November 15, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

Uncategorized · Leave a comment·Edit

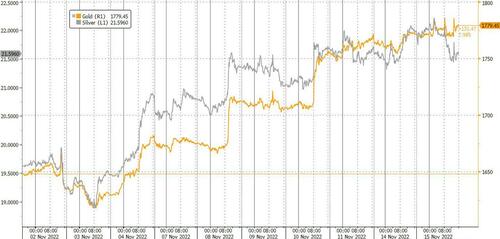

GOLD PRICE CLOSE: UP $0,15 to $1773.50

SILVER PRICE CLOSE: DOWN $0.56 to $21.65

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1778.45

Silver ACCESS CLOSE: 21.58

New: early yesterday morning//

Bitcoin morning price: $16,844 UP 590

Bitcoin: afternoon price: $16,816 UP 562

Platinum price closing DOWN $0.35 AT $1027.65

Palladium price; closing UP $6.35 at $2044.05

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: 2360.41 DOLLARS UP 2.62 CDN DOLLARS PER OZ

BRITISH GOLD: 1498.22 POUNDS PER OZ DOWN 7,32 POUNDS PER OZ

EURO GOLD: 1718.17 EUROS PER OZ UP 3.57 EUROS PER OZ.

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: NOVEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,773.600000000 USD

INTENT DATE: 11/14/2022 DELIVERY DATE: 11/16/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 38

132 C SG AMERICAS 50 1

190 H BMO CAPITAL 5

435 H SCOTIA CAPITAL 53

661 C JP MORGAN 33

737 C ADVANTAGE 14 18

800 C MAREX SPEC 4 3

880 C CITIGROUP 2

880 H CITIGROUP 21

TOTAL: 121 121

MONTH TO DATE: 6,242

TOTAL: 220 220

MONTH TO DATE: 6,12

JPMORGAN STOPPED 85/220

GOLD: NUMBER OF NOTICES FILED FOR NOV. CONTRACT: 121 NOTICES FOR 12,100 OZ or 0.3763 TONNES

total notices so far: 6242 contracts for 624,200 oz (19.415 tonnes)

SILVER NOTICES: 17 NOTICE(S) FILED FOR 85,000 OZ/

total number of notices filed so far this month 374 : for 1,870,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $0.05

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////TINY CHANGES IN GLD INVENTORY: A DEPOSIT OF 0.29 TONNES INTO THE GLD//

INVENTORY RESTS AT 910.41 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $.56

AT THE SLV// :/SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF OF 1.286 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 470.634 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 2214 CONTRACTS TO 144,108 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE HUGE GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG GAIN OF $0.41 IN SILVER PRICING AT THE COMEX ON MONDAY. OUR SHORTERS/HFT WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.41)., AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS, AS WE HAD AN ATMOSPHERIC SIZED GAIN IN OUR TWO EXCHANGES OF 3594 CONTRACTS. WE HAD A SOME ATTEMPTED SPEC SHORT COVERINGS OF THEIR SHORTFALLS WITH MINOR SUCCESS .WE HAD MINIMAL SPEC SHORT ADDITIONS AS THE PRICE OF THE METAL REMAINED FLAT . // OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. HUGE NUMBER OF NEWBIE SPEC LONGS ADDED TO THEIR POSITIONS CAUSING ADDITIONAL MISERY TO OUR SHORTERS.

WE MUST HAVE HAD:

I) SOME ATTEMPTED (WITH MINIMAL SUCCESS) SPECULATOR SHORT COVERINGS WITH ZERO SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /// HUGE NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.045 MILLION OZ FOLLOWED BY TODAY’S 50,000 QUEUE JUMP//NEW STANDING:2,575,000 MILLION OZ/ / // V) GIGANTIC SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: +100

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF NOV:

TOTAL CONTRACTS for 11 days, total 22,555 contracts: 112.775 million oz OR 10.252MILLION OZ PER DAY. (2050 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 112.775 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 112.755 MILLION

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2214 WITH OUR $0.41 GAIN IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1380 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR NOV. OF 1.345 MILLION OZ FOLLOWED BY TODAY’S 50,000 QUEUE JUMP/ .. WE HAVE AN ATMOSPHERIC SIZED GAIN OF 3494 OI CONTRACTS ON THE TWO EXCHANGES FOR 17.470MILLION OZ.. THE SILVER SHORTS ARE NOW TRAPPED AS THEY ARE HAVING CONSIDERABLE DIFFICULTY IN COVERING THOSE SHORTS D WITH THE HUGE GAIN IN PRICE ON THURSDAY.

WE HAD 17 NOTICE(S) FILED TODAY FOR 85,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 5983 CONTRACTS TO 502,424 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -683 CONTRACTS.

.

THE GOOD SIZED DECREASE IN COMEX OI CAME DESPITE OUR GAIN IN PRICE OF $7.30//COMEX GOLD TRADING/MONDAY // CONSIDERABLE ATTEMPTED SPECULATOR SHORT COVERINGS TO NO AVAIL//(MAYBE SOME SPEC SHORT ADDITIONS IF THEY ARE STUPID ENOUGH), ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION WITH CONTINUED ADDITIONS FROM OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS. IT SEEMS THAT EVERYBODY WISHES TO BUY BUT NO SELLERS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR NOV. AT 12.386 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S GIGANTIC 21,000 OZ QUEUE JUMP //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR STRONG GAIN IN PRICE OF $7.30 WITH RESPECT TO MONDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 1195 OI CONTRACTS (3.717 PAPER TONNES) ON OUR TWO EXCHANGES..

(THE COMEX LOSS WAS ALL TAKEN UP THROUGH EFP’S. THESE WILL CIRCLE BACK TO COMEX ON EXERCISING OF DELIVERY CONTRACTS).

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7178 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 502,224

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1195 CONTRACTS WITH 5983 CONTRACTS DECREASED AT THE COMEX (SHORT SPECULATORS FAILING TO GET OUT OF THEIR MESS) AND 7178 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON(AND THESE EFP’S WILL CIRCLE BACK AND EXERCISE FOR DELIVERABLE GOLD. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1878 CONTRACTS OR 5.841 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7178) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (5983): TOTAL GAIN IN THE TWO EXCHANGES 1195 CONTRACTS. WE NO DOUBT HAD 1) CONSIDERABLE ATTEMPTED BUT FAILED SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS. WE HAD ZERO SHORT SPEC ADDITIONS/// // SOME NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR NOV. AT 12.386 TONNES FOLLOWED BY TODAY’S GOOD QUEUE JUMP OF 35,600 OZ //NEW STANDING 23.808 TONNES///3) ZERO LONG LIQUIDATION //// //.,4) GOOD SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

NOV

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV. :

49,561 CONTRACTS OR 4,956,100 OZ OR 154.16 TONNES 11 TRADING DAY(S) AND THUS AVERAGING: 4505EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY(S) IN TONNES: 154.16TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 154.16/3550 x 100% TONNES 4.33% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 154.16 TONNES//INITIAL ( SO FAR MUCH LARGER THAN PREVIOUS MONTHS)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GIGANTIC SIZED 2214 CONTRACT OI TO 144,108 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1380 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 1380 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1380 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2241 CONTRACTS AND ADD TO THE 1380 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED GAIN OF 3594 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 17.970MILLION OZ//

OCCURRED WITH OUR RISE IN PRICE OF $0.41….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 50.68 PTS OR 1.64% //Hang Seng CLOSED UP 723.41 OR 4.11% /The Nikkei closed UP 26.70 OR 0.10% //Australia’s all ordinaires CLOSED DOWN 0.07% /Chinese yuan (ONSHORE) closed UP TO 7.0460 //OFFSHORE CHINESE YUAN UP 7.0457// /Oil DOWN TO 85.24 dollars per barrel for WTI and BRENT AT 92.68 / Stocks in Europe OPENED ALL MIXED. ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 5983 CONTRACTS TO 502,224 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR RISE IN PRICE OF $7.30 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (7178 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT SEEMS THAT SPEC SHORTS ARE STILL HAVING TROUBLE COVERING THEIR HUGE SHORTFALL.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON -ACTIVE DELIVERY MONTH OF NOV.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 7178 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 7178 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 7178 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A fair SIZED TOTAL OF 1,195 CONTRACTS IN THAT 7178 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A good SIZED COMEX OI GAIN OF5983 CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR RISE IN PRICE OF GOLD $7.30//WE ARE FINALLY WITNESSING SOME SPEC SHORTS TRYING TO COVER THEIR SHORTFALL WITH LIMITED SUCCESS. BANKERS CONTINUE AS NET BUYERS OF COMEX GOLD CONTRACTS AS THEY HAVE BEEN NET LONG FOR THE PAST FEW MONTHS. WE ALSO HAD HUGE ADDITIONAL NEWBIE SPECS GOING LONG. IT LOOKS LIKE OUR SPEC SHORTS ARE IN DEEP TROUBLE

