I HAD A CRASH JUST BEFORE POSTING AND I LOST EVERYTHING

I PUT THE COMEX DATA BACK

AND THE MAJOR STORIES OF THE DAY

I HOPE EVERYTHING WILL BE OK FOR TOMORROW

THE 4 OCLOCK DATA IS ACCURATE

H

GOLD PRICE CLOSED: DOWN $19.70 TO $1914.45

SILVER PRICE CLOSED: DOWN $0.34 AT $22.45

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1913.10

Silver ACCESS CLOSE: 22.30

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $28,887 UP 995 Dollars

Bitcoin: afternoon price: $30,009 UP XXX dollars

Platinum price closing $926.28 DOWN $15.45

Palladium price; $1282.20 DOWN $67.00

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,516.75 DOWN 11.62 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1501.30 DOWN 12.20 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1746.45 DOWN 12.1 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

JPMorgan stopped 102/198 contracts

FOR JUNE:

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2023. CONTRACT: 198 NOTICES FOR 19800 OZ or 0.6158 TONNES

total notices so far: 19,857 contracts for 1,985,700 oz (61.76 tonnes)

FOR JUNE:

SILVER NOTICES: 0 NOTICE(S) FILED FOR NIL OZ/

total number of notices filed so far this month : 423 for 2,115,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $19.70

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

/NO CHANGES IN GOLD INVENTORY AT THE GLD:////

INVENTORY RESTS AT 934.03 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 34 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ????? A MASSIVE DEPOSIT OF 5.784 MILLION OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 468.967 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 4130 CONTRACTS TO 148,503 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR GIGANTIC $0.40 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. TAS ISSUANCE WAS A HUMONGOUS SIZED 1367 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH . CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 1317 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.40). BUT WERE SUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD AN ATMOSPHERIC LOSS ON OUR TWO EXCHANGES OF 2330 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 13.370 MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

A HUMONGOUS ISSUANCE OF EXCHANGE FOR PHYSICALS( 1800 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.935 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP + 0 MILLION OZ EXCHANGE FOR RISK(ISSUED TODAY: TOTAL ISSUED SO FAR: 13.370 MILLION OZ)// TOTAL STANDING FOR THE MONTH 4.270 MILLION OZ + 13.370 MILLION EXCHANGE FOR RISK = 17,640 MILLION OZ// ) // HUGE SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/VI) STRONG NUMBER OF T.A.S. CONTRACT ISSUANCE (1800 CONTRACTS)//

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –XXX CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTRACTS for 14 days, total 16,937 contracts: OR 84.685 MILLION OZ (1207 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 84.685 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 84.685 MILLION OZ//MUCH LARGER THAN LAST MONTH

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4130 CONTRACTS WITH OUR LOSS IN PRICE OF $0.40 IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 1800 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.935 MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP+ 0 MILLION EXCHANGE FOR RISK TODAY + 13.37 MILLION EXCHANGE FOR RISK(PRIOR)//NEW TOTAL STANDING: 17.640 MILLION OZ////// .. WE HAVE AN ATMOSPHERIC SIZED LOSS OF 2330 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 1387//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION RAID. THE NEW TAS ISSUANCE TODAY (1419) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 0 NOTICE(S) FILED TODAY FOR NIL OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 866 CONTRACTS TO 437,171 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED – XXX CONTRACTS

WE HAD A SMALLL SIZED DECREASE IN COMEX OI ( 4130 CONTRACTS) DESPITE OUR $2.45 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JUNE. AT 70.79 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0.1959 TONNE E.F.P. JUMP TO LONDON: NEW TOTAL 64.000 TONNES STANDING SO FAR // + /A STRONG ISSUANCE OF 1162 T.A.S. CONTRACTS ////YET ALL OF..THIS HAPPENED WITH A $2.45 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 2514 OI CONTRACTS (7.818 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3380 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 437,171

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2514 CONTRACTS WITH 866 CONTRACTS DECREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): A SMALL 505 CONTRACTS) AND 3380 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2514 CONTRACTS OR 7818 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3380 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (866) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 9,394 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 70.79 TONNES FOLLOWED BY TODAY’S 6300 OZ E.F.P. JUMP TO LONDON //// NEW STANDING FALLS TO 64.000 TONNES// /3) ZERO LONG LIQUIDATION//4) SMALL SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: SMALL T.A.S. ISSUANCE: 505 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

TOTAL EFP CONTRACTS ISSUED: 31,715 CONTRACTS OR 3,171,500 OZ OR 98.64TONNES IN 14 TRADING DAY(S) AND THUS AVERAGING: 2400 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAY(S) IN TONNES 98.64 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 98.64/3550 x 100% TONNES 2.76% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 98.64 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 4130 CONTRACTS OI TO 148.503 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 1800 CONTRACTS (RECORD ISSUANCE)

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1800 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1800 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 4130 CONTRACTS AND ADD TO THE 1800 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2330 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 11.65 MILLION OZ

OCCURRED DESPITE OUR $0.40 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING//WEDNeSDAY NIGHT

SHANGHAI CLOSED DOWN 42.46 PTS OR 1.31% //Hang Seng CLOSED DOWN 388.73 PTS OR 1.98% /The Nikkei closed UP 186.23 OR 0.56% //Australia’s all ordinaries CLOSED DOWN 0.57 % /Chinese yuan (ONSHORE) closed DOWN 7.1884 /OFFSHORE CHINESE YUAN DOWN TO 7.1896 /Oil DOWN TO 71.16 dollars per barrel for WTI and BRENT UP AT 75.78 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 866 CONTRACTS DOWN TO 437,171 DESPITE OUR LOSS IN PRICE OF $2.45 ON WEDNESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3380 EFP CONTRACTS WERE ISSUED: : AUGUST 3380 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3380 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2330 CONTRACTS IN THAT 3380 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 866 COMEX CONTRACTS..AND THIS VERY STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $2.45//WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A FAIR 505 CONTRACTS. THROUGHOUT LAST WEEK, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (64.000) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.195 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $2.45) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR FAIR GAIN OF 2514 CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE TAS LIQUIDATION THROUGHOUT THE WEDNESDAY COMEX SESSION . THE TAS ISSUED WEDNESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 7.819 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE. (70.709 TONNES) FOLLOWED BY TODAY’S 6300 OZ E.F.P. JUMP..NEW STANDING REMAINS AT 64.000 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR HUGE LOSS IN PRICE TO THE TUNE OF $2.45

WE HAD – REMOVED CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 2514 CONTRACTS OR 251,400 OZ OR 7.819 TONNES.

Estimated gold volume today:// XX fair

final gold volumes/yesterday XX poor

//JUNE 21/ FOR THE JUNE 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 96.453 OZ int.Delaware 3 kilobars . |

| Deposit to the Dealer Inventory in oz | 16,012.057 oz Brinks |

| Deposits to the Customer Inventory, in oz | 16,001.885 oz Brinks |

| No of oz served (contracts) today | 198 notice(s) 19800 OZ 1.552 TONNES |

| No of oz to be served (notices) | 962 contracts 96,200 oz 2.992 TONNES |

| Total monthly oz gold served (contracts) so far this month | 19,677 notices 1,967,700 OZ 61.203 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

No dealer withdrawals

Customer deposits: 1

i)Into Brinks 16,012.057 oz

total dealer deposits: 16,012.057 oz

we had one customer deposit:

i) Into Brinks: 16,001.885 oz

total deposits: 16,001.885 oz

Withdrawals: 1

i) out of Int. Delaware: 96.453 oz (3 kilobars)

total 96.453 oz

Adjustments;1 dealer to customer

i) Out of Brinks 13,210.510 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 899 contracts having LOST 563 contracts. We had 500 contracts served on Tuesday so we LOST 63 contracts or an additional 6300 oz will NOT stand for gold at the comex.

