by harveyorgan · in Uncategorized · Leave a comment·Editi

GOLD PRICE CLOSED: DOWN $2.25 TO $1972.75

SILVER PRICE CLOSED: DOWN $0.22 AT $23.48

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1971.75

Silver ACCESS CLOSE: 23.62

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

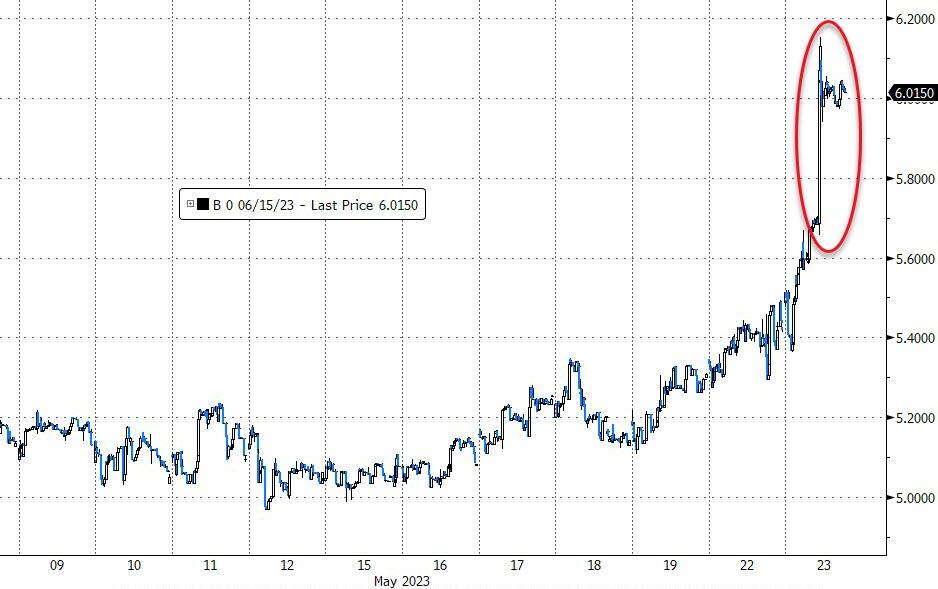

Bitcoin morning price:, $27,340 UP 467 Dollars

Bitcoin: afternoon price: $27,206 UP 601 dollars

Platinum price closing $1054.85 DOWN $17.50

Palladium price; $1452.85 DOWN $37.20

“Our system is so stinkin’ corrupt that we owe Sodom and Gomorrah an apology.” … Trader Dan Norcini in 2009

GO GATA!

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,666.75 UP 3.50 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1590.52UP 6.25 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1833.30 UP 11.26 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MAY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,974.800000000 USD

INTENT DATE: 05/22/2023 DELIVERY DATE: 05/24/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 2

365 H MAREX CAPITAL M 2

661 C JP MORGAN 1

737 C ADVANTAGE 2

800 C MAREX SPEC 3

880 H CITIGROUP 4

TOTAL: 7 7

MONTH TO DATE: 6,039

JPMorgan stopped 1/7 contracts

FOR MAY:

GOLD: NUMBER OF NOTICES FILED FOR MAY/2023. CONTRACT: 7 NOTICES FOR 700 OZ or 0.02177 TONNES

total notices so far: 6039 contracts for 603,900 oz (18.784 tonnes)

FOR MAY:

SILVER NOTICES: 24 NOTICE(S) FILED FOR 120,000 OZ/

total number of notices filed so far this month : 2529 for 12,645,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP DOWN $2.25..

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//WOW!!

/NO CHANGES IN GOLD INVENTORY AT THE GLD:///

INVENTORY RESTS AT 942.74 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 22 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV.: /; : INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 471.330 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A TINY SIZED 38 CONTRACTS TO 137,678 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS TINY SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.19 FALL IN SILVER PRICING AT THE COMEX ON MONDAY. TAS ISSUANCE WAS A GOOD SIZED 470 CONTRACTS. THESE WILL BE USED FOR MANIPULATION NEXT MONTH. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY: A GOOD 470 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THEY VALUE 0 TO A POSITION LIMIT IF A CALENDAR SPREAD OCCURS. IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED THE COMPLAINT IN SIMILAR FASHION TO ALL OF THOSE DEMOCRATIC CRIMES COMMITTED WITH NO ATTENTION GIVEN BY ATTORNEY GENERALS.

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.19). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A TINY GAIN ON OUR TWO EXCHANGES OF 62 CONTRACTS WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 4.250 MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH DUE TO (TAS) MANIPULATION, AND FINAL WEEK IN THE DELIVERY CYCLE DUE TO COMEX SPREADERS MANIPULATION.

WE MUST HAVE HAD:

A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS( 100 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.105 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF 110,000 OZ (QUEUE JUMP RAISES THE AMOUNT OF SILVER STANDING)+0 EXCHANGE FOR RISK// TOTAL 4.25 MILLION OZ OF EXCHANGE FOR RISK FOR THE MONTH(RAISES THE AMOUNT OF SILVER STANDING):THUS TOTAL OF 17.670 MILLION OZ OF STANDING FOR DELIVERY V) TINY SIZED COMEX OI GAIN/ SMALL SIZED EFP ISSUANCE/VI) GOOD NUMBER OF SHORT T.A.S. CONTRACT INITIATION//SOME T.A.S LIQUIDATION MANIPULATING THE PRICE SOUTHBOUND.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -removed 29 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTRACTS for 17 days, total 10,625 contracts: OR 53.125 MILLION OZ . (625 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 53.125 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 53.1250 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 38 CONTRACTS DESPITE OUR FAIR SIZED $0.19 LOSS IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 100 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 13.105 MILLION OZ//FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 110,000 OZ (INCREASES THE AMOUNT OF SILVER STANDING) +// + 0.0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //TOTAL EXCHANGE FOR RISK MONTH= 4.25 MILLION//NEW TOTALS 13.310 MILLION OZ + 4.25 MILLION = 17.670 MILLION OZ// .. WE HAVE A TINY SIZED GAIN OF 68 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GOOD 470!!//SOME FRONT END OF THE TAS CONTRACT LIQUIDATED.

