SEPT 14//GOLD PRICE DOWN $7.70 TO $1699.70//SILVER UP 6 CENTS TO $19.60//PLATINUM UP $15.50 TO $908.75//PALLADIUM UP $36.05 TO $2169.75// PRODUCER PRICES (PPI) A FORERUNNER OF FUTURE INFLATION REPORT: RED HOT!!/COVID UPDATES, DR PAUL ALEXANDER, VACCINE INJURY//ISRAELI GOVERNMENT STUDY ON THE VACCINES SHOW HUGE INJURIES AND THEN THIS WAS HIDDEN//BANK OF JAPAN CONTEMLATING FX INTERVENTION TO SUPPORT THE YEN//EUROPEAN ENERGY PROBLEMS; GERMANY CONTEMPLATING COMPLETE NATIONALIZATION OF UNIPER//USA IS SET FOR A RAILWAY STRIKE//IMPORTANT COMMENTARY RE MARK CABANA ON INTEREST RATE RISES//SWAMP STORIES FOR YOU TONIGHT///

118 C MACQUARIE FUT 8 132 C SG AMERICAS 86 323 C HSBC 19 435 H SCOTIA CAPITAL 16 624 H BOFA SECURITIES 255 657 C MORGAN STANLEY 37 661 C JP MORGAN 616 267 685 C RJ OBRIEN 20 690 C ABN AMRO 28 709 C BARCLAYS 139 732 C RBC CAP MARKETS 2 737 C ADVANTAGE 12 800 C MAREX SPEC 32 905 C ADM 13

total notices so far: 4664 contracts for 466,400 oz (14.5069 tonnes)

SILVER NOTICES: 23 NOTICES FILED FOR 115,000 OZ/

total number of notices filed so far this month 6327 : for 31,635,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $7.70

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: //// A WITHDRAWAL OF 2.03 TONNES FROM THE GLD/

INVENTORY RESTS AT 962.91 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $.06

AT THE SLV// ://NO CHANGES IN SILVER INVENTORY AT THE SLV//:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 465.899 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 1170 CONTRACTS TO 135,530. AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.31 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.31) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A STRONG GAIN OF 637 CONTRACTS ON OUR TWO EXCHANGES,; HOWEVER WE HAD SOME/MINOR SPECULATOR LIQUIDATION.(SHORT COVERING)

WE MUST HAVE HAD: I) SOME/MINOR/ SPECULATOR SHORT LIQUIDATIONS ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 135,000 OZ QUEUE JUMP / // V) STRONG SIZED COMEX OI GAIN/(//SOME SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -1577

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTACTS for 9 days, total 9362 contracts: 46.810 million oz OR 5.200 MILLION OZ PER DAY. (1040 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 46.810 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 46.810 MILLION OZ///

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1170 WITH OUR $0.31 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 230 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /GOOD BANKER ADDITIONS A// MINOR SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 135,000 OZ QUEUE JUMP // .. WE HAD A STRONG SIZED LOSS OF 940 OI CONTRACTS ON THE TWO EXCHANGES FOR 4.700MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 23 NOTICE(S) FILED TODAY FOR 115,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1965 CONTRACTS TO 463,674 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:—4411 CONTRACTS.???

.

THE FAIR SIZED DECREASE IN COMEX OI CAME WITH OUR FALL IN PRICE OF $22.85//COMEX GOLD TRADING/TUESDAY / WE MUST HAVE HAD MINOR SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND /STRONG SPECULATOR SHORT ADDITIONS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 27,800 OZ //NEW STANDING 14.5629 TONNES

YET ALL OF..THIS HAPPENED WITH OUR HUGE FALL IN PRICE OF $22.85 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A SMALL SIZED GAIN OF 422 OI CONTRACTS 1.315 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2387 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 463,674