The next front month after June is the non active delivery month of July. Here, July LOST 147 contracts to stand at 2391 contracts.

AUGUST LOST 3168 contracts up to 365,152 contracts

We had 198 contracts filed for today representing 19,800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 50 notices were issued from their client or customer account. The total of all issuance by all participants equate to 198 contract(s) of which 5 notices were stopped (received) by j.P. Morgan dealer and 218 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2023. contract month,

we take the total number of notices filed so far for the month (19,875 x 100 oz ), to which we add the difference between the open interest for the front month of JUNE (899 CONTRACT) minus the number of notices served upon today 198 x 100 oz per contract equals 2,057,600 OZ OR 64.00 TONNES the number of TONNES standing in this active month of June.

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (19,875) x 100 oz + (899) {OI for the front month} minus the number of notices served upon today (500) x 100 oz) which equals 2,057,600 oz standing OR 64.00 TONNES

TOTAL COMEX GOLD STANDING: 64.000 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,055,246.664 OZ 63.92 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,584,958.309 OZ

TOTAL REGISTERED GOLD: 11,704,821,493 (364.06 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,880,136.816 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,649,285 OZ (REG GOLD- PLEDGED GOLD) 300.13 tonnes//

END

SILVER/COMEX

JUNE 22//2023// THE JUNE 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 858,998.378 oz CNT Int. Delaware Manfra . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 103,138.454 oz Delaware |

| No of oz served today (contracts) | 0 CONTRACT(S) (NIL OZ) |

| No of oz to be served (notices) | 431 contracts (2,155,000 oz) |

| Total monthly oz silver served (contracts) | 423 Contracts (2,115,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposits

total dealer deposit: nil oz

total dealer deposits: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We had 1 deposits customer account:

i) Into Delaware 103,138.454 oz

total customer deposits: 103,138.454 oz

JPMorgan has a total silver weight: 142,366 million oz/271.379 million =52.45% of comex .//dropping fast

Comex withdrawals 3

i) Out of CNT: 22,985.950 oz

ii) Out of Int. Delaware 228,390.928 oz

iii) out of Manfra: 607,621.500 oz

total withdrawals: 858,998.378 oz

adjustments: 1

dealer to customer: manfra

20,680.600 oz

TOTAL REGISTERED SILVER: 27.096 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 271.379 million oz

DEALER SILVER DROPPING FAST. (moves into the 27 million oz column)

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE /2023 OI: 431 CONTRACTS HAVING LOST 0 CONTRACT(S).

WE HAD 0 NOTICES FILED ON TUESDAY SO WE LOST 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF JUNE

JULY HAD A 7351 CONTRACT LOSS TO 53,604CONTRACTS

AUGUST GAINED 28 CONTRACTS TO STAND AT 175

SEPT HAS A GAIN OF 31`67 CONTRACTS UP TO 82,175

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 127,197 huge /

Comex volume: confirmed yesterday:75,183 good

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 423 x 5,000 oz = 2,115,000 oz

to which we add the difference between the open interest for the front month of JUNE(431) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2023 contract month: 423 (notices served so far) x 5000 oz + OI for the front month of JUNE (431) – number of notices served upon today (0 )x 500 oz of silver standing for the JUNE contract month equates to 4.270 million oz + 2.935 EXCHANGE FOR RISK TODAY + 10.435MILLION OZ EXCHANGE FOR RISK (PRIOR)//NEW TOTAL: 17.640 MILLION OZ STANDING

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JUNE 21/WITH GOLD DOWN $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 934.03 TONES

JUNE 20/WITH GOLD DOWN $22.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.03 TONNES

JUNE 16/WITH GOLD UP $0.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.03 TONNES

JUNE 15/WITH GOLD UP $2.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 929.70 TONNES

JUNE 14/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 931.44 TONNES

JUNE 13/WITH GOLD DOWN $10.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.01 TONNES FORM THE GLD///INVENTORY RESTS AT 931.44

JUNE 12/WITH GOLD DOWN $7.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.65 TONNES

JUNE 9/WITH GOLD DOWN $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.65 TONNES

JUNE 8/WITH GOLD UP $20.45 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.46 TONNES FROM THE GLD///INVENTORY RESTS AT 934.65 TONNES

JUNE 7 WITH GOLD DOWN $22.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 938.11 TONNES

JUNE 6/WITH GOLD UP $6.90 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 939.56 TONNES

JUNE 5/WITH GOLD UP $5.00 TODAY : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 938.11 TONNES

JUNE 2/WITH GOLD DOWN $24.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 938.11 TONNES

JUNE 1/WITH GOLD UP $14.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 939.56 TONNES

MAY 31/WITH GOLD UP $5.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 939.56 TONNES

MAY 30/WITH GOLD UP $14.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 26/WITH GOLD UP $.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 941.29 TONNES

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

GLD INVENTORY: 934.03 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 21/WITH SILVER DOWN $.40 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.784 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 20/WITH SILVER DOWN 89 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 16/WITH SILVER UP 23 CENTS TODAY :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 463.183 MILLION OZ

JUNE 15/WITH SILVER DOWN 17 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.377 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 463.642 MILLION OZ//

JUNE 14/WITH SILVER UP 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 735,000 OZ FROM THE SLV///INVENTORY RESTS AT 465.019 MILLION OZ//

JUNE 13/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 465.754 MILLION OZ//

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

JUNE 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF SILVER TO THE TUNE OF 550,000 OZ//INVENTORY RESTS AT 467.269 MILLION OZ

JUNE 8/WITH SILVER UP $0.63 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 7/WITH SILVER DOWN 17 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.01 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 6/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.809 MILLION OZ//

JUNE 5/WITH SILVER DOWN $.13 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 266,000 OZ FROM THE SLV////INVENTORY RESTS AT 466.809 MILLION OZ/

JUNE 2/WITH SILVER DOWN 23 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV./INVENTORY RESTS AT 467.015 MILLION OZ/

JUNE 1/WITH SILVER UP 49 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.933 MILLION OZ

MAY 31/WITH SILVER UP 37 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 367,000 OZ FROM THE SLV////INVENTORY RESTS AT 467.933 MILLION OZ//

MAY 30/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 26/WITH SILVER UP $0.44 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.306 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

CLOSING INVENTORY 463.183 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

END

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

3,Chris Powell of GATA provides to us very important physical commentaries

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS/THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1884

OFFSHORE YUAN: 7.1896

SHANGHAI CLOSED DOWN 42.46 PTS OR 1.31%

HANG SENG CLOSED DOWN 388.73 PTS OR 1.98%

2. Nikkei closed UP 186.23 PTS OR 0.56%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 102.14 EURO RISES TO 1.0925 UP 5 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.371 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 141.77/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.403***/Italian 10 Yr bond yield FALLS to 4.037*** /SPAIN 10 YR BOND YIELD FALLS TO 3.345…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.671

3j Gold at $1934.25 silver at: 23.05 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 55 /100 roubles/dollar; ROUBLE AT 84.23//

3m oil into the 71 dollar handle for WTI and 75 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 141.77// 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .371% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8972 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9802 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.755 UP 3 BASIS PTS…

