by harveyorgan · in Uncategorized · Leave a comment·Editi

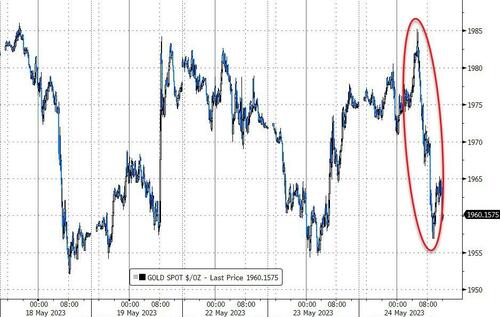

GOLD PRICE CLOSED: DOWN $9.50 TO $1963.25

SILVER PRICE CLOSED: DOWN $0.35 AT $23.13

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1971.75

Silver ACCESS CLOSE: 23.62

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

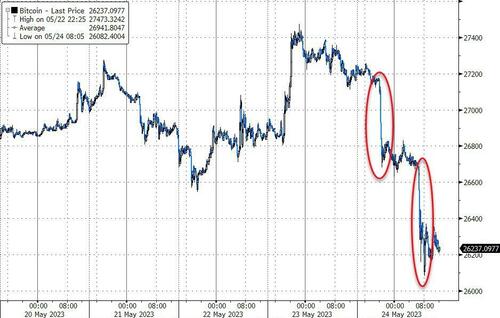

Bitcoin morning price:, $26,716 DOWN 490 Dollars

Bitcoin: afternoon price: $26,239 DOWN 967 dollars

Platinum price closing $1025.95 DOWN $25.90

Palladium price; $1406.50 DOWN $46.35

“Our system is so stinkin’ corrupt that we owe Sodom and Gomorrah an apology.” … Trader Dan Norcini in 2009

GO GATA!

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,662.00 DOWN 4.75 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1583.94 DOWN 6.75 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1821.33 DOWN 12.60 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

ZERO GOLD

JPMorgan stopped 0/0 contracts

FOR MAY:

GOLD: NUMBER OF NOTICES FILED FOR MAY/2023. CONTRACT: 0 NOTICES FOR 700 OZ or 0.0000 TONNES

total notices so far: 6039 contracts for 603,900 oz (18.784 tonnes)

FOR MAY:

SILVER NOTICES: 25 NOTICE(S) FILED FOR 125,000 OZ/

total number of notices filed so far this month : 2554 for 12,770,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP DOWN $9.50..

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//WOW!!

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:///A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD/

INVENTORY RESTS AT 941.29 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 35 CENTS AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV: ; : INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 471.330 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1938 CONTRACTS TO 135,740 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.22 FALL IN SILVER PRICING AT THE COMEX ON TUESDAY. TAS ISSUANCE WAS A STRONG SIZED 636 CONTRACTS. THESE WILL BE USED FOR MANIPULATION NEXT MONTH. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY: A STRONG 636 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THEY VALUE 0 TO A POSITION LIMIT IF A CALENDAR SPREAD OCCURS. IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED THE COMPLAINT IN SIMILAR FASHION TO ALL OF THOSE DEMOCRATIC CRIMES COMMITTED WITH NO ATTENTION GIVEN BY ATTORNEY GENERALS.

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.22). AND WERE UNSUCCESSFUL IN KNOCKING SOME SPEC LONGS AS WE HAD A HUGE LOSS ON OUR TWO EXCHANGES OF 948 CONTRACTS WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 4.250 MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION. WE WILL HAVE IN OUR FINAL WEEK IN THE DELIVERY CYCLE(BEGINNING TOMORROW) MORE MANIPULATION IN OUR PRECIOUS METALS DUE TO COMEX SPREADERS LIQUIDATION WITH AN ADDED FEATURE OF TAS LIQUIDATION.

WE MUST HAVE HAD:

A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 900 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.105 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF 80,000 OZ (QUEUE JUMP RAISES THE AMOUNT OF SILVER STANDING)+0 EXCHANGE FOR RISK// TOTAL 4.25 MILLION OZ OF EXCHANGE FOR RISK FOR THE MONTH(RAISES THE AMOUNT OF SILVER STANDING):THUS TOTAL OF 17.75 MILLION OZ OF STANDING FOR DELIVERY V) HUGE SIZED COMEX OI LOSS/ HUGE SIZED EFP ISSUANCE/VI) HUGE NUMBER OF SHORT T.A.S. CONTRACT INITIATION (636 CONTRACTS)//CONSIDERABLE T.A.S LIQUIDATION MANIPULATING THE PRICE SOUTHBOUND.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -removed 90 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTRACTS for 18 days, total 11,525 contracts: OR 57.625 MILLION OZ . (640 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 57.625 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 57.625 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1938 CONTRACTS DESPITE OUR FAIR SIZED $0.22 LOSS IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 900 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 13.105 MILLION OZ//FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 80,000 OZ (INCREASES THE AMOUNT OF SILVER STANDING) +// + 0.0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //TOTAL EXCHANGE FOR RISK MONTH= 4.25 MILLION//NEW TOTALS 13.500 MILLION OZ + 4.25 MILLION = 17.75 MILLION OZ// .. WE HAVE A HUGE SIZED LOSS OF 1038 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 636!!//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED.

WE HAD 25 NOTICE(S) FILED TODAY FOR 125,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1,425 CONTRACTS TO 479,080 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -66 CONTRACTS

WE HAD A SMALL SIZED DECREASE IN COMEX OI ( 1,425 CONTRACTS) WITH OUR $2.25 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR MAY. AT 3.5085 TONNES ON FIRST DAY NOTICE // PLUS 0 OZ QUEUE JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)/+ /A HUGE ISSUANCE OF 1160 T.A.S. CONTRACTS/STRONG FRONT END OF TAS LIQUIDATION AND TO BOOT: THE FIRST FOR GOLD COMEX: A STRONG 400 EXCHANGE FOR RISK FOR 40,000 OZ OF FUTURE DELIVERY OR 1.244 TONNES////YET ALL OF..THIS HAPPENED WITH OUR $2.25 LOSS IN PRICE WITH RESPECT TO TUESDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 3628 OI CONTRACTS (11.284 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 5043 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 479,148

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3696 CONTRACTS WITH 1,357 CONTRACTS DECREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): 1140 CONTRACTS) AND 5053 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3628 CONTRACTS OR 11.284 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5053 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (1,425) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 3628 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 3.5085 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 0 OZ // NEW STANDING: 19.101 TONNES+ 1.244 TONNES OF EXCHANGE FOR RISK//NEW TOTALS: 20.345 TONNES // ///3) ZERO LONG LIQUIDATION//4) SMALL SIZED COMEX OPEN INTEREST LOSS/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 1140 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 58,972 CONTRACTS OR 5,897,200 OZ OR 183.42 TONNES IN 18 TRADING DAY(S) AND THUS AVERAGING: 3276 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAY(S) IN TONNES 183.42 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 183.42/3550 x 100% TONNES 5.16% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES ( MUCH SMALLER THAN LAST MONTH)

MAY: 183.42 TONNES (HEADING FOR ANOTHER SMALL MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A GIGANTIC SIZED 1938 CONTRACTS OI TO 135,740 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 900 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 900 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 900 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1938 CONTRACTS AND ADD TO THE 900 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1038 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 5.190 MILLION OZ

