MARCH 14/GOLD CLOSED DOWN $4.75 TO $1906.40//SILVER HOWEVER CLOSED UP 9 CENTS TO $21.91//PLATINUM CLOSED DOWN $14.35 TO $989.35 WHEREAS PALLADIUM WAS UP $19.60 TO $1505.75//COVID UPDATES//DR PAUL ALEXANDER//VACCINE IMPACT/SLAY NEWS//UKRAINE VS RUSSIA UPDATES//SILICON VALLEY AND SIGNATURE BANK FAILURE UPDATES// KEY ARTICLES: DR MICHAEL HUDSON AND BRANDON SMITH//SWAMP STORIES FOR YOU TONIGHT//CREDIT SUISSE FALLS ANOTHER 4% AS THEIR CREDIT DEFAULT SWAPS RISE//PROTESTS BY DUTCH FARMERS AGAIN//USA CPI COMES IN AS EXPECTED AT 0.4%//6% Y/Y//

323 C HSBC 222 435 H SCOTIA CAPITAL 43 624 H BOFA SECURITIES 220 657 C MORGAN STANLEY 6 661 C JP MORGAN 83 737 C ADVANTAGE 1 13 880 C CITIGROUP 8 905 C ADM 1 33

TOTAL: 315 315

TOTAL: 9 9 MONTH TO DATE: 3,021

JPMORGAN stopped 0/315 contracts

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR MAR/2023. CONTRACT: 315 NOTICES FOR 31500 OZ or 0.9797 TONNES

total notices so far: 3336 contracts for 333600 oz (10.3764 tonnes)

SILVER NOTICES: 3 NOTICE(S) FILED FOR 15,000 OZ/

total number of notices filed so far this month : 2971 for 14,855,000 oz

END

GLD

WITH GOLD DOWN $4.75

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 11.85 TONNES INTO THE GLD//////(VERY STRANGE..WHERE DID THEY GET ALL OF THAT GOLD/?)

INVENTORY RESTS AT 913.27TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $.09

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.1287 MILLION OZ FROM THE SLV: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 477.592. MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY AN IMPOSSIBLE SIZED 5066 CONTRACTS TO 123,906 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUMONGOUS SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR HUMONGOUS $1.35 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY (THIS IS FAIRY TALES). OUR NEW LOW COMEX OI SILVER WAS SET AT 121,299 MARCH 3/2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $1.35). BUT WERE SUCCESSFUL IN KNOCKING SOME SPEC LONGS AS WE HAD A HUMONGOUS LOSS ON OUR TWO EXCHANGES 3130 CONTRACTS (WITH THE $1.35 GAIN IN PRICE???). WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS( 1936 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.58 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF 40,000 OZ//NEW STANDING: 15.160 MILLION OZ + THE 1.0 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 16.160 MILLION OZ/ //// V) IMPOSSIBLE SIZED COMEX OI LOSS/ STRONG SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –243 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 10 days, total 6936 contracts: OR 34.680 MILLION OZ . (694 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 34.680 MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 34.680 MILLION OZ//INITIAL

RESULT: WE HAD A RIDICULOUSLY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5066 DESPITE OUR $1.35 GAIN IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS SIZED EFP ISSUANCE CONTRACTS: 1936 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAR OF 15.58 MILLION OZ//FIRST DAY NOTICE// FOLLOWED BY TODAY’S 40,000 OZ QUEUE JUMP (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 1.0 MILLION OF EXCHANGE FOR RISK ISSUED EARLY IN MARCH (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 16.160 MILLION OZ .. WE HAVE A HUMONGOUS SIZEDLOSS OF 3130 OI CONTRACTS ON THE TWO EXCHANGES WHICH MAKES ABSOLUTELY NO SENSE!!

WE HAD 3 NOTICE(S) FILED TODAY FOR 15,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY AN IMPOSSIBLE SIZED 1223 CONTRACTS TO 468,037 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED 808 CONTRACTS.

.

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 1223 CONTRACTS) DESPITE OUR $48.85 GAIN IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR MAR. AT 4.9953 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 45,600 OZ (1.418 TONNES) //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London).

YET ALL OF..THIS HAPPENED WITH OUR $48.85 GAIN IN PRICEWITH RESPECT TO FRIDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 6609 OI CONTRACTS (20.556 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7832 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 468,037

IN ESSENCE WE HAVE A GOOD INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6609 CONTRACTS WITH 1223CONTRACTS DECREASED AT THE COMEX AND 7832 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 6609 CONTRACTS OR 20.556 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7831 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (1,223) TOTAL GAIN IN THE TWO EXCHANGES 6609 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR MAR. AT 4.9953 TONNES FOLLOWED BY TODAY’S 45,600 OZ QUEUE JUMP//NEW STANDING 11.676 TONNES // ///3) ZERO LONG LIQUIDATION //4) FAIR SIZED COMEX OPEN INTEREST LOSS// 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

TOTAL EFP CONTRACTS ISSUED: 41,280 CONTRACTS OR 4,128,000 OZ OR 128.39 TONNES IN 10 TRADING DAY(S) AND THUS AVERAGING: 4128 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10TRADING DAY(S) IN TONNES 128.39 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 128.39/3550 x 100% TONNES 3.60% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 128.39 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY AN IMPOSSIBLE SIZED 5066 CONTRACTS OI TO 123,906 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A RECORD LOW OF 121,299 CONTRACTS MARCH 3/2023.

EFP ISSUANCE 1936 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1936 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1936 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 5066CONTRACTS AND ADD TO THE 1936 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUMONGOUS LOSS OF 3130 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES //17.65 MILLION OZ

OCCURRED DESPITE OUR $1.35 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED DOWN 23.38 PTS OR 0.72% //Hang Seng CLOSED DOWN 448.01 PTS OR % 2.27 /The Nikkei closed DOWN 610.92% PTS OR 2.19% //Australia’s all ordinaries CLOSED DOWN 1.50% /Chinese yuan (ONSHORE) closed DOWN 6.8765//OFFSHORE CHINESE YUAN DOWN TO 6.8746// /Oil DOWN TO 73.49 dollars per barrel for WTI and BRENT AT 79.43 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A RIDICULOUSLY SIZED 1223 CONTRACTS DOWN TO 468,037 WITH OUR HUMONGOUS GAIN IN PRICE OF $48.85 ON MONDAY

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAR… THE CME REPORTS THAT THE BANKERS ISSUED A VERY STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 7832 EFP CONTRACTS WERE ISSUED: : APRIL 7832 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 7832 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 6609 CONTRACTS IN THAT 7832LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 1,223 CONTRACTS..AND THIS GOOD SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR HUMONGOUS GAIN IN PRICE OF $48.85. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAR (11.673) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 11.673 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $48.85) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR GOOD SIZED GAIN OF 6,609 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 20.556 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAR. (4.9953 TONNES) FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 45,500 OZ (1.415 TONNES)… ALL OF THIS WAS ACCOMPLISHED WITH OUR HUMONGOUS GAIN IN PRICE TO THE TUNE OF $48.85

WE HAD +808 CONTRACTS ADDED TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT(FIGURE THAT ONE OUT!!)

NET GAIN ON THE TWO EXCHANGES 6609 CONTRACTS OR 660900 OZ OR 20.556 TONNES

Total monthly oz gold served (contracts) so far this month

3336 notices 333,600 10.3764 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 1

i) out of Brinks 257.200 oz (8kilobars)

total withdrawals: NIL oz

in tonnes: 0.007 tonnes

Adjustments; 1

dealer to customer//JPMorgan 24,066.95 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 732 contracts having GAINED 446 contracts. We had 9 notices filed on MONDAY so we

gained A HUGE 455 contracts or an additional 45,500 oz will stand for metal at the comex

April lost A HUGE 30,919???? contracts down to 222,818 contracts (UNUSUAL FOR THAT MANY TO LEAVE THIS EARLY//SPREADER??)

May GAINED 93 contracts to stand at 258

We had 315 notice(s) filed today for 31,500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 83 notices were issued from their client or customer account. The total of all issuance by all participants equate to 315 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR. /2023. contract month,

we take the total number of notices filed so far for the month (3336 x 100 oz ), to which we add the difference between the open interest for the front month of (MAR. 732 CONTRACTS) minus the number of notices served upon today 315 x 100 oz per contract equals 375,300 OZ OR 11.673 TONNES the number of TONNES standing in this active month of MARCH.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (3336 x 100 oz+ 732 OI for the front month minus the number of notices served upon today (315)x 100 oz} which equals 375,300 oz standing OR 11.673 TONNES in this active delivery month of MARCH..