USA 30 YR BOND YIELD: 3.836 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.715 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 23.56…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.42 UP 10 BASIS PTS (RATES RISING RAPIDLY)

end

2. Overnight: Newsquawk and Zero hedge:

Global Stocks Slump For 4th Day After Central Bank Rate Hike Barrage

BY TYLER DURDEN

THURSDAY, JUN 22, 2023 – 08:16 AM

US equity futures and global markets slumped for a 4th day as policy tightening fears from the US to Norway to Switzerland to the UK hobbled the recent bull run which sent US stocks to a 52-week high last Friday. At 7:45am, S&P 500 and Nasdaq futures were down 0.3% following a selloff on Wall Street on hawkish warnings by Fed Chair Jerome Powell in testimony to Congress. The Bloomberg dollar index was higher with the Norwegian krone outperforming among Group-of-10 currencies. Treasury yields edged higher across the curve, mirroring mild increases in the UK and Europe. Brent crude slid nearly 1%, gold fell and Bitcoin topped $30k amid optimism over ETFs related to the token but has since reversed back under after today’s tightening barrage. Today’s macro data focus includes Jobless data, Home Sales, regional mfg activity, and the leading index. Powell speaks at 10am and there are 4x other Fedspeakers.

In premarket trading, Tesla shares dropped more than 2%, set to extend losses to a second session, after Morgan Stanley joined Barclays in downgrading the stock to equal-weight from overweight.

Here are some other notable premarket movers:

- Alcoa Corp. shares are down 2.3% in premarket trading after Morgan Stanley downgraded the aluminum company to underweight from equal-weight.

- Boeing Co. shares are 1.9% lower as its biggest supplier suspended production after union workers voted to strike, in a surprise development that risks disrupting the planemaker’s plan to hike output of its cash-cow 737 Max jet.

- Nvidia falls as much as 1.4% in premarket trading as the biggest gainers of 2023, including Meta and Tesla, take a breather, set to extend losses to a second consecutive session.

- Root shares jump 60% in premarket trading after the Wall Street Journal reported on Wednesday that Embedded Insurance has offered to acquire the car-insurance startup for $19.34 a share, citing unidentified people.

All industry subsectors fell into the red in Europe, where the region’s key Stoxx 600 index slumped about 1%, extending declines to a fourth day. UK stocks stayed lower after the Bank of England raised its benchmark rate by more than economists’ expectations, stepping up its fight against the worst bout of inflation since the 1980s and warning it may have to hike again. Here are the most notable European movers:

- Ocado shares jump as much as 22% following a story in the Times published late Wednesday that mentions “speculation of bid interest,” without saying where it got the information

- Anheuser- Busch InBev shares advance as much as 1.1% after Deutsche Bank upgrades its recommendation on the stock to buy, seeing an “attractive entry point for a quality company”

- MTG gains as much as 9.9% after Handelsbanken reiterated its short-term buy recommendation for the Swedish gaming media group, saying the company is on a “fast track to recovery”

- SES shares gain as much as 5.9% after ending talks with Intelsat, with analysts saying the outcome is positive as the satellite company can now focus on returning cash to shareholders instead

- Valmet drops as much as 6.1%, its sixth straight decline and to lowest in six months, after Danske Bank downgrades the industrial equipment and service provider to hold and notes increased risks

- Electrolux shares fall as much as 6.8% after Bloomberg News reported that Midea had dropped its pursuit of the Swedish home appliance maker after discussions with the firm and its top shareholder

- Novo Nordisk shares fall as much as 3.2% after Danish newspaper BT reported the EMA is investigating a possible link between the firm’s Wegovy and Ozempic drugs, and thyroid cancer

- Idorsia falls as much as 5.4% after Morgan Stanley resumes coverage at underweight. The broker says it prefers caution until there are signs of accelerating sales for lead insomnia drug Quviviq

Central banks’ battle with inflation far from over as inflation proves to be far stickier than they predicted just two years ago, and thwarting bets that tightening cycles were set to wind down. That’s prompted investors to rethink animal spirits unleashed by last week’s Fed rate pause. “Recession risks are arguably higher if rates are higher for longer, but risk assets are not reflecting that,” said Janet Mui, head of market analysis at RBC Brewin Dolphin. “Markets are re-assessing whether further risk taking is justified after the year-to-date-rally.”

In the US, hard-landing fears re-established themselves amid the prospect of tighter policy, pushing the inversion of a key segment of the Treasury yield curve to a full percentage point for the first time since March.

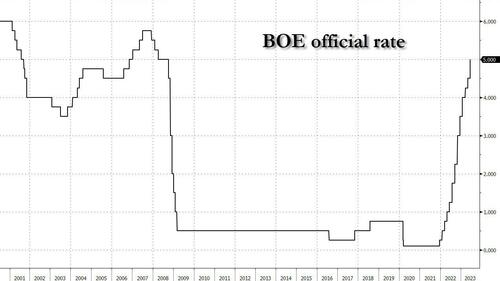

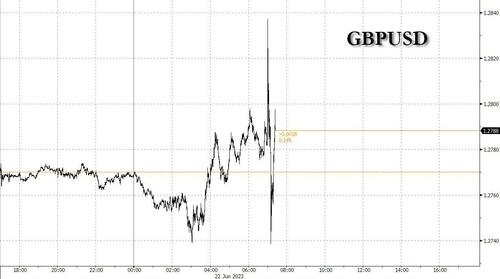

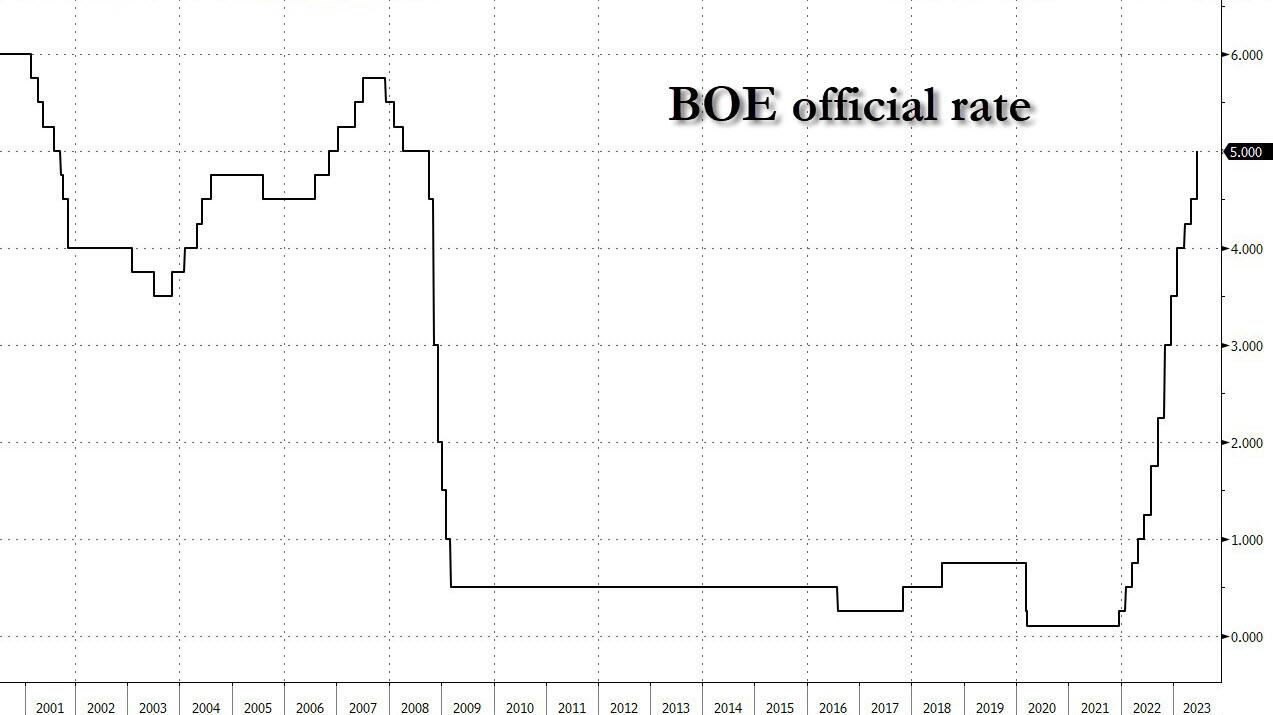

As noted earlier, the BOE lifted its policy rate by 50 basis points to 5% as it struggles to contain inflation that rose by 8.7%, higher than expected for a fourth month. Money market pricing now implies the BOE’s benchmark will reach 6% by the end of the year, which would be the highest since the turn of the century.