OCCURRED WITH OUR $0.22 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 41.49 PTS OR 1.28% //Hang Seng CLOSED DOWN 315.32 POINTS OR 1.62% /The Nikkei closed DOWN 275.09 OR 0.89% //Australia’s all ordinaries CLOSED DOWN 0.73 % /Chinese yuan (ONSHORE) closed UP 7.0491 /OFFSHORE CHINESE YUAN DOWN TO 7.0579 /Oil UP TO 74.10 dollars per barrel for WTI and BRENT AT 77.99 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 1425 CONTRACTS DOWN TO 479,080 WITH OUR LOSS IN PRICE OF $2.25 ON TUESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5053 EFP CONTRACTS WERE ISSUED: : JUNE 5053 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5053 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3628 CONTRACTS IN THAT 5053 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED LOSS OF 1.357 COMEX CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $2.25. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE),THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE TODAY WAS A HUGE 1160 CONTRACTS. DURING THIS WEEK THEY SOLD THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE). FOR EXAMPLE WITH TONIGHT’S READING OF TAS, 100% OF ISSUANCE OF T.A.S. WAS JUNE AND AUGUST. TONIGHT WE HAVE A FIRST FOR GOLD: AN ISSUANCE OF A STRONG 400 EXCHANGE FOR RISK CONTRACTS TOTALLING 40,000 OZ OR 1.244 TONNES OF GOLD. EXCHANGE FOR RISK IS A FUTURE DELIVERY CONTRACT WHERE THE BUYER ASSUMES THE RISK THAT THEIR DELIVERY CONTRACT WILL BE ENACTED. (WHAT A BUNCH OF GARBAGE)

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (19.101) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.101 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $2.25) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR FAIR SIZED GAIN OF 3628 CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE TAS LIQUIDATION. IT CONTRAST TO THE LAST FEW MONTHS, THE TAS LIQUIDATION CONTINUES UNABATED. AND NOW WE HAVE EXCHANGE FOR RISK INITIATED FOR GOLD.

WE HAVE GAINED A TOTAL OI OF 11.284 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY. (3.5085 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF NIL oz (0.00 TONNES)//NEW STANDING 19.101 TONNES+1.244 exchange for risk// new total20.345 tonnes ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $2.25

WE HAD +REMOVED 66 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3628 CONTRACTS OR 362,800 OZ OR 11.284 TONNES.

Estimated gold comex today 287,730// fair-good

final gold volumes/yesterday 283,133// FAIR- good

//MAY 24/ MAY 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 385.810 OZ BRINKS 12 KILOBARS . |

| Deposit to the Dealer Inventory in oz | NIL |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 0 notice(s) 0 OZ 0.0000 TONNES |

| No of oz to be served (notices) | 102 contracts 10200 oz 0.3172 TONNES |

| Total monthly oz gold served (contracts) so far this month | 6039 notices 603,900 OZ 18.787 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 1

i) Out of Brinks: 385.810 oz (12 kilobars)

total withdrawals: 385.810 oz

Adjustments; 1 dealer to customer/ JPMorgan

i) Out of JPMorgan: 477,364.254 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 102 contracts having LOST 7 contracts. We had 7 contracts filed

on TUESDAY, so we GAINED 0 contracts or an additional NIL oz (0. tonnes) will stand for gold in this non active delivery month of May

June LOST A HUGE 21,828 contracts DOWN to 140,399 contracts.

July added 122 contracts to stand at 2623 contracts.

AUGUST GAINED 19,749 contracts UP to 280,497 contracts

We had 0 contracts filed for today representing NIL oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2023. contract month,

we take the total number of notices filed so far for the month (6,039 x 100 oz ), to which we add the difference between the open interest for the front month of MAY (102 CONTRACTS) minus the number of notices served upon today 0 x 100 oz per contract equals 614,1200 OZ OR 19.101 TONNES the number of TONNES standing in this NON- active month of May. And now we must add 1.244 tonnes of gold delivery through our 400 contract exchange for risk//new total 20.345 tonnes of gold.

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (6,039 x 100 oz) x 102 OI for the front month minus the number of notices served upon today (0)x 100 oz} which equals 614,100 oz standing OR 19.101 TONNES + 1.244 (exchange for risk) = 20.345 tonnes

TOTAL COMEX GOLD STANDING: 20.345 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,696,563.034 OZ 52.77 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,612,305,124 OZ

TOTAL REGISTERED GOLD: 11,884,414.794 (369,65 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,727,890.420 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,187,851 OZ (REG GOLD- PLEDGED GOLD) 316.885 tonnes//

END

SILVER/COMEX

MAY 24//2023// THE MAY 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 510,619.320 oz CNT JPMorgan Delaware . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 169,641.100 oz Delaware |

| No of oz served today (contracts) | 25 CONTRACT(S) (125,000 OZ) |

| No of oz to be served (notices) | 146 contracts (730,000 oz) |

| Total monthly oz silver served (contracts) | 2554 Contracts (12,770,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into Delaware: 169,641.100 oz

Total deposits: 169,641.100 oz

JPMorgan has a total silver weight: 141.303 million oz/272.161 million =51.94% of comex .//dropping fast

Comex withdrawals 3

i) out of CNT : 120,164.280 oz

ii) Out of Delaware: 7055.440 oz]

iii) Out of JPMorgan: 383,399.600 oz

Total withdrawal: 510,619.320 oz

adjustments: 1//dealer to customer

jpmorgan; 402,893.310 OZ

TOTAL REGISTERED SILVER: 30.195 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 272.161 million oz

CALCULATION OF SILVER OZ STANDING FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2023 OI: 171 CONTRACTS HAVING LOST 8 CONTRACT(S). WE HAD 24 CONTRACTS FILED ON TUESDAY, SO WE GAINED 16 CONTRACTS OR AN ADDITIONAL 80,000 OZ WILL STAND FOR DELIVERY ON THIS SIDE OF THE POND

JUNE HAD A 9 CONTRACT GAIN TO 1124

JULY HAD A 2801 CONTRACT LOSS TO 109,343 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 25 for 125,000 oz

Comex volumes// est. volume today 52,227 fair

Comex volume: confirmed yesterday: 64,827 FAIR

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 2554 x 5,000 oz = 12,770,000 oz

to which we add the difference between the open interest for the front month of MAY(171) and the number of notices served upon today 25 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2023 contract month: 2554 (notices served so far) x 5000 oz + OI for the front month of May (171) – number of notices served upon today (25 )x 500 oz of silver standing for the MAY contract month equates to 13.5000 million oz + THE CRIMINAL 0 MILLION OZ EXCHANGE FOR RISK TODAY//NEW TOTAL EXCHANGE FOR RISK: 4.250//NEW TOTAL 17.75 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 937.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 931.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

GLD INVENTORY: 941/29 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

CLOSING INVENTORY 471.330 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

This is high for Poland: they purchased 15 tonnes of gold last month

(Schiff Gold)

Poland Resumes Buying Gold

WEDNESDAY, MAY 24, 2023 – 06:30 AM

Poland is buying gold again.

The National Bank of Poland added nearly 15 tons of gold to its reserves in April, according to data published by the bank last week. It was the largest increase in the country’s reserves since June 2019 when the bank boosted reserves by almost 100 tons.

The purchase increased the value of Poland’s gold reserves from $14.55 billion to $15.52 billion.

Poland’s official gold holdings rank as the 22nd largest in the world. Gold makes up about 8.5% of the Bank of Poland’s total reserves.

In the fall of 2021, Bank of Poland President Adam Glapiński said the central bank planned to add 100 tons of gold to its reserves in 2022. It’s unclear why the bank didn’t follow through. This recent purchase could signal the beginning of another round of buying to reach that 100-ton goal.