WE HAD 24 NOTICE(S) FILED TODAY FOR 120,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 6,192 CONTRACTS TO 480,505 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -115 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI ( 6,192 CONTRACTS) DESPITE OUR $4.70 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR MAY. AT 3.5085 TONNES ON FIRST DAY NOTICE // PLUS 300 OZ QUEUE JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)/+ /A SMALLER ISSUANCE OF 713 T.A.S. CONTRACTS/SOME FRONT END OF TAS LIQUIDATION////YET ALL OF..THIS HAPPENED WITH OUR $4.70 LOSS IN PRICE WITH RESPECT TO MONDAY’S TRADING.WE HAD A FAIR SIZED LOSS OF 2787 OI CONTRACTS (8.668 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3405 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 480,505

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2787 CONTRACTS WITH 6,192 CONTRACTS DECREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): 713 CONTRACTS) AND 3405 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 2787 CONTRACTS OR 8.668 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3405 CONTRACTS) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (6,192) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 2787 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 3.5085 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 300 OZ // NEW STANDING: 19.101 TONNES // ///3) MINOR LONG LIQUIDATION//4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: T.A.S. ISSUANCE: 713 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 53,919 CONTRACTS OR 5,391,900 OZ OR 167.710 TONNES IN 17 TRADING DAY(S) AND THUS AVERAGING: 3171 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES 167.710 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 167.710/3550 x 100% TONNES 4.73% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES ( MUCH SMALLER THAN LAST MONTH)

MAY: 157.119 TONNES (HEADING FOR ANOTHER SMALLER MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A TINY SIZED 38 CONTRACTS OI TO 137,678 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 100 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 100 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 100 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 38 CONTRACTS AND ADD TO THE 100 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 62 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL .310 MILLION OZ

OCCURRED WITH OUR $0.19 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED DOWN 50.23 PTS OR 1.52% //Hang Seng CLOSED DOWN 246.92 POINTS OR 1.25% /The Nikkei closed DOWN 246.92 OR 1.25% //Australia’s all ordinaries CLOSED DOWN 0.04 % /Chinese yuan (ONSHORE) closed DOWN 7.0547 /OFFSHORE CHINESE YUAN DOWN TO 7.0661 /Oil DOWN TO 72.82 dollars per barrel for WTI and BRENT AT 76.88 / Stocks in Europe OPENED ALL MOSTLY RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 6192 CONTRACTS DOWN TO 480,505 WITH OUR LOSS IN PRICE OF $4.70 ON MONDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3405 EFP CONTRACTS WERE ISSUED: : JUNE 3405 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3405 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2787 CONTRACTS IN THAT 3405 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 6,192 COMEX CONTRACTS..AND THIS FAIR SIZED LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $4.70. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE),THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE THIS MORNING WAS A TOUCH SMALLER AT 713 CONTRACTS. DURING THIS WEEK THEY SOLD THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE). FOR EXAMPLE WITH TONIGHT’S READING OF TAS 100% OF ISSUANCE OF T.A.S. WAS JUNE AND AUGUST.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (19.101) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.101 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $4.70) //// BUT WERE UNSUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD OUR FAIR SIZED LOSS OF 2787 CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE TAS LIQUIDATION.

WE HAVE LOST A TOTAL OI OF 8.311 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY. (3.5085 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 300 oz (0.00933 TONNES)//NEW STANDING 19.101 TONNES ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $4.70

WE HAD +REMOVED 115 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 2787 CONTRACTS OR 278700 OZ OR 8.668 TONNES.

Estimated gold comex today 258,945// fair

final gold volumes/yesterday 217,770// FAIR

//MAY 23/ MAY 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 99.297 OZ Delaware . |

| Deposit to the Dealer Inventory in oz | NIL |

| Deposits to the Customer Inventory, in oz | 32,151.000 oz Brinks 1000 kilobars |

| No of oz served (contracts) today | 7 notice(s) 700 OZ 0.02177 TONNES |

| No of oz to be served (notices) | 102 contracts 10200 oz 0.3172 TONNES |

| Total monthly oz gold served (contracts) so far this month | 6039 notices 603,900 OZ 18.787 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into Brinks: 32,151.000 oz

1000 kilobars

total deposits: 32,151.000 oz

customer withdrawals: 1

i) Out of Delaware: 99.297 oz

total withdrawals: 99.297 oz oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 109 contracts having LOST 98 contracts. We had 101 contracts filed

on MONDAY, so we GAINED A SMALL 3 contracts or an additional 300 oz (0.00933 tonnes) will stand for gold in this non active delivery month of May

June LOST A HUGE 15,245 contracts DOWN to 162,227 contracts.

July added 254 contracts to stand at 2501 contracts.

AUGUST GAINED 8805 contracts UP to 260,801 contracts

We had 7 contracts filed for today representing 700 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 7 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2023. contract month,

we take the total number of notices filed so far for the month (6,039 x 100 oz ), to which we add the difference between the open interest for the front month of MAY (109 CONTRACTS) minus the number of notices served upon today 7 x 100 oz per contract equals 614,1200 OZ OR 19.101 TONNES the number of TONNES standing in this NON- active month of May.

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (6,039 x 100 oz) x 109 OI for the front month minus the number of notices served upon today (1)x 100 oz} which equals 614,100 oz standing OR 19.101 TONNES

TOTAL COMEX GOLD STANDING: 19.0917 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,696,563.034 OZ 52.77 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,612,690.934 OZ

TOTAL REGISTERED GOLD: 12,356,429.711 (384.336 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,256,429.711 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,659,866 OZ (REG GOLD- PLEDGED GOLD) 331.565 tonnes//

END

SILVER/COMEX

MAY 23//2023// THE MAY 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2,495,709.077 oz CNT Loomis Manfra JPMorgan Delaware . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 600,360.300 oz JPMorgan |

| No of oz served today (contracts) | 24 CONTRACT(S) (120,000 OZ) |

| No of oz to be served (notices) | 155 contracts (775,000 oz) |

| Total monthly oz silver served (contracts) | 2529 Contracts (12,645,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into JPMorgan: 600,360,300 oz

Total deposits: 600,360.300 oz

JPMorgan has a total silver weight: 141.687 million oz/272.502 million =52.20% of comex .//dropping fast