“The UK has the unenviable title of highest core inflation rate in the G7, and by quite some margin,” said Seema Shah, chief global strategist at Principal Asset Management. “It requires the central bank to adopt a clearly hawkish attitude that signals further sizeable moves over the coming months.n. A sharper slowdown of the UK economy will be an unfortunate, but necessary, fallout from monetary policy.”

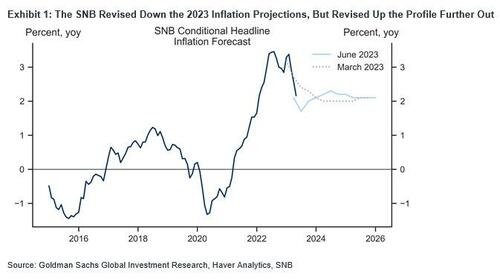

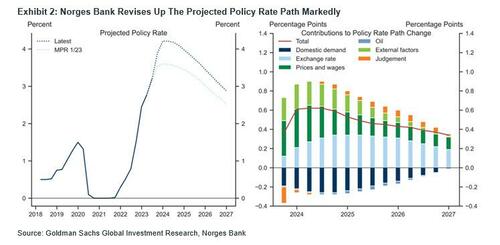

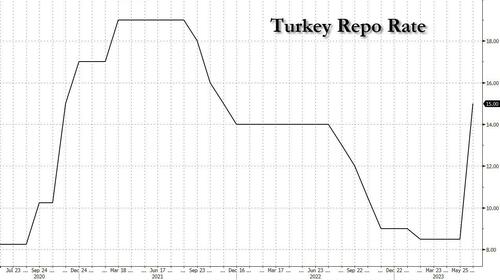

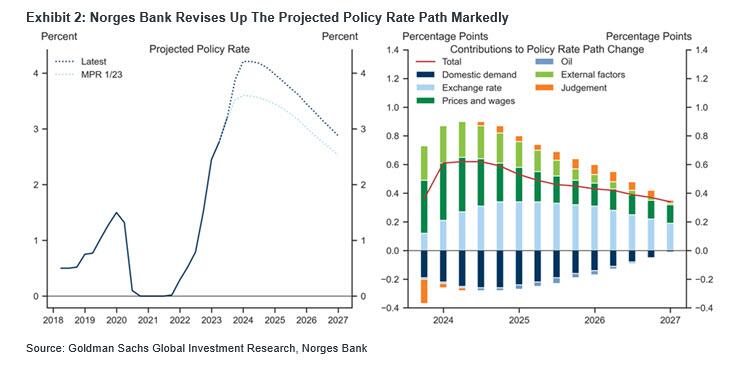

Earlier, Norway’s central bank lifted its key deposit rate by 50 basis points to 3.75%, the 11th hike in its benchmark since September 2021. Officials said the rate will “most likely be raised further in August” and forecast a peak rate of 4.25% later this year. By contrast, the Swiss National Bank delivered the smallest interest-rate hike since it began monetary tightening a year ago, lifting its key rate by a quarter-point to 1.75%. Swiss inflation is the slowest of any advanced economy. Turkey’s central bank hiked significantly less than most economists expected, a sign that policymakers will favor a gradual transition from an era of ultra-cheap money.

Earlier in the session, Asian stocks stopped a three-day losing streak, as investors assessed remarks from Federal Reserve officials on the trajectory for US interest rates. The MSCI Asia Pacific Index climbed as much as 0.3% as Japanese benchmarks advanced, with the Topix rising to a fresh 33-year high. Markets in Greater China, which have been a drag on sentiment in the region this week as the stimulus trade faded, were closed for a holiday.

- China is closed for holiday

- ASX 200 was pressured with weakness across all sectors and as tech conformed to the underperformance stateside.

- Nikkei 225 traded negatively but with the downside limited by recent currency weakness and after BoJ Board Member Noguchi echoed the central bank’s dovish tone in which he noted that the central bank’s new guidance is showing a strong commitment to patiently keeping easy policy and what’s most important is to ensure momentum for wage growth becomes trend by maintaining easy policy.

- KOSPI was positive with the index underpinned by investment-related headlines including reports that European companies pledged investments in South Korea related to batteries, future cars and other cutting-edge industries.

“Fed Chair Powell continued to make a case for two more rate hikes but other Fed member commentaries leaned dovish,” Charu Chanana, market strategist at Saxo Markets, wrote in a note. Stocks in the Philippines headed for correction territory amid a government tax plan on snacks and sweetened beverages. The Thai equity benchmark was poised for its lowest close in 27 months, amid a selloff by foreign funds as political concerns following the nation’s May election continued to sour sentiment for the country’s stocks. Optimism on impending Chinese stimulus, which had supported domestic and regional shares earlier in June, has faded after a series of disappointing announcements over the past week. However, the MSCI Asia gauge is still up more than 5% this month

In FX, the dollar is marginally softer against most FX majors; Aussie at the bottom of G-10 scoreboard. Treasury 10-year yield broadly steady near 3.72%. JGB futures pare opening gains to trade little changed after solid 5-year auction. Aussie curve inverts again with 10-year yield about 3.5bps lower.

In commodities, WTI crude muted around $72.30; gold similarly quiet near $1,933. Bitcoin remains above $30k following Wednesday’s strong rally.

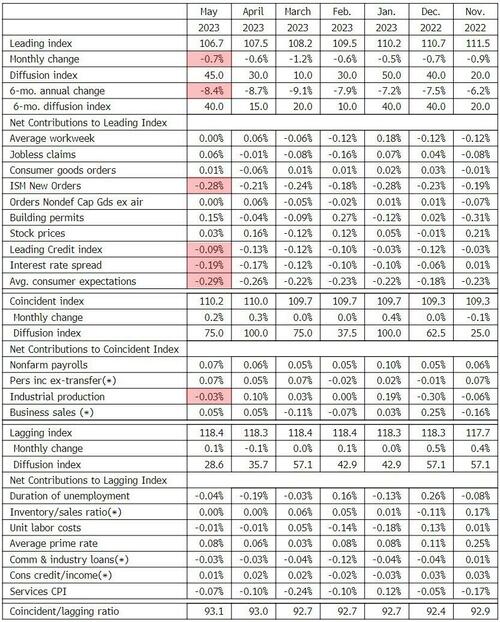

To the day ahead now, and the main highlight is the Bank of England’s latest policy decision which as noted earlier was a surprising 50 bps rate hike. In addition, we’ll hear Fed Chair Powell’s testimony to the Senate Banking Committee, along with the Fed’s Waller, Bowman, Mester and Barkin, ECB Vice President de Guindos and the ECB’s Panetta. Otherwise, US data releases include the weekly initial jobless claims, existing home sales for May, the Conference Board’s leading index for May, and the Kansas City Fed’s manufacturing activity index for June. In addition, there’s the European Commission’s preliminary consumer confidence for the Euro Area in June.