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING NOV (22.834 TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 22.834 TONNES/INITIAL (TOTAL SO FAR THIS YEAR 564.435 TONNES)

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $7.30) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A FAIR GAIN OF 1195 CONTRACTS ON OUR TWO EXCHANGES. WE HAD ZERO SPEC SHORT ADDITIONS AND MINIMAL SPEC SHORT COVERINGS.. WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 1878 CONTRACTS.// WE HAVE GAINED A TOTAL OI OF 3.717 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR NOV. (22.834 TONNES)…THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE OF $7.30

WE HAD -683 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1195 CONTRACTS OR 119,500 OZ OR 3.717 TONNES

Estimated gold volume 346,777// very good//

final gold volumes/yesterday 227,682/ fair

INITIAL STANDINGS FOR NOVEMBER 2022 COMEX GOLD //NOV 15

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 140,660.630oz Brinks HSBC (390 kilobars) JPMorgan (3,000 kilobars) |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 197.803 oz HSBC |

| No of oz served (contracts) today | 121 notice(s) 12,100 OZ 0.37636 TONNES |

| No of oz to be served (notices) | 1099 contracts 109,900 oz 3.418 TONNES |

| Total monthly oz gold served (contracts) so far this month | 6242 notices 624200 19.415TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into HSBC: 197.803 oz

total deposits 197,803. oz

customer withdrawals:3

i) Out of Brinks: 31,668.740 oz

ii) Out of JPMorgan: 96,453.000 oz (3,000 kilobars)

iii) Out of HSBC: 12,538.890 oz (390 kilobars)

total: 140,660.630 oz

total in tonnes: 4.3749 tonnes

Adjustments: 0//

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR NOVEMBER.

For the front month of NOV. we have an oi of 1220 contracts having GAINED 144 contracts. We had 220 notices served on MONDAY so we gained a WHOPPING 364

or an additional 36,400 OZ (1.132 TONNES) will stand in this non active month of November. We will have Nov gold tonnage standing increase daily from this day forth until the end of the month.

This queue jumping originates in London with the exercising of London based EFP’s for comex gold.

December LOST A FAIR 15,748 contracts DOWN to 254,273. AS INDICATED ABOVE MUCH OF THE COMEX LOSS ENDS UP AS EFP’S TO LONDON AND THESE WILL CIRCLE BACK. DEC WILL BE A DILLY OF A DELIVERY MONTH.

JANUARY LOST 17 contract to stand at 222.

February gained 7991 contacts up to 201,698.

We had 121 notice(s) filed today for 12100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 121 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 33 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the NOV. /2022. contract month,

we take the total number of notices filed so far for the month (6242) x 100 oz , to which we add the difference between the open interest for the front month of (NOV 1220 CONTRACTS) minus the number of notices served upon today 121 x 100 oz per contract equals 734,100 OZ OR 22.834 TONNES the number of TONNES standing in this non active month of NOV.

thus the INITIAL standings for gold for the NOV. contract month:

No of notices filed so far (6242) x 100 oz+ (1220) OI for the front month minus the number of notices served upon today (121} x 100 oz} which equals 734,100 oz standing OR 22.808 TONNES in this NON active delivery month of NOV..

TOTAL COMEX GOLD STANDING: 22.834 TONNES (A HUMONGOUS STANDING//NEW RECORD FOR NOV (GENERALLY THE POOREST DELIVERY MONTHS FOR A NON ACTIVE MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,930,287.070 OZ 60.04 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 23,971,924.047 OZ

TOTAL REGISTERED GOLD: 11,142,699.707 OZ (346,58 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 12,829,224.300 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,212,412OZ (REG GOLD- PLEDGED GOLD) 286.54 tonnes//rapidly declining

END

SILVER/COMEX

NOV 15//INITIAL NOV. SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 610,574.949 oz Brinks CNT Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 184,973.900 oz Delaware |

| No of oz served today (contracts) | 17 CONTRACT(S) (85,000 OZ) |

| No of oz to be served (notices) | 141 contracts (705,000 oz) |

| Total monthly oz silver served (contracts) | 374 contracts (1,870,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 3 withdrawals out of the customer account

i) Out of Brinks: 973.400 oz

ii) Out of CNT: 8712.600 oz

iii) Out of Manfra: 600,889.349 oz

Total withdrawals: 610,574.949 oz

JPMorgan has a total silver weight: 153.534million oz/296.596 million =51.77% of comex .//dropping fast

Comex deposits:

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 35,322 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 296.586MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF NOV OI: 158 CONTRACTS HAVING GAINED 8 CONTRACT(S.)

WE HAD 2 NOTICES FILED ON MONDAY, SO WE GAINED 10 CONTRACTS OR AN ADDITIONAL 50,000 OZ WILL STAND

FOR SILVER IN THIS VERY NON ACTIVE DELIVERY MONTH OF NOVEMBER.

DECEMBER SAW A LOSS OF 2515 CONTRACTS DOWN TO 69,055

(WE WILL HAVE A DANDY DEC. DELIVERY MONTH AS THE CONTRACTION IS GOING VERY SLOWLY)

JANUARY SAW A LOSS OF 15 CONTRACTS UP TO 1372 CONTACTS.

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY:17 for 85,000 oz

Comex volumes:105,928// est. volume today// huge

Comex volume: confirmed yesterday: 74,920 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 374 x 5,000 oz = 1,870,000 oz

to which we add the difference between the open interest for the front month of NOV(158) and the number of notices served upon today 17 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the NOV../2022 contract month: 747 (notices served so far) x 5000 oz + OI for front month of NOV (158) – number of notices served upon today (17) x 5000 oz of silver standing for the NOV. contract month equates 2,575,000 oz.

We will gain in silver oz standing from this day forth until the end of the month.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:49,371// est. volume today// poor

Comex volume: confirmed yesterday: 101,267 contracts ( huge)

END

GLD AND SLV INVENTORY LEVELS

NOV 15/WITH GOLD UP $.05: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 29 TONNES INTO THE GLD////INVENTORY RESTS AT 910.41 TONNES

NOV 14/WITH GOLD UP $7.30: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 910.12 TONNES

NOV 11/WITH GOLD UP $15.25//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD////INVENTORY RESTS AT 911.57 TONNES

NOV 10/WITH GOLD UP $40.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.38 TONNES

NOV 9/WITH GOLD DOWN $2.00: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES INTO THE GLD////INVENTORY RESTS AT 908.38 TONNES

NOV 8/WITH GOLD UP $34.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.47 TONNES FROM THE GLD//: INVENTORY RESTS AT 905.49 TONNES

NOV 7/WITH GOLD UP $2.95: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.63 TONNES FROM THE GLD//INVENTORY RESTS AT 906.96. TONNES

NOV 4/WITH GOLD UP $44.45 TO $1673.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.48 TONNES FROMTHE GLD////INVENTORY RESTS AT 911.59 TONNES.

NOV 3/WITH GOLD DOWN $18.30 TO $1628.85: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.05 TONNES FROM THE GLD////INVENTORY RESTS AT 915.07 TONNES

NOV 2/WITH GOLD UP 55 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 919.12 TONNES.

NOV 1/WITH GOLD UP $9.20 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES FORM THE GLD../INVENTORY RESTS AT 920.57 TONNES

OCT 31/WITH GOLD DOWN $4.00; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD//INVENTORY RESTS AT 922.59. TONNES//

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

GLD INVENTORY: 910.41 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

NOV 15/WITH SILVER DOWN $.56 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.286 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.634 MILLION OZ..

NOV 14/WITH SILVER UP 41 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 11/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ FROM THE SLV///INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 10/WITH SILVER UP 39 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 368,000 OZ INTO THE SLV///INVENTORY RESTS AT 472.476 MILLION OZ//

NOV 9/WITH SILVER DOWN 10 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV/; A WITHDRAWAL OF 3.821 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 472.108 MILLION OZ//

NOV 8/WITH SILVER UP 48 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.751 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 475.929 MILLION OZ//

NOV 7/WITH SILVER UP 12 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 4/WITH SILVER UP $1.31 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.972 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 3.WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 566,000 OZ FROM THE SLV////INVENTORY RESTS AT 482.650 MILLION OZ//

NOV 2/WITH SILVER DOWN 9 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 92,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.216 MILLION OZ//

NOV 1/WITH SILVER UP 53 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 415,000 OZ FORM THE SLV////INVENTORY RESTS AT 483.308 MILLION OZ

OCT 31: WITH SILVER FLAT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .644 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 483.723 MILLION OZ//

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: A WITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

CLOSING INVENTORY 470.634 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff .

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

14 Nov 2022

3. Chris Powell of GATA provides to us very important physical commentaries

4. OTHER PHYSICAL SILVER/GOLD COMMENTARIES

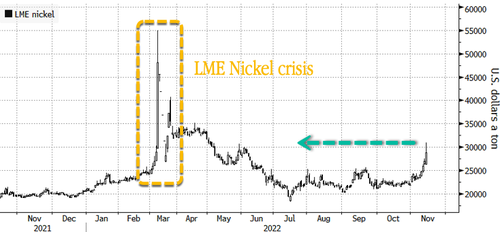

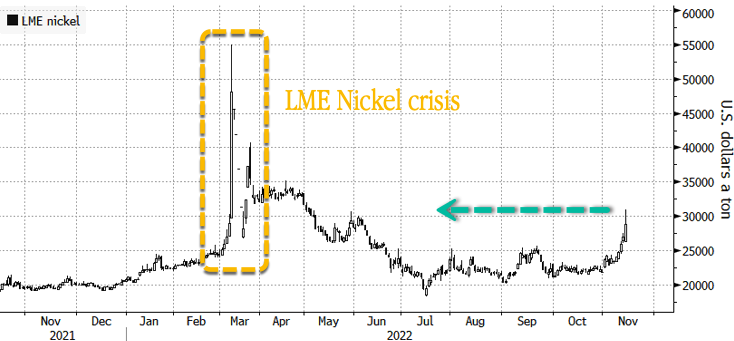

5.OTHER COMMODITIES: NICKEL

Nickel Jumps As Tesla-Backed Miner Sparks Supply Fears

TUESDAY, NOV 15, 2022 – 03:15 PM

Nickel prices jumped Tuesday on the news of production setbacks at the troubled Goro nickel mine, which has one of the world’s largest deposits and is partially owned by Trafigura Group and backed by Tesla Motors, reported Bloomberg.

Goro is located in the South Pacific island French territory of New Caledonia. The mine has been forced to curtail production following a leak from its tailings dam — an earth-fill embankment dam used to store byproducts after separating the ore from mining waste.

A spokesperson from owner Prony Resources said the Goro Mine reported a “limited release of salt-laden liquid” following torrential rains in August. Corrective measures required by local authorities reveal nickel output would be reduced in the fourth quarter.

The nickel market has seen wild price swings in the last two sessions following reports of an explosion at a nickel factory in Indonesia on Monday, which sent prices skyrocketing 15%, though prices retreated after the owner of the operation denied reports.

Prices on the London Metal Exchange jumped as high as 7.5% to $31k per ton on Tuesday, hitting the highest level since May.

Nickel prices trading on the LME have seen increased volatility. In March, the LME halted trading for a week after prices soared 250% in two sessions.

Brazilian miner Vale SA previously owned Goro. It was sold last year to Prony — a group comprising Trafigura, Agio Global, and the New Caledonian government.

The good news is that “minimum quantities required by our customer contracts will be met, and we expect to be at full capacity again shortly,” Prony said.

Global supply tightness for the battery-critical making metal comes as electric-vehicle demand soars. This will undoubtedly keep the costs of EVs out of reach for the average person.

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

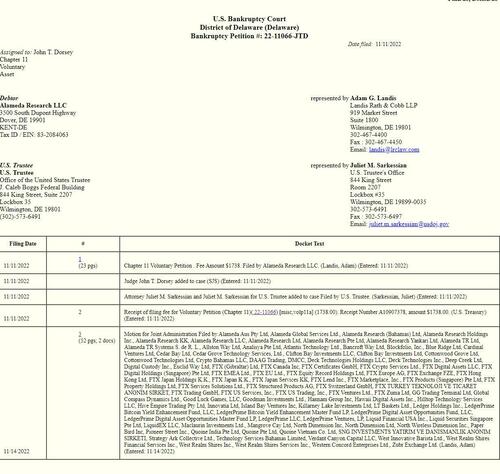

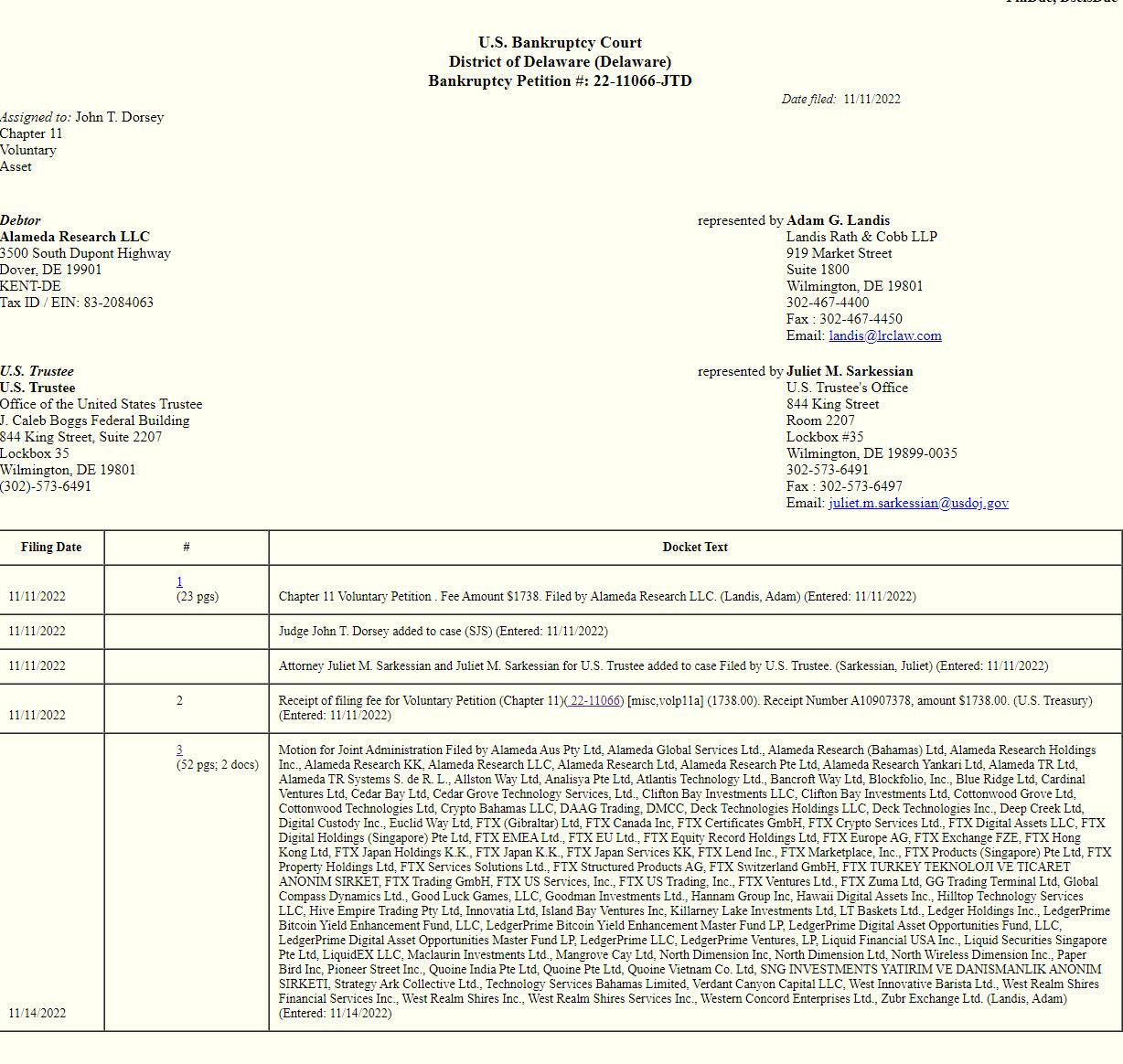

Bankman-Fried Trying To Raise Fresh Capital As Bankruptcy Lawyers Reveal More Than One Million Creditors

TUESDAY, NOV 15, 2022 – 11:10 AM

We have been waiting for the FTX bankruptcy docket to add anything more than merely procedural filings (or any filings for that matter), and certainly the so-called First Day filings which should lay out what really happened at the now bankrupt exchange-cum-hedge fund, but the only thing we have gotten so far is this: just two entries in the docket for a case which the entire world is closely following.