In 2021, Glapiński said holding gold was a matter of financial security and stability.

Gold will retain its value even when someone cuts off the power to the global financial system, destroying traditional assets based on electronic accounting records. Of course, we do not assume that this will happen. But as the saying goes – forewarned is always insured. And the central bank is required to be prepared for even the most unfavorable circumstances. That is why we see a special place for gold in our foreign exchange management process.”

He went on to discuss some of the benefits of gold as a monetary asset.

After all, gold is free from credit risk and cannot be devalued by any country’s economic policy. Besides, it is extremely durable, virtually indestructible.”

Glapiński also hinted that worries about the stability of the US dollar were driving the decision to increase the country’s gold reserves.

Gold is characterized by a relatively low correlation with the main asset classes – especially the US dollar dominating the NBP reserve portfolio – which means that including gold in the reserves reduces the financial risk in the process of investing them.”

The trend toward de-dollarization has only accelerated since Glapiński made these comments.

Poland also repatriated 100 tons of gold from England in 2019.

“The gold symbolizes the strength of the country,” Glapiński told reporters at the time.

Central banks around the world have been piling up gold over the last two years. After a record-setting 2022, central bank gold reserves increased by 228 tons through the first three months of 2023, a Q1 record. This was 38% higher than the previous first-quarter record set in 2013.

Total central bank gold buying in 2022 came in at 1,136 tons. It was the highest level of net purchases on record dating back to 1950, including since the suspension of dollar convertibility into gold in 1971. It was the 13th straight year of net central bank gold purchases.

According to the World Gold Council, there are two main drivers behind central bank gold buying — its performance during times of crisis and its role as a long-term store of value.

It’s hardly surprising then that in a year scarred by geopolitical uncertainty and rampant inflation, central banks opted to continue adding gold to their coffers and at an accelerated pace.”

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

3,Chris Powell of GATA provides to us very important physical commentaries

this is what happens when you go after them with just “spoofing”

(Reuters)

Banks win dismissal of U.S. silver price-fixing suit

Submitted by admin on Mon, 2023-05-22 19:17 Section: Daily Dispatches

By Jonathan Stempel

Reuters

Monday, May 22, 2023

NEW YORK — A U.S. judge on Monday dismissed long-running litigation by investors who accused HSBC Holdings and Bank of Nova Scotia of conspiring to fix silver prices.

U.S. District Judge Valerie Caproni in Manhattan said the investors lacked legal standing to pursue federal antitrust claims under the Sherman Act, or claims under the federal Commodity Exchange Act.

Investors had accused HSBC, Scotiabank, and Deutsche Bank of manipulating silver prices from 2007 to 2013, saying they had “smoking gun” evidence of a price-fixing conspiracy among those banks and several other silver market makers.

The litigation began in 2014 and Deutsche Bank settled for $38 million two years later.

In a 24-page decision, Caproni found the investors unable to trace their losses to banks’ alleged effort to depress the Fix, which set benchmark prices for silver bars, and trade derivatives based on advance knowledge of the Fix price.

Caproni said the investors did not show it was “plausible, as opposed to merely possible” that distorted pricing affected their trades, and said any damages were “too speculative.”

The judge also said the investors were not “efficient enforcers” of their private antitrust claims, unlike people who might have sold silver at the Fix price. …

… For the remainder of the report:

https://www.reuters.com/legal/banks-win-dismissal-us-silver-price-fixing-litigation-2023-05-22/

END

Removal of a 2,000 rupee note (24 dollars worth) spurs purchases of gold and silver

(Hindustan Times/GATA)

India’s withdrawal of 2000-rupee note spurs purchases of gold and silver

Submitted by admin on Mon, 2023-05-22 20:36Section: Daily Dispatches

From the Hindustan Times, Delhi

Monday, May 22, 2023

The demand for bullion saw a sudden jump on Saturday, which dealers in various parts of the country said was expected to continue until people offloaded a bulk of their R2,000 banknotes for gold and silver, even as a rush to exchange the high-value currency notes is expected at banks from Monday.

The Reserve Bank of India on Friday said it was withdrawing from circulation ₹2,000 currency notes introduced seven years ago after demonetisation, resulting in a rush to use the banknotes

People scrambled to buy gold and silver in bulk in bullion markets, leading to increase in prices, dealers in several states said.

“The sale of bullion has shot up after the withdrawal of R2,000 currency notes was announced,” said Vinod Maheshwari, a bullion dealer at Lucknow’s Chowk Sarrafa market. Traders were selling gold and silver at 10% higher rates to those paying with R2,000 notes, he said, adding that there was no significant increase in the rates of jewellery. …

… For the remainder of the report:

* * *

4. OTHER GOLD/SILVER RELATED COMMENTARIES/…

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: COFFEE/ROBUSTA

Viet Nam and Indonesia huge coffee producers are experiencing extreme weather and that could affect coffee production. This is huge coffe prices are more than decade highs.

(zerohedge)

Robusta Prices Hit 12-Year High As El Niño Threat Sparks Shortage Fears

WEDNESDAY, MAY 24, 2023 – 04:15 AM

Vietnam and Indonesia are experiencing extreme weather that could affect coffee production. This has pushed robusta coffee prices to more than decade highs. An emerging El Nino ahead of a Northern Hemisphere summer could worsen coffee production at the end of the Northern Hemisphere growing season later this year.

Over the last few months, we’ve followed the emerging El Nino weather pattern. We’ve noted the following:

- ‘Triple-Digit’ La Nina Ending As El Nino May Strike Soon

- “We’ve Been Warned”: El Nino Watch Initiated As Ag-Industry In Crosshairs

- Is El Nino Supercharging Heatwave Across Asia?

- NASA Satellite Spots Large Wave Rolling Across Pacific As El Niño Likely Coming

Bloomberg said:

An emerging El Niño weather pattern will curb output from top supplier Vietnam, bringing hotter, drier conditions later this year. Indonesia, the No. 3 producer, had its crops harmed by excessive rainfall, with the US Department of Agriculture forecasting an 18% decline in output for the new season that started in April. That prospect pushed up prices again on Monday with crops in another key grower Brazil already hurt by drought.

As a result of adverse weather conditions in top-producing robusta growing countries, prices of the coffee bean have soared to 12-year highs.

Over the last year and a half, the cost-of-living squeeze has pushed more consumers to cheaper robusta beans versus high-quality arabica beans.

“There’s been so much of a demand shift away from higher-priced coffee that even the market isn’t even being satisfied by higher robusta exports,” said Judith Ganes, who runs a commodities firm in New York.