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 422 CONTRACTS WITH 1965 CONTRACTS DECREASED AT THE COMEX AND 2387 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 422 CONTRACTS OR 1.315 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2387) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (1965): TOTAL GAIN IN THE TWO EXCHANGES 422 CONTRACTS. WE NO DOUBT HAD 1) MINOR SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS//STRONG SPECULATOR SHORT ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.409 TONNES FOLLOWED BY TODAY’S QUEUE. JUMP OF 27,800 oz. 3) ZERO LONG LIQUIDATION//// //.,4) FAIR SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

18,236 CONTRACTS OR 1,823,600 OZ OR 56.72 TONNES 9 TRADING DAY(S) AND THUS AVERAGING: 2026 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES: 56.72 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 56.72/3550 x 100% TONNES 1.60% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 56.72 TONNES (MUCH LESS ISSUANCE THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER,FELL BY A GIGANTIC SIZED 1170 CONTRACT OI TO 135,530 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 230 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 230 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 230 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1170 CONTRACTS AND ADD TO THE 230 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED LOSS OF 940 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 4.700 MILLION OZ

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 26.25 PTS OR .80% //Hang Sang CLOSED DOWN 479.76 PTS OR 2.48% /The Nikkei closed DOWN 796.01 OR 2.78%. //Australia’s all ordinaires CLOSED DOWN 2.51% /Chinese yuan (ONSHORE) closed DOWN AT 6.9609//OFFSHORE CHINESE YUAN DOWN 6.9752// /Oil UP TO 87,19 dollars per barrel for WTI and BRENT AT 92.72 / Stocks in Europe OPENED ALL MIXED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1965 CONTRACTS TO 463,674 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS FAIR COMEX DECREASE OCCURRED DESPITE OUR STRONG FALL IN PRICE OF $22.85 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2387 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2387 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :2387 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2387 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED SIZED TOTAL OF 422 CONTRACTS IN THAT 2387 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 1965 CONTRACTS..AND THIS SMALL GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG FALL IN PRICE OF GOLD $22.85. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (14.5629),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 14.5629 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $22,85) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A GOOD SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 422 CONTRACTS // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS ADDED TO THEIR POSITIONS////// WE HAVE REGISTERED A SMALL SIZED GAIN OF 1.315 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT. (14.5629 TONNES)…

WE HAD 4411 CONTRACTS ADDED FROM COMEX TRADES. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 422 CONTRACTS OR 42200 OZ OR 1.315 TONNES

Estimated gold volume 164,889/// poor/

final gold volumes/yesterday 253,548/ fair

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 14

Total monthly oz gold served (contracts) so far this month

4664 notices 466,400 OZ 14.5069 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into Delaware: 1999.900 oz

total deposits 1999.900 oz

0 customer withdrawals:

total: nil oz

total in tonnes: 0.00 tonnes

Adjustments: 1 Brinks:

32,215.302 oz dealer to customer

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 793 contracts having GAINED 271 contracts .

We had 7 notices filed on TUESDAY so we gained 278 contracts or an additional 27,800 oz

will stand for gold in this very non active delivery month of September.

October GAINED 869 contracts UP to 43,145

November GAINED 129 contracts to stand at 189

December LOST 3788 contracts DOWN to 375,233

We had 775 notice(s) filed today for 77,500 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 616 notices were issued from their client or customer account. The total of all issuance by all participants equate to 775 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 267 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (4664) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 793 CONTRACTS ) minus the number of notices served upon today 775 x 100 oz per contract equals 468200 OZ OR 14.5629 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (4664) x 100 oz+ (793) OI for the front month minus the number of notices served upon today (775} x 100 oz} which equals 468,200 oz standing OR 14.5629 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 14.5629 TONNES (A GREAT STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 6327 x 5,000 oz = 31,635,000 oz

to which we add the difference between the open interest for the front month of SEPT(793) and the number of notices served upon today 23 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT./2022 contract month: 6,327 (notices served so far) x 5000 oz + OI for front month of SEPT (793) – number of notices served upon today (23) x 5000 oz of silver standing for the SEPT contract month equates 32,430,000 oz. .