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 2971 x 5,000 oz = 14,855,000 oz

to which we add the difference between the open interest for the front month of MAR(64) and the number of notices served upon today 3 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2023 contract month: 2971 (notices served so far) x 5000 oz + OI for the front month of MAR (64) – number of notices served upon today (3) x 500 oz of silver standing for the MAR. contract month equates 15.160 million oz +the 1.0 million oz of exchange for risk//new total standing 16.160 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 913.27 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 477.592 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

SVB Lessons: If You Can’t Hold It, It’s Not Really Yours

The failure of Silicon Valley Bank and Signature Bank reminds us of a very important truth — if you can’t hold it in your hand, you don’t really own it…

That’s why it’s wise to hold at least some of your wealth in hard assets like gold and silver that are in your direct possession or at least stored in a secure, allocated, segregated, and insured storage facility.

The FDIC insures bank deposits up to $250,000. If you have more than that in a financial institution, you could lose everything above that limit if a bank fails.

Depositors at SVB and Signature Bank lucked out. The government has made provisions to cover uninsured deposits. But there’s no guarantee that will happen when the next bank goes under.

And even if you don’t have more than $250,000 in the bank, you could easily find yourself locked out of your account. Just last week, a computer glitch caused money in some Wells Fargo accounts to disappear.

Most people assume “that can’t happen here” in the US. But as we saw over last week, the US banking system is vulnerable to collapse.

The dirty little secret is US banks don’t hold your money in their vaults. They loan it out to other people. In the US fractional reserve banking system, financial institutions only have enough cash on hand to cover a fraction of their deposits. If too many people show up at the bank to demand their money at the same time, the bank will not have enough funds available to cover all of the withdrawals. This is why bank runs are so dangerous. They can cause a bank to go under.

When you put your money in a bank, you create “counterparty risk.” In a nutshell, it is the risk that a person or institution on the other side of a transaction might not fulfill its obligation – i.e. the bank doesn’t have the money to return your deposit.

Even if you managed to withdraw all of ‘your’ money in physical cash from banks tomorrow and put it in your well-guarded safe at home, you are still a creditor to the Fed & Treasury. You still hold IOU paper with risk of loss.”

In fact, you’ve suffered significant losses in the value of your dollars over the last two years thanks to rampant price inflation.

Gold and silver carry no counterparty risk. They are tangible assets that you can hold in your hand. They can be bought and sold all over the world. Their value is recognized globally. While the price of gold or silver may fall, it will never fall to zero. Precious metals can’t default on their payments, they can’t commit fraud, and they can’t go bankrupt.

Of course, it’s impossible to lower risk to zero. If you store your gold and silver at home, you could get robbed. If you vault your precious metals, it is possible for that third-party storage entity to commit fraud, get robbed, or be destroyed by an act of God. Nevertheless, the counterparty risk introduced by storing your gold and silver is relatively low compared to the risk of a bank failure or rapidly depreciating fiat currency — especially in the current financial situation.

END

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

Two Fed-Supervised Banks Blew Up Last Week; Two More Dropped Over 40 Percent Yesterday; and the Fed Wants to Investigate Itself — Again

By Pam Martens and Russ Martens: March 14, 2023 ~

Last Wednesday, federally-insured Silvergate Bank announced that it was closing shop and liquidating. Its parent’s stock price (Silvergate Capital, ticker SI) had lost over 90 percent of its value over the prior year; it was under a Justice Department investigation for how it moved money for crypto-kingpin Sam Bankman-Fried’s house of frauds; and its depositors were fleeing. Oh – and by the way – its primary regulator was the Federal Reserve Bank of San Francisco.

Last Friday, California state regulators closed Silicon Valley Bank and the Federal Deposit Insurance Corporation (FDIC) became the receiver. Its stock price had lost over 80 percent of its market value over the prior year; $150 billion of its $175 billion in deposits were uninsured, either because they exceeded the $250,000 FDIC cap and/or they were foreign deposits. The bank was effectively operating as a Wall Street IPO pipeline in drag as a federally-insured bank. The Federal Home Loan Bank of San Francisco had quietly been bailing it out – to the tune of $15 billion. Oh – and by the way – its primary regulator was the Federal Reserve Bank of San Francisco. And while all of this hubris was occurring, the CEO of Silicon Valley Bank, Gregory Becker, was sitting on the Board of Directors of his regulator, the Federal Reserve Bank of San Francisco.

Let’s pause right here for a moment. This is far from the first time that the CEO of a questionable bank was sitting on the Board of a Federal Reserve Bank. As Citigroup CEO, Sandy Weill, was burying the bank under off balance sheet vehicles that would eventually crater the bank in 2008; send its stock price to 99 cents in early 2009; and require the largest bank bailout by the Fed in U.S. history, Weill was also serving on the Board of Directors of the New York Fed. And while Jamie Dimon was CEO of JPMorgan Chase and it was losing what eventually grew to $6.2 billion of bank depositors’ money in wild derivative bets in London, Dimon was also sitting on the Board of the New York Fed. Even when there was a big public uproar over Dimon’s presence on the New York Fed Board as the London Whale derivatives scandal came to light, Dimon remained in place.

Oh, and by the way, the Fed member banks in each of the 12 Federal Reserve Districts that can choose to be regulated by the Fed, literally own their regulator. That’s right, they own the stock in their regional Fed bank, which is a private institution, unlike the Federal Reserve in Washington, D.C. which is an “independent” federal agency. (See, for example, These Are the Banks that Own the New York Fed and Its Money Button.)

As the first crypto-related bank failure occurred on Wednesday (Silvergate Bank) and the second largest bank failure in U.S. history occurred on Friday (Silicon Valley Bank) and the third largest bank failure in U.S. history occurred on Sunday (Signature Bank), President Joe Biden attempted yesterday to reassure the public, stating that “Americans can rest assured that our banking system is safe.”

But by the close of the stock market yesterday, two more banks whose primary regulator was a Fed regional bank had lost more than 40 percent of their market value – in one day’s trading session. (That doesn’t sound to us like things are under control.) Western Alliance Bancorp (ticker WAL), which is also supervised by the San Francisco Fed, lost 47 percent of its market value by the closing bell. Metropolitan Commercial Bank (bank holding company ticker is MCB) lost 43.78 percent of its market value yesterday. It is supervised by the New York Fed.

Adding to the ongoing arrogance of the Fed, its Chairman, Jerome Powell, released a statement two minutes after the market closed yesterday, stating that “The events surrounding Silicon Valley Bank demand a thorough, transparent, and swift review…” So, once again, it’s decided to investigate itself. The Fed’s Vice Chairman for Supervision, Michael Barr, will oversee the investigation.

The last time the Fed decided to investigate itself was over its unprecedented trading scandal where various Fed officials engaged in highly inappropriate trading during the pandemic when Fed officials had insider knowledge of bailout actions the Fed planned to take to stem the stock market rout. Powell referred the investigation into that matter to the Fed’s Inspector General – who reports to (wait for it) the Federal Reserve Board, which is headed by Powell. The first news of that trading scandal came to light in early September 2021. It’s now 19 months later and the public has yet to hear a peep about the results of any investigation into the worst actor in the trading scandal, former Dallas Fed President Robert Kaplan. (See our report: Robert Kaplan Was Trading Like a Hedge Fund Kingpin for Five Years while President of the Dallas Fed; a Dozen Legal Safeguards Failed to Stop Him.)

Against this backdrop of Fed hubris, the PBS program, Frontline, will tonight premiere a two-hour documentary on the Fed’s controversial monetary policies that have led us to this dangerous point in time. The Age of Easy Money comes from the award-winning producers James Jacoby and Anya Bourg.

In the documentary, economist Nouriel Roubini says “We lived in a bubble, in a dream, and this dream and bubble is bursting.” Jim Millstein, Co-Chairman of Guggenheim Securities, shares this: “I’ve never been more worried in the 42 years that I’ve been a professional. The Fed is absolutely right to try and get it [inflation] under control by raising interest rates in slowing economic activity. But the most highly levered players in our economy are going to come under real stress whether that’s households or businesses or governments, as interest costs rise.”

Actually, what’s blowing up right at this moment and scaring the daylights out of the American people are the U.S. banks (some of which were supervised by the Fed) that are sitting on a cumulative $620 billion of unrealized losses.

According to a February 28 statement from the Federal Deposit Insurance Corporation on the condition of federally- insured U.S. banks and savings associations, “Unrealized losses on securities totaled $620.4 billion in the fourth quarter, down 10.1 percent from the prior quarter. Unrealized losses on held–to–maturity securities totaled $340.9 billion in the fourth quarter. Unrealized losses on available–for–sale securities totaled $279.5 billion in the fourth quarter.”