Market Snapshot

- S&P 500 futures down 0.2% to 4,400.00

- MXAP down 0.1% to 166.06

- MXAPJ down 0.2% to 521.84

- Nikkei down 0.9% to 33,264.88

- Topix little changed at 2,296.50

- Hang Seng Index down 2.0% to 19,218.35

- Shanghai Composite down 1.3% to 3,197.90

- Sensex little changed at 63,491.22

- Australia S&P/ASX 200 down 1.6% to 7,195.49

- Kospi up 0.4% to 2,593.70

- STOXX Europe 600 down 0.9% to 452.79

- German 10Y yield little changed at 2.45%

- Euro little changed at $1.0991

- Brent Futures down 0.7% to $76.61/bbl

- Gold spot down 0.3% to $1,926.72

- U.S. Dollar Index little changed at 102.08

Top overnight news

- Washington-Beijing tensions set to ratchet up even further as the White House turns its attention toward curtailing China’s cloud giants. NYT

- India’s stock market spikes as investors increasingly embrace the narrative that the country is set to overtake China as the world’s economic growth engine (and it helps that India doesn’t have the geopolitical risks swirling around China). FT

- Norway’s central bank has raised its main interest rate by 50bps (vs 25bps expected) to 3.75 per cent and said borrowing costs are “most likely” to be lifted further in August after inflation overshot expectations. FT

- The head of Germany’s central bank has warned inflation is a “very greedy beast” and it would be a “first-order error” to stop raising interest rates even if it keeps falling in the coming months. Joachim Nagel, president of the Bundesbank, on Wednesday said some central banks in the past had given up too early in the fight against inflation and it was his “intention that we should really prevent this” from happening in the eurozone. FT

- Ukraine warns that its gas transit deal w/Russia’s Gazprom could end when the current contract expires in 2024 (this is one of the last arteries supplying gas from Russia into Europe and accounts for ~5% of the latter’s supply). FT

- Britain’s red-hot inflation is set to force the BOE to step up the pace of rate hikes again today. It’s expected to push ahead with a 25-bp rise to 4.75% — though money markets put a 40% chance on a 50-bp increase. Officials won’t lay out full new forecasts until August, but today’s minutes will be scrutinized for any signals on the outlook and what the BOE might do about it. BBG

- Deutsche Bank CEO Christian Sewing said he expects trading results to improve in the second half. Citing “momentum” in fixed income, he told Bloomberg Television that traders should see “a slight recovery” this year. He also said the bank is committed to returning €8 billion to shareholders. BBG

- India is expected to purchase state-of-the-art U.S. drones and jointly produce jet-fighter engines in a multibillion-dollar deal designed to wean New Delhi off arms purchases from Russia. WSJ

- Twitter Chief Executive Linda Yaccarino intervened to help repair the relationship between the social-media company and Alphabet’s Google after a payment issue, a person familiar with the matter said, an early example of the new CEO’s management style. Twitter is now paying Google for its cloud services after not consistently paying some of those bills, people familiar with the matter said. Those bills amounted to more than $20 million a month recently. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly lower following the tech-led declines on Wall St and with risk appetite also constrained by key holiday closures with markets across the Greater China region shut for the Dragon Boat Festival. ASX 200 was pressured with weakness across all sectors and as tech conformed to the underperformance stateside. Nikkei 225 traded negatively but with the downside limited by recent currency weakness and after BoJ Board Member Noguchi echoed the central bank’s dovish tone in which he noted that the central bank’s new guidance is showing a strong commitment to patiently keeping easy policy and what’s most important is to ensure momentum for wage growth becomes trend by maintaining easy policy. KOSPI was positive with the index underpinned by investment-related headlines including reports that European companies pledged investments in South Korea related to batteries, future cars and other cutting-edge industries.

Top Asian news

- China’s Commerce Minister said China is willing to push forward economic and trade ties with France.

- White House economic adviser Bernstein said he expects US relations with China will improve and also commented that where the US is now looks nothing like a recession.

European bourses trade on the backfoot with selling pressure having picked up since the cash open without a clear fundamental driver. US equity futures are also softer on the session, albeit to a lesser extent than European peers with the ES just about holding around the 4400 mark. Equity sectors in Europe are lower across the board with selling pressure most prominent in Banking, Autos and Travel & leisure names. In terms of individual movers, Ocado (+42%) is by far the best performer in the Stoxx 600 amid speculation in The Times that Amazon (AMZN) could be a potential suitor – Amazon declined to comment.

Top European News

- Boeing’s Biggest Supplier Suspends Output After Strike Vote

- Ukraine Recap: Double Bridge From Crimea to Mainland Damaged

- SNB Dials Down Interest-Rate Hike But Says More Increases Likely

- China’s Chesir Said to Eye Merck KGaA’s €1 Billion Pigments Arm

- Norway Raises Rate by Half Point to Ramp up Inflation Fight

- US Welcomes EU’s Security Strategy on China, Envoy Says

- Ocado Shares Jump After Times Report Citing Bid Interest

FX

- DXY sits in a tight range on either side of 102.00.

- GBP, NZD, CAD are all firmer against the USD, the former ahead of the BoE announcement at noon London time.

- Yen continues to track Treasuries relative to JGBs following another BoJ official reading from the dovish script.

- Aussie one again resides as a laggard, while Chinese markets were closed overnight.

- Euro eventually reclaimed 1.10+ status against the Dollar, with hefty in-the-money OpEx for the NY cut.

Fixed Income

- Bunds reversed through Wednesday’s low before finding some underlying support at 133.04.

- Gilts are losing more momentum as the clock ticks down to high noon at the BoE that is evenly priced to stick with 25bps or go large at 50bps.

- The T-note is nearer to its intraday trough than its peak ahead of US jobless claims, existing home sales and more Fed speak.

- Deutsche Bank CEO Sewing sees fixed income recovery in Q3/Q4, via BBG TV.

Commodities

- WTI and Brent August futures have tilted negative in tandem with the broader risk appetite but, in the bigger picture, remain choppy within tight ranges as markets brace for a heavy central bank day as eyes now turn to the BoE.

- Spot gold is relatively flat under USD 1,930/oz, with the Dollar index also contained, in the run-up to the aforementioned central bank events on the docket.

- Base metals are now mostly firmer (vs mostly softer around the European cash open) despite the subdued risk appetite and relatively flat Dollar.

- IEA’s Birol said the IEA still sees tight oil market in H2 even with a sluggish China; very little new LNG coming onto market this year, according to Bloomberg.

Central Banks

SNB:

- SNB hiked its Policy Rate by 25bps to 1.75%, in-fitting with analyst expectations but shy of market pricing which leaned towards 50bps. SNB said cannot be ruled out that additional rises in the SNB policy rate will be necessary, and added in the current environment, the focus is on selling foreign currency. Click here for the full release.

- SNB Chairman Jordan said most likely we will have to tighten monetary policy again, but we can also take a more gradual approach, according to Reuters.

- SNB Financial Stability Report: In the SNB’s view, going forward, banks should be required to prepare a minimum amount of assets that can be pledged at central banks. Inflation and interest rates should remain lower than in other advanced economies.