And while the criminal mastermind behind FTX, Bankman-Fried, should at least be doing everything he can to explain where the billion in client funds vaporized to, as he promised…

… at least until such time as he is finally arrested (which Elon Musk said will never happen because he is such a prominent Democratic donor), he appears to have little desire to do the right thing, and instead has been trying to salvage an unfixable situation and according to the WSJ, the 2nd largest democrat donor still thinks that he can raise enough money to make users whole.

Bankman-Fried, alongside a few remaining employees, spent the past weekend calling around in search of commitments from investors to plug a shortfall of up to $8 billion in the hopes of repaying FTX’s customers, the WSJ sources said. It wasn’t clear if any proceeds from such fundraising would go into his personal bank account, nor was it clear if he was merely calling other fugitive criminals such as Jho Low who made billions by robbing Malaysia blind with the help of Goldman Sachs, or is simply hoping to find even bigger idiots than his current roster of “erudite” investors.

The WSJ goes on to redundantly notes that the “efforts to cover that shortfall have so far been unsuccessful.” The paper also couldn’t determine what SBF is offering in return for any potential cash infusion, or whether any investors have committed. To be sure, the last thing on SBF’s mind is to transfer some of his well-hidden offshore funds to make those customers who trusted him whole.

Before the chapter 11 filing, Bankman-Fried had spoken to companies including rival crypto exchanges Coinbase and Kraken, plus hedge funds and venture capital investors in the hope of a bailout, according to people familiar with those talks. His largest rival, Binance, agreed briefly to buy FTX, before backing out.

The amount needed to make FTX solvent would likely be multiples of the $1.9 billion the company raised during its existence. FTX’s most recent funding round was in January, when it raised $400 million from a long list of Silicon Valley and Wall Street names, including Tiger Global and SoftBank Group Corp.

In separate news, FTX’s bankruptcy lawyers said the case could involve more than one million creditors: that means there will be a lot of angry people when the Democrat-controlled DOJ announces it has no plans to press charges against one of the most generous (and criminal of course) Democrat donors in history. Because the last thing anyone wants is to tie the money laundering loose ends between Democrats, Ukraine and crypto fund flows over the past year.

END

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 7.0460

OFFSHORE YUAN: 7.0457

SHANGHAI CLOSED UP 50.68 PTS OR 1.64%

HANG SENG CLOSED UP 723.41 OR 4.11%

2. Nikkei closedUPN 26.70 PTS OR 0.10%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 105.98/Euro RISES TO 1.0405

3b Japan 10 YR bond yield: FALLS TO. +.239!!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 139,24/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.083%***/Italian 10 Yr bond yield FALLS to 4.058%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.109%…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.252//

3j Gold at $1785.65//silver at: 21.90 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 35/100 roubles/dollar; ROUBLE AT 60.21//

3m oil into the 85 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 139.24DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9408– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9789well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.801% DOWN 7 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.998% DOWN 6 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,61…

GREAT BRITAIN/10 YEAR YIELD: 3.405%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Surge Over 4,000 As Yields And Dollar Slide On Positive US-China Sentiment, Solid Earnings

TUESDAY, NOV 15, 2022 – 07:47 AM

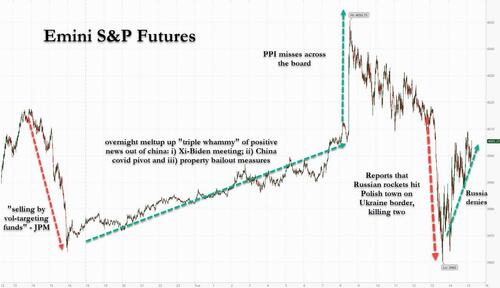

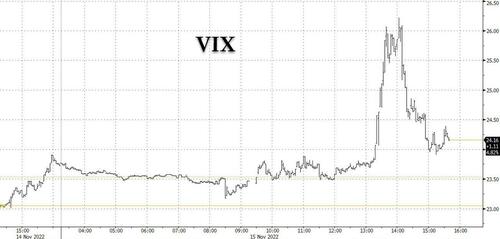

US futures jumped from Monday’s shallow dip, which in turn followed the S&P 500’s best week since June, boosted by a triple-whammy of positive news out of China, including the Xi-Biden meeting which pointed to easing tensions between Washington and Beijing, China’s Covid pivot and property measures, and solid earnings from Walmart which boosted guidance and announced a new $20BN buyback. Contracts on the Nasdaq 100 extended earlier gains and were up 1.1% as of 7:1 a.m. ET while S&P 500 futures surged above 4000, rising almost 1.0%. Treasury yields and the dollar slipped while bitcoin resumed its modest rise. At 8:30am we get another inflation read in the form of the latest PPI Print, which is also expected to ease modestly.

In premarket trading, chipmakers AMD, Nvidia and Intel Corp. rose between 1.3%-2% while Tesla Inc., Amazon.com Inc., Apple Inc., and Alphabet Inc. all added about 1% each. Coinbase and Marathon Digital led cryptocurrency-linked stocks higher as Bitcoin extended gains with investors waiting for more details about an industry-recovery fund promised by Binance Holdings Chief Executive Officer Changpeng ‘CZ’ Zhao. Chinese stocks listed in the US were set to rise for a fourth day, after a triple-whammy of positive news including Xi-Biden meeting, Covid pivot and property measures. Alibaba (BABA US) soared 11% in premarket trading. Lithium-exposed stocks edged lower following a selloff in Asian peers amid worries over potentially weaker demand from Chinese firms. Here are the other notable premarket movers:

- Getty Images (GETY US) falls 12% in US premarket trading, after the media company reported third quarter earnings that missed the average analyst estimate.

- Ginkgo Bioworks (DNA US) shares slip as much as 2.6% in US premarket trading as the cell-programming platform provider’s revenue beat was eclipsed by worries over how a tougher economic environment could impact prospects.

- Harley-Davidson (HOG US) is initiated with an underperform rating, its only sell-equivalent recommendation, and a $39 PT at Jefferies, which says the strength in the motorcycle maker’s shares is overdone.

- Lithium-exposed stocks edged lower in US premarket trading following a selloff in Asian peers amid worries over potentially weaker demand from Chinese firms.

- Nubank (NU US) shares jump 15% in premarket trading after the Brazilian digital bank’s third-quarter results. Morgan Stanley said the lender delivered a strong print, showing beats for client net adds, revenue, gross profit and adjusted net income.

- Shoals Technologies (SHLS US) shares soar as much as 22% in US premarket trading, on track for its biggest rise in five months, as analysts nudged their price targets higher after the solar energy products supplier narrowed its revenue forecast for the full year. Brokers said that the firm’s rising backlog and awarded orders bode well for the future and increase visibility for next year

Markets have turned risk-on in recent days, trading off a softer-than-expected US data print that many reckon will allow the Fed to raise rates in 50 basis-point increment, after consecutive 75 basis-point hikes. That view was encouraged by dovish comments from Vice Chair Lael Brainard who said on Monday it would probably be “appropriate soon to move to a slower pace of increases.”

“The issue the market has to wrestle with is how long is the Fed going to keep rates at that level and I think there is some positive sentiment out there that the Fed is going to pivot sometime in 2023,” Peter Kraus, Chairman and CEO at Aperture Investors, told Bloomberg Television.

Sentiment also got a solid boost overnight following signs of easing tensions between the US and China (even if Xi probably does not see it that way, and instead he delivered a speech at the G20 summit in Bali, Indonesia, in which he urged against politicizing food and energy issues, and called for scrapping unilateral sanctions and restrictions on technology cooperation in this area, something which won’t happen). In any case, after the meeting between Joe Biden and Xi Jinping on Monday, Washington said the two sides would resume cooperation on issues including climate change and food security, and that Biden and Xi jointly chastised the Kremlin for loose talk of nuclear war over Ukraine.

Investors also remain focused on central banks: Swissquote analyst Ipek Ozkardeskaya said equity markets are in “a vicious circle” as “investors want to feel better, but the Fed can’t let them feel much better as a market rally would play against its inflation fight.” Last week’s rebound was a “flash in the pan, but the downside risks have certainly eased,” she said.

Meanwhile, markets are watching growing risks to earnings following corporate America’s weakest reporting season since the first quarter of 2020, and the outlook for stock markets in 2023. “The equity market will continue to rally until the end of the year with some volatility, but once you get to 2023 there will be some realization that interest rates will actually start to slow economic activity,” said Peter Kraus, chief executive officer at Aperture Investors. “In 2023, you will have more volatility and you’ll have a decline in equity markets,” Kraus said on Bloomberg TV.