For coffee drinkers, the low-cost robusta bean is set to become even more expensive as a shortage worsens this summer. There doesn’t seem to be an immediate end to breakfast inflation.

end

5 B GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS// WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.0491

OFFSHORE YUAN: 7.0579

SHANGHAI CLOSED DOWN 41.49 PTS OR 1.28%

HANG SENG CLOSED DOWN 315.32 PTS OR 1.62%

2. Nikkei closed DOWN 275.09 PTS OR 0.89%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 103.49 EURO RISES TO 1.0775 UP 6 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.405 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 138.37 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.4285***/Italian 10 Yr bond yield FALLS to 4.293*** /SPAIN 10 YR BOND YIELD FALLS TO 3.492…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.863

3j Gold at $1981.85 silver at: 23.46 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 21 /100 roubles/dollar; ROUBLE AT 59.92//

3m oil into the 74 dollar handle for WTI and 77 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 138.37 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .405% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9028 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9728 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.674 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 3.927 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.281 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.89…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.2336 UP 8 BASIS PTS (RATES RISING RAPIDLY)

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Slide, European Stocks Tumble On Barrage Of Global Bad News

WEDNESDAY, MAY 24, 2023 – 08:07 AM

US equity futures drift drift lower for the second day following a deluge of bad news across global markets driving European stocks to their biggest drop in two months, pushing copper below $8,000 and snuffing out this year’s gains in China equities. As of 730am ET, S&P futures were down 0.4% to 4,143 following Tuesday’s 1.1% drop with Nasdaq futures sliding the same amount. Treasury yields are flat trading around 3.67%, the USD is slightly stronger, and bitcoin got the usual Asian session trapdoor as gold rose. Commodities are mixed: energy rallied (WTI + 2.1%) while metals are falling on concerns about China’s fading recovery. Yesterday, we saw de-risking in crowding stocks with Momentum Winners and MegaCap Tech being the biggest laggards. On debt ceiling negotiation, two parties have not come to an agreement. Today, we will receive the FOMC Minutes at 2pm ET; AI-leader Nviidia reports after the close.

In premarket trading, megacap tech was mixed with MSFT and AMZN recovering, while the rest are lower. Nvidia Corp., a stock at the center of the artificial intelligence frenzy, lost almost 1%. Regional banks are mostly higher as Pacwest continues to sell more assets to meet liquidity needs (why this is positive remains unclear) while large-cap banks lagging. Here are the most notable premarket movers:

- Palo Alto Networks rose as much as 4.6% in premarket trading, after the network security company reported third- quarter results that beat expectations on key metrics. It also raised the low end of its full-year revenue forecast.

- Agilent shares sink 8.8% in premarket trading after the life sciences company cut its adjusted earnings per share guidance for the year to a level below the average analyst estimate.

- US- listed stocks of Shopify fell as much as 2.1% in premarket trading, after BNP Paribas Exane cut its recommendation on the Canadian e-commerce company to underperform from neutral. It said there are “better opportunities elsewhere,” given the company’s valuation relative to expected sales growth.

- Urban Outfitters gains as much as 12% in US premarket trading after the retailer reported better-than-expected fiscal first-quarter net sales. The results prompted analysts to raise their price targets on the stock as strength at Anthropologie and Free People offset soft sales for its namesake brand.

- PacWest shares rose as much as 9.8% in premarket trading on Wednesday, poised to extend gains for a third session in a row, after the troubled US regional lender agreed to sell its Civic Financial Services unit to real estate lending firm Roc360 as part of efforts to bolster liquidity.

- View shares jumped 15% in postmarket trading after CEO Rao Mulpuri disclosed the purchase of 47,468 shares.

- Intuit shares dropped 5% in extended trading before rebounding in premarket trade after the tax-preparation software company reported third-quarter revenue that was weaker than expected.

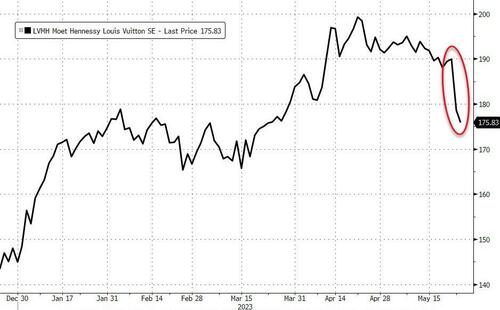

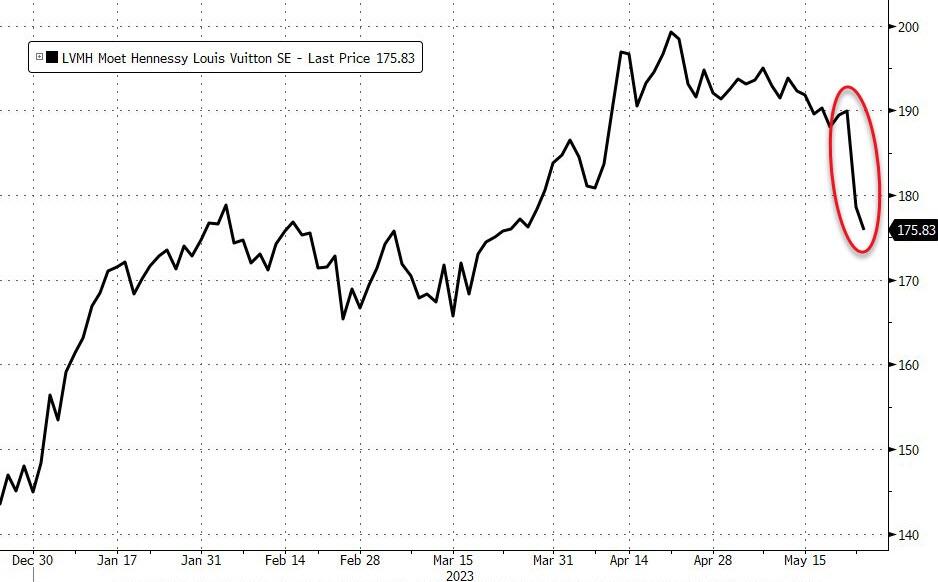

There were plenty of reasons for investors to be pessimistic according to Bloomberg: in the US, there was little progress in debt-ceiling talks and investors are increasingly worried about a default. Yields on securities maturing June 6 topped 6% Tuesday, compared with bills maturing May 30 that are yielding about 2%. China’s sputtering economy and worsening geopolitical ties also hurt sentiment, and UK inflation came in higher than all economist predictions setting the stage for painful encounter with stagflation. Meanwhile, as discussed earlier, Europe’s luxury bubble indeed appears to be bursting as Luxury stocks, one of this year’s most popular trades, extended losses, with LVMH and Gucci owner Kering SA sliding about 2%. European real estate and carmakers slumped on concern that UK interest rates are heading higher.

“Right now we’re defensively positioned,” said Janet Mui, head of market analysis at RBC Brewin Dolphin, in an interview on Bloomberg TV. “We expect a US recession. We have pushed back the date of that recession to 2024 but we think it’s inevitable. Interest rates will stay high in the US, contrary to what the market is currently pricing, so I think that is negative for the economy and corporate profits. This will drive equity markets lower.”

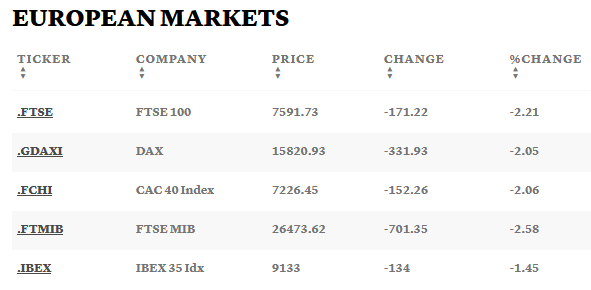

In Europe stocks are firmly in the red as investors contemplate the prospect of additional monetary policy tightening. The Stoxx 600 Index lost 1.7%, the biggest intraday loss since March 24 as gilts slid, lifting the yield on the 10-year note was up five basis points at 4.21% following a blazing hot UK CPI print; travel, autos and consumer products the worst-performing sectors. Here are the most notable European movers:

- Marks & Spencer rise as much as 12% after the UK retailer reported FY23 earnings and said it plans to reinstate its dividend. The results “positively smashed” expectations, according to Shore Capital

- Sinch gains as much as 6.7% after JPMorgan raised the cloud communications firm to overweight, saying the group now sits at an attractive re-entry point following its selloff since January highs

