over Yamana in an all-stock deal valuing it at $6.7 billion in May.

But a slump in its shares after the deal was announced dented the valuation and at Thursday’s close the all-stock offer valued Yamana at just north of $4 billion.

Yamana, whose shares were up 15% after news of the rival bid, said it had informed Gold Fields that the new offer was a “superior proposal.” Gold Fields has five business days to make a new offer should it wish to. …

It seems that the World Gold Council’s duty of reporting official gold holdings of nations has gone array

(Ronan Manly)

Ronan Manly: This week’s central bank gold data from World Gold Council was just made up

Submitted by admin on Fri, 2022-11-04 21:37Section: Daily Dispatches

9:39p ET Friday, November 4, 2022

Dear Friend of GATA and Gold:

Bullion Star gold market analyst Ronan Manly reveals tonight that most of the record gold buying by central banks that was reported this week by the World Gold Council cannot be documented or even reliably attributed. Rather, Manly finds, almost 78% of the central bank gold buying claimed by the gold council is just the estimate of a mysterious council consultant, unsupported by any official data.

Of course, Manly adds, financial news services, including Bloomberg and Reuters, reported the gold council’s claim without any scrutiny.

Manly concludes: “Why does the Gold Establishment not want a light shone on the central bank gold world and why are they protecting the secrecy? Equally, why do the large financial media organizations, such as Bloomberg, never want to investigate the central bank gold market?

“If this was the international oil market, they’d be all over OPEC and the producers and the industry with a huge number of reporters and journalists doing an extensive investigation.”

Manly’s report is headlined “Gold Establishment Supports Central Bank Secrecy Instead of Exposing It” and it’s posted at Bullion Star here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

end

Craig Hemke is noticing what we are seeing: huge declines in the comex silver vaults (as well as Gold vaults)

(Craig Hemke/Sprott)

Craig Hemke at Sprott Money: Watch the Comex silver vaults

Submitted by admin on Sun, 2022-11-06 19:06Section: Daily Dispatches

7:06p ET Sunday, November 6, 2022

Dear Friend of GATA and Gold:

Declining silver vault inventories, the TF Metals Report’s Craig Hemke writes this week at Sprott Money, could actually mean something for the price of the metal this time.

Hemke concludes: “So look sharp, pay attention, and keep an eye on the silver market in the months ahead. The year 2023 was already shaping up to be interesting and volatile for the precious metals. Any physical supply shortages, which then lead to a disruption in the fractional-reserve and digital-derivative pricing scheme, could make the year historic and memorable as well.”

Hemke’s analysis is headlined “The Comex Silver Vaults” and it’s posted at Sprott Money here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

4. OTHER PHYSICAL SILVER/GOLD COMMENTARIES

5.OTHER COMMODITIES:

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 7.2282

OFFSHORE YUAN: 7.2319

SHANGHAI CLOSED UP 7.02 PTS OR 0.23%

HANG SENG CLOSED UP 434.37 OR 2.69%

2. Nikkei closed UP 327.90 PTS OR 1.21%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 110.39/Euro RISES TO 0.9978

3b Japan 10 YR bond yield: FALLS TO. +.248!!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 146.72/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.272%***/Italian 10 Yr bond yield FALLS to 4.421%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.325%…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.709//

3j Gold at $1675.40//silver at: 20.65 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 49/100 roubles/dollar; ROUBLE AT 61.09//

3m oil into the 92 dollar handle for WTI and 98 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 146.72DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9898–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9877well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.138% DOWN 2 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 4.218% DOWN 3 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,61…GETTTING DANGEROUS

GREAT BRITAIN/10 YEAR YIELD: 3.579%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Reverse Sharp Early Losses To Trade Near Session Highs Ahead Of Midterms

MONDAY, NOV 07, 2022 – 08:09 AM

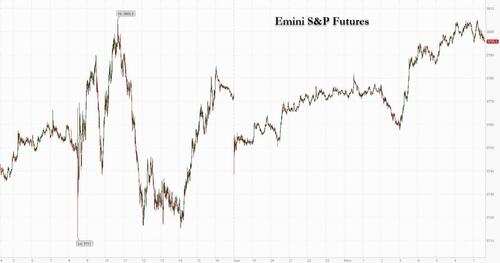

This morning’s price action has a whiff of what happened two weeks ago when a relentless barrage of bad earnings reports by tech giants propelled stocks higher during the latest bear market meltup, amid speculation the worst news is priced in. Well, after last week’s FOMC mauling, risk has once again started to meltup following Friday’s stark divergence between the “good” payrolls number and “catastrophic” employment data, sending stocks sharply higher and the dollar sliding.