Age of Easy Money will air tonight on PBS stations (check local listings) and on Frontline’s YouTube channel at 9 p.m. eastern time and 8 p.m. central time

end

3. CHRIS POWELL//GATA AND OTHER IMPORTANT GOLD COMMENTARIES

Total unrealized losses at uSA banks total $620 billion

(CNN New York/GATA)

U.S. banks have unrealized losses of $620 billion, FDIC says

Submitted by admin on Mon, 2023-03-13 11:54Section: Daily Dispatches

By Nicole Goodkind CNN, New York Sunday, March 12, 2023

Silicon Valley Bank’s collapse last week sent tingles of panic down investors’ spines as it highlighted a larger problem across the banking sector: The widening gap between the value large lenders place on the bonds they hold and what they’re actually worth on the market.

SVB’s downfall was tied, in part, to the plunge in the value of bonds it acquired during boom times, when it had a lot of customer deposits coming in and needed somewhere to park the cash

But SVB isn’t the only institution with that issue. U.S. banks were sitting on $620 billion in unrealized losses — assets that have decreased in price but haven’t been sold yet– at the end of 2022, according to the Federal Deposit Insurance Corp.

What’s happening: Back when interest rates were near zero, U.S. banks scooped up lots of Treasuries and bonds. Now, as the Federal Reserve hikes rates to fight inflation, those bonds have declined in value.

When interest rates rise, newly issued bonds start paying higher rates to investors, which makes the older bonds with lower rates less attractive and less valuable.

The result is that most banks have some amount of unrealized losses on their books.

“The current interest rate environment has had dramatic effects on the profitability and risk profile of banks’ funding and investment strategies,” said FDIC Chairman Martin Gruenberg in prepared remarks at the Institute of International Bankers last week. …

For sure: USA intervention encourages bad investor behaviour. It always happens

(Reuters/GATA)

Moral hazard is concern as U.S. intervenes to save big banks

Submitted by admin on Mon, 2023-03-13 12:03Section: Daily Dispatches

By Scott Murdoch and Carolina Mandl Reuters Monday, March 13, 2023

U.S. regulators may have stemmed a banking crisis by guaranteeing deposits of collapsed Silicon Valley Bank (SVB), but some experts warn that the move has encouraged bad investor behavior.

Following a weekend of discussions over the future of SVB owner SVB Financial Group, banking regulators unveiled emergency funding plans for the bank.

Billionaire hedge fund manager Bill Ackman wrote on Twitter that if authorities had not intervened, “we would have had a 1930s bank run continuing first thing Monday causing enormous economic damage and hardship to millions.”

“More banks will likely fail despite the intervention, but we now have a clear roadmap for how the gov’t will manage them.”

Yet by guaranteeing that depositors would lose no money, authorities have again raised the question of moral hazard — removal of people’s incentive to guard against financial risk.

“This is a bailout and a major change of the way in which the U.S. system was built and its incentives,” said Nicolas Veron, senior fellow at the Peterson Institute for International Economics in Washington. “The cost will be passed on to everyone who uses banking services.” …

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.8765

OFFSHORE YUAN: 6.8746

SHANGHAI CLOSED DOWN 23.38 PTS OR 0.72%

HANG SENG CLOSED DOWN 448.01 PTS OR 2.27 %

2. Nikkei closed DOWN 610.92 PTS OR 2.19%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 103.31 Euro RISES TO 1.0724 UP 9 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.262!!(Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 134.06/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.343%***/Italian 10 Yr bond yield RISES to 4.206%*** /SPAIN 10 YR BOND YIELD RISES TO 3.423…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.265//

3j Gold at $1911.00//silver at: 21.70 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 26/100 roubles/dollar; ROUBLE AT 75.26//

3m oil into the 73 dollar handle for WTI and 79 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 134.06/10 YEAR YIELD AFTER BREAKING .54%, RISES TO .262% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9109–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9771well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.634% UP 12 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.734 UP 8 BASIS PTS//INVERTED TO THE 10 YEAR!!

USA 2 YR BOND YIELD: 4.2295 UP 20 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,98…

GREAT BRITAIN/10 YEAR YIELD: 3.4995% UP 13 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Rise, Bank Stocks Soar On Report Private Equity Firms Circle SVB Loan Book

TUESDAY, MAR 14, 2023 – 08:03 AM

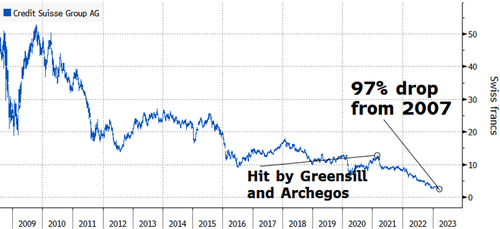

Market mood recovered from yesterday’s bank rout as contagion fears from the collapse of SIVB and SBNY appear to have subsided for the time being, despite a hiccup earlier in the session when Credit Suisse stock hit a new record low after the Swiss bank said it had identified material weaknesses in its internal control over financial reporting as of December 31, 2022 and 2021. The mood was lifted by a Bloomberg report that Apollo Global and Blackstone have expressed interest in snapping up a book of loans held by Silicon Valley Bank, suggesting the collapsed bank contagion may be contained after bigger buyers step in.

S&P futures were up 0.8% to 3,920 and Nasdaq 100 futures rise 0.7% ahead of US CPI later today (full CPI preview here). Major US banks were broadly higher in the premarket as regional lender First Republic Bank surged 39% after plunging on Monday. This has led to a rebound in short end yields with US two-year up 27bps on the day to 4.22% (still down around 85bps from last week’s peak). Plunging rates gripped Wall Street’s attention yesterday, when the yield dropped more than a half-percentage point in the biggest move since the 1980s. The 10-year yield rose three basis points to 3.60%, while a gauge of the dollar snapped three days of losses.

In premarket trading, financial stocks traded higher, alongside the broader market as banks rally off a historically bad Monday; the mood was lifted by the aforementioned BBG report that Apollo and Blackstone, two of the world’s largest alternative asset managers, are among investors looking to buy pieces of Silicon Valley Bank. First Republic Bank jumped 44% in premarket trading, while PacWest Bancorp rose 34% and Western Alliance Bancorp added more than 20%. Bigger lenders were also in the green, with Bank of America Corp advancing 3% and Citigroup Inc. adding 1.3%. Here are some other notable premarket movers:

United Airlines shares drop 6.1% after the carrier slashed its 1Q outlook and now expects to post a loss for the period. Analysts said that the revised guidance was due to the change in timing for pilot contract accrual, though note other aspects of the 2023 outlook remain unchanged.

Uber and Lyft advanced after a California appeals court upheld the current law classifying gig workers as independent contractors instead of employees. Analysts noted that this would allow the companies to avoid any negative impact to their business. Uber rose as much as 5.8% and Lyft jumped 6.4%

Cryptocurrency-exposed stocks rose after Bitcoin extends its gains as US authorities stepped in to stem spreading concerns about the health of the nation’s financial system after Silicon Valley Bank’s collapse. Bitfarms (BITF US) +8.5%, Stronghold Digital (SDIG US) +8.5%, Marathon Digital (MARA US) +2.1%, Riot Platforms (RIOT US) +1.3%, Coinbase (COIN US) +0.6%

Momentive Global rose 18% to $9.13 per share, after the SurveyMonkey owner said it had agreed to be acquired by a consortium led by Symphony Technology Group for $9.46/share cash.

Gitlab fell 33% after the software company gave a full-year revenue forecast that was weaker than expected. Analysts note that the management’s outlook seems conservative amid a tough macro environment.

Amylyx Pharmaceuticals the maker of a drug for amyotrophic lateral sclerosis, rose 20% in after-market after posting 4Q revenue that easily topped estimates.

Watch Apple stock as Evercore ISI said it deserves to trade at a premium valuation compared to its big tech peers, citing the iPhone maker’s higher operating efficiency, large share repurchase program and consistent execution.

The S&P 500 closed Monday down 0.2%, after bouncing between gains and losses amid a rout in bank shares while the policy-sensitive Nasdaq climbed 0.8%, the most in over a week. The fallout from SVB’s collapse prompted President Joe Biden to promise stronger regulation of US lenders, while reassuring depositors that their money is safe.

Treasuries had been whipsawed in recent days — with a measure of volatility climbing to the highest since 2009 — and banking shares plunged as the collapse of Silicon Valley Bank and two other US lenders prompted wagers the Federal Reserve will pause its hiking cycle and even cut interest rates to stabilize the financial system. But a hot inflation reading later today could muddy that outlook and spark a fresh wave of volatility in fixed-income markets.

“A policy mistake is hands down the biggest risk in the market,” Mary Manning, global portfolio manager for Alphinity Investment Management, said on Bloomberg Television. “Controlling inflation but also addressing the fact there is some instability in the banking system is difficult.”

As BBG notes, swap contracts referencing Fed policy meetings slashed the odds of any increase to less than one-in-two. Meanwhile, contracts for the rest of 2023 suggest that the Fed could cut rates by almost a full percentage point from the peak in May before the year is out. Goldman economists as well as asset managers from PIMCO said the Fed could take a breather on the policy rate following the collapse of SVB. Nomura economists took it one step further, saying the Fed could cut its target rate next week.