- Mediobanca jumps as much as 3.6%, making it the best performer on the Stoxx 600 Financial Services Index, after the investment bank unveiled new profitability and remuneration targets

- SSE shares climb as much as 2.7% to the highest in a year, after the utility’s raised guidance exceeded expectations, according to Morgan Stanley

- Deliveroo shares rise as much as 6%, the most in almost 11 weeks, after Morgan Stanley upgraded the firm to overweight, saying it remains “fundamentally bullish” on the food-delivery sector

- Intertek rises as much as 2.9% after the testing and inspection company gave a trading update. The company is the top performer on the Stoxx 600 industrials index, which is down 1.9% on Wednesday

- Embracer shares plunge as much as 44% as the Swedish video-game maker slashed its full-year profit target after a planned partnership worth more than $2 billion in revenue fell through

- LondonMetric shares drop as much as 10% after the UK REIT’s update was not enough to offset broader declines among housebuilders on Wednesday as inflation remained stronger than expected

- UK homebuilders fall on Wednesday, with their shares among the worst performers in the FTSE 100 and FTSE 250, as Britain’s inflation rate remained much stronger than expected

“Inflation continues to dominate – from boardrooms to shop floors – especially after stickier than expected UK inflation cemented bets of more BoE rate hikes ahead,” said Angeline Ong, a financial analyst at IG Group.

Asian stocks were mostly lower following the negative lead from Wall St where sentiment was weighed on by the ongoing debt limit impasse with just 9 days left to the X-date and amid US-China frictions after the US House China Select Committee Chair called for retaliation against China’s ban on Micron.

- Hang Seng and Shanghai Comp. were lower amid US-China frictions after the White House spoke out against the Micron ban, while a lawmaker called for the Commerce Department to add Changxin Memory Technologies to the entity list and ensure no US export licenses are granted to firms operating in China which are used to backfill Micron.

- Nikkei 225 was pressured after its recent pullback to beneath the 31,000 level despite reports that the government is to consider childcare handouts for those up to 18 years old, while the first positive reading this year in the monthly Reuters Tankan manufacturing survey did little to spur risk appetite.

- NZX 50 was underpinned after a dovish RBNZ rate hike which signalled the end of its rate increases.

- ASX 200 declined with the resilience in the commodity-related sectors offset by weakness across the broader market and after the Westpac Leading Index remained depressed.

- India’s S&P BSE Sensex fell 0.3% to 61,773.78 as of 03:45 p.m. in Mumbai, while the NSE Nifty 50 Index declined by a similar measure. The retreat was their biggest since May 17. All but three of the 10 Adani Group stocks ended with losses on Wednesday with the flagship unit Adani Enterprises falling the most since March 28 on profit taking following recent sharp rally. HDFC Bank contributed the most to the index’s decline, falling 1.3%. Out of 30 shares in the Sensex index, 16 rose, while 14 fell.

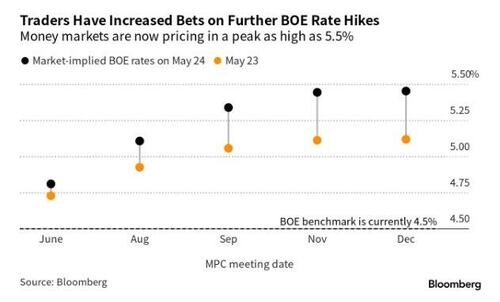

In FX, the Bloomberg dollar index is unchanged erasing an earlier spike. Sterling extends gains in the immediate aftermath after UK CPI came in hotter than the highest estimate, but has since turned lower versus the greenback. The New Zealand dollar dropped as much as 1.3% after the central bank unexpectedly signaled that no further policy tightening will be needed. Policymakers hiked interest rates to 5.5%, in line with projections.

- GBP/USD was up by as much as 0.5% to 1.2470, after hitting a one-month low Tuesday, before reversing gains.

- NZD/USD fell as much as 1.9% to 0.6131 after theReserve Bank of New Zealand said it sees rate cuts starting in the third quarter of next year after lifting the policy rate to 5.5% as expected.

- EUR/SEK jumped as much as 0.5% to 11.4966, the highest since March 2009, as global stocks extended an earlier sell off.

In rates, Treasuries were slightly richer across the curve after unwinding early losses that were spurred by selloff in gilts following upside surprise by UK inflation data. Subsequently 2-year UK yields remained higher by around 20bp into early US session, sharply underperforming among core European rates. US 10-year yields around 3.675%, richer by ~2bps vs Tuesday close and outperforming gilts by 7bp in the sector; long-end slightly outperforms, flattening 5s30s spread by ~1.5bp ahead of belly supply at 1pm New York time. The 10-year UK bond yield jumped as much as 21 basis points to 4.37%, the highest since October, after data showed the UK inflation rate at 8.7% in April, higher than any of the 36 estimates from economists or the 8.4% forecast by the central bank. UK money markets priced in a peak BOE rate of as high as 5.5%, compared with around 5.1% on Tuesday. Back in the US, there is a $43bn 5-year note auction follows strong demand for Tuesday’s 2-year sale, which stopped 1.5bp through the WI level. WI 5-year around 3.702% is ~20bp cheaper than April’ stop- out, which. US session highlights include 5-year note auction and FOMC minutes release.

In commodities, metals were broadly lower. A new wave of Covid is threatening to set back the country’s economy, and investors have been rattled by Beijing’s move to ban purchases of Micron Technology Inc.’s products. Crude futures meanwhile extended their recent advance with WTI rising 2% to trade near $74.40. Spot gold is little changed around $1,975.

Bitcoin fell 1.6%, back under $27K, under pressure as the risk tone remains downbeat as the clock ticks down to the US X-date.

Looking to the day ahead now, and we’ll get the release of the Fed’s minutes from their last meeting in May. Other central bank speakers will include ECB President Lagarde, BoE Governor Bailey and the Fed’s Waller. Data releases include the UK CPI reading for April and Germany’s Ifo business climate indicator for May.

Market Snapshot

- S&P 500 futures down 0.2% to 4,149.25

- MXAP down 0.7% to 160.95

- MXAPJ down 0.9% to 509.11

- Nikkei down 0.9% to 30,682.68

- Topix down 0.4% to 2,152.40

- Hang Seng Index down 1.6% to 19,115.93

- Shanghai Composite down 1.3% to 3,204.75

- Sensex down 0.2% to 61,841.41

- Australia S&P/ASX 200 down 0.6% to 7,213.80

- Kospi little changed at 2,567.45

- STOXX Europe 600 down 1.5% to 459.11

- German 10Y yield little changed at 2.47%

- Euro up 0.1% to $1.0782

- Brent Futures up 1.1% to $77.68/bbl

- Gold spot down 0.0% to $1,974.48

- U.S. Dollar Index little changed at 103.51

Top Overnight News

- New Zealand’s central bank on Wednesday signaled it was done tightening after raising rates by 25 basis points to the highest in more than 14 years at 5.5%, ending its most aggressive hiking cycle since 1999. RTRS

- US and China will attempt to stabilize relations with a dinner scheduled for Thurs between Commerce Sec Gina Raimondo and her Chinese counterpart. WSJ

- China downplays the Micron ban with the gov’t signaling it’s an isolated incident and not part of a broader crackdown on foreign companies. However, a senior Republican member of the House called on the Commerce Dept. to add Chinese memory maker Changxin Memory to the US blacklist in retaliation for the Micron ban announced Sunday. SCMP / RTRS