And while some may have expected the selling to return after Sunday’s latest cut to high end iPhone 14 shipping forecasts, which Apple blamed on China but which appears to have been driven as much by a decline in demand and sent AAPL shares down 2%, this morning US stock futures have reversed earlier losses of more than 1% and looking to extend Friday’s rebound, as investor attention turns to the latest inflation report and the midterm elections later this week. At 7:30am ET, contracts on the Nasdaq 100 were up 0.4% after earlier sliding as much as 1.3% as Chinese officials reiterated their intention to “unswervingly” stick to a Covid Zero approach; S&P 500 futures also reversed early declines to rise 0.4%. The benchmark had snapped a four-day slump on Friday following a mixed jobs report. The dollar reversed earlier gains; while Monday’s partial gains in Treasuries were underpinned by a 4-basis point drop in the 10-year yield. The two-year rate, more sensitive to monetary policy, remained higher around the 4.68% level.

Among individual movers in premarket trading, Facebook parent Meta (which really should change its name back already) rose following a report that it is planning to start cutting thousands of jobs this week, about a week after we said it should do that immediately.

As noted above, Apple dropped after the company reduced the outlook for shipments of its latest premium iPhone due to China lockdowns. Chinese stocks listed in the US are on track to extend their rally to a fifth day even even though health authorities repeated their strict adherence to the country’s Covid Zero policies. Alibaba rose 1.3% in premarket trading, JD.com +1.4%, Baidu +2.1%, Li Auto +3.1%, XPeng +5.1%. Here are the other notable premarket movers:

Peabody Energy shares rise as much a 6% in premarket trading, after the US coal miner and Australia’s Coronado Global Resources ended merger talks.

Activision Blizzard shares fall 0.8% in US premarket trading after a NY Post report that Microsoft’s takeover of the entertainment software firm was facing heightened scrutiny from regulators, with some Activision insiders fretting that the transaction could crumble.

Redfin shares slide 8% as Oppenheimer cut the real estate brokerage to underperform, saying its core business model is “fundamentally flawed,” and putting a street-low $1.30 PT on the stock.

Keep an eye on Estee Lauder (EL US) as the stock was downgraded to hold from buy at Berenberg, which also cuts its price target, saying the cosmetics maker lacks visibility on a potential recovery.

Keep an eye on Ruth’s Hospitality after the stock was downgraded to market perform from strong buy at Raymond James, with the broker expecting higher inflation to limit earnings per share growth in 2023.

As BBG notes, US equities have tried to recover in the fourth quarter after slumping this year as investors wagered that signs of peaking in inflation would allow the Federal Reserve to slow the pace of rate hikes. The next clue will come on Thursday, with October’s consumer price index report expected to show a slight cooling in prices from the previous month.

“Markets are essentially in a struggle between people who argue the Fed has hiked rates too much and should pivot and the other group that says inflation needs to be fought harder and the Fed needs to hike more,” said Joachim Klement, head of strategy, accounting and sustainability at Liberum Capital. Victoria Scholar of Interactive Investor, agreed, saying she expects stock volatility to continue as markets face “an eclectic mix of drivers,” including the midterm elections on Tuesday.

Morgan Stanley’s in house permabear Mike Wilson turned even more bullish on Monday saying investors should stay bullish on equities ahead of the midterms. Polls pointing to Republicans winning at least one chamber of Congress provide a potential catalyst for lower bond yields and higher equity prices, which would be enough to keep the bear-market rally going, they said. Meanwhile, the permabulls at JPMorgan said the same thing they have said since Jan 1 – buy the dip because a potential peak in bond yields and “very downbeat” sentiment may support stocks.

The bout of optimism outweighs, for the moment, the Federal Reserve’s resolute campaign against price surges, signs of stress in US corporate performance and China’s announcement it will “unswervingly” adhere to current Covid Zero policy. But corporate earnings are casting a dampener on sentiment as margins reel from the impact of high inflation. Goldman Sachs Group Inc. strategists lowered their S&P 500 profit estimates for each year until 2024, saying margin contraction in the third quarter signals more pain ahead.