“Niggling concerns that mild recessions could be on the way have been replaced by a wall of worry about runs on smaller banks,” as well as the risk that larger ones may turn more risk averse to lending, according to Susannah Streeter, head of money and markets at Hargreaves Lansdown. Inflation data will be closely watched “as another hot reading will reinforce expectations that a rate rise, albeit smaller, will be on the cards next week,” she said.

Then there is CPI to look forward to: traders are looking to the US consumer price index report later in the day for cues that may trigger further shifts in the outlook for monetary policy. Our full CPI preview can be found here.

The bank selloff “certainly creates a headwind for aggressive Fed action, if any action,” said Gary Schlossberg, a senior economist at Wells Fargo. “But there is that very important data coming out which may not ease concerns over inflation. It means the Fed has even more of a balancing act.”

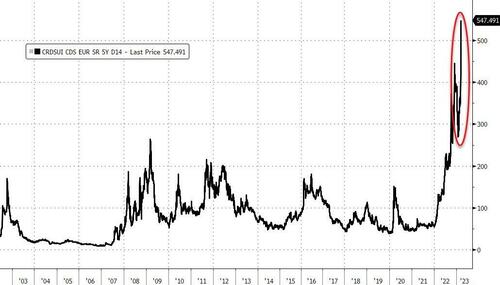

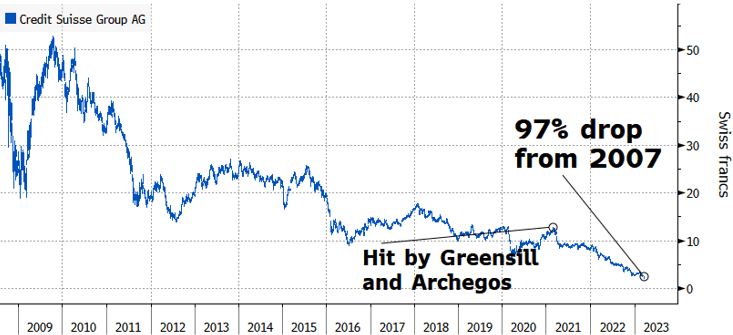

European stocks are also ahead, albeit slightly, with the Stoxx 600 adding 0.2%. European real estate shares jump the most in a month on bets central banks will slow the pace of interest-rate hikes, with the Stoxx 600 Real Estate subindex outpacing all others; elsewhere, utilities and industrials were among the best-performing sectors while the FTSE 100 underperforms, down 0.2%. Credit Suisse shares slide to new record lows, shedding as much as 5.6%, after the lender said it had found “material weaknesses” in its reporting and control procedures for the past years. Here are the most notable European movers:

Generali shares rise as much as 2.5% and are the top performers on the FTSE MIB index, after the Italian insurer reported full-year operating results that were ahead of estimates

Icade shares jump as much as 10%, their biggest gain since November 2020, after the real estate investment trust entered a pact with Primonial REIM to sell its stake in Icade Santé

Wojas surge as much as 33% to a record high after the Polish footwear producer said it had received a 138.6m zloty contract to make military shoes for the country’s army.

Close Brothers shares fall as much as 7.5% after the UK financial services firm posted 1H pretax operating profit that missed the average analyst estimate

PolyPeptide falls as much as 22% to a record low, after the biotech reported full- year results that were once again weaker than expected even after two profit warnings, according to ZKB

TP ICAP falls as much as 8.9% after dark pool unit Liquidnet saw “subdued” block trading activity last year, amid a broader equity-market rout, according to the firm’s results

Fraport shares fall as much as 7%. Warburg notes free cash flow levels are still “deep in negative territory,” even as the German airport operator posted a good set of FY results

Earlier in the session, shares of Asian financial firms decline after Treasury yields dropped and US bank stocks slid amid continued concerns related to bank failures. The MSCI Asia Pacific Financials Index falls as much as 2.7% to the lowest since Nov. 29. Investors questioned whether the US government’s rescue plan for the banking system will prevent more fallout from SVB’s collapse. The KBW Bank Index dropped nearly 12% Monday, the most since March 2020. The 10-year Treasury yield shed about 13 basis points to 3.57%; two-year yields plunged 61 bps

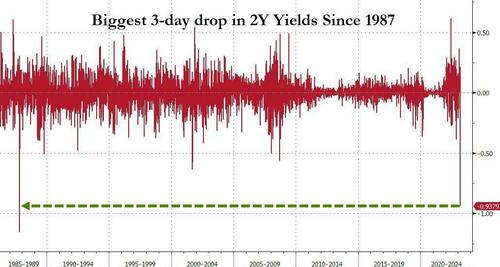

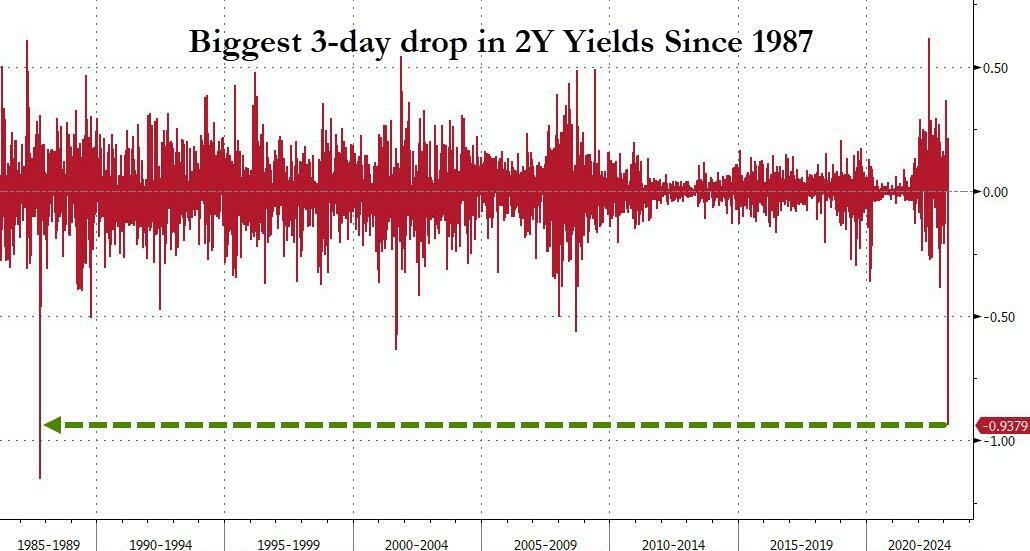

Japanese stocks fell for a third day as investors continued to assess the fallout from the collapse of Silicon Valley Bank and rethink expectations for Federal Reserve monetary policy. The Topix Index fell 2.7% to 1,947.54 as of the market close in Tokyo, while the Nikkei 225 declined 2.2% to 27,222.04. The yen weakened slightly after strengthening 1.4% Monday to 133.21 per dollar. Mitsubishi UFJ Financial Group Inc. contributed the most to the Topix’s decline, decreasing 8.6%. Out of 2,159 stocks in the index, 66 rose and 2,081 fell, while 12 were unchanged. The Topix’s gauge for banks and insurers dragged the broader index down, both tumbling at least 6%, as the SVB trouble has driven investor attention to the heavy investment in US bonds by Japan’s lenders. The uncertain sentiment toward financial institutions also set off a plunge in bond yields in the US and Japan. The US two-year Treasury yield dropped on Monday, logging the biggest three-day retreat since Black Monday of October 1987, as market participants continued to flee US bank shares even after US regulators announced a rescue plan Sunday evening. Japan’s five-year yield also tumbled to lowest since Dec. 2 earlier today. Bond Yields’ Plunge Is Biggest Since Volcker Era on Bank Worries “News around US banks had a major impact creating the ‘flight to safety’ sentiment,” said Mamoru Shimode, chief strategist at Resona Asset Management. “Investors are leveraging and taking out loans, and their money is connected to the financial system, so they are reducing their positions due to a sense of uncertainty.”