Comex withdrawals 5

i) Out of CNT 1,023,188.590

ii) Out of Delaware 75,506.768 oz

iii) Out of Loomis: 93,806.610 oz

iv) Out of JPMorgan: 1,091,937.920 oz

v) Out of Manfra 311,269.189 oz

Total withdrawal: 408,195.128 oz

adjustments: 2//dealer to customer

i) Out of JPMorgan: 35,278.100 oz

ii) Manfra: 245,007.114 oz

TOTAL REGISTERED SILVER: 30.598 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 272.502 million oz

CALCULATION OF SILVER OZ STANDING FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2023 OI: 175 CONTRACTS HAVING LOST 41 CONTRACT(S). WE HAD 63 CONTRACTS FILED ON MONDAY, SO WE GAINED 22 CONTRACTS OR AN ADDITIONAL 110,000 OZ WILL STAND FOR DELIVERY ON THIS SIDE OF THE POND

JUNE HAD A 6 CONTRACT LOSS TO 1133

JULY HAD A 247 CONTRACT LOSS TO 112,144 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 24 for 120,000 oz

Comex volumes// est. volume today 58,102 fair

Comex volume: confirmed yesterday: 40,874 poor

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 2529 x 5,000 oz = 12,525,000 oz

to which we add the difference between the open interest for the front month of MAY(179) and the number of notices served upon today 24 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2023 contract month: 2529 (notices served so far) x 5000 oz + OI for the front month of May (179) – number of notices served upon today (24 )x 500 oz of silver standing for the MAY contract month equates to 13.4200 million oz + THE CRIMINAL 0 MILLION OZ EXCHANGE FOR RISK TODAY//NEW TOTAL EXCHANGE FOR RISK: 4.250//NEW TOTAL 17.670 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 937.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 931.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

GLD INVENTORY: 942.74 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

CLOSING INVENTORY 471.330 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

A good one from Peter Schiff today

(Peter Schiff)

Peter Schiff: The Fed Is Losing The Inflation Fight

TUESDAY, MAY 23, 2023 – 07:20 AM

We saw a big selloff in the gold market last week and the price dropped below $2,000 an ounce. The catalyst for that selloff was tough talk from several Federal Reserve officials and an increasing expectation that the central bank will raise rates again in June. As Peter Schiff explained in his podcast, everybody thinks the Fed is going to win the inflation fight because it is going to be even tougher. In reality, they are talking tougher because they are losing the fight.

On Thursday, Dallas Fed President Lorie Logan said she’s concerned that “much too high” inflation is not cooling fast enough to allow the Fed to pause its interest-rate hike campaign in June.

The data in coming weeks could yet show that it is appropriate to skip a meeting. As of today, though, we aren’t there yet.”

While the stock market shrugged off the tougher Fed talk, the dollar strengthened, gold fell and the short end of the bond market also sold off.

If the FOMC does raise rates next month, it will push the Fed funds rate to between 5.25 to 5.5%. As Peter pointed out, this would drive rates above the peak of the last cycle back in June 2006.

We will be above the interest rate level that precipitated the 2008 financial crisis and Great Recession. Except the difference is today that we have so much more debt than we did back then. Everybody has a lot more debt — the government, corporations, individuals. So, that level of interest will do far more damage today than it did in 2007. And we know how much damage it did then because we had the financial crisis of 2008. So, the financial crisis that has already begun in 2023 is going to be much worse than the one that we had in 2008.”

Household debt is now above $17 trillion for the first time ever. Even more concerning is the fact that credit card debt was flat in Q1. Credit card balances typically fall in the first quarter.

Americans are using their credit cards as a lifeline. That’s how they’re dealing with higher prices. They’re charging stuff.”

In March alone, revolving credit, which included credit card debt, was up 17.3% on an annual basis. Meanwhile, interest rates on credit card debt have spiked to over 20%. Peter said this indicates that the Fed really isn’t making any progress on inflation.

The consumer keeps spending. Where are they getting the money? They’re borrowing it. Credit continues to expand. That’s part of the inflationary dynamic. Inflation is an expansion of the money supply, which includes credit. So, consumers are not cutting back on their spending because of higher prices. They’re not even cutting back on their spending because of higher interest rates. They just keep on spending. So, prices are going to keep on rising, and this next quarter-point rate hike isn’t going to be any more effective than the previous rate hikes, which means they’re going to have to do it again.”

But Peter said no matter how much they hike, it’s not going to matter. That’s what the markets fail to understand. Everybody is thinking that since the central bank is going to fight even harder to fight inflation, it’s a good sign and the Fed is on course to slay the inflation dragon.

No. The Fed is losing its fight with inflation. That’s why it’s going to try harder. But it’s going to be ineffective. If they couldn’t beat inflation with 5%, they’re not going to beat it with 5.25%.”

It’s not just household debt that’s a problem. The federal government has a debt problem of its own. Federal revenues have collapsed even as the Biden administration keeps right on spending. And why are tax receipts going down? Because the economy is weakening.

The Leading Economic Indicators were down for the 13th straight month. The last time we had a losing streak this started in 2007 and lasted 20 months.

I think we’re going to break that record. And the most ironic part about it is the biggest positive indicator in the LEI, and without this, it would have been lower, is the stock market because the stock market is going up. But I’ve said this before. The stock market going up is not a sign of a strong economy. It’s actually the reverse. The reason the stock market is going up is because investors expect a recession, and they expect the Fed to cut rates at some point due to that recession.”

But Peter emphasized that inflation will still be a problem. In fact, it will get even more out of hand as the Fed starts easing to try to prop up the collapsing economy.

In this podcast, Peter also talked about the debt ceiling and his defamation lawsuit.

https://www.zerohedge.com/markets/peter-schiff-fed-losing-inflation-fight

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

EGON VON GREYERZ..

Gold’s Key Indicator

Egon von Greyerz

May 23, 2023

Egon von Greyerz interviews with Kitco at Deutsche Goldmesse, Frankfurt, Germany.

After the recent bank collapses and string of interest rate hikes, Egon von Greyerz shows his deep concerns for the U.S. monetary system.

“It’s not that gold is getting incredibly strong [by itself], it’s that everything else is getting weaker, and that in particular means your currency, whether it’s the world reserve currency, British pound sterling etc.”