We have an inventory of 45.903 million oz of registered silver at the comex so Sept delivery of 32.430 MILLION OZ represents 70.64% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

GLD INVENTORY: 962.88 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

CLOSING INVENTORY 465.899 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: ECB Inflation Fight Bad News For The Fed

The European Central Bank (ECB) raised interest rates another 75 basis points last week. In his podcast, Peter Schiff explained how the ECB inflation fight could create big problems for the Federal Reserve and the US dollar.

The 75-basis point rate hike was a huge ECB standards, but it’s still basically spitting into the ocean when it comes to battling eurozone inflation. European inflation is worse than US inflation. The official CPI came in at a record 9.1% in August. This rate hike brings the eurozone interest rate to 1.25%. Given that it was below zero at the beginning of the year, the ECB is taking a pretty aggressive stance. But even with the hiking, the real interest rate is still -7.85%. That’s not going to slay 9.1% inflation.

Euro weakness has contributed to the high eurozone CPI. The euro traded below parity with the dollar for a good part of last week until a small rally after the ECB announcement. Peter said euro weakness is also one of the reasons US inflation isn’t even higher.

While the eurozone has had to deal with the problem of a weak euro making their inflation stronger, America has had the benefit of a strong dollar making our inflation weaker. So, as bad as our inflation has been, think about how much worse it would have been had the dollar been weak as opposed to strong — at least relative to other currencies.”

Peter said he thinks the tone of the ECB press conference was more significant than the rate hike that was bigger than expected. ECB president Christine Lagarde made it clear she is now firmly in the inflation-fighting camp.

Her rhetoric is very similar to Jerome Powell’s rhetoric in how committed the ECB is to fighting inflation and bringing inflation back down to its 2% target.”

This 2% target represents a subtle but significant shift in ECB policy. Under Mario Draghi, the ECB emphasized a policy of getting inflation close to but always below 2%.

Now, of course, that whole policy made no sense, and nobody questioned it. I never heard a single person at a press conference talk about how ridiculous such a policy was and ask Mario Draghi to explain it. After all, why is 1.9% inflation great, but 2% is a disaster, and so is 1.8? What is the magical number that makes 1.9 the sweet spot? Or is it 1.99? Maybe 1.9 is still too low because you can still get closer to 2% without touching it.”

Peter said this “nonsensical” policy was all about trying to come up with an excuse to continue with an easy money policy to protect eurozone politicians from facing reality and cut government spending.

[The ECB] was trying to bail out European politicians by allowing them to deficit spend, to continue to buy votes with borrowed money, and to make it work, the ECB had to keep borrowed money super-cheap. So, they came up with this ridiculous theory that because inflation was still not quite close enough to 2%, they needed negative interest rates. They needed quantitative easing.”

Two percent was originally conceived of as a ceiling. The original idea was to keep inflation below 2%, not get as close to 2% as possible. As Peter pointed out, getting close to 2% makes no sense. Why is 1% inflation a problem? Nevertheless, when eurozone CPI was running at 1.5%, Draghi insisted it wasn’t enough.

Now, the ECB is faced with an even bigger problem. It has to move the inflation needle down from over 9% back down to 2%.

If it was so difficult to get it up to two from just below, imagine how much more difficult it’s going to be to get it all the way back down from nine-and-a-half to two. And what type of political pain are Europeans going to have to endure as a consequence of this?”

We’re about to find out how much pain Europeans are going to have to do because Lagarde is saying the ECB is going to bring it down come hell or high water.

As Peter noted, the most recent rate hike doesn’t do much to bring the ECB closer to that 2% goal. Lagarde even admitted that the current rate remains accommodative.

If inflation is the problem, and you’re committed to solving it, why are you deliberately making it worse? If you know you have a stimulative monetary policy in the face of much too high inflation … why do you continue to fuel the fire? If Lagarde was really serious about fighting inflation, she would have raised interest rates a lot more than 75 basis points.”