South Korea’s Kospi dropped 2.6%, the most since Sept. 26, as foreign investors sell equities in Kospi futures and cash markets amid worries about repercussions from the SVB crisis. “Emerging markets are vulnerable every time there are worries about financial risks in developed markets,” Seo Jung-Hun, an analyst at Samsung Securities said by phone “It appears that foreign investors are hedging their risks through South Korea” by heavily selling Kospi 200 futures. Foreigners cut 1.4 trillion won worth of futures in the Kospi 200 Index, the most since August 2021, while selling net 638 billion won in the Kospi cash markets

In Australia, the S&P/ASX 200 index fell 1.4% to 7,008.90, its lowest close since Jan. 3. The benchmark extended losses to a third day, as all sectors declined. Equities across Asia fell, led by weakness in financial stocks as the collapse of Silicon Valley Bank continued to reverberate across global markets. In New Zealand, the S&P/NZX 50 index fell 0.7% to 11,595.47

In India, major equity indexes plunged for a fourth consecutive session as most Asian markets extended their declines, triggered by the continued selloff in financials. Indian software makers were the worst performers on worries over the banking sector in the US, their biggest revenue generator. The S&P BSE Sensex fell 0.6% to 57,900.19 in Mumbai, while the NSE Nifty 50 Index declined by a similar measure as the guages come within 2% of entering a so-called correction from their record peaks in early December. Asia’s benchmark stock index erased all of its gains for the year as financials extended the rout following the implosion of Silicon Valley Bank. “Markets are likely to remain under pressure in the near term,” Siddhartha Khemka, head of retail research at Mumbai-based Motilal Oswal Financial Services said. US inflation data to be released later Tuesday will be a key factor to watch, he added. Tata Consultancy Services contributed the most to the Sensex’s decline, decreasing 2%. Out of 30 shares in the Sensex index, 7 rose and 23 fell

In FX, a gauge of the greenback rebounded from a three-week low as Treasury yields rose before the release of US inflation data. The Japanese yen was the weakest of the G-10 currencies, while the Dollar Index adds 0.2%. Traders may take their next cue from US inflation data to gauge if the Federal Reserve will halt its tightening campaign to limit the fallout from higher interest rates

In rates, Treasuries are cheaper across front-end and belly of the curve, unwinding a portion of Monday’s aggressive bull-steepening rally. Long-end yields slightly richer on the day, re-flattening 2s10s and 5s30s spreads ahead of February inflation data, Tuesday’s main calendar event. Yields cheaper by as much as 24bp across front-end of the curve with 2s10s, 5s30s spreads flatter by ~21bp and ~10bp on the day; 10-year yields around 3.59%, cheaper by ~2bp vs Monday’s close, with bunds and gilts lagging by 7bp and 6bp in the sector. Early gains in Treasuries during Asia session were spurred by report that Credit Suisse Group AG said it found “material weaknesses” in its reporting and control procedures for the past two years. UK and German two-year yields rise 12bps and 10bps respectively. Ahead of CPI, Fed-dated OIS price in around 19bp of rate-hike premium for the March policy meeting, up from 13bp at Monday’s close.

In commodities, oil extended a decline ahead of the inflation data with WTI futures declining down 2.7% to trade near $72.80. Bitcoin rises 1.0% while spot was gold down 0.6% after rising in the three previous sessions as traders turned to haven assets.

To the day ahead now, and data releases include the US CPI release for February, the NFIB small business optimism index for February and the UK unemployment rate for January. Otherwise, central bank speakers include Fed Governor Bowman.

Market Snapshot

S&P 500 futures up 0.4% to 3,873.50

MXAP down 2.2% to 155.29

MXAPJ down 1.7% to 500.30

Nikkei down 2.2% to 27,222.04

Topix down 2.7% to 1,947.54

Hang Seng Index down 2.3% to 19,247.96

Shanghai Composite down 0.7% to 3,245.31

Sensex down 0.7% to 57,817.37

Australia S&P/ASX 200 down 1.4% to 7,008.88

Kospi down 2.6% to 2,348.97

STOXX Europe 600 little changed at 443.15

German 10Y yield little changed at 2.26%

Euro down 0.4% to $1.0693

Brent Futures down 1.5% to $79.58/bbl

Brent Futures down 1.5% to $79.56/bbl

Gold spot down 0.4% to $1,906.05

U.S. Dollar Index up 0.36% to 103.97

Top Overnight News

China said its embassy in Washington would once again permit foreign tourists to visit the country, the latest example of Beijing lifting its COVID restrictions. WSJ

Just 1 week ago it would have been hard to imagine anyone asking if the CPI print even matters. Oh how quickly things change. This makes me believe risk is skewed to the downside post CPI print. Unless we get a shockingly hot number mkt will remain more focused on unfolding banks drama ( a soft print will be disregarded as not relevant). For headline print GIR look for +.4% MoM ( vs +.4% cons and +.5% prior) and +6.08% YoY (vs +6% cons and +6.4% prior). For core MoM GIR looking for +.45% (vs +.4% consensus and +.4% prior) and YoY of +5.56% (vs 5.5% cons and 5.6% prior). GS GBM

Gov. Ron DeSantis of Florida has sharply broken with Republicans who are determined to defend Ukraine against Russia’s invasion, saying in a statement made public on Monday night that protecting the European nation’s borders is not a vital U.S. interest and that policymakers should instead focus attention at home. NYT

U.S. regulators are likely to let emergency measures announced Sunday to shore up investor confidence in the banking sector sink in and increase scrutiny of the industry before intervening with any further steps, regulatory experts said. RTRS

Biden was apparently “highly skeptical” of intervening in the bank industry over the weekend but was finally brought on board by fears about contagion. WaPo

FDIC is concerned that it is now expected to guarantee all depositors every time a bank fails, something it is not designed to do. Politico

The FHLB system, a key source of cash for regional lenders, raised $88.7 billion through the sale of short-term notes, according to people with knowledge of the matter, more than the $64 billion initially planned. BBG

Moody’s placed First Republic Bank, Western Alliance Bancorp., Intrust Financial Corp., UMB Financial Corp., Zions Bancorp. and Comerica Inc. on review for downgrade, the latest sign of concern over the health of regional financial firms following the collapse of Silicon Valley Bank.

The DOJ is probing last year’s collapse of the TerraUSD stablecoin, raising the risk of criminal charges against its fugitive creator Do Kwon, the WSJ reported. Separately, US prosecutors are looking at Telegram chats among employees at Jump, Jane Street and the now-bankrupt Alameda about a potential bailout of the TerraUSD project, and whether market manipulation was involved, a person familiar said. BBG

One year after the Federal Reserve started frantically raising interest rates, the collapse of Silicon Valley Bank answered what had become perhaps the hottest question on Wall Street: When is something going to break? BBG

Credit Suisse says it has identified material weaknesses in its internal control over financial reporting as of December 31, 2022 and 2021, according to the annual report: BBG

Some of the world’s top money managers are sitting on a windfall after the collapse of Silicon Valley Bank spurred the biggest rally in US Treasuries since the early 1980s: BBG

A more detailed look at global markets courtesy of Newqsuawk

Asia-Pac stocks declined amid a continuation of the selling in financials and with risk appetite constricted amid the fallout from the recent US bank collapses. ASX 200 spent most of the session beneath the 7,000 level with the index pressured by substantial losses in nearly all sectors and amid headwinds from weak data releases in which Westpac consumer sentiment remained near historic lows and NAB business surveys deteriorated. Nikkei 225 slumped due to heavy losses in financial stocks which occupied the list of the 10 worst performers, while the Tokyo Stock Exchange banking index suffered its worst day in over three years. Hang Seng and Shanghai Comp. retreated albeit with less aggressive selling in the mainland on reopening news as China is to resume the issuance of all types of visas for foreigners from March 15th.

Top Asian News

US President Biden said he will talk to Chinese President Xi soon but didn’t specify when. Furthermore, National Security Adviser Sullivan said President Biden anticipates a call opportunity with Chinese President Xi once China’s government returns to work after the NPC, while Sullivan added the US had communicated with China over the AUKUS submarine pact and China’s military build-up.

EU seeks new controls to limit China acquiring high-tech and is exploring ways to police how European companies invest in production facilities overseas, according to FT.

The Great Hiking Cycle Is Seen as Done as Yields Drop Below Cash

SVB Crisis Puts Focus on Chinese Tech IPOs in the US: ECM Watch

China Assets Stand Out as Oasis of Calm Amid SVB Fallout

Germany, Brazil Plan High-Level Meetings as Ties Strengthen

Japan Yield Falls Past Previous BOJ Ceiling as US Hike Bets Ease

Global Financial Stocks Lose $465 Billion as SVB Fallout Spreads

European bourses are posting tentative gains, Euro Stoxx 50 +0.2%, as the risk tone remains fragile given financial stability concerns. Banking names in Europe remain softer, with Credit Suisse lagging after finding material weakness in its 2021/22 financial reporting; for the sector more broadly, GS highlights there is a limited risk of direct contagion to Europe. Stateside, futures are modestly firmer but have been unable to claw back any of Monday’s marked downside, ES +0.4%, ahead of February’s CPI. CATL’s (3007540 CH) at least USD 5bln Swiss IPO is said to be delayed amid regulatory concern, according to Reuters sources; no new timetable for Swiss listing.

Top European News

UK PM Sunak invited US President Biden to visit Northern Ireland for the anniversary of the Good Friday Agreement, while President Biden said that he intends to go to Northern Ireland

UK Chancellor Hunt is to set out plans for 12 new investment zones in the Budget to “supercharge” growth in hi-tech industries, while the scheme is to be backed by GBP 80mln of investment over five years in each of the new high-growth zones, according to Sky News.