- The chief executive of Nvidia, the world’s most valuable semiconductor company, has warned that the US tech industry is at risk of “enormous damage” from the escalating battle over chips between Washington and Beijing. FT

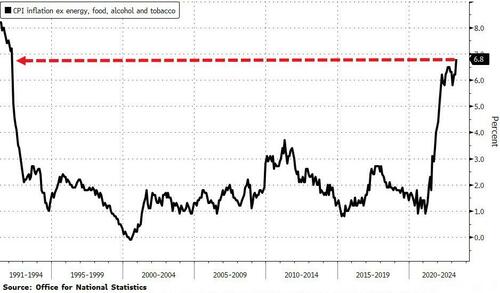

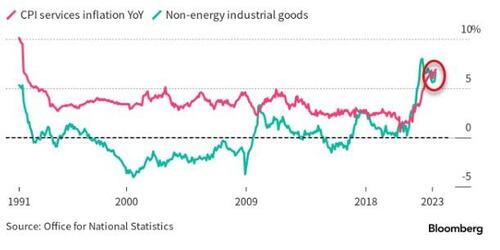

- UK’s inflation overshoots the Street consensus, with headline CPI coming in at +8.7% (down from +10.1% in March, but above the Street’s +8.2% forecast) and core CPI coming in at +6.8% (up from +6.2% in March and above the Street’s +6.2% forecast). RTRS

- Mexico’s President Andrés Manuel López Obrador said his administration is considering buying Citigroup’s local retail-banking unit, Banamex, which the U.S. financial giant put up for sale last year. WSJ

- Speaker Kevin McCarthy left the US Capitol late Tuesday afternoon saying the two parties had yet to reach a deal to avert a first-ever US default, and a top lieutenant said there are no more meetings planned. Republican Representative Garret Graves, one of McCarthy’s chief negotiators, suggested just hours after a two-hour meeting in the Capitol with his White House counterparts that the two sides were at a standoff. BBG

- The Cayman Islands Monetary Authority has engaged lawyers to assess its legal options after deposits at Silicon Valley Bank’s branch in the territory were seized by the Federal Deposit Insurance Corp., a government official told affected depositors. WSJ

- US regional banks are rushing to exploit rules that allow depositors to hold tens of millions of dollars in insured accounts, offering security far exceeding government-backed insurance to soothe clients unnerved by the recent banking turmoil. FT

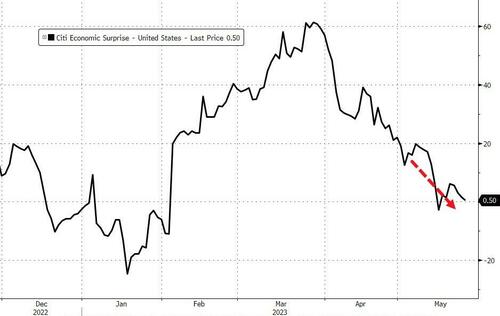

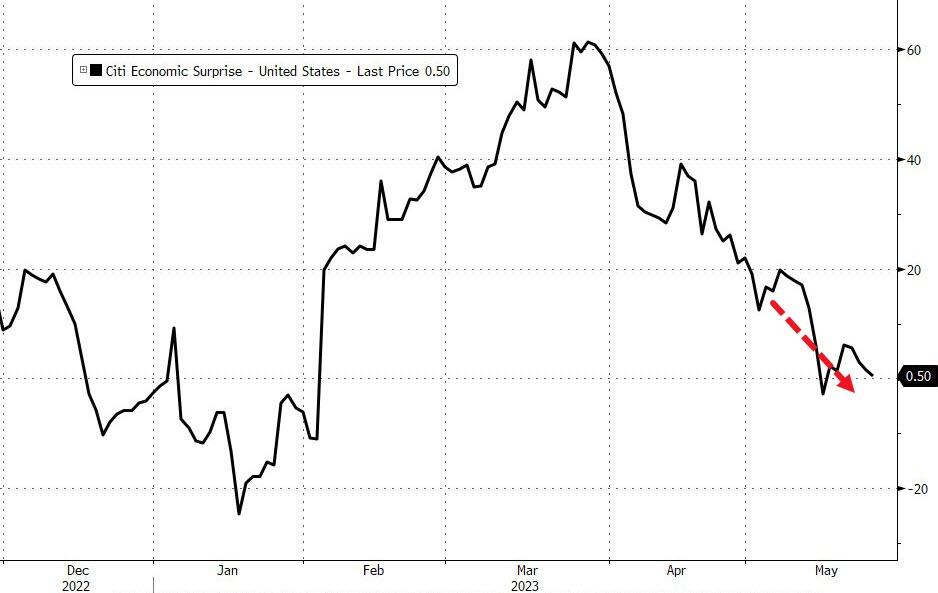

- US economic surprise index collapsing over the last 3 months… (measures eco data surprises relative to market expectations…positive reading means data releases have been stronger than expected and vice versa)

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly lower following the negative lead from Wall St where sentiment was weighed on by the ongoing debt limit impasse with just 9 days left to the X-date and amid US-China frictions after the US House China Select Committee Chair called for retaliation against China’s ban on Micron. ASX 200 declined with the resilience in the commodity-related sectors offset by weakness across the broader market and after the Westpac Leading Index remained depressed. NZX 50 was underpinned after a dovish RBNZ rate hike which signalled the end of its rate increases. Nikkei 225 was pressured after its recent pullback to beneath the 31,000 level despite reports that the government is to consider childcare handouts for those up to 18 years old, while the first positive reading this year in the monthly Reuters Tankan manufacturing survey did little to spur risk appetite. Hang Seng and Shanghai Comp. were lower amid US-China frictions after the White House spoke out against the Micron ban, while a lawmaker called for the Commerce Department to add Changxin Memory Technologies to the entity list and ensure no US export licenses are granted to firms operating in China which are used to backfill Micron.

Top Asian News

- China’s new ambassador to the US Xie said US-China relations face serious difficulties and hopes the US will get back on the right track, while he added that they will seek to enhance China-US exchanges and cooperation.

- RBNZ hiked the OCR by 25bps to 5.50% as expected, while it maintained the peak rate forecast at 5.50% and noted that the OCR is set to remain restrictive for the foreseeable future. RBNZ said the level of interest rates is constraining spending and inflation and it forecasts negative GDP growth in Q2 and Q3. Furthermore, the rate decision was made by a majority of five votes to two and the Committee discussed the suitability of a pause or a 25bps hike.

- RBNZ Governor Orr said during the press conference that the newest data is satisfactory after a long battle and noted it was the first time the Monetary Policy Committee voted on the decision, while he added that they have seen inflation, core inflation and inflation expectations come down, but as a cautious central bank, they are foreshadowing keeping restrictive monetary policy for some time.

- RBA Official Jacobs says the balance sheet is starting to unwind pandemic bond purchases, around AUD 20bln of purchased bonds have matured, pace will increase to circa. AUD 35-45bln/year. Click here for more detail.

European bourses are pressured as headwinds mount, Euro Stoxx 50 -1.6%; attention on debt talks, UK CPI, poor Ifo, US-China tensions and continued luxury sector downside. Sectors are pressured across the board with Real Estate lagging on hawkish BoE pricing while Luxury names continue to slip with analysts citing an MS luxury conference pointing to relatively more subdued performance in the US. US futures are softer but much more contained as we await more concrete developments on the debt ceiling, ES -0.2%, with updates this morning via multiple journalists skewed to the downside overall on a near-term agreement.

Top European News

- ECB President Lagarde reiterates the ECB will bring rates to sufficiently restrictive levels and keep them at those levels for as long as necessary.