Why would you not raise rates to the level you think they need to be if inflation is really the threat that’s being conveyed?

The reason they’re not doing that is because they can’t do that, which is basically an admission that they can’t really fight inflation either. All they can do is pretend that they’re going to fight inflation.”

In fact, they are in a position very similar to the one the Federal Reserve finds itself in.

Peter said Lagarde seems to be sending a message to eurozone politicians that they had better get their house in order because they can no longer count on the central bank to bail them out.

Keep in mind, unlike the Fed, the ECB is a single mandate bank. Its sole function is price stability. With inflation over 9%, it doesn’t have any wiggle room, regardless of the economic or market pain.

Peter said this could be a “game-changer” for the markets. Up until last week, the Fed was the only of the three major central banks pretending to fight inflation. Now, Japan is the only one still churning out easy money. Japanese inflation remains a bit below that of Europe and the US, giving policymakers there a little time before they have to pivot.

The ECB pivot could have a major impact on the dollar, and Peter said he thinks the euro has seen its lows relative to the greenback. Legarde even conceded that the weak euro was contributing to the inflation problem. That would imply policy going forward will be to strengthen the euro.

If the ECB is really committed to a strong euro to fight inflation, that is a big problem for the United States, which is now going to have to deal with a weaker dollar, which is going to complicate its efforts to fight inflation…

The Fed’s efforts to fight inflation were being helped by the strength of the dollar. But, if now the dollar is going to turn, and it’s going to weaken instead of strengthening, that is going to put upward pressure on US inflation at the same time that it puts some downward pressure on eurozone inflation. And now, the Fed is going to have to fight even harder and the markets are not prepared for that outcome at all.”

In this podcast, Peter also talks about Jerome Powell’s admission that the US is on an unsustainable fiscal path, the fact that the Fed is an enemy of the people, how the UK government will make the energy problem worse, and the lack of new money flowing into crypto.

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

GOLD/SILVER

END

3.Chris Powell of GATA provides to us very important physical commentaries

4. OTHER GOLD/SILVER COMMENTARIES

The US Mint Is Selling Gold For 50% Higher Than The Spot Price

NEWS PROVIDED BY

American Bullion, Inc.

September 13, 2022, 16:59 GMT

American Bullion shares insights about the reasons of various precious metals products’ price differences compared to their “Spot” prices

LOS ANGELES, CA, UNITED STATES, September 13, 2022 /EINPresswire.com/ — First of all, what does “spot price” even mean?

Spot prices are most frequently referenced in relation to the price of commodity futures contracts, such as contracts for oil, wheat, or gold, but not the tangible products of gold and silver, such as coins or bars.

When it comes to physical gold, any type of raw bullion needs to be mined and refined, which incurs cost. The greater the purity, the greater the refining cost. And then, the gold bullion needs to be minted into bars or coins (which incurs additional expense, but can also reduce or eliminate the need for assaying at the time of sale). Finally, the finished products then need to be distributed through the supply chain to wholesalers, then retailers and ultimately to the buyers. Remember to add the costs of storage, shipments and insurance during this journey which adds up to the ultimate price tag.

Here’s an example of product cost above spot price. With the day’s spot price listed as $1,705, the United States Mint Website is advertising new uncirculated one-ounce Gold American Eagle coins for sale for $2,570.00 ea. directly to retail buyers.

Besides the beauty of its design, trustworthiness and popularity, American Eagles are also highly preferred for other reasons, such as being a very discreet asset. According to ICTA (Industry Council of Tangible Assets), most products are subject to be reported by IRS Form 1099-B when selling back to dealers over a certain qty/weight. But American Eagle products are not on that list.

Market pricing can be somewhat volatile daily, but is predicated greatly by the market conditions of supply and demand.

This is also a good reason to speak with an experienced precious metals dealer, like American Bullion, who is also a US Mint Listed