NORGES BANK:

- Norges Bank hiked its Policy Rate by 50bps to 3.75% vs expectations for a 25bps hike to 3.50%. Norges said the current assessment of the outlook and balance of risks implies that the policy rate will most likely be raised further in August. Click here for the full release.

- Norges Bank Chief said significant uncertainty regarding the Crown currency development; Crown exchange rate weaker than models can explain, according to Reuters.

Geopolitics

- US National Security Adviser Sullivan is to travel to Denmark this weekend to meet representatives from India, Brazil and other countries that have not condemned Russia’s invasion of Ukraine in an effort to boost support for Kyiv, according to FT.

- US Coast Guard ship transited Taiwan Strait following Secretary of State Blinken’s China visit, according to Reuters.

- Russian gas flows through Ukraine could stop next year as the Ukrainian energy minister stated that a renewal of the five-year transit contract to supply Europe was unlikely, according to FT.

- German Chancellor Scholz on China talks, says we warned against any changes to territorial status quo by force, particularly in Taiwan, according to Reuters.

- US and India are to sign major deals on fighter-jet engines, and drones during PM Modi’s visit, according to a US official cited by AFP

US Event Calendar

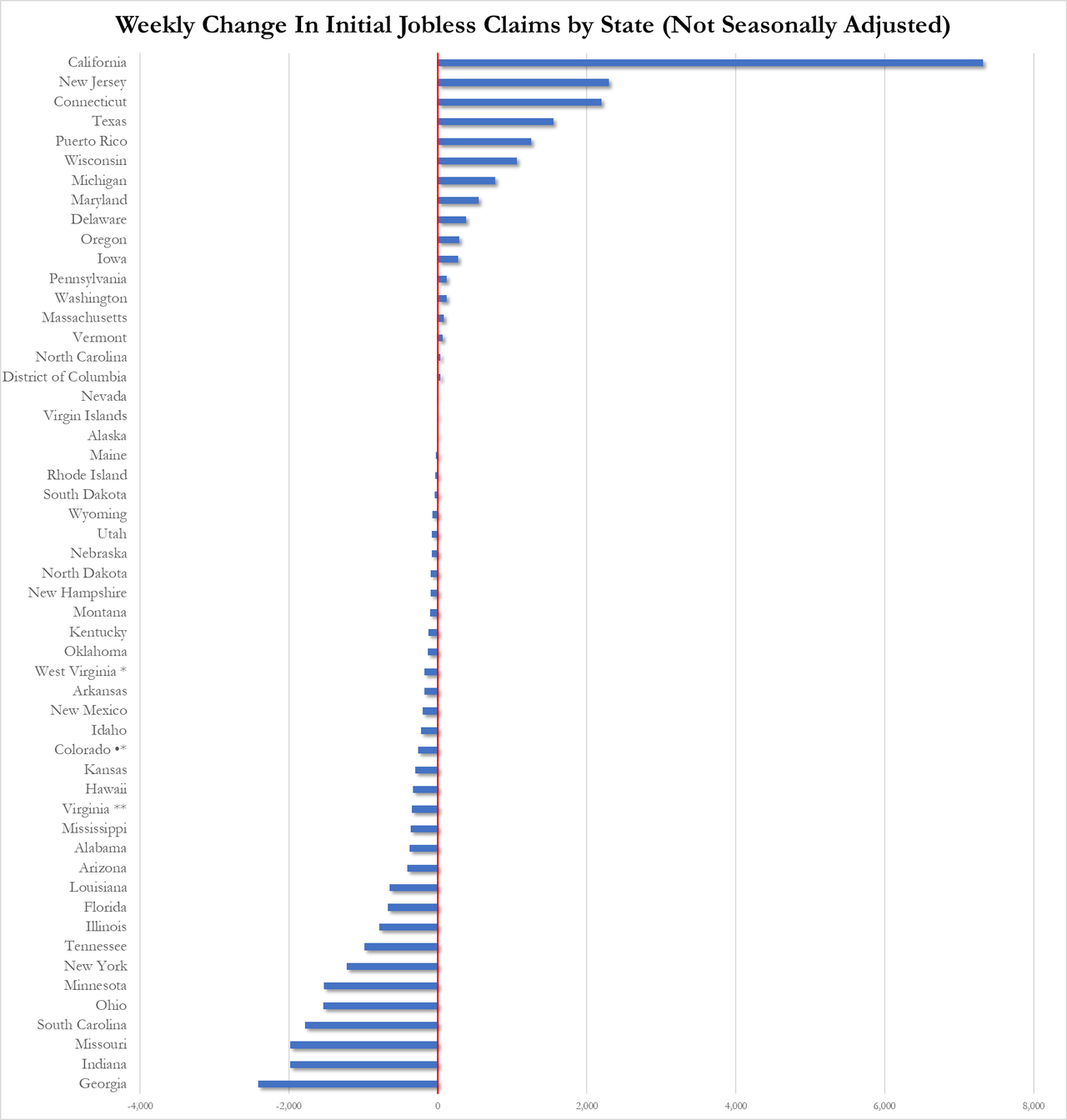

- 08:30: June Initial Jobless Claims, est. 259,000, prior 262,000

- 08:30: June Continuing Claims, est. 1.79m, prior 1.78m

- 08:30: 1Q Current Account Balance, est. -$218b, prior -$206.8b

- 10:00: May Existing Home Sales MoM, est. -0.7%, prior -3.4%

DB’s Jim Reid concludes the overnight wrap

The last 24 hours proved to be another tough session for markets, by recent standards at least, with both the S&P 500 (-0.52%) and the STOXX 600 (-0.50%) down for a 3rd consecutive day. This was the first time since the May 4th and June 9th respectively. There were several factors behind this, including some hawkish remarks from Fed Chair Powell as he reiterated the Fed’s intention to keep hiking rates. That meant investors again moved to price out the prospects for 2023 Fed cuts. But on top of that, we had several bad macro headlines from the UK, where another upside inflation surprise ramped up the pressure on gilts once again, and led to growing concerns that stagflation was on the cards.

It’s difficult to stress just how bad that UK release was yesterday, since both headline and core CPI surprised on the upside for a 4th consecutive month. That left headline CPI at +8.7% (vs. +8.4% expected), and in many respects the more worrying story was core CPI hitting a 31-year high of +7.1% (vs. +6.8% expected). This persistence for both headline and core is now making the UK a real outlier on inflation, with the highest rate in the G7 by some margin. For instance, headline Euro Area inflation “only” stood at +6.1% in May, and if you calculate US inflation on the same basis as Europe does, then the comparable headline measure is now down to just +2.7%.

With that upside CPI in hand, investors started to fully price in a 6% Bank Rate over the coming months, which is the first time that’s happened since the mini-budget turmoil last September. Unsurprisingly, this prompted a sizeable selloff for gilts too, though the 2yr yield (+9.3bps) at 5.05% remained a little below its post-GFC high reached this Monday. And if that wasn’t enough, we also found out yesterday that the UK debt-to-GDP ratio surpassed 100% of GDP in May for the first time since March 1961. For a sense of how long ago that was, it was a month before Yuri Gagarin became the first man in space and was also the last time Spurs were on course to win the league title.