In March, SVB Financial Group, the parent company of Silicon Valley Bank (SVB), filed for bankruptcy. Signature Bank, a New York-based regional bank also went under, the third-biggest bank failure in U.S. history. Greyerz argued the moves portend a larger move. “We have reached the end of this monetary era,” said Greyerz. “It doesn’t happen overnight and it’s taken longer than I expected, nevertheless it’s happening and..it’s starting to accelerate.”

Investors have been fleeing the banking sector. Year-to-date the SPDR S&P Bank ETF is down 22%. Gold has benefitted, trading above $2,000 an ounce for much of 2023. The fear trade has also benefited the gold miners, which are up 10% year to date. Coverage of Deutsche Goldmesse 2023 sponsored by Defiance Silver.

0:20 – What do the recent bank failures indicate?

2:00 – End of the monetary era.

3:55 – Dedollarization

6:05 – Why focus on currencies to determine the direction of gold?

7:48 – The problem with service-based economies.

https://lemetropolecafe.com/dospassos.cfm?pid=18440

3,Chris Powell of GATA provides to us very important physical commentaries

WALL STREET ON PARADE The Fed Has a New Scandal on Its Hands: Colluding with Central Banks to Rig Libor; Evidence Is Being Tweeted Out

https://wallstreetonparade.com/2023/05/the-fed-has-a-new- scandal-on-its-hands-colluding-with-central-banks-to-rig- libor-evidence-is-being-tweeted-out/

END

4. OTHER GOLD/SILVER RELATED COMMENTARIES/…

Vince Lanci: Blackrock Takes Large Silver Position In PSLV – YouTube

| A MUST VIEW: | BLACKROCK PURCHASES A HUGE PERCENTAGE OF SPROTT PSLV | |||||||||||

2.5% of total issued stock

However in order to obtain the stock, they needed to borrow silver from the SLV

And now the PSLV and Sprott CEF are close to a premium which is exactly what Eric Sprott wants.

At a premium he will go out and buy more silver so as to not dilute shareholders

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: OLIVE OIL

Drought especially in Spain, is plaguing the production of olive oil . Spain produces over 40% of the world’s production

(zerohedge0

Olive Oil Prices Soar As Top Producer Plagued With Drought

TUESDAY, MAY 23, 2023 – 02:45 AM

Spain’s severe drought and parched soils have sent olive oil prices to levels not seen in more than a decade. The surge in olive oil prices, along with fresh produce, is exacerbating already high food prices as the Northern Hemisphere summer starts in less than a month.

Data from Bloomberg shows that Spanish extra-virgin olive oil prices have jumped 200% since 2020 to 5,870 euros per metric ton — the highest level since 2010. Most of the price surge was recorded in the last year.

“Output in the country could more than halve this season due to the arid conditions, according to a Spanish farming industry group,” Bloomberg said. Spain accounts for 40% of the world’s supply, indicating prices across Europe and other regions are being pushed higher.

Europe’s Monitoring Agricultural Resources recently said Spain is under severe weather stress, with barely any rainfall since January. The drought is damaging crops and threatens to drive food prices even higher across Europe.

Research firm Gro Intelligence penned a note last week that warned the country is in “extreme” drought across top croplands — the highest recorded reading in at least two decades — while soil moisture levels are the lowest since at least 2010.

Drought conditions in Spain have been exacerbated by above-average temperatures that could be due to an emerging El Nino weather pattern. We warned this might create disruptions in the agricultural industry.

El Nino comes as global food prices remain at decade highs.

These price levels are dangerous because high inflation can spark social unrest in countries.

END

end

5 B GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

We have been highlighting this to you before. Africa’s first test run for a CBDC has failed

(Armstrong)

Africa’s First Test Run For A CBDC has Failed

TUESDAY, MAY 23, 2023 – 03:30 AM

Authored by Martin Armstrong via ArmstrongEconomics.com,

The transition to CBDC in Nigeria did not go as planned. The elites always seek out African nations to use as their test subjects. Nigeria attempted to slowly roll out the program dubbed eNaira built on the Hyperleger Fabric blockchain. The Central Bank of Nigeria (CBN) is solely responsible for running the nodes of this digital currency. Beginning stress tests stated this currency could execute 2,000 transactions per section. In October 2021, the government began offering incentives to citizens who chose to CBN.

A year later, the country was still hesitant to make the switch so the central bank began implementing forceful measures. In October 2022, the CBN decided to cancel and resign the currency in a “move aimed at restoring the control of the Central Bank of Nigeria (CBN) over currency in circulation.”

They stated that the original paper notes would only be legal tender until January 31, 2023, leaving the people with no alternative but to convert their cash. Nigerians were no stranger to the concept of currency cancellation as it is something the government has routinely done.

The CBN openly announced that the end goal was to target a 100% cashless society replaced with eNaira. Fewer than 0.5% of Nigerians adopted the eNaira and protests erupted across the nation.

The central bank set a cash withdrawal limit of ₦100,000 ($225) per week for individuals and ₦500,000 ($1,123) for businesses. Citizens wishing to take out larger sums were subject to a processing fee between 5% and 10%. ATMs were limited to ₦20,000 ($45) per day, and only ₦200 ($0.45) notes or lower denominations were available in the machines.

Bloomberg reported that 90% of the country previously used cash for transactions. They did not want to convert to CBDC but were provided with no alternative. Demonetizing the currency reduced available cash from 3.2 trillion nairas to 1 trillion nairas. This led to the central bank creating over 10 billion eNairas. The people are continually protesting these measures as their society which was largely dependent on cash interactions has been destabilized.

This is how it all begins.

They are using Nigeria and other countries as test subjects before rolling out these programs in the West. It is hard for Americans to fathom currency cancelation, as it has never occurred here.

Yet, the Federal Reserve has made it clear that they are looking into this option. Per usual, they market it as a “convenience” for the people.

In truth, it is a way to ensure money stays on the grid under the thumb of government. They will not allow one cent to go untaxed, and as the program expands, they can remove individuals and organizations from participating in society entirely.