European stocks and US futures pare earlier declines as dollar extends declines beyond Friday’s lows. Euro Stoxx 50 rises 0.5%. Travel, miners and autos are the strongest performing sectors in Europe. DAX outperforms peers, adding 0.7%, FTSE 100 is flat, underperforming peers. Here are some of the biggest European movers today:

Telecom Italia rises as much as 8.2% to its highest intraday level since mid August following a report that Vivendi, the biggest shareholder in the phone operator, is open to discussions with the Italian government on creating a single land-line phone network.

Ryanair shares rise as much as 4.9% as the low-cost airline flagged strong bookings through next summer, shrugging off impact from a potential recession in Europe.

PostNL rises as much as 5.4% after the company notes that 4Q will be its strongest quarter, as it takes mitigating actions amid a macroeconomic environment that has deteriorated.

Flutter Entertainment shares rise as much as 5.4% in Dublin after an arbitrator told Fox Corp. that exercising its option to acquire an 18.6% stake in sports-betting giant FanDuel, which is majority owned by Flutter, would cost it at least $3.72b.

GSK falls as much as 3.3% after its antibody blood cancer drug Blenrep failed its confirmatory phase 3 trial. Citi says the news is likely to result in the drug being taken off the market in the US and the EU, expressing “minimal” expectations for commercial success going ahead.

Novozymes falls as much as 3.3% as Credit Suisse flags lower earnings and peer multiples for the world’s largest maker of industrial enzymes.

UniCredit shares declined as much as 4.2% following a FT report on Nov. 6 that the ECB had clashed with the Italian lender over its distribution plans and its Russia presence. Shares were 3% down in early trading Monday, the worst performer on the Stoxx 600 Banks Index.

Kingfisher falls as much as 3.6% as it was cut to neutral from outperform and PT trimmed to 247p from 305p at Credit Suisse on macro risks facing the DIY retailer.

Earlier in the session, Asia stocks climbed as traders snapped up Chinese stocks in hopes of an eventual reopening and as US bond yields slipped. The MSCI Asia Pacific Index advanced as much as 1.8% to the highest in a month, led by materials and technology stocks. China’s tech shares extended their rally from Friday, which was spurred by reported progress in efforts to prevent the delisting of Chinese companies from US bourses. Hong Kong topped gains in the region even though Chinese officials stuck to their Covid Zero approach over the weekend, as investors said extreme pessimism had already been priced into Greater China markets. Most gauges across Asia also advanced after 10-year Treasury yields edged lower. Supporting sentiment, the dollar slipped after a bigger-than-expected increase in the US unemployment rate spurred hope the Federal Reserve may eventually slow the pace of rate hikes. Vietnam’s shares, however, fell to their lowest in two years.

Japanese stocks climbed, as strong corporate earnings boosted investor sentiment while the market continued to look for clues on when the Federal Reserve’s monetary tightening may subside. The Topix rose 1% to close at 1,934.09, while the Nikkei advanced 1.2% to 27,527.64. Keyence Corp. contributed the most to the Topix Index gain, increasing 1.9%. Out of 2,165 stocks in the index, 1,520 rose and 558 fell, while 87 were unchanged. “Overall there there are more upward revisions,” said Mamoru Shimode, chief strategist at Resona Asset Management, regarding recent earnings reports. “The market is still looking six months to a year ahead, so the focus is gradually shifting” to results for the next fiscal year.

Australian stocks also extended gains with the S&P/ASX 200 index rising 0.6% to close at 6,933.70, extending gains for a second session, boosted by an advance in mining and energy shares. The mining sector climbed to the highest in a month, after tracking Friday’s gains in commodity prices as US jobs data, a softer dollar and China reopening hopes boosted materials last week. In New Zealand, the S&P/NZX 50 index rose 0.5% to 11,290.34.

Investors will focus on whether the subtle relaxation of China’s Covid Zero policy will gather momentum in the coming weeks, Saxo Capital Markets strategists wrote in a note. “This will be key not just for mainland and HK markets, but also for commodity markets.” Last week’s rally in Chinese shares, the biggest in years, helped lift Asia’s equity benchmark by more than 6% from an October trough. Whether that trend will continue depends on China’s tone on lockdowns and vaccinations. Investors will also keep an eye on US inflation data expected on Thursday

In FX, the Bloomberg Dollar Spot Index swung to a 0.3% loss after earlier rising by as much as 0.5%, as the greenback fell against most of its Group-of-10 peers. NZD and AUD are the weakest performers in G-10 FX, SEK and GBP outperform.