The latest Bank of America’s global fund manager survey for November showed sentiment remains “uber-bearish,” with investors still crowded into the dollar and cash, while tech stocks remain unpopular. “My biggest concern is the market gets ahead of itself and we get into a situation where the Fed feels it needs to rein in, and tighten more than it otherwise would have, as markets became too frothy,” Kristina Hooper, chief global strategist at Invesco said on Bloomberg Radio.

In Europe the Stoxx 600 index swung between losses and gains, though the market is close to a three-month high and Germany’s Dax index is on the cusp of a technical bull-market, having narrowly missed that milestone on Monday. The Euro Stoxx 50 rises 0.1%. CAC 40 outperforms peers, adding 0.3%, FTSE MIB lags, dropping 0.3%. Utilities, food & beverages outperformed while retail and telecoms underperform as more sectors turn negative on the day. Here are some of the biggest European movers today:

- Teleperformance shares rise as much as 9.4%, the third session of gains in a recovery from a recent drop suffered by the customer relationship management services firm following a report related to its content moderation business in Colombia.

- UK utilities and energy firms advance after reports that UK’s Chancellor Jeremy Hunt is considering a new 40% windfall tax on the “excess returns” of electricity generators.

- Drax rises 4.0%, Centrica +5.0%

- BAE Systems shares gain as much as 4.1% after a trading update from the defense contractor that analysts said shows trading momentum remains solid.

- Ambu falls as much as 16%, the most since May, after the Danish medical technology firm’s latest earnings and outlook disappointed, according to analysts.

- Ocado shares plunge as much as 13% in Tuesday morning trading, paring the 30% rally in the previous two sessions after last week’s softer-than-expected US inflation data provided a boost to growth stocks.

- Nexi shares fall as much as 11%, the most intraday since March 2020, after holder Intesa Sanpaolo sold its stake in the payment services firm.

- Vodafone shares slump as much as 9.2% and are on track for their lowest close in 25 years after the telecom operator trimmed its outlook for Ebitda after- leases to the lower end of its previous range, citing higher energy costs.

- Cellnex slides as much as 6.5% after a share placement of 25.6m shares at EU33.50/share.

Earlier in the session, Asian stocks rallied as China led the region higher, buoyed by more property easing measures and signs of reduced US-China tensions. The MSCI Asia Pacific Index rose as much as 1.9% to a two-month high, lifted by technology shares. Chinese stocks in the sector helped pace the benchmark’s gain as investors bet the worst may be over for some of the major players. Meanwhile, Taiwan’s TSMC surged after a filing showed Warren Buffett recently bought a stake of about $5 billion in the chipmaker. China and Hong Kong benchmarks extended their recent rebounds, with the Hang Seng Index entering a bull market, gaining as much as 4.2% as regulators moved to further ease a liquidity crunch faced by real estate developers. Sentiment was also lifted by Monday’s meeting between Joe Biden and Xi Jinping that generated hopes of warmer ties between the two superpowers. That encounter offset the weak retail sales data that underscored the impact of Covid lockdowns on China’s economy. There’s “some easing of bilateral tensions from the Xi-Biden meeting,” said Marvin Chen, a Bloomberg Intelligence analyst, who added that China’s macro data, which came in below expectations, could “boost the probability of more easing measures in the near term.”

Japanese equities erased earlier losses, as investors weighed Fed comments for clues on where rate hikes might go and as improvement in US-China ties lifted sentiment across Asia. The Topix Index rose 0.4% to 1,964.22 as of market close Tokyo time, while the Nikkei advanced 0.1% to 27,990.17. Sumitomo Mitsui Financial Group Inc. contributed the most to the Topix Index gain, increasing 4.2% as the company raised its key profit forecast and announced a share buyback plan. Out of 2,165 stocks in the index, 1,308 rose and 766 fell, while 91 were unchanged. “The financial results are almost all done as of yesterday and the stock market is running out of materials,” said Hideyuki Suzuki, general manager at SBI Securities. “All the important indicators from the FOMC, US CPI data, and earnings are over. The question is what the future holds from here.”

Stocks in India advanced as easing inflation boosted investors’ sentiment while the country’s corporate earnings season ended. A rally in lenders boosted the benchmark Sensex to a new high while pushing the NSE Nifty 50 Index near its record level. The S&P BSE Sensex rose 0.4% to 61,872.99 in Mumbai, while the NSE Nifty 50 Index advanced by an similar measure. Thirteen of the 19 sector sub-indexes advanced, led by oil and gas and telecom companies. ICICI Bank contributed the most to the index gain, increasing 1.9%. Out of 30 shares in the Sensex index, 19 rose and 10 fell, while 1 was unchanged. The consumer-price index for October rose 6.77%, easing from the 7.4% rise in September, which was the highest level in nearly two years, while the pace of wholesale inflation slowed to 8.4%, its first single digit reading in 19 months.

In FX, the dollar resumed its decline, giving G-10 FX some relief. The yen trades at around the level of 139/USD, while pound rises to $1.18. The Bloomberg Dollar Spot Index swung to a loss early in the European session as the greenback weakened against all of its Group-of-10 peers. Treasury yields fell, led by the belly of the curve. The five-year yield was down around 5bps.

- The euro rose to a four-month high of $1.0437. Most European bond yields fell, led by the long end of the curve; Italy’s 10-year yield fell by 10bps and Germany’s by 4bps. Germany Nov. ZEW investor expectations rise to -36.7; est. -51.0

- The pound rose against both the dollar and the euro after UK wages grew at the fastest pace in more than a year. Investors will also be watching inflation data Wednesday and the UK’s fiscal announcement Thursday

- UK investors are facing the biggest glut of gilts in nearly a decade. Government bond sales will hit £185 billion ($217 billion) for this fiscal year to April, according to the median estimate of 10 banks surveyed by Bloomberg. The bid-to- cover on a UK 10-year gilt sale fell to its lowest level since Oct. 2019 at 2.11, according to data compiled by Bloomberg

- The Aussie and Kiwi touched fresh two-month highs. RBA minutes showed policy makers were prepared to return to larger rate hikes if needed. Australia’s bond curve twist-flattened.

- The yen rebounded on broad-based dollar weakness. The Japanese currency earlier dropped after data showed Japan’s economy unexpectedly shrank in the third quarter.

In rates, Treasury and bunds 10-year yields are about 1.5bps lower, gilts 10-year yield little changed. Treasury futures topped Monday’s highs in early US trading, led by bunds after ECB’s Villeroy said a slower pace of hikes is likely after next month’s meeting. Into the move 10-year yields drop below 50-DMA for the first time since August. The US Treasuries’ advance was led by the belly, with 5-year yields richer by nearly 6bp on the day, steepening 5s30s spread by ~3bp; 10-year, lower by 4.5bp at ~3.81%, trails bunds by more than 2bp.US auctions resume Wednesday with $15b 20-year bonds, followed by $15b 10-year TIPS Thursday.

In commodities, WTI crude futures ease to below $85; as benchmarks are pressured with the overarching COVID headwind weighing on the demand side and overshadowing any potential upside from the USD & G20. Currently, WTI Dec’22 and Brent Jan’23 are lower by just over USD 1/bbl and have printed fresh November troughs of USD 84.06/bbl and USD 91.52/bbl respectively. Precious metals have lost their initial shine but spot gold remains in proximity to yesterday’s USD 1775/oz high. Ags. are in focus on the above reports, though initial pressure has eased a touch as Russia says it will make a decision at an appropriate time.

To the day ahead now, and data releases from the US include October’s PPI reading and the Empire state manufacturing survey for November, while in Europe there’s UK employment data for October and the German ZEW survey for November. Central bank speakers include the Fed’s Harker, Cook, Barr and the ECB’s Elderson. Finally, earnings releases include Walmart and Home Depot.