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS// TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.0547

OFFSHORE YUAN: 7.0661

SHANGHAI CLOSED DOWN 50.23 PTS OR 1.52%

HANG SENG CLOSED DOWN 246.93 PTS OR 1.25%

2. Nikkei closed DOWN 129.06 PTS OR 1.12%

3. Europe stocks SO FAR: ALL MOSTLY RED

USA dollar INDEX DOWN TO 103.39 EURO FALLS TO 1.0779 DOWN 31 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.409 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 138.51 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.4885***/Italian 10 Yr bond yield RISES to 4.338*** /SPAIN 10 YR BOND YIELD RISES TO 3.537…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 3.3865

3j Gold at $1960.10 silver at: 23.14 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 3 /100 roubles/dollar; ROUBLE AT 80.23//

3m oil into the 72 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 138.51 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .409% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9014 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.8701 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.748 UP 3 BASIS PTS…

USA 30 YR BOND YIELD: 3.987 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.378 UP 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.85…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.170 UP 10 BASIS PTS

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Slide As Debt Ceiling Talks Enter 11th Hour, European PMIs Crumble

TUESDAY, MAY 23, 2023 – 08:09 AM

US equity futures are lower, as treasuries also dropped across the curve, with the two-year yield rising for an eighth day, after the latest round of talks between Joe Biden and Kevin McCarthy Monday ended without a deal, while Eurozone manufacturing activity shrank at the fastest pace since the pandemic shuttered factories three years ago, threatening to sap momentum from an economy driven by services. The dollar rose as did bitcoin, gold fell again while oil reversed earlier losses and jumped to session highs after Saudi Arabia’s energy minister told oil speculators to “watch out” just over a week before the OPEC+ alliance is due to meet.

At 7:45am ET, US equity futures dropped 0.2% to session lows, dropping back under 4,200, whlie the Nasdaq was shocking in the red perhaps finally realizing where the 10Y yield is. Lowe’s slipped 1.5% in pre-market trading after cutting its sales outlook. In Europe, a rout in luxury-goods makers including Hermes International and LVMH dragged the Stoxx 600 lower after Deutsche Bank AG analysts warned the sector is crowded and valuations are lofty. Tokyo’s Topix index fell for the first time in eight days, with semiconductor-related stocks turning lower on news that Japan’s tighter export controls will take effect July 23.

In premarket trading, one of the last major retailers left to report Lowe’s slumped after it cut its comparable sales forecast for the full year. Here are the other notable premarket movers:

- Yelp shares jump 11% in premarket trading after TCS Capital Management said it believes “several buyers” would pay a premium for the company as the activist investor confirmed it had written to the board urging the exploration of a sale.

- Zoom fluctuated in US premarket trading. The video communications platform boosted its revenue guidance for the full year and management outlined plans to incorporate artificial intelligence into its products.

- PacWest shares surged in premarket trading Tuesday, set to extend Monday’s gains. The surge was fueled by the bank’s sale of a $2.6 billion portfolio of 74 real estate construction loans to Kennedy Wilson for about $2.4 billion.

- Microvast plunged as much as 24%, following the US Energy Department’s cancellation of a planned $200 million grant to the lithium-ion battery maker amid criticism over ties to China.

- Chimerix shares jump 5% in premarket after Baird Equity Research initiates coverage on the biopharmaceutical company with an outperform recommendation. The broker said Chimerix has a lead agent for the treatment of H3 K27M-mutant glioma that is potentially first in class.

- Tegna shares rose 2.3% in extended trading after the company announced share a share buyback plan and said its merger with Standard General was terminated.

The neverending debt drama continued overnight after Joe Biden and House Speaker Kevin McCarthy called their discussions on Monday productive, but an agreement remains elusive. That left traders on tenterhooks with only a few days left before June 1, when Treasury Secretary Janet Yellen said her department may run out of cash. Any deal would have to be approved by Congress before then.

“I think a default is very unlikely as I don’t think either Democrats and Republicans want it, but we could get close to it and the deadline,” Fabiana Fedeli, chief investment officer for equities and multi-asset at M&G Plc, said on Bloomberg TV. “The closer we get to the deadline the more nervous clients will get. You could have a move towards safer havens, perhaps the long end of yield curve” she warned.

Today’s macro focus will be May PMIs at 9.45am, where consensus estimates the Mfg PMI to print to dip to 50.0 from 50.2 while the Services PMI is also expected to drop to 52.5 from 53.6 prior.

European stocks slumped as a rout in luxury-goods makers including Hermes International and LVMH dragged local markets lower after Deutsche Bank AG analysts warned the sector is crowded and valuations are lofty. The Stoxx 600 was down 053% with consumer products, retailers and industrials the worst-performing sectors. Among individual stock movers, Vivendi SE tumbled after billionaire Vincent Bollore sold shares of the media conglomerate, a sign that he’s isn’t planning a buyout. Swiss asset manager Julius Baer Group Ltd. sank after disappointing results. Here are the most notable European movers:

- European paper and pulp manufacturers gain after their Brazilian peer Suzano raised June pulp prices in Asia by $30 per ton, according to a Bloomberg report

- Qiagen rise as much as 3.3% after Morgan Stanley upgraded the diagnostics and laboratory technology firm to overweight from equal-weight, saying the firm’s outlook is being undervalued

- Cranswick shares rise as much as 5.9%, making it the top performer in the FTSE 250 Index on Tuesday, after the meat supplier reported sales and profit for the full year that beat estimates

- SSP Group shares rise as much as 5.2% after the food-service company reported first-half revenue that beat estimates. Analysts highlighted new business wins and SSP’s trading momentum

- Banca Profilo shares jump as much as 9.1% after Twenty First Capital Sas reaches an agreement with Banca Profilo’s controlling shareholder Arepo BP SpA to buy a 29% stake in the bank

- Crayon gains as much as 16% after the Norwegian IT firm reported 1Q results, including gross profit growth of 31%. DNB says gross profit, Ebitda and operating free cash flow all beat estimates

- BW LPG shares gain as much as 10%, hitting a record high, after the Norwegian LPG carrier firm’s 1Q results beat expectations, with DNB calling the report solid and a proposed dividend “hefty”

- Julius Baer shares decline as much as 8.5%, the most in a year, after it reported assets under management of CHF429 billion as of the end of April, which analysts said was below expectations

- Vivendi falls in Paris trading after billionaire Vincent Bollore sold shares in the media conglomerate, damping optimism among speculators that he would launch a buyout offer

- RS Group shares decline as much as 5.6%, hitting the lowest since June 2022, after the outlook from the industrial and electronic products distributor pointed to a slowdown in its broader markets

Earlier in the session, Asian stocks were mized as participants digested the latest from the debt limit negotiations with the meeting between US President Biden and House Speaker McCarthy said to be productive but still lacked any major breakthrough.