The euro rose above parity before paring gains. European bond yields were mostly lower as pricing for central major bank hikes were pared. Bund yields fell by up to 3bps while Italian yields fell by up to 5bps

The pound led G-10 gains after erasing earlier losses against the dollar. Gilt yields fell on the belly of the curve. The BOE is set to sell medium-maturity gilts held under its asset purchase facility later Monday. UK house prices fell at the sharpest pace in almost two years as rising mortgage rates and a gloomy outlook for the economy depressed demand

The New Zealand and Australian dollars pared losses after earlier dropping by more than 1% in a possible reflection of disappointment over the prospects of China easing its Covid-Zero stance

The yen pared losses as the the dollar lost traction in early European trading

In rates, Treasuries are mixed with the curve flatter into early US session as front-end cheapens led by losses in front-end of the German curve. Stocks rally and dollar extends Friday’s slide. 10-year yields are around 4.13%, richer by ~3bp on the day, outperforming bunds and gilts by 1bp and 4bp in the sector; long-end gains flatten 2s10s by 4bp, 5s30s by 3bp. Dollar issuance slate empty so far; desks expect $25b to $30b of new debt this week, front- loaded ahead of CPI and Friday’s market close for US Veterans Day. Bunds, gilts and USTs 10-year yields all decline about 1 basis point as bonds pare losses. Peripheral spreads tighten to Germany with 10y BTP/Bund narrowing 3.1bps to 213.4bps.

In commodities, WTI trades within Friday’s range, falling 0.6% to near $92; WTI and Brent futures have trimmed losses seen in wake of China sticking to its COVID policy over the weekend. Kuwait appointed Ahmed Jaber al-Aydan as the new CEO of Kuwait Oil Company and Wadha al-Khateeb as CEO of Kuwait National Petroleum Company, while new leaders were also appointed for Kuwait Integrated Petroleum Industries Company and other state companies in the energy sector, according to Reuters. Kuwait’s KPC aims to export its first oil product cargo from its 615k Al Zour refinery by mid-November, according to Reuters sources. Spot gold reversed earlier losses and climbed back above USD 1,675/oz after printing a base at around USD 1,665/oz earlier today. Base metals have also trimmed earlier losses amid the improvement in risk appetite and decline in the Buck, with 3M LME copper re-eyeing USD 8,000/t to the upside after forfeiting the level overnight.

Bitcoin is under modest pressure though pivots the mid-point of a sub-USD 1/k range which itself is a similar magnitude above the USD 20k mark.

Market Snapshot

S&P 500 futures up 0.3% to 3,788.25

STOXX Europe 600 up 0.4% to 418.47

MXAP up 1.7% to 142.45

MXAPJ up 1.8% to 459.88

Nikkei up 1.2% to 27,527.64

Topix up 1.0% to 1,934.09

Hang Seng Index up 2.7% to 16,595.91

Shanghai Composite up 0.2% to 3,077.82

Sensex up 0.3% to 61,153.50

Australia S&P/ASX 200 up 0.6% to 6,933.71

Kospi up 1.0% to 2,371.79

German 10Y yield down 0.7% to 2.28%

Euro up 0.3% to $0.9986

Brent Futures down 0.3% to $98.24/bbl

Gold spot down 0.2% to $1,679.09

U.S. Dollar Index down 0.35% to 110.49

Top Overnight News from Bloomberg

The Federal Reserve “hasn’t accomplished anything” in loosening the US labor market even after four consecutive 75-basis-point hikes, former New York Fed President Bill Dudley said

The ECB should keep raising interest rates, even at a reduced pace, until inflation excluding energy and food prices starts to ease, Governing Council member Francois Villeroy de Galhau said

Chancellor Jeremy Hunt is drawing up plans for tax increases and public spending cuts worth up to £54bn a year to fill the black hole in the UK public finances, according to allies of Britain’s chancellor, the FT reported

European households are paying more than ever for their electricity and natural gas, even as governments spend billions to shield consumers from the energy crisis

China’s total debt as a percentage of gross domestic product climbed to new record high of 272.1% in the third quarter, surpassing the previous record of 271% just a quarter ago, data compiled by Bloomberg showed

The BOJ can end up holding more than 100% of benchmark debt as its ownership doesn’t fall even when it sells the securities to market participants using repurchase agreements

President Joe Biden’s national security adviser and senior Kremlin aides have held private talks in recent months to reduce the risk of a broader conflict over Ukraine, the Wall Street Journal reported. A peace settlement wasn’t a goal of the discussions, according to the report

APAC stocks mostly gained as investors continued to pile on the reopening bets despite China ‘unswervingly’ maintaining its COVID approach, while the region also shrugged off disappointing Chinese trade data. ASX 200 was higher as strength in the commodity-related and consumer sectors atoned for the weakness in tech and financials with the latter not helped by Westpac’s earnings which showed a decline in cash profit and revenue. Nikkei 225 strengthened from the open and climbed above the 27,500 level with the index unfazed by the weak earnings releases from the likes of Sharp and SoftBank Corp. Hang Seng and Shanghai Comp recovered from opening losses in which the Hong Kong benchmark briefly surged by more than 3% amid strength in property names and a continued tech rally, while the mainland index was less decisive amid disappointing Chinese trade data and after China stuck to its strict COVID policy, as well as reported its largest number of daily infections in 6 months.