Germany has reportedly made last-minute demands on the reform of EU fiscal rules, according to Bloomberg, casting doubts on a draft proposal agreed by EU members. Follows reports that EU Finance Ministers are to discuss the Growth and Stability Pact on 14th March, draft conclusions show general support for the switch from a one-rule-fits-all approach to debt reduction to multi-year plans tailored to each nation, via Politico; Germany said to seek to ensure nations bring down debt by a common quantitative benchmark/target.

SVB/Bank Bailout update

Top Senate and top House Democrats said Congress will be looking closely at the causes behind the run on SVB and other banks, as well as how a similar crisis can be prevented in the future.

Silicon Valley Bank N.A. CEO said they are conducting business as usual within the US and expect to resume cross-border transactions in the coming days, while the CEO added the FDIC transferred all deposits and all assets of former Silicon Valley Bank to the newly created, full-service FDIC-operated ‘bridge bank’ and all depositors have full access to their money with deposits protected.

FDIC is still looking to sell SVB (SIVB) and told GOP senators it is planning another auction, according to WSJ sources.

Moody’s withdrew Signature Bank’s (SBNY) long-term and short-term local currency bank deposit ratings, while it downgraded its subordinate debt to C from BAA3 and will withdraw ratings. Furthermore, Moody’s placed multiple US banks under review for downgrade including Zions Bancorporation (ZION), Comerica (CMA), UMB (UMBF), Western Alliance (WAL), First Republic (FRC), Signature Bank (SBNY) and Intrust.

Large US banks are reportedly inundated with new depositors as smaller lenders face turmoil with JPMorgan (JPM), Citigroup (C) and other large financial institutions trying to accommodate customers wanting to move deposits quickly, according to FT.

Credit Suisse (CSGN SW) found material weakness in financial reporting for 2021 and 2022, though the reports fairly present the situation. Co. at its AGM is to discuss the proposal for a distribution of a dividend to shareholders of CHF 0.05 gross per registered share for the financial year 2022. Adding, it could require significant resources to correct the material deficiencies within report, developing a remediation plan to address this. Note, this update is not in relation to the SVB situation. On SVB, CEO adds credit exposure is not material.

FX

The DXY is firmer and benefitting from some consolidation/corrective price action in yields, with the index briefly surmounting 104.00 as the US 2 & 10yr yields convincingly reclaimed 4.00% and 3.50% respectively.

Given the action in yields and the USD’s recovery, the JPY is the clear underperformer giving back much of Monday’s haven-premium; USD/JPY above 134.00 from a 133.04 base.

As such, G10 peers are lower across the board though with the magnitude of downside less pronounced than the JPY move with EUR and GBP relatively unreactive to data prints; around 1.07 and 1.215 respectively vs the USD.

Antipodeans are more rangebound with AUD and NZD around 0.665 and 0.621 respectively while the SEK as perhaps derived some incremental support from familiar Riksbank commentary.

PBoC set USD/CNY mid-point at 6.8949 vs exp. 6.8933 (prev. 6.9375)

Fixed Income

Core benchmarks have experienced a marked turnaround, after an initial move higher around Credit Suisse’s update, with USTs now below 114.00 from a 115.07+ peak.

Amidst this, yields are elevated across the curve with the US experiencing marked bear-flattening with US CPI due and potential remarks from Fed’s Bowman.

Within Europe, Bunds peaked just above 137 and have since reversed to below 135.00 while the UK sale was well-received and seemingly helped to lift Gilts off lows ahead of German Bobl supply.

Commodities

WTI and Brent have been declining throughout the European morning after settling lower by around USD 2.0/bbl, with the front month futures below USD 73/bb; and USD 79/bbl respectively.

Nat Gas experiences some modest divergence with Henry Hub firmer and Dutch TTF softer, with ING highlighting renewable generation and milder forecasts for northern Europe as factors.

Metals are mixed, spot gold is slightly softer but is holding above USD 1900/oz while base metals continue to slip given the broader tone.

Indian oil ministry says there are no discussions on payments of Russian oil in CNY, according to Reuters sources; India has no obligation to purchase Russian oil below the price cap.

Black Sea grain deal has been extended according to Tass citing the Russian Deputy Foreign Minister; under prior conditions. Ukraine will adhere to the terms of the prior 120-day corridor, via Reuters citing a senior gov’t official. However, Turkey and the UN subsequently clarified that talks are ongoing on an extension.

Geopolitics

US President Biden said alongside Australian PM Albanese that he doesn’t view what they are doing as a challenge to anybody but is more about stability in the Indo-Pacific after AUKUS leaders met and agreed on a plan to deliver nuclear-powered submarines to Australia.

North Korea fired two short-range ballistic missiles into the East Sea. South Korea said the missiles flew 620km and the repeated launches are a grave act of provocation threatening peace and security in the region. South Korea also said it will carry out combined drills with the US as planned and maintain readiness based on overwhelming capability, while the US military said North Korean missile launches do not pose an immediate threat to US personnel or territory or to their allies.

Russian Deputy Foreign Minister says Washington seeks to create flashpoints for geopolitical confrontation with Russia in Moldova and Georgia, via Al Jazeera.

Crypto

US DoJ is probing the collapse of Do Kwon’s TerraUSD stablecoin and FBI and New York officials have questioned former Terraform Labs team members, according to WSJ.

Crypto conglomerate Digital Currency Group (DCG) is reportedly trying to find new banking partners for portfolio companies following the collapse of SVB (SIVB), Signature Bank (SBNY), and Silvergate (SI), according to messages viewed by CoinDesk