- China’s CSI 300 Index falls 1.4% to close at its lowest since Jan. 4, with losses steepening in afternoon trading led by telecoms and financials. Benchmark about 1% away from wiping out 2023 gains; Shanghai Composite drops 1.5%. Hang Seng Index down as much as 1.6%, Hang Seng Tech Tech -1.5%. Mainland stocks was pressured after Chinese press reports noted expectations for the PBoC’s benchmark lending rates to remain unchanged for some time and after the US denied it was planning to lift sanctions on China’s defence minister.

- Tokyo’s Topix index fell for the first time in eight days, with semiconductor-related stocks turning lower on news that Japan’s tighter export controls will take effect July 23. Toyota Motor Corp. tumbled in the final minute of trading. Japan’s Nikkei 225 initially climbed to its highest level since August 1990 and was on course to match its longest win streak in around four years, before eventually deteriorating in afternoon trade.

- ASX 200 was kept afloat but with the upside capped by weakness in the consumer sectors and after Australia’s Flash Manufacturing PMI remained in a contraction.

- Key stock gauges in India rose for the third successive day amid continued buying by overseas investors and gains in the Adani pack. The NSE Nifty 50 Index advanced 0.2% to 18,348 in Mumbai, while the S&P BSE Sensex closed higher by 18.1 points at 61,981.79. Adani Group stocks clocked third straight day of gains following the observations made by a Supreme Court-appointed panel in relation to stock price manipulation. Adani Ports recovered all of its post-Hindenburg Report losses during the day. of consumer-facing firms and lenders were also contributors to the rally in Nifty 50 and the Sensex indexes, and helped them outperform most Asian peers. The MSCI Asia-Pacific Index closed 0.6% lower. Adani Enterprises contributed the most to the Nifty 50’s gain, surging 13.2%. Out of 50 shares in the Nifty index, 28 rose, while 22 fell.

In FX, the dollar index rose 0.2%, hovering near its two-month high, after talks between Joe Biden and Kevin McCarthy Monday ended without a deal, though they called their discussions productive and vowed to keep negotiating. The Japanese yen is the best performer among the G-10’s, rising 0.2% versus the greenback. The Norwegian krone is the weakest. GBP/USD fell as much as 0.5% to 1.2373, its lowest since April 21 after disappointing PMI prints; EUR/GBP trades 0.1% higher at 0.8703.

In rates, treasuries added to Monday’s losses with front-end underperforming led by two-year Treasury yields rising another 5bps to 4.36% and flattening the curve even as stock futures also dropped as European names stumbled after euro-zone manufacturing activity shrank at the fastest pace since the pandemic. Treasury yields cheaper by up to 7bp across front-end of the curve with 2s10s, 5s30s spreads flatter by ~4bp on the day; 10- year yields around 3.745%, cheaper by ~ 3bp with gilts following suit, lagging by 1bp and 5.5bp in the sector. European bonds are also in the red and Gilts also fell, underperforming their European counterparts, as UK services PMI data showed cost pressures in the services sector increased at the fastest pace in three months. The Treasury auction cycle begins 2-year note sale, and Fed Chair Powell reportedly will make an unscheduled appearance. $42b 2-year note auction at 1pm New York time begins cycle that also includes 5- and 7-year sales Wednesday and Thursday. WI 2-year yield at 4.335% is ~37bp cheaper than last month’s, which tailed by 0.3bp.

In commodities, crude futures rose with Brent trading near $76.70 of session highs after Saudi Arabia’s energy minister threatened bearish oil speculators. Spot gold falls 0.6% to $1,960.

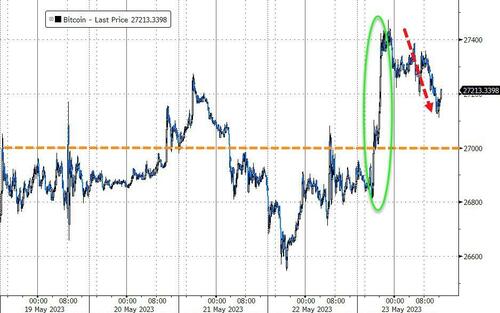

Bitcoin is bid and has convincingly surmounted the USD 27k handle to a USD 27.47k peak as we await a busy US agenda where the debt ceiling, Powell and PMIs are all potential macro movers.

To the day ahead now, and the main highlight will be the flash PMIs from Europe and the US. Other US data releases include new home sales for April, and the Richmond Fed’s manufacturing index for May. From central banks, we’ll hear from ECB Vice President de Guindos, the ECB’s Muller, Villeroy and Nagel, the Fed’s Logan and the BoE’s Haskel.

Market Snapshot

- S&P 500 futures little changed at 4,202.75

- MXAP down 0.4% to 162.32

- MXAPJ down 0.4% to 514.15

- Nikkei down 0.4% to 30,957.77

- Topix down 0.7% to 2,161.49

- Hang Seng Index down 1.3% to 19,431.25

- Shanghai Composite down 1.5% to 3,246.24

- Sensex up 0.4% to 62,180.82

- Australia S&P/ASX 200 little changed at 7,259.89

- Kospi up 0.4% to 2,567.55

- STOXX Europe 600 down 0.3% to 467.52

- German 10Y yield little changed at 2.46%

- Euro down 0.1% to $1.0799

- Brent Futures down 0.2% to $75.87/bbl

- Gold spot down 0.6% to $1,960.23

- U.S. Dollar Index up 0.16% to 103.37

Top Overnight News

- Saudi Arabia’s top energy official issued another warning to oil short-sellers, just over a week before the OPEC+ alliance is due to meet. “I keep advising them that they will be ouching — they did ouch in April,” Saudi Energy Minister Prince Abdulaziz bin Salman said at the Qatar Economic Forum in Doha on Tuesday. “I would just tell them: Watch out!” BBG

- Japan’s flash PMIs improve in May, with manufacturing rising to 50.8 (up from 49.5 in April) and services jumping to 56.3 (up from 55.4 in April). S&P

- Taiwan’s industrial production sinks by far more than anticipated in April, coming in -22.8% (vs. the Street -13% and down from -16% in March) (Bloomberg); shipping container production slumps dramatically amid a steep pullback in the global transport industry as consumers globally cut back on discretionary goods purchases. FT