Market Snapshot

- S&P 500 futures up 0.6% to 3,990.50

- STOXX Europe 600 little changed at 432.94

- MXAP up 1.9% to 154.34

- MXAPJ up 2.3% to 500.95

- Nikkei little changed at 27,990.17

- Topix up 0.4% to 1,964.22

- Hang Seng Index up 4.1% to 18,343.12

- Shanghai Composite up 1.6% to 3,134.08

- Sensex up 0.3% to 61,785.91

- Australia S&P/ASX 200 little changed at 7,141.63

- Kospi up 0.2% to 2,480.33

- German 10Y yield down 2.1% to 2.13%

- Euro up 0.6% to $1.0394

- Brent Futures down 1.3% to $91.89/bbl

- Gold spot up 0.2% to $1,774.81

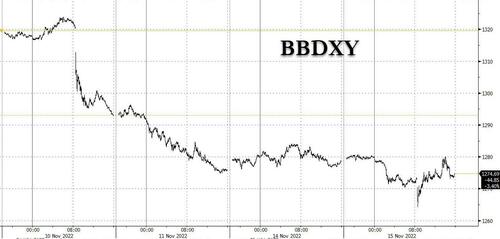

- U.S. Dollar Index down 0.35% to 106.29

Top Overnight News from Bloomberg

- Signs of inflation peaking in the US are a relief for policy makers around the world who’ve been raising interest rates at a record pace to combat price pressures, ECB Governing Council member Francois Villeroy de Galhau said

- UK Chancellor Jeremy Hunt is considering a new 40% windfall tax on the “excess returns” of electricity generators as part of his sprawling package of tax rises and spending cuts this week, according to a person familiar with the proposal

- Oil inventories in developed nations have sunk to the lowest since 2004, leaving global markets vulnerable as sanctions on Russian exports take effect, according to the International Energy Agency

- Global investors reduced their holdings of China government bonds in the onshore market for a ninth-month running in October amid concerns over policy uncertainty spurred by President Xi Jinping’s consolidation of power

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed following a weak lead from Wall Street with newsflow also quiet overnight. ASX 200 saw pressure from its Metals & Mining sector, whilst the RBA minutes provided little in terms of hints for the upcoming meeting and left all options open. Nikkei 225 saw some downside after Q3 Japanese GDP unexpectedly fell into contraction, but losses were trimmed as the JPY weakened. KOSPI was contained whilst Taiwan’s Taiex outperformed as TSMC was boosted by a Berkshire Hathaway stake in the name. Hang Seng and Shanghai Comp cheered the meeting between US President Biden and Chinese President Xi, which was telegraphed as candid, whilst Chinese stocks saw little action to the Retail Sales contraction and sub-forecast IP metrics.

Top Asian News

- China reports 1,661 new confirmed COVID cases in mainland (prev. 1,794 a day earlier), via Reuters.

- PBoC injected CNY 850bln via 1yr MLF at a maintained rate of 2.75%; PBoC injected CNY 172bln via 7-day reverse repos with the rate at 2.00% for a CNY 170bln net injection.

- PBoC said longer-term fund injection exceeds Nov MLF maturities, according to Bloomberg.

- Chinese Vice President Wang said China will maintain strong policy continuity, according to Bloomberg.

- China’s Stats Bureau said will actively expand demand, stabilise employment and prices; will consolidate the foundation of economic recovery; economic recovery slows due to COVID flare-ups, via Reuters.

- China’s stats bureau spokesman said the property market shows some positive changes but the downward trend continues; expects China’s CPI to remain benign, via Reuters.

European bourses are mixed overall, Euro Stoxx 50 +0.2%, as opening gains scale back after a mostly constructive APAC session. Stateside, US futures are firmer across the board with Tech leading after strong APAC tech trade and in wake of Fed’s Brainard, ES +0.7%. Home Depot Inc (HD) Q1 2023 (USD): EPS 4.24 (exp. 4.12), Revenue38.9bln (exp. 37.95bln); Comps sales +4.3% (exp. 3.1%); reaffirms FY22 guidance.

Top European News

- UK PM Sunak will accept an official recommendation to increase the living wage from GBP 9.50 an hour to about GBP 10.40 an hour — a rise of nearly 10%, according to The Times.

- UK Chancellor Hunt is considering a 40% windfall tax on “excess returns” made by electricity generators as part of his Autumn Statement, according to Bloomberg sources.

- ECB’s Villeroy said ECB will probably continue to hike rates but may do so in a more flexible and less rapid manner; jumbo hikes will not become a new habit. We are clearly approaching the normalisation range of around 2%, via Reuters.

- EU Parliament and member states agreed on an EU budget for 2023, according to dpa.

- G20 draft declaration noted that central banks will continue to appropriately calibrate the pace of monetary policy tightening, via Reuters.

FX

- DXY continues to slip after a pronounced move which occurred prior to the European cash open, currently near sub-106.00 lows to the broad benefit of peers.

- USD/JPY has been touted by some as a key driver of the above move given its quick move from above-140.00 to sub 139.00.

- GBP benefits from the USD weakness and perhaps firm wage metrics though this was accompanied by an unexpected unemployment uptick, ahead of Wednesday’s CPI and Thursday’s fiscal update.

- Yuan remains in keen focus as it moves comparatively closer to the 7.00 handle, though proved resilient to soft overnight data with focus firmly on the broader USD move.

- SEK was unfased by soft-headline but hot-core vs exp. CPIF metrics, though this has prompted SEB to raise the risk of a 100bp Riksbank hike.

Fixed Income

- BTPs are leading the fixed income complex with upside in excess of a point to a session peak of 117.26 vs trough 116.04 on supply-side dynamics.

- Bunds are similarly bid though to a lesser extent than periphery counterparts, having incrementally surpassed yesterday’s 139.26 peak.

- Well-received German 7yr supply sparked limited upside while a softer UK outing caused Gilts to temporarily pullback to near-unchanged.

- USTs move in tandem with EGBs with yields lower as such in wake of Fed’s Brainard, who backed the FOMC downshifting to a lower increment of rate hikes in December.

- Retail orders for the November 2028 BTP Italia reach EUR 4bln, via Reuters citing Bourse data.

Commodities

- Crude benchmarks are pressured with the overarching COVID headwind weighing on the demand side and overshadowing any potential upside from the USD & G20.

- Currently, WTI Dec’22 and Brent Jan’23 are lower by just over USD 1/bbl and have printed fresh November troughs of USD 84.06/bbl and USD 91.52/bbl respectively.

- IEA Monthly Oil Market Report: 2023 global oil output is to grow 740k BPD to 100.7mln BPD. Demand growth will slow to 1.6 mb/d in 2023, down from 2.1 mb/d this year, as mounting economic headwinds impede gains.

- Russia is reportedly expected to agree to extend the Black Sea grain-export deal, via Bloomberg. Subsequently, Russia says it will announce its decision on extension of Black Sea grains deal in an appropriate time, TASS reports.

- Precious metals have lost their initial shine but spot gold remains in proximity to yesterday’s USD 1775/oz high.

- Ags. are in focus on the above reports, though initial pressure has eased a touch as Russia says it will make a decision at an appropriate time.

G20

- Australian PM says there were positive discussions on trade embargoes levelled on Australia by China. Adds, the meeting with Chinese President Xi was another important step towards stabilising the relationship, will cooperate where possible with China. Many steps yet to take.

- Chinese President Xi says Sino-Australian relations have encountered difficulties in recent years and this is not what we wanted to see, according to State Media

- Russian Foreign Minister Lavrov says he has proposed to the G20 the removal of discriminatory barriers on energy markets; UN will deal with the removal of barriers for Russian grain and fertilizers; the G20 draft declaration has reference to an exchange of views re. Ukraine, West added phrase that many delegations condemned Russia. Russia highlighted alterative points of view.

Geopolitics

- Chinese President Xi said China advocates a ceasefire in the Ukraine crisis and calls for peace talks, via state media.

- Chinese President Xi told US President Biden that China will make all efforts for peaceful “reunification” with Taiwan, according to the Chinese Foreign Minister. China upholds the “one country, two systems” proposal for Taiwan, according to Reuters

- Chinese President Xi told French President Macron that China and Europe should expand two-way trade and investments, via state media.