- BoE Governor Bailey says banks are exposed to climate related hazards.

- EU banks are reportedly to sail through early rounds of stress tests, according to Bloomberg.

- German economy is expected to grow modestly on Q2 as a rebound in industry offset stagnating household consumptions, according to the Bundesbank monthly report.

FX

- DXY is firmer and towards highs after spending much of the morning trading on either side of the psychological 103.50 level ahead of the FOMC minutes.

- NZD experienced a significant drop after the RBNZ signalled an end to its tightening cycle in what was a dovish hike.

- AUD slipped and remains soft in tandem with the broader risk tone and losses across base metals.

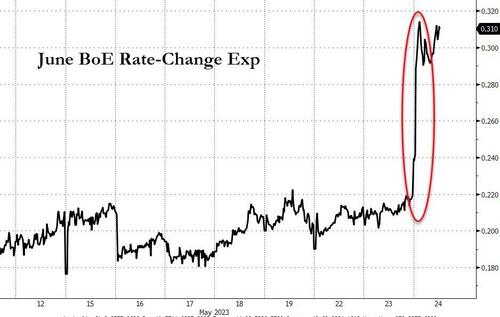

- GBP was briefly lifted following the hotter-than-expected UK inflation data which solidified the case for a June BoE hike.

- PBoC set USD/CNY mid-point at 7.0560 vs exp. 7.0556 (prev. 7.0326)

Fixed Income

- Gilts gapped lower to sub-95.00 following hotter-than-expected UK CPI, with market pricing now implying 75bp of further tightening.

- Given this, EGBs/USTs spent the morning underwater but have since made their way back into positive territory as attention returns to the US debt ceiling, with USTs and Bunds now incrementally firmer.

- For reference, the morning’s dual-tranche German supply was well received overall, particularly when taking into account that the morning’s marked concession had largely evaporated by the time the auction commenced.

Commodities

- WTI and Brent July futures are firmer intraday with the complex seemingly underpinned following commentary from the Saudi Energy Minister yesterday.

- Spot gold resides around USD 1,975/oz in a near-USD 10/oz range in the run-up to the FOMC.

- Base metals are softer across the board amid the demand implications from a weaker-than-expected Chinese rebound coupled with the state-side jitters on the debt ceiling front.

- US Energy Inventory Data (bbls): Crude -6.8mln (exp. +0.8mln), Cushing +1.7mln, Gasoline -6.4mln (exp. -1.1mln), Distillate -1.7mln (exp. +0.4mln).

- Russian watchdog says it is prepared to support restrictions on petrol exports, via Ifx. Subsequently, Russian Energy Minister says we are considering restriction on gasoline exports and not a ban.

Debt Ceiling headlines

- White House said invoking the 14th Amendment to work around the debt ceiling won’t “fix the current problem” but wouldn’t shut the door entirely on pursuing the strategy if they can’t reach a deal, according to USA Today.

- US GOP Rep. Graves said they don’t have additional meetings set up and noted there are some areas where they are very close although there are still substantial gaps including over the debt limit duration.

- Fox’s Pergram tweets “Unclear where debt ceiling talks stand today. Talks have continued. But there has yet to be a breakthrough”.

- US Democrats have reportedly criticised Republican negotiators for seeking an increase in military spending in debt ceiling discussions, via WSJ citing sources; some in the admin. reportedly struggling to see a path forward in the discussions

- Punchbowl News, on the US debt ceiling talks, says “with no deal imminent, McCarthy has signalled that he’d likely send lawmakers home Thursday evening, anticipating that negotiations will drag into next week.”

- White House and Republicans are expected to resume debt talks today, according to Reuters sources.

Geopolitics

- Russian PM Mishustin, in Beijing, says relations between Russia and China are at an unprecedented high level. Adding, Xi’s Russia visit in March was another confirmation of the “special” nature of bilateral relations. Subsequently echoed by Chinese President Xi.

- Russian Foreign Minister Lavrov (according to a translated tweet) says that increasing Western involvement in Ukraine will lead to nuclear war.

- Russia’s Deputy Foreign Minister says F-16s will be a “legitimate target” for Russia if supplied to Ukraine, according to RIA.

US Event Calendar

- 07:00: May MBA Mortgage Applications, prior -5.7%

- 14:00: May FOMC Meeting Minutes

Central bank speakers

- 12:10: Fed’s Waller Discusses the Economic Outlook

- 14:00: May FOMC Meeting Minutes

DB’s Jim Reid concludes the overnight wrap

AI hasn’t yet been able to solve the debt ceiling problem and markets struggled yesterday, with front end bonds and equities selling off together as investors grew increasingly concerned about the debt ceiling. It’s true that both sides are still talking and the mood music sounds (mostly) positive, but we might only be days away from the deadline in early June, and any deal that’s reached is still going to need to be passed through both houses of Congress. So there are real concerns that this could go right down to the wire, and investors are slowly gearing up accordingly. There’s also been talk about whether a short-term extension might now be needed to get this over the line, but for the time being, Speaker McCarthy has continued to downplay the prospect that will happen. So investors continue to wait nervously with no signs of a deal emerging just yet.

When it came to the last 24 hours, it was reported by Punchbowl News that McCarthy had told Republicans in a closed-door meeting that “we are nowhere near a deal yet”. But later on, McCarthy told reporters that a deal could still be reached by June 1. By last night, GOP Representative Graves, who has been one of McCarthy’s lead negotiators, said some progress had been made but then added that “we’re going to have to see some movement or some fundamental change in what they’re doing,” and that there was not an additional meeting currently set up. House Majority Leader Scalise also questioned how the June 1st x-date was calculated, which prompted markets to believe the two sides were still some ways apart. Speaker McCarthy has said he would not waive a rule allowing Congress to review a bill for 3 days before a vote, if he holds that line it will further compress the timetable to get a deal done before early-June.