- The US said it has no plans to lift sanctions on Chinese Defense Minister Li Shangfu, appearing to backtrack on comments made a day earlier by President Joe Biden while he attended the Group of Seven summit in Japan. BBG

- Europe’s flash PMIs for May are mixed, with a steep drop in manufacturing (44.6, down from 45.8 in April and below the Street’s 46 consensus) while services hold in better (55.9, down from 56.2 in April but ahead of the Street’s 55.5 forecast). S&P

- Biden/McCarthy meeting is called “productive” and “better than any other”, but a deal still hasn’t been reached, while the “X-date” fast approaches (Yellen reiterated the June 1 ceiling breach date). Politico

- Private equity groups are increasingly selling shares in portfolio companies at a discount to the price at which they went public, in a sign they do not expect stock market valuations to regain their previous highs soon. Private equity-backed follow-ons in the US are up 180 per cent year on year, but almost two-thirds of the deals were priced below the companies’ IPO. FT

- Deere will sell $36 billion of medium-term notes through John Deere Financial. It filed to sell notes ranking as senior or subordinated due nine months or more from the date of issue. BBG

- Activist investor TCS Capital Management has built a stake in Yelp and is calling on the service-recommendation site to explore strategic alternatives including a sale, people familiar with the matter said. WSJ

- HF VIPS: Mega-cap tech remains at the top of Goldman’s list of popular hedge fund long positions. MSFT, AMZN, META, and GOOGL remain the top four stocks in the VIP list this quarter, with the Info Tech and Comm Services sectors accounting for nearly half of the list. The VIP list contains the 50 stocks that appear most often among the top 10 holdings of fundamental hedge funds. The basket has outperformed the S&P 500 in 58% of quarters since 2001 with an average quarterly excess return of 37 bp. 13 new constituents: AER, AVGO, DDOG, FCNCA, GDDY, IAC, ISEE, JPM, LLY, NEWR, SPOT, TTWO, WMT. Read Ben Snider and team’s HF trend monitor HERE.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were indecisive as participants digested the latest from the debt limit negotiations with the meeting between US President Biden and House Speaker McCarthy said to be productive but still lacked any major breakthrough. ASX 200 was kept afloat but with the upside capped by weakness in the consumer sectors and after Australia’s Flash Manufacturing PMI remained in a contraction. Nikkei 225 initially climbed to its highest level since August 1990 and was on course to match its longest win streak in around four years, before eventually deteriorating in afternoon trade. Hang Seng and Shanghai Comp. were subdued following Hong Kong’s failure to sustain the early tech-led momentum from China’s approval of 86 domestic online games in May, while the mainland was pressured after Chinese press reports noted expectations for the PBoC’s benchmark lending rates to remain unchanged for some time and after the US denied it was planning to lift sanctions on China’s defence minister.

Top Asian News

- Chinese press reports stated that the PBoC’s Loan Prime Rates are expected to remain unchanged for some time and noted the LPR faces little downside due to the economic recovery and banks’ tight NIM.

- Russian PM Mishustin said on his visit to China that Russia-China ties will positively impact both countries and 2023 trade turnover between the countries could reach USD 200bln, according to TASS and RIA.

European bourses are pressured, Euro Stoxx 50 -0.5%, with the exception of the FTSE 100 +0.1% which is deriving some support from regional banking names on post-PMI hawkish BoE implications. Back to Europe, bourses came under pressure from the region’s PMIs as it has hawkish ECB implications and with the Manufacturing sector still under marked pressure. Sectors are somewhat mixed with Real Estate bolstered while Luxury names are tarnished after a cautious note from Deutsche Bank. Stateside, futures are essentially flat with the ES pivoting 4200 as we await more substantive debt ceiling updates and remarks from Fed’s Powell. Lowe’s Companies Inc (LOW) Q1 2023 (USD): adj. EPS 3.67 (exp. 3.44), Revenue 22.35bln (exp. 21.6bln); SSS -4.3% (exp. -3.2%); updates outlook

EU is seeking to reimpose a EUR 14.3bln tax demand on Apple (AAPL), via FT; Competition Commissioner Vestager is looking to overturn the EU’s 2020 legal defeat over a tax bill to Ireland.

Top European News

- UK Chancellor Hunt will meet with food manufacturers today to ask for help from the industry to ease the pressure on households and steps up pressure on supermarkets to rein in soaring prices, according to FT.

- Hungary is accelerating discussions with Brussels to release nearly a third of its EU funding after a long stand-off, but officials warned funds will likely remain frozen because of differences over reform efforts, according to FT.

FX

- DXY underpinned after productive US debt ceiling discussions as the index meanders around a Fib at 103.330.

- Yen regains poise with some traction from upbeat Japanese PMIs and USD/JPY running into supply ahead of 139.00.

- Aussie underperforms either side of 0.6650 as iron ore slides and the Yuan depreciates below 7.0000.

- Kiwi loses traction on the eve of RBNZ irrespective of hawkish shift in pricing, with NZD/USD at the lower end of 0.6302-0.6254 bounds.

- Euro keeps tabs on 1.0800 as strength in EZ services counters manufacturing deficiencies, but Pound waning on 1.2400 handle as UK PMIs miss consensus across the board.

- PBoC set USD/CNY mid-point at 7.0326 vs exp. 7.0327 (prev. 7.0157)

Fixed Income

- Debt futures plumb new cycle lows as bearish momentum continues to build.

- Bunds down to 133.69, Gilts 97.22 and T-note 113-09 ahead of US prelim PMIs, new home sales and Fed’s Logan all ahead of USD 42bln 2 year supply.

- Mixed EU PMIs largely shrugged aside along with UK and German auctions awaiting more talks on the US debt ceiling.

Commodities

- Crude benchmarks are in close proximity to the unchanged mark after Monday’s circa. USD 0.40/bbl firmer settlement with the complex focused on Energy Officials at the Qatar Economic Forum.

- Currently, WTI and Brent are incrementally softer and around the mid-point of USD 71.71-72.62/bbl and USD 75.65-76.53/bbl parameters.

- Saudi Energy Minister says I keep telling speculators they will be “ouching” and they did hurt in April, I would tell them to watch out.

- Russian Deputy PM Novak says growth of Russian energy shipments to China at 40% in 2023, via Interfax.