That backdrop sets us up for the Bank of England’s latest policy decision today at 12pm London time. There’s little doubt that they’ll deliver another hike, but since the CPI print there’s been growing questions about a potential 50bp move today, or alternatively if they might signal bigger moves at future meetings. Current market pricing is suggesting there’s a 37% chance of a 50bp move. But looking over the June and August meetings together, we’ve got 76bps of rate hikes priced, so that implies markets are fully pricing in a larger move for one of the next two decisions. Our UK economist is sticking to his 25bp call for today’s meeting, but thinks the sticky inflation raises the hawkish risks. See his latest blog here.

Central banks were in focus elsewhere yesterday, since Fed Chair Powell was testifying before the House Financial Services Committee. In many respects his remarks were similar to those from last week’s FOMC decision, and he reiterated that “the process of getting inflation back down to 2 percent has a long way to go”. Among other Fed speakers, Chicago Fed President Goolsbee noted that the decision to keep rates on hold in June “was a close call”, a hawkish-leaning comment for one of the more dovish FOMC members this year. Meanwhile, Atlanta Fed President Bostic (non-voter) said that “the bar to justify further rate hikes is higher than it was a few months ago” and that his baseline was to hold rates through year-end, implying that he was one of the just two FOMC members in the June dot plot that expected to keep rates on hold in 2023. However, Bostic added that he did not expect a rate cut for “most of 2024”.

For markets, the main takeaway was anticipating a Fed that stays higher for longer. While futures moved to price in marginally less chances of a hike in July (from 74% to 69%), there was growing scepticism that the Fed would be cutting rates at all this year, and the rate priced in by the December meeting closed at 5.23% (+1.2bps), just shy of the post-SVB’s highs reached on Monday of 5.24%. On the back of this, 2yr Treasury yields (+3.05bps to 4.715%) sold off, while the 10yr yield was just lower than unchanged on the day, -0.2bps at 3.719%. The 2s10s slope thus reached a new post-SVB low of -100.4bps. Those concerns were evident among equities too, where the S&P 500 (-0.52%) fell for a third consecutive day. Tech stocks led the decline, with the NASDAQ (-1.21%) and the FANG+ index of megacap tech stocks (-2.41%) underperforming. That said, volatility remained incredibly subdued, with the VIX index falling back to 13.2pts, which is its lowest closing level since January 2020.

Back in Europe, markets followed a similar pattern yesterday, with bonds and equities both losing ground. By the close, yields on 10yr bunds (+3.0bps), OATs (+3.5ps) and BTPs (+2.0bps) had all risen, which came as investors fully priced in two further hikes from the ECB over the months ahead. At the same time, the STOXX 600 shed -0.50%, with tech stocks leading the declines once again.

Asian equity markets are mixed this morning amid thin trading due to a holiday in Hong Kong, mainland China and Taiwan. As I type, the KOSPI (+0.35%) is seeing gains with the Nikkei fairly flat. The S&P/ASX 200 (-1.57%) is sharply down, extending its losses for a second day due to a sell-off in technology and mining stocks. Outside of Asia, US stock futures are indicating small additional losses with those on the S&P 500 (-0.09%) and NASDAQ 100 (-0.14%) slightly lower.

To the day ahead now, and the main highlight will be the Bank of England’s latest policy decision. In addition, we’ll hear Fed Chair Powell’s testimony to the Senate Banking Committee, along with the Fed’s Waller, Bowman, Mester and Barkin, ECB Vice President de Guindos and the ECB’s Panetta. Otherwise, US data releases include the weekly initial jobless claims, existing home sales for May, the Conference Board’s leading index for May, and the Kansas City Fed’s manufacturing activity index for June. In addition, there’s the European Commission’s preliminary consumer confidence for the Euro Area in June.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

Negative sentiment continues on Super Thursday in the run-up of the BoE – Newsquawk US Market Open

THURSDAY, JUN 22, 2023 – 06:03 AM

- European bourses trade on the backfoot with selling pressure having picked up since the cash open; Chinese markets were closed overnight.

- US equity futures are also softer on the session, albeit to a lesser extent than European peers with the ES just about holding around the 4400 mark.

- SNB’s rate hike disappointed markets but matched analyst expectations while Norges opted for a larger-than-forecast rate hike and guided another hike in August.

- DXY sits in a tight range on either side of 102.00, EUR/USD eventually reclaimed 1.10+ status, with hefty in-the-money OpEx for the NY cut.

- Looking ahead, highlights include US IJC, Existing Home Sales, EU Consumer Confidence (Flash), BoE, CBRT & Banxico announcements, Speeches from Fed’s Powell, Bowman, Barkin, ECB’s de Guindos

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses trade on the backfoot with selling pressure having picked up since the cash open without a clear fundamental driver.

- US equity futures are also softer on the session, albeit to a lesser extent than European peers with the ES just about holding around the 4400 mark.

- Equity sectors in Europe are lower across the board with selling pressure most prominent in Banking, Autos and Travel & leisure names. In terms of individual movers, Ocado (+42%) is by far the best performer in the Stoxx 600 amid speculation in The Times that Amazon (AMZN) could be a potential suitor – Amazon declined to comment.

- Click here and here for a recap of the main European updates.

- Click here for more detail.

FX

- DXY sits in a tight range on either side of 102.00.

- GBP, NZD, CAD are all firmer against the USD, the former ahead of the BoE announcement at noon London time.

- Yen continues to track Treasuries relative to JGBs following another BoJ official reading from the dovish script.

- Aussie one again resides as a laggard, while Chinese markets were closed overnight.

- Euro eventually reclaimed 1.10+ status against the Dollar, with hefty in-the-money OpEx for the NY cut.

- Click here for notable OpEx for the NY Cut.

- Click here for more detail.

FIXED INCOME

- Bunds reversed through Wednesday’s low before finding some underlying support at 133.04.

- Gilts are losing more momentum as the clock ticks down to high noon at the BoE that is evenly priced to stick with 25bps or go large at 50bps.

- The T-note is nearer to its intraday trough than its peak ahead of US jobless claims, existing home sales and more Fed speak.

- Deutsche Bank CEO Sewing sees fixed income recovery in Q3/Q4, via BBG TV.

- Click here for more detail.

COMMODITIES

- WTI and Brent August futures have tilted negative in tandem with the broader risk appetite but, in the bigger picture, remain choppy within tight ranges as markets brace for a heavy central bank day as eyes now turn to the BoE.

- Spot gold is relatively flat under USD 1,930/oz, with the Dollar index also contained, in the run-up to the aforementioned central bank events on the docket.

- Base metals are now mostly firmer (vs mostly softer around the European cash open) despite the subdued risk appetite and relatively flat Dollar.

- IEA’s Birol said the IEA still sees tight oil market in H2 even with a sluggish China; very little new LNG coming onto market this year, according to Bloomberg.

- Click here for more detail.

NOTABLE US HEADLINES

- US House is reportedly to vote on Biden impeachment resolution today, according to Axios.

- US federal court scheduled the initial appearance in the Hunter Biden case for July 26th, according to a CBS reporter.

CRYPTO

- Bitcoin extended on this week’s rally and climbed back above the USD 30,000 level.

CENTRAL BANKS

SNB:

- SNB hiked its Policy Rate by 25bps to 1.75%, in-fitting with analyst expectations but shy of market pricing which leaned towards 50bps. SNB said cannot be ruled out that additional rises in the SNB policy rate will be necessary, and added in the current environment, the focus is on selling foreign currency. Click here for the full release.

- SNB Chairman Jordan said most likely we will have to tighten monetary policy again, but we can also take a more gradual approach, according to Reuters.

- SNB Financial Stability Report: In the SNB’s view, going forward, banks should be required to prepare a minimum amount of assets that can be pledged at central banks. Inflation and interest rates should remain lower than in other advanced economies.