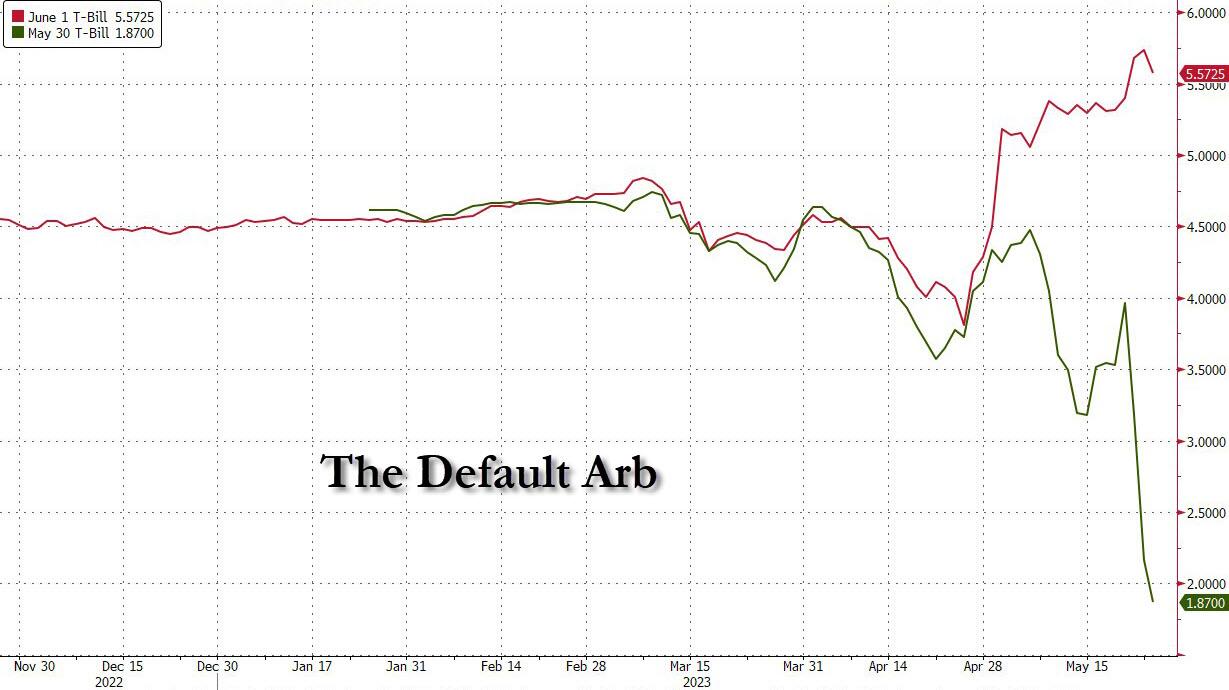

Those issues surrounding the debt ceiling have put serious pressure on US Treasuries over recent days. At the front end, yesterday a Treasury auction of a 21-day cash management T-bill yielded 6.2%, which is above what last week’s 4W bill received (5.84%). The bill is due June 15 and would fully capture Treasury Secretary Yellen’s projected x-date period of “early-June”, furthermore there is an expected influx of corporate tax revenue around that date and so the risk of default remains very much prior to that point. That said there is typically lower demand for the cash management bills than benchmark issues but the fact remains that we have not seen a 6-handle on US Treasury security since 2000 when 2, 10 and 30yrs traded at that level.

In terms of other benchmarks, the 1M and 3M US T-bills were flat after a late rally with the latter rising marginally (+0.2bps) to a fresh post-2001 high of 5.226% – eclipsing last Thursday’s close. And when it came to longer maturities, rising 10yr Treasury yields ran out of steam after having risen for 7 consecutive session as they fell back -2.3bp, taking them to 3.692%. They did hit 3.75% earlier in the session but risk-off seemed to provide a bid after Europe went home. Overnight, they are -1.2bps lower at 3.68% as I type.

Whilst investors might be worried about a US default, another factor behind those Treasury declines has been growing scepticism that the Fed are actually going to cut rates this year. Indeed, only yesterday we got some better-than-expected data from the US, since the flash composite PMI hit a 13-month high in May of 54.5 (vs. 53.0 expected). Then 15 minutes later, the data on new home sales for April came in 683k on an annualised basis (vs. 665k expected), which was also a 13-month high. So that added to the signs that the economy was proving resilient as we move deeper into Q2, and helped to push back fears of an imminent recession.

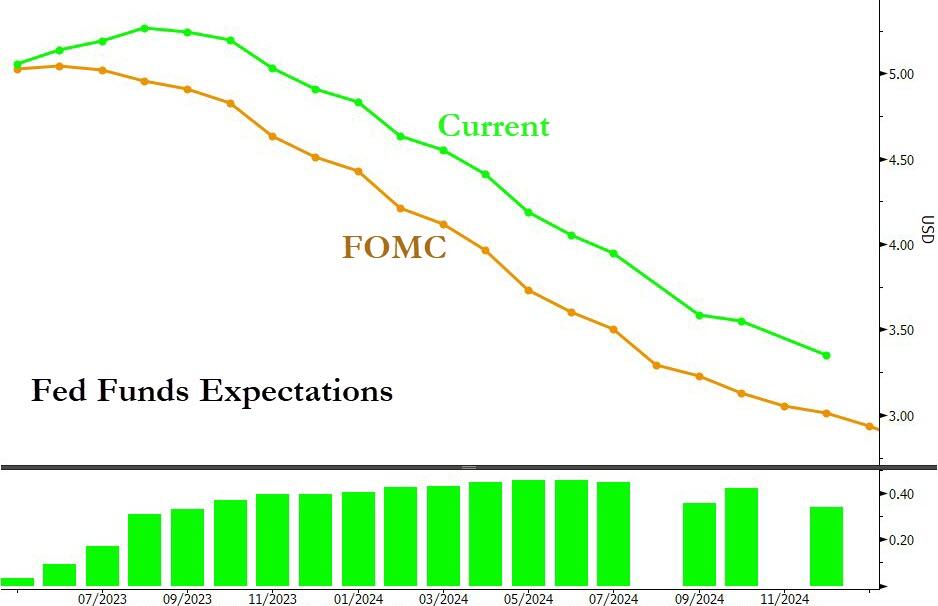

With that strong data in hand, investors dialled back their expectations for rate cuts from the Fed over the course of 2023. For instance, the rate priced in by the December meeting was up another +1.2bps to 4.71%, which is its highest level since SVB’s collapse in early March. Bear in mind that on March 15, when the market turmoil was at its height, the rate expected in December hit a closing low of 3.75%, so we’ve now recovered a full 100bps from that point, which shows how the market has increasingly put that turmoil behind it. And although fears about the debt ceiling are rising, the underlying base case for investors is still that a deal or an extension will be agreed as on previous occasions, allowing investors to look through this current crisis too.

For equities, the tone was downbeat yesterday as the S&P 500 finished near the lows of its daily trading range down -1.12%. The NASDAQ largely matched the broader index, falling -1.26% yesterday, with megacap tech stocks giving way in the US afternoon as the FANG+ index (-1.29%) saw its largest pullback in nearly a month. Look out for Nvidia’s (-1.57%) earnings after the bell today. The stock (up +110% in 2023) is the fifth largest in the S&P 500 and now has a market cap of $758.9bn, which for context is double the biggest company in the Stoxx 600 (Nestle – EUR 310bn) and nearly 5x larger than the biggest corporate in the DAX (SAP – EUR 151bn).

The tone was a bit better in Europe given the late selloff in the US, and the STOXX 600 fell -0.60%, whilst the CAC 40 (-1.33%) saw the biggest underperformance as luxury good stocks struggled. That came as the flash PMIs were broadly in line with consensus across the continent, with the composite Euro Area print at 53.3 (vs. 53.5 expected).

Sovereign bonds in Europe broadly followed the US, with yields on 10yr bunds (+1.0bps), OATs (+0.1bps) and BTPs (+0.7bps) rising on the day. The big underperformer were UK gilts however, where 10yr yields (+9.4bps) rose to their highest level since Liz Truss was PM last October, at 4.158%. That followed comments from BoE officials before MPs, including Governor Bailey who said that “there are risks of persistence” on inflation. Meanwhile Catherine Mann, the most hawkish member of the MPC, commented that “tightening and tight are not the same” and said “real rates are still below zero”. That prompted investors to dial up their expectations for rate hikes over the months ahead, with terminal now priced above 5%. Keep an eye out for the April CPI release shortly after this goes to press as well, where the headline reading is expected to come out of double-digits (8.2% expected vs. 10.1% last month) as last year’s spike in energy prices drops out of the annual comparison.

Speaking of inflation, there was some further good news from Europe as natural gas prices fell to their lowest level in nearly 2 years. That was thanks to a -1.97% decline yesterday, taking futures down to €29.13/MWh, which also leaves prices on track for their 8th consecutive weekly decline. It’s true that Brent crude oil prices (+2.17%) hit a 2-week high yesterday of $77.64/bbl. But more broadly the trend for commodities has been continuously lower over recent months, and Bloomberg’s Commodity Spot Index fell to its lowest level since December 2021.