US Event Calendar

06:00: Feb. SMALL BUSINESS OPTIMISM 90.9, est. 90.3, prior 90.3

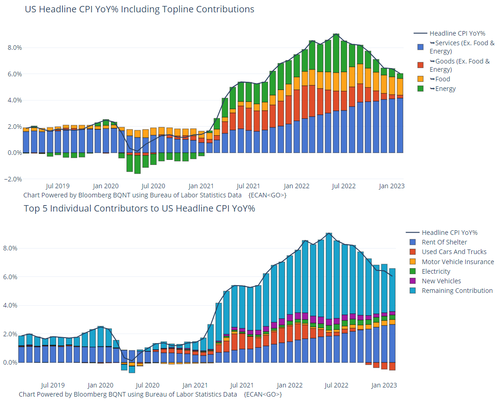

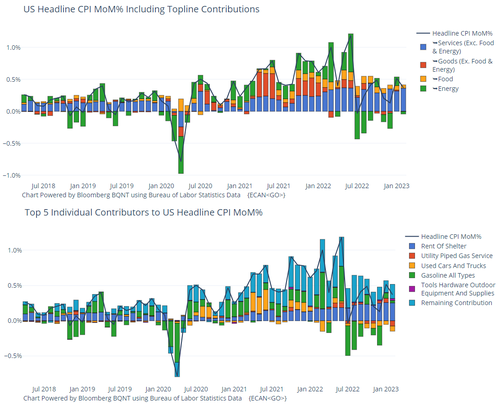

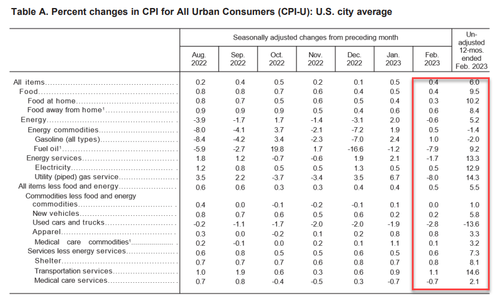

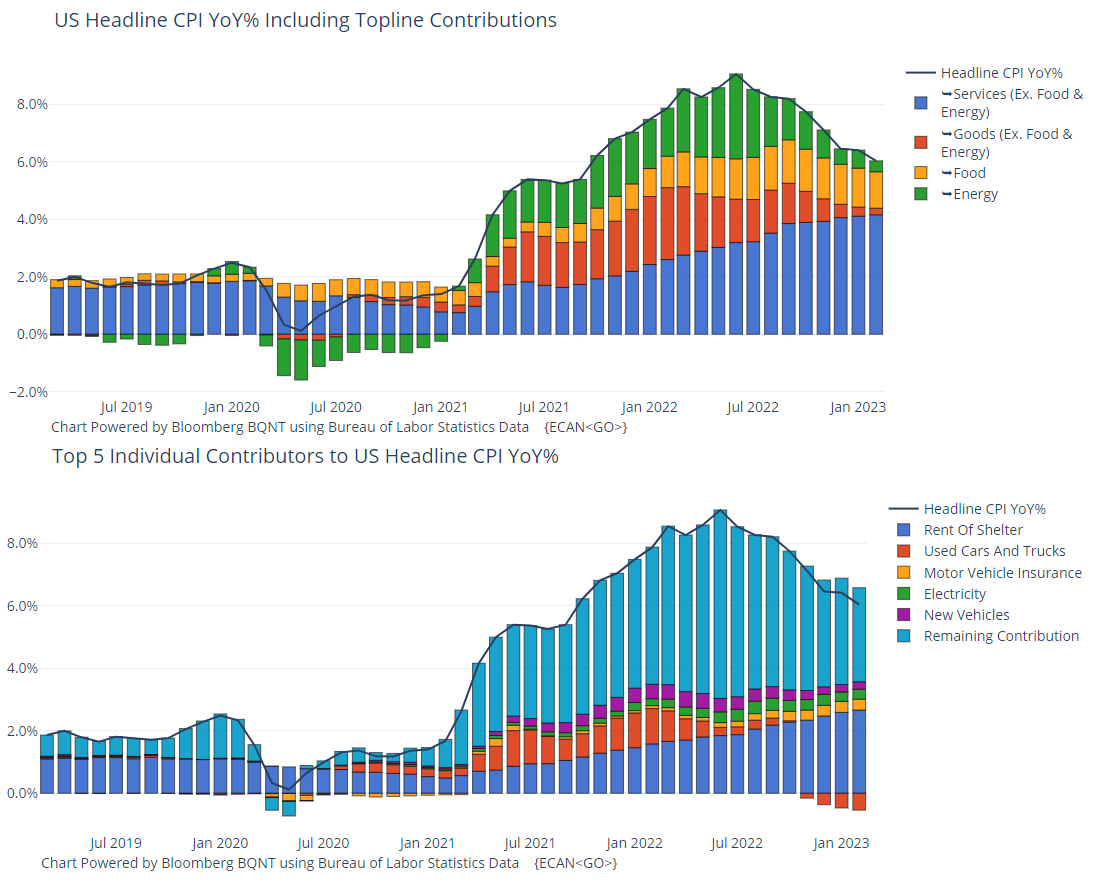

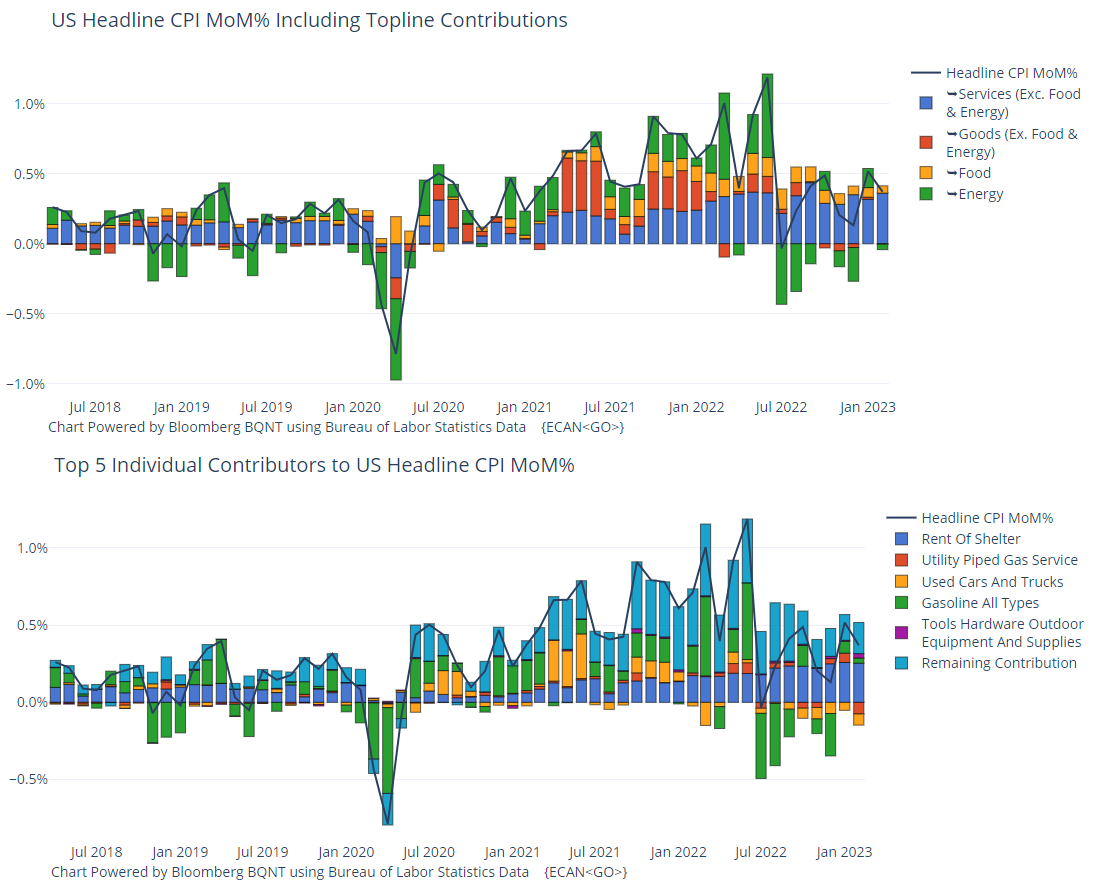

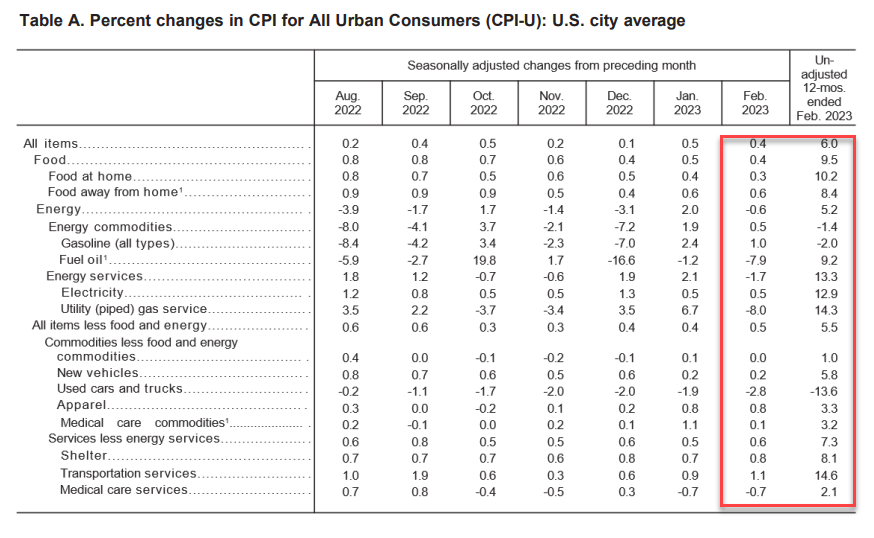

08:30: Feb. CPI MoM, est. 0.4%, prior 0.5%; Feb. CPI YoY, est. 6.0%, prior 6.4%

CPI Ex Food and Energy MoM, est. 0.4%, prior 0.4%; CPI Ex Food and Energy YoY, est. 5.5%, prior 5.6%

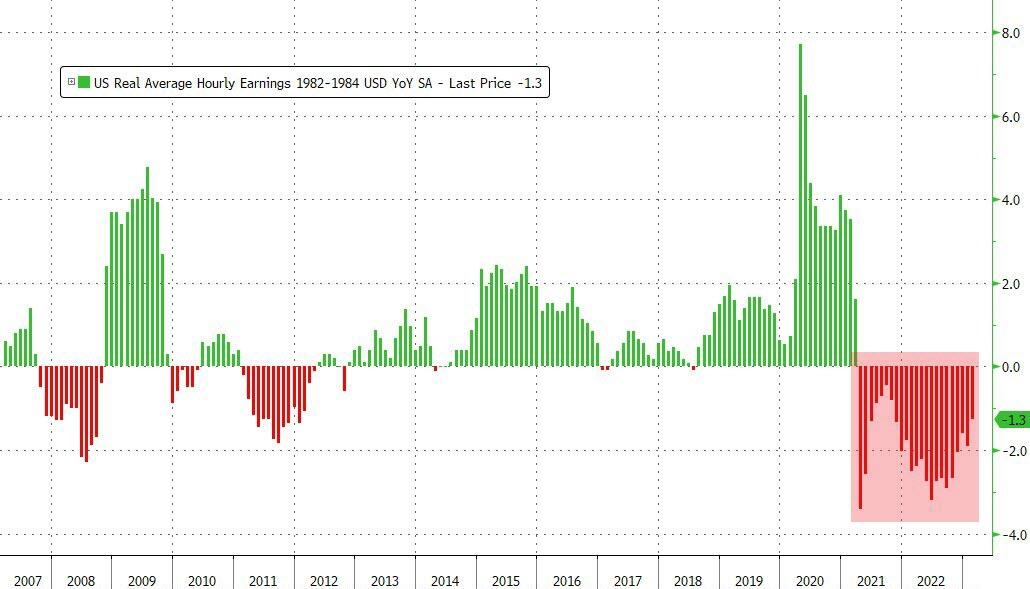

Real Avg Hourly Earning YoY, prior -1.8%, revised -1.9%

Real Avg Weekly Earnings YoY, prior -1.5%, revised -1.9%

DB’s Jim Reid concludes the overnight wrap

In late summer 1998 I went on holiday for 2 weeks. Before I went, a Mexico 2002 maturity bond traded at around +150-200bps over DM government bonds. After a relaxing two weeks in the sun with no mobile phones etc and no financial news flow I ambled back into the office to the shock of finding that same Mexico bond that I’d been involved in launching as a salesman a few months earlier was now trading at around +900bps. I was dumbfounded. Since then, I’ve learnt not to be too shocked by anything in financial markets even if yesterday was up there with some of the wilder days I can remember. In some benchmark assets (e.g. US 2yr yields) we saw far bigger moves that even during the GFC. However if you just looked at the S&P 500 (-0.15%) you’ll be forgiven for thinking yesterday was a big fuss about nothing.