- Spot gold slips as the USD remains underpinned though the yellow metal remains above Friday’s USD 1954/oz trough; base metals similarly dented on the USD and with continued attention on China’s recent sub-par metrics.

Debt Ceiling News

- US President Biden said that he is optimistic they will make some progress on the debt ceiling and that they need a bipartisan agreement and sell it to constituencies, while he added that they need to cut spending and should look at tax loopholes and that the wealthy pay their fair share, according to Reuters. US President Biden later commented that he concluded a productive meeting with House Speaker McCarthy about the need to prevent a default and reiterated once again that default is off the table, while they will continue to discuss the path forward.

- US House Speaker McCarthy said after the meeting with President Biden that he felt they had a productive discussion but don’t have an agreement yet and that staff will continue discussions with negotiators instructed to come back together and find common ground. McCarthy also noted the tone of the conversation was better than any previous time and believes they can get a deal done. Furthermore, he is confident that President Biden wants a deal, while they both agreed that they want to reach an agreement and will talk daily until they get this done.

- White House debt limit negotiators returned to Capitol Hill to resume talks but later declined to comment after the talks concluded for the night, according to Bloomberg.

- US Treasury Secretary Yellen reiterated that debt-limit measures could still run out as soon as June 1st and that it is highly likely cash will run out by early June, according to a statement from the Treasury Department.

- “Sources close to McCarthy said the House could pass a short-term boost if there was a deal and the Treasury Department needed a very brief patch to avoid default, But barring that, don’t expect it to happen”, according to Punchbowl.

Geopolitics

- Twitter source noted a drone attack was said to have targeted the departments of the Ministry of Internal Affairs and FSB in Russia’s Belgorod, while air raid alerts sounded in central and western Ukraine due to Shahed drone activity.

- Russia’s Belgorod regional Governor said a counter-terrorism operation continues and a return to homes in the region’s Gaivoron district is not possible yet, according to Reuters.

- Hungarian PM Orban says the nation will continue to block EU Ukraine aid and the 11th sanctions package; says Ukraine must stop backlisting OTP Bank.

US event calendar

- 08:30: May Philadelphia Fed Non-Manufactu, prior -22.8

- 09:45: May S&P Global US Manufacturing PM, est. 50.0, prior 50.2

- 09:45: May S&P Global US Services PMI, est. 52.5, prior 53.6

- 09:45: May S&P Global US Composite PMI, est. 53.0, prior 53.4

- 10:00: May Richmond Fed Index, est. -8, prior -10

- 10:00: April New Home Sales MoM, est. -2.6%, prior 9.6%

- 10:00: April New Home Sales, est. 665,000, prior 683,000

Central Bank Speakers

- 09:00: Fed’s Logan

DB’s Jim Reid concludes the overnight wrap

Since it’s AI week, it’s probably worth mentioning that there was a very brief selloff in markets yesterday after unconfirmed reports circulated on Twitter about an explosion near the US Pentagon. For all of a few minutes after the US open, that saw the S&P 500 shed around a quarter of a per cent, whilst yields on 10yr Treasuries moved about 4bps lower as well, even though nothing had been officially confirmed. The tweet was deleted shortly after and the Pentagon confirmed that no explosion had taken place, meaning that markets snapped back those moves in short order. But given the suggestions that the initial photo might have been AI-generated, it just shows the potential pitfalls for markets if fake news driven by AI can cause concrete movements in asset prices. That could be a growing issue over the months and years ahead, particularly if the technology is able to provide increasingly convincing images and that’s before we get to deep fakes. Indeed who knows if it’s really us typing this.

Actually typing is a bit more difficult than normal this morning as I burnt my hand yesterday. File this under first world problems but a power cut/surge blew our boiling water tap yesterday. As we don’t have a kettle I had to make a coffee by putting a pan in the oven (normal for our type of oven when cooking). I took it out carefully with the oven glove and then went over to get my cup. In the 10 seconds I was away I forgot the pan was piping hot and picked it up to pour and scolded my hand.

That’s how you maybe prove this isn’t AI as no robot would be so stupid. Anyway, whilst AI might be the long-term focus right now, in the short term the main issue for investors continues to be the debt ceiling, as the clock ticks towards a potential deadline in early June. Last night’s meeting between Biden and McCarthy seemed to be constructive with Speaker McCarthy saying, “The tone tonight was better than any other time we have had discussions” and President Biden adding “that default is off the table and the only way to move forward is in good faith toward a bipartisan agreement.” This meeting came shortly after Treasury Secretary Yellen’s announcement that it was now “highly likely” that the Treasury would run out of cash in early June with a default possible as soon as June 1. Prior to that meeting President Biden and Speaker McCarthy told reporters that a deal needed to get done in the next few days to avoid hitting the debt ceiling, with the latter saying “decisions have to start being made.”

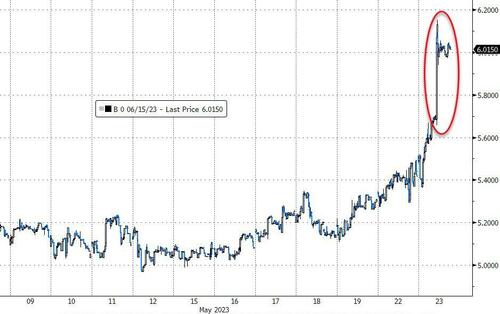

With the issue still not resolved at yesterday’s close, markets grew increasingly alarmed about the potential implications of a default, and yields on short-term T-bills continued to rise. For instance, the 1-month T-bill yield surged by +13.2bps yesterday to 5.46%, which was just under the highs reached early last week. This morning we’ve reversed yesterday’s losses on the overnight headlines from Biden and McCarthy

As investors were focusing on the debt ceiling, US Treasuries came under further pressure from a collection of hawkish Fed speakers yesterday. That started with St Louis Fed President Bullard (non-voter), one of the most hawkish FOMC members, who said that “I think we’re going to have to grind higher with the policy rate”, and that his thinking was for “two more moves this year”. Earlier in the day, Minneapolis Fed President Kashkari (voter) had also sounded open to another hike in June, saying that “I think right now it’s a close call, either way, versus raising another time in June or skipping.” Later on however, San Francisco Fed President Daly (non-voter) didn’t give an obvious signal, saying that there was still a lot of time to collect information ahead of the June meeting.