US Event Calendar

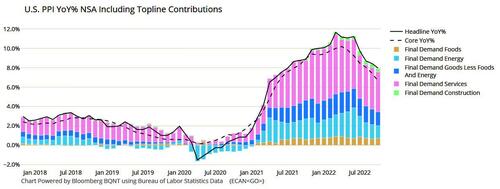

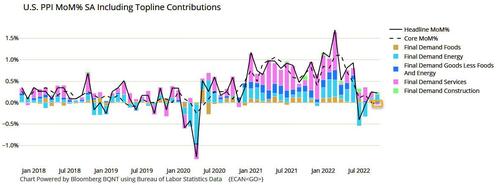

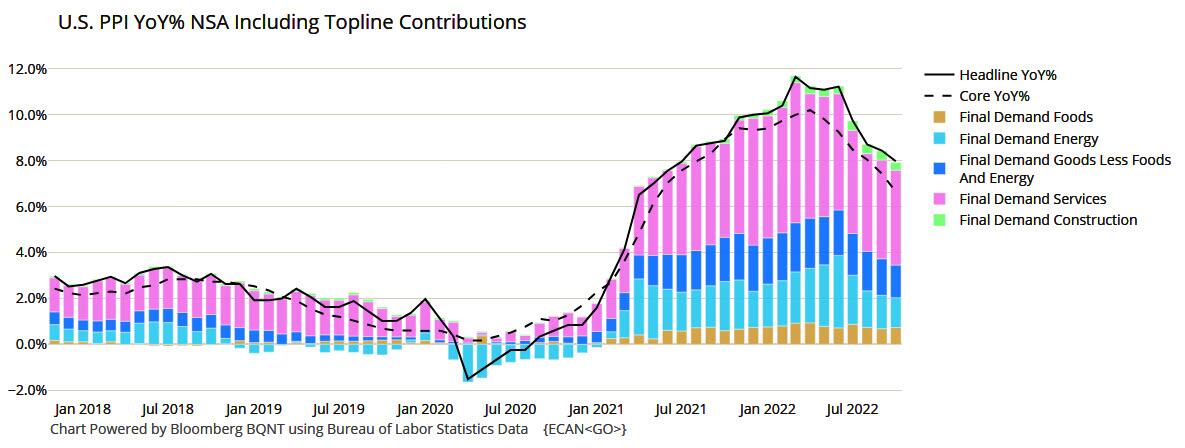

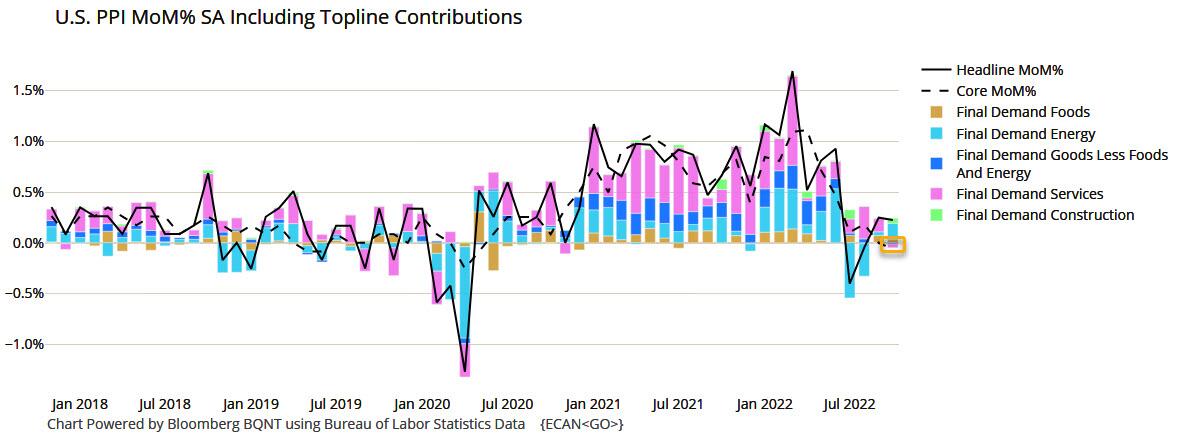

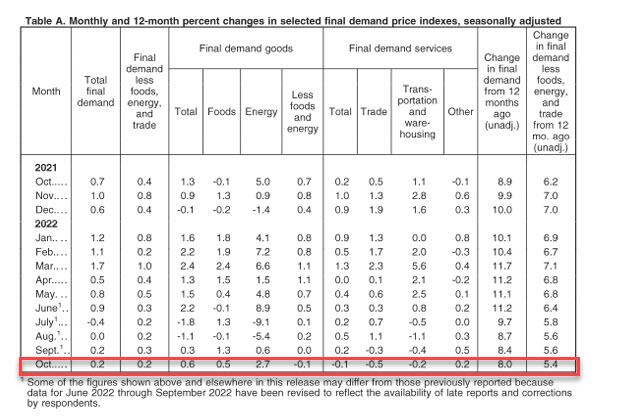

- 08:30: Oct. PPI Final Demand YoY, est. 8.3%, prior 8.5%

- Oct. PPI Final Demand MoM, est. 0.4%, prior 0.4%

- Oct. PPI Ex Food and Energy YoY, est. 7.2%, prior 7.2%

- Oct. PPI Ex Food and Energy MoM, est. 0.3%, prior 0.3%

- Oct. PPI Ex Food, Energy, Trade YoY, est. 5.6%, prior 5.6%

- Oct. PPI Ex Food, Energy, Trade MoM, est. 0.3%, prior 0.4%

- 08:30: Nov. Empire Manufacturing, est. -6.0, prior -9.1

Central Banks

- 09:00: Fed’s Harker Discusses the Economic Outlook

- 09:00: Fed’s Cook Discusses Post-Covid Challenges Facing Women

- 10:00: Fed Vice Chair for Supervision Barr Speaks Before Senate Panel

DB’s Jim Reid concludes the overnight wrap

I appreciate the EMR is often a medical bulletin as well as a market report and today’s there’s a new entry on the former. It looks like I’m going to have a back operation in the next few weeks. My sciatic nerve has no room to move and while I’m not in pain at the moment (unlike earlier this year) due to two injections in recent months, I have constant tingling and pins and needles down my leg. All conservative approaches have hit the end of the road and the worry is that if I leave it too long I’ll do permanent damage to the nerve. If anyone wants to make a late intervention to help sway me one way or the other in terms of back surgery feel free to do so. I think my mind is made up though as I don’t see an alternative. All a bit scary but all with the aim of getting me 30 more years (minimum) on the golf course and the chance to reach my goal of getting to scratch before the ageing process prevents that!!

The injection of optimism inserted into the limbs of the financial market after last week’s US CPI report showed some signs of fading yesterday although there’s been a recovery in Asia as China continues to support the economy and the interpretation of Biden/Xi meeting yesterday is spun a bit more positively in Asia.

Yields have risen across the Treasury curve to start the week as investors moved to dial back some of their more dovish post-CPI expectations for next year. In part, that was prompted by some pretty hawkish comments from Fed Governor Waller on Sunday night that we mentioned in yesterday’s edition. But that trade was then given further momentum by the New York Fed’s latest Survey of Consumer Expectations, which showed inflation expectations moving higher across all horizons, and echoes the uptick we saw in the University of Michigan’s reading last Friday as well. Consistent with that, our US economist’s composite measure of inflation expectations has increased. They’ve published their latest series in a full update, available here.

Diving into those inflation expectations from yesterday, the New York Fed’s latest survey showed the 1yr expectation moving up half a point to 5.9%, 3yr expectations rising two-tenths to 3.1%, and 5yr expectations up two-tenths as well to 2.4%. To be fair, all those measures are still below their levels as recently as Q2, but the upticks over the last couple of months will raise some fears that the longer inflation remains elevated, the more difficult it’ll be to keep expectations anchored around target levels. For now you would have to say that long-run expectations have held in remarkably well in the face of 40-yr highs in actual inflation. October’s US PPI will be an important release today, especially the health care component that feeds directly into core PCE – the Fed’s preferred gauge.

A notable push back on the slightly more hawkish momentum to start the week were comments as Europe closed from Fed Vice Chair Brainard, who struck a far less hawkish tone than Governor Waller had the previous day. For instance, Brainard said that it would “probably be appropriate soon to move to a slower pace of increases”, which gave further support to the idea the Fed will slow down its hikes to a 50bp pace next month (fully priced now though). That wasn’t too out of line with the rest of Fed speakers since the November meeting, but where the Vice Chair did separate herself was by noting the step down in pace need not be explicitly tied to a higher terminal rate, something Chair Powell argued during his Press Conference, and she did not explicitly rule out interest rate cuts next year, which would be more of a ‘pivot’ rather than the recently communicated ‘pause’ for the Fed. That gave risk assets a bit of support, but it appears she is out of consensus from the rest of the Committee, so the gains were not sustained.

With all said and done, investors ended the day expecting a slightly more aggressive Fed, with the rate priced in by Fed funds futures for end-2023 up +6.2bps to 4.46%. As a result, US Treasury yields rose across the board as trading resumed after Friday’s Veterans’ Day holiday. The 10yr yield was up +4.1bps to 3.85% (3.87% in Asia), and the more policy-sensitive 2yr yield saw an even larger move of +5.7bps to 4.39%. Those moves were driven by real yields, with the 10yr real yield up +8.4bps on the day to 1.49%. As you’ll see from my CoTD yesterday, 10yr US real yields had their second largest fall since the GFC on Thursday (link here). Only the intitial covid related fall in March 2020 beats it.