Overall, I came out of yesterday even more convinced of our long-standing H2 2023 US hard landing view but with absolutely no idea at the moment what the Fed and ECB are going to do at their meetings over the next week and even beyond. I always thought that with inflation where it was, that central banks would keep hiking until they broke something, which was especially likely with the yield curve so inverted. Now they have broken something, is that enough for a pause? Much will depend on whether markets and contagion risk can calm quickly enough. If the FOMC meeting was today I strongly suspect they wouldn’t hike but a week is a long time in these markets. For the recession call it’s simpler. As per last month’s chart book we were just “Waiting for the lag” (link here). It’s fair to say that the lag has well and truly arrived and it’s unlikely now that a key part of our macro story, namely lending standards, are going to get looser given all that’s gone on. So no change to our very bearish year end 2023 credit spread targets through all this crisis.

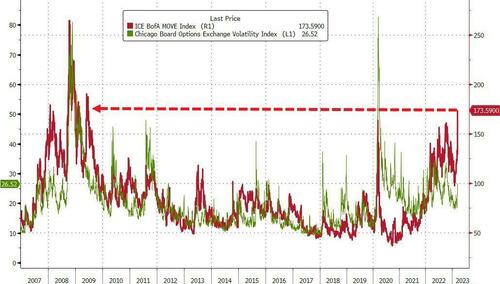

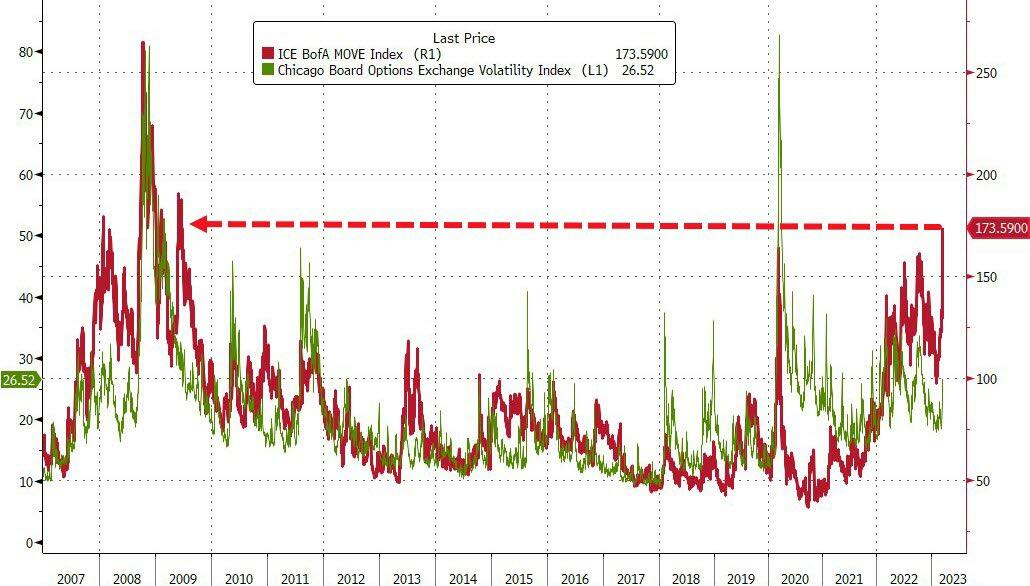

Back to current markets, let’s first run through some of the astonishing stats from yesterday. The most remarkable was that we saw the biggest daily decline in the 2yr Treasury yield (-61.0bps) since October 7 1982 when the 2yr yield fell -75bps to 10.469% in what was a very different rate environment. In Europe, the 2yr German yield saw its biggest decline (-40.7bps) in available data back to reunification in 1990. And for equities, the KBW Banks Index (-11.66%) saw its worst performance since the height of the pandemic in March 2020 even if there was a big divide between big and small banks (see below). In the meantime, there are now serious questions being asked about whether the Fed might even call it a day on their current hiking cycle, and pricing for the Fed funds rate by the end of the year has now collapsed by over -140bps since last Wednesday. Meanwhile the MOVE index of bond volatility hit 14-year highs.

After all that, there’ve been few signs of any letup in Asian markets this morning, with banks leading a further round of equity declines. For instance, the TOPIX Banks index in Japan is down another -7.21%, which builds on its -9.17% decline over the previous two sessions. That has meant all the major equity indices have lost ground, including the Nikkei (-2.20%), the KOSPI (-2.37%), the Hang Seng (-1.59%), the Shanghai Comp (-0.77%) and the CSI 300 (-0.67%). Sovereign bond yields have moved lower in Asia too, with Japan’s 10yr government bond yield (-7.8bps) moving down to 0.24% this morning, which interestingly is beneath the Bank of Japan’s previous ceiling of 0.25% for the 10yr yield, which they moved up to 0.5% back in December.

Whilst markets in Asia have continued yesterday’s trend, those in the US this morning are showing signs of stabilising. Equity futures are pointing higher, with those on the S&P 500 up +0.31% after the index’s run of three consecutive declines. Furthermore, we’ve even seen a sharp rebound in the 2yr Treasury yield, which is up +18.4bps this morning to 4.16%, following its largest daily decline since 1982 over the previous session. The only thing to remember is that we have been here before to some extent, since 24 hours ago futures were pointing to an even sharper equity rebound before we ended up with the S&P seeing a modest decline, so this story could still have plenty of twists and turns remaining.

In terms of the latest on the SVB situation, concerns about potential contagion to other banks remain prominent, in spite of the moves we mentioned in yesterday’s edition from the FDIC and the Fed. We did hear from President Biden, who reassured the public that “the banking system is safe” and proposed new regulation that would “strengthen the rules for banks to make it less likely this kind of bank failure would happen again”. But he didn’t outline any specific proposals, and any new legislation would have to get past the Republican majority in the House of Representatives. After the US close the Fed announced that they would be launching an internal investigation into the supervision of Silicon Valley Bank, led by Vice Chair for Supervision Michael Barr.

In a move that highlights the current need for funding in financial markets, the US Federal Home Loan Banks raised $88.7bn in a bond sale yesterday, exceeding their initial target. The FHLB system is a Depression-era tool designed to be a lender of short-term funding to private banks in order to lessen the load on the Fed and make it not seem like banks are reaching for their “lender of last resort”. Silicon Valley Bank had tapped the FHLB last Thursday before the Fed stepped in and took control of the situation. Given the large bond sale it is likely that other regional banks are still looking for liquidity.

The lingering contagion concerns and fears about further outflows meant that bank stocks plummeted yesterday, particularly among some of the US regional banks. For instance, First Republic ended the day down -61.93%, which was actually a recovery from its intraday low of -78.56%. Another was Western Alliance Bancorp, which fell -47.06% having been as low as -84.88%. Both experienced trading halts during the day, and overnight Moody’s has placed the ratings of both on review for a downgrade. By contrast, the biggest banks were relatively unscathed, with JPMorgan only down -1.80%, whilst Bank of America (-5.81%) and Citigroup (-7.45%) also outperformed the wider KBW Banks Index.

Aside from contagion fears, the other big question moving forward is how central banks react to this turmoil. Up until Thursday of last week, investors had little doubt that the Fed would keep on hiking rates for some months, and a larger 50bps hike was seen as the most likely outcome for the next meeting. But the view now is that the SVB collapse has torpedoed any chance they might accelerate to 50bps, and even a 25bps move is now seen as questionable depending on what happens over the coming days. We’ve also seen financial conditions tighten with astonishing speed, with Bloomberg’s index seeing its largest move tighter over 3 days since March 2020 at the height of the pandemic.