NORGES BANK:

- Norges Bank hiked its Policy Rate by 50bps to 3.75% vs expectations for a 25bps hike to 3.50%. Norges said the current assessment of the outlook and balance of risks implies that the policy rate will most likely be raised further in August. Click here for the full release.

- Norges Bank Chief said significant uncertainty regarding the Crown currency development; Crown exchange rate weaker than models can explain, according to Reuters.

OTHER:

- BoJ Board Member Noguchi said Japan’s economy is to recover moderately and BoJ’s new guidance is showing a strong commitment to patiently keeping easy policy, while he also noted that the global economy and markets are risks to Japan’s economy. Furthermore, Noguchi said the shape of the yield curve is now smooth as a whole and what’s most important is to ensure momentum for wage growth becomes a trend by maintaining easy policy. Noguchi does not see the need to make operational tweaks to Yield Curve Control (YCC) for the time being; BoJ should prioritise keeping yields stably low to sustainably achieve price target as early as possible.

- Brazil Central Bank maintained the Selic rate at 13.75%, as expected, while it removed the reference to a possible resumption of the tightening cycle if the disinflationary process does not proceed as expected and said it will persevere with its policy until the consolidation of disinflation and anchoring of inflation expectations around its target. BCB said the current scenario demands patience and serenity in conducting monetary policy and stated that various measures of underlying inflation remain above the range compatible with meeting the inflation target, while it lowered its 2023 CPI forecast to 5.0% from 5.8% and cut its 2024 CPI forecast to 3.4% from 3.6%.

GEOPOLITICS

- US National Security Adviser Sullivan is to travel to Denmark this weekend to meet representatives from India, Brazil and other countries that have not condemned Russia’s invasion of Ukraine in an effort to boost support for Kyiv, according to FT.

- US Coast Guard ship transited Taiwan Strait following Secretary of State Blinken’s China visit, according to Reuters.

- Russian gas flows through Ukraine could stop next year as the Ukrainian energy minister stated that a renewal of the five-year transit contract to supply Europe was unlikely, according to FT.

- German Chancellor Scholz on China talks, says we warned against any changes to territorial status quo by force, particularly in Taiwan, according to Reuters.

- US and India are to sign major deals on fighter-jet engines, and drones during PM Modi’s visit, according to a US official cited by AFP

APAC TRADE

- APAC stocks were mostly lower following the tech-led declines on Wall St and with risk appetite also constrained by key holiday closures with markets across the Greater China region shut for the Dragon Boat Festival.

- ASX 200 was pressured with weakness across all sectors and as tech conformed to the underperformance stateside.

- Nikkei 225 traded negatively but with the downside limited by recent currency weakness and after BoJ Board Member Noguchi echoed the central bank’s dovish tone in which he noted that the central bank’s new guidance is showing a strong commitment to patiently keeping easy policy and what’s most important is to ensure momentum for wage growth becomes trend by maintaining easy policy.

- KOSPI was positive with the index underpinned by investment-related headlines including reports that European companies pledged investments in South Korea related to batteries, future cars and other cutting-edge industries.

NOTABLE ASIA-PAC HEADLINES

- China’s Commerce Minister said China is willing to push forward economic and trade ties with France.

- White House economic adviser Bernstein said he expects US relations with China will improve and also commented that where the US is now looks nothing like a recession.

DATA RECAP

- New Zealand Trade Balance (NZD)(May) 46.0M (Prev. 427.0M)

- New Zealand Exports (NZD)(May) 6.99B (Prev. 6.8B)

- New Zealand Imports (NZD)(May) 6.95B (Prev. 6.38B)

2 c. ASIAN AFFAIRS

ASIAN AND AUSTRALIAN CLOSINGS//EUROPE OPENING TRADING:

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 42.46 PTS OR 1.31% //Hang Seng CLOSED DOWN 388.73 PTS OR 1.98% /The Nikkei closed UP 186.23 OR 0.56% //Australia’s all ordinaries CLOSED DOWN 0.57 % /Chinese yuan (ONSHORE) closed DOWN 7.1884 /OFFSHORE CHINESE YUAN DOWN TO 7.1896 /Oil DOWN TO 71.16 dollars per barrel for WTI and BRENT UP AT 75.78 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

2 d./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

2e) JAPAN

JAPAN

END

3 CHINA /

CHINA/USA

end

4.EUROPEAN AFFAIRS//UK /SCANDAVIAN AFFAIRS

UK

BOE Shocks Markets With Surprise 50bps Rate Hike In Crusade Against Red Hot Inflation

THURSDAY, JUN 22, 2023 – 07:26 AM

Extending Thursday’s central bank tightening barrage, which saw rate hikes from the likes of Switzerland, Norway and Turkey, moments ago the BOE shocked markets with a bigger-than-expected half-point rise in the interest rates to 5%, the 13th consecutive rate hike of the current cycle and the highest level since 2008, as the BOE has stepped up its fight against sticky high inflation.

Voting seven to two in favor of the larger-than-expected increase (Dinghra and outgoing member Tenreyro voted for unchanged and nobody voted for a 25bps hike), the central bank’s Monetary Policy Committee said it was responding to “material news” in recent economic data that showed worse inflationary pressures in the UK economy.

As noted above, the two dissents on the BOE’s rate-setting committee were external members Silvana Tenreyro, in her last meeting, and Swati Dhingra. They argued that the existing rate rises have yet to impact the economy fully and falling energy prices will push inflation below target by the end of the forecast horizon.

The BoE hopes its decisive move demonstrates determination to get a grip on rapidly rising prices. In a letter to the chancellor explaining the move, governor Andrew Bailey said: “Bringing inflation down is our absolute priority.” Justifying the move, the MPC said: “There has been significant upside news in recent data that indicates more persistence in the inflation process.”

The BoE policymakers led by governor Andrew Bailey also reiterated earlier guidance pointing toward higher rates warning that “if there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required” and said nothing to rein in market expectations for rates peaking around 6% by early next year, which would be the highest in over two decades.

“If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required,” Bailey wrote in a letter to Chancellor of the Exchequer Jeremy Hunt. He added: “Bringing inflation down is our absolute priority. The MPC will do what is necessary to return inflation to the 2% target.”

The decision announced Thursday suggests UK borrowing costs could keep rising through the summer even after the US Federal Reserved paused its tightening spree. Britain remains an outlier in the Group of Seven nations, with consumer prices rising 8.7% in May, four times the BOE’s 2% target and more than double the rate in the US, while core CPI hit a new 31-year high.

For borrowers, the move signals further hardship. Two year mortgage rates have tripled to more than 6% since March 2022, and experts are warning of a mortgage “time bomb” as households refinance at unaffordable levels.

The decision will also reinforce financial market movements over the past month that have prompted lenders to withdraw fixed-rate mortgage rate deals and increase the costs of home loans substantially in what has become known as a mortgage “time bomb”. With at least 800,000 fixed mortgages due to move on to significantly higher rates in the second half of this year, lawmakers across the political spectrum are starting to blame the Bailey and the BOE for failing to halt inflation earlier.

Prime Minister Rishi Sunak’s government is facing calls to help struggling borrowers but has so far resisted them for fear of undermining the BOE. If rates hit market forecasts of 6%, the UK will collapse into recession, Bloomberg Economics expects. Hunt is pressing high street lenders to help struggling borrowers, moving the issue up the political agenda at a time when the ruling Conservative Party is preparing to fight an election widely expected next year.