Against that backdrop, US equities struggled for momentum too, with the S&P 500 (-0.89%) losing ground after its massive +6.52% surge over the previous two sessions. The more cyclical sectors led the declines, and the NASDAQ (-1.12%) lost even more ground on the day. However in Europe there was a much more positive story, with the STOXX 600 up +0.14% to its highest level in over two months, alongside gains for the FTSE 100 (+0.92%), the CAC 40 (+0.22%) and the DAX (+0.62%). This European strength was evident in sovereign bond markets too, where yields on 10yr bunds (-1.5bps), OATs (-1.2bps) and BTPs (-3.0bps) all ended the day lower.

Asian equity markets are mostly trading higher this morning with the Hang Seng (+3.62%) sharply higher lifted by the outperformance of the Hang Seng Tech index (+6.81%) as Chinese listed tech stocks rose significantly. Stocks in mainland China are also up with the CSI (+1.47%) and the Shanghai Composite (+1.27%) extending their previous session gains despite a slew of disappointing economic data. As discussed at the top, the Asian interpretation is that we saw a slight easing of China-US tensions following the Biden-Xi meeting on the sidelines of the G20 summit in Indonesia (more below). Elsewhere, the Nikkei (+0.10%) is modestly higher with the KOSPI (-0.11%) bucking the trend in early trade.

In overnight trading, US stock futures are pointing to a positive start with contracts on the S&P 500 (+0.52%) and the NASDAQ 100 (+0.74%) both rising.

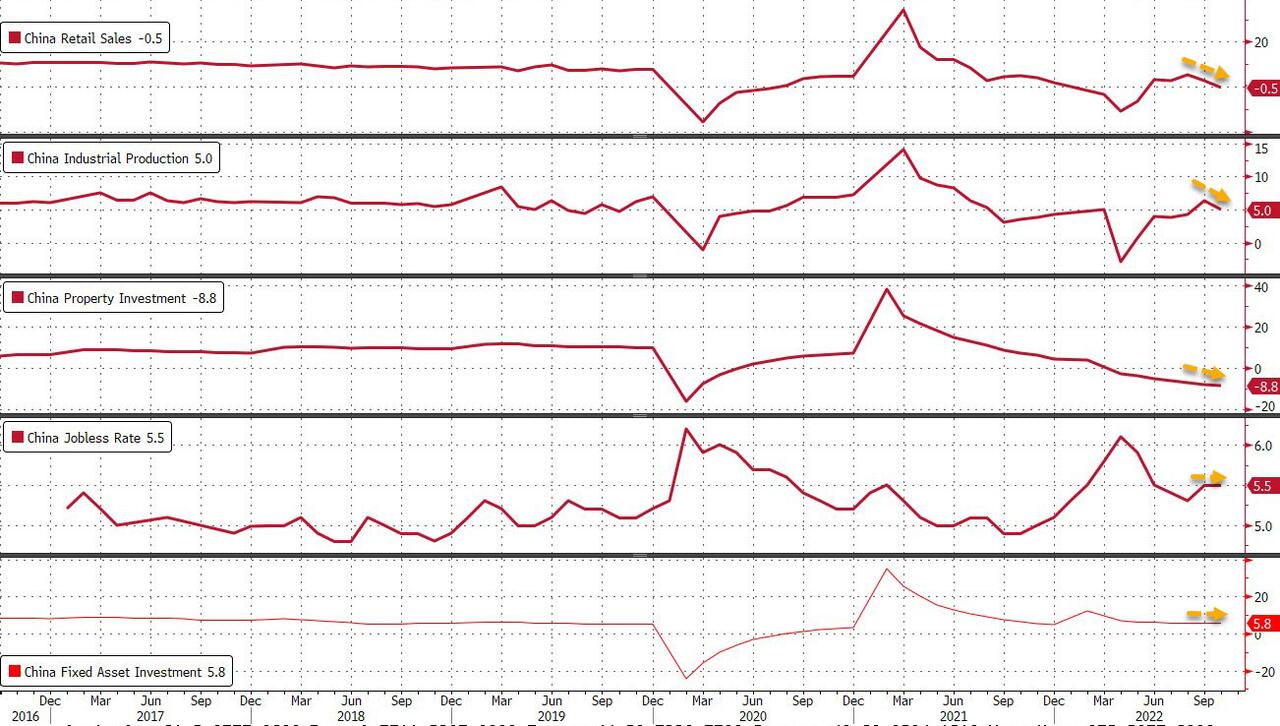

Coming back to China, early morning data revealed that industrial production rose +5.0% y/y in October, lower than the market expected rise of +5.3% and much slower than September’s +6.3% increase indicating a further loss of momentum in the world’s second biggest economy. At the same time, retail sales unexpectedly contracted -0.5% y/y (v/s +0.7% expected), down from +2.5% growth in September as strict Covid restrictions along with a downturn in property markets pushed consumers to tighten their belts. Markets are largely ignoring this data as covid and property restrictions have subsequently been eased so the direction of travel should get more positive from here.

Elsewhere, Japan’s economy unexpectedly shrank for the first time in four quarters as Q3 GDP fell -0.3% q/q (v/s +0.3% expected) compared to an upwardly revised growth of +1.1% in the prior quarter as inflation and the weak yen hit the country.

In the geopolitical sphere, let’s now recap US President Biden and Chinese President Xi’s first meeting in person as the leaders of their respective countries yesterday. That took place on the sidelines of the G20 summit in Indonesia, and the White House said afterwards that US Secretary of State Blinken would visit China to follow up on the discussions, which was taken by many as a positive sign towards de-escalating tensions. However, there were some points of tension, with the White House statement saying that Biden had “raised U.S. objections to the PRC’s coercive and increasingly aggressive actions towards Taiwan, and China’s statement said that “anyone that seeks to split Taiwan from China will be violating the fundamental interests of the Chinese nation”. So something for the hawks and doves but the conclusion might be that the summit beat low expectations coming into it.

Staying on politics, it’s now been a week since the midterm elections and we still don’t know which party will control the House of Representatives following the weekend confirmation that the Democrats took the Senate. It’s looking increasingly likely it will go to the Republicans, who currently have a lead in the vote count across enough of the outstanding districts to win a majority, and NBC’s forecast points to a narrow 220-215 Republican majority based on what we currently have as well. As we go to press, the current tally stands at 217 Republicans and 204 Democrats with Republicans just 1 win away from taking the House.

Tonight however, attention will turn towards the 2024 presidential contest, since former President Trump has said he’ll be making an announcement at 9pm EST, and speculation has centred around a potential 2024 announcement. Normally, the presidential announcements from the top-tier contenders happen around Q1 or Q2 of the year after the midterms. But if today does mark an announcement, the rationale for going early will be to clear the field of other potential contenders, with Trump hoping that the Republican primary is effectively uncontested like normally happens for sitting presidents. As it stands, Trump’s biggest rival for the nomination is widely considered to be Florida Governor Ron DeSantis, who was re-elected Governor last week with lead of almost 20 points over his Democratic opponent. He was seen to be the Republican’s big success story of the night.

The crypto saga continues, but there was some stabilisation in Bitcoin prices, which retreated just -0.57% after bouncing around all day. There’s certainly still more to come on the story as it becomes clear who was exposed to failed exchanges and funds, but Marion Laboure on my team has already contextualised the episode and looks ahead about what it implies in her piece out yesterday. Link here

To the day ahead now, and data releases from the US include October’s PPI reading and the Empire state manufacturing survey for November, while in Europe there’s UK employment data for October and the German ZEW survey for November. Central bank speakers include the Fed’s Harker, Cook, Barr and the ECB’s Elderson. Finally, earnings releases include Walmart and Home Depot.

end

AND NOW NEWSQUAWK (EUROPE/REPORT)

BTPs bolstered, USD slips and US equity futures firmer; Fed speak ahead – Newsquawk US Market Open

TUESDAY, NOV 15, 2022 – 06:45 AM

- European bourses are mixed overall, Euro Stoxx 50 +0.2%, as opening gains scale back after a mostly constructive APAC session.

- Stateside, US futures are firmer across the board with Tech leading after strong APAC tech trade and in wake of Fed’s Brainard, ES +0.7%.

- DXY continues to slip after a pronounced move which occurred prior to the European cash open, currently near sub-106.00 lows to the broad benefit of peers.