A more detailed look at global markets courtesy of Newsquawk

China health commission spokesman said China will not waver in preventing a COVID rebound and in the dynamic clearing of cases as soon as they emerge, while it did not make adjustments to anti-COVID protocols and a China disease control official said they are to guide localities to continue strengthening COVID vaccination of the elderly. Furthermore, a Peking University infectious disease expert said the current prevention strategy is still able to control COVID despite the high transmissibility of variants and asymptomatic carriers, although an Education Ministry official noted that it is necessary to prevent excessive epidemic prevention and not add extra layers of measures, according to Reuters.

Beijing City is set to improve COVID rules for people entering the city, but vows to stick to COVID-Zero policy, according to a Beijing Official cited by Bloomberg.

Haizhu district of Guangzhou, China is to extend COVID restrictionsuntil November 11th, via Bloomberg.

China’s Zhengzhou city is taking steps to improve the precision of epidemic control measures after being criticised for a one size fits all approach and the city government apologised for the problems in the latest COVID fight, while it vowed to implement social management and control measures in a precise manner to avoid simply locking down communities.

China’s new daily COVID-19 cases were rose to the highest in six months with the country reporting 5,436 new cases on Sunday, according to Bloomberg.

PBoC Deputy Governor Fan Yifei, who is a key driver of the digital yuan transition, was detained for investigation and is suspected of serious violations of discipline and law, according to SCMP.

Japan’s government releases a statement on the US inflation Reduction Act in which it stated that the requirement of EV tax credits is not consistent with the US and Japanese governments’ shared policy to work with allies and like-minded partners to build resilient supply chains. Japan added that if the IRA would be implemented as it is to provide discriminatory incentives, it is possible that Japanese automakers will hesitate to make further investments towards the electrification of vehicles, according to Reuters.

Japan is reportedly to fund its extra budget with bond issuance of JPY 22.9tln, via Bloomberg citing documents.

Top Asian News

Major bourses in Europe kicked off the session with mild losses across the board but the downside faded within the first hour of trade. Sectors are mostly firmer and have experienced a turnaround since the cash open – with defensives now largely towards the bottom of the bunch. US equity futures have also moved into the green after posting mild losses overnight and in the run-up to the European cash open. IATA September update: Total Traffic +57% YY; International Traffic +122% YY. All markets reported strong growth, led by APAC.

Top European News

UK PM Sunak and Chancellor Hunt are to announce a stealth tax raid on pensions later this month, according to The Telegraph. It was also reported the Chancellor is set to outline GBP 60bln in tax and spending cuts with early drafts of the autumn statement containing plans for up to GBP 35bln of spending cuts and GBP up to GBP 25bln on tax increases, according to The Guardian.

UK PM Sunak warned that people cannot expect the state to “fix every problem” and vowed to regain the trust of voters by being honest about the scale of the economic difficulties ahead, according to The Times.

UK PM Sunak is reportedly under pressure regarding bullying claims concerning one of his closest political allies with the opposition Labour party calling for an independent investigation of allegations of bullying by Sir Gavin Williamson who was appointed as Minister of State without Portfolio last month, according to FT.

UK stamp duty in Q3 rose to a record high of GBP 3.6bln although property market analysts warned the trend will reverse as house prices decline, according to FT.

UK steel industry warned that it needs state aid to survive a green transition with two large producers calling for the government to match the support offered to suppliers across Europe, according to FT.

Traders have pointed to a squeeze in the “repo” market and short-dated gilts, according to The Times and The Telegraph.

ECB and UniCredit (UCG IM) are reported to clash regarding capital plans and Russia presence with tensions building amid the Italian lender’s aggressive strategy to overhaul lending operations, according to FT.

Germany is to allocate EUR 83.3bln or 42% of a major protection scheme that was launched in October to finance a cap on gas and power prices next year, according to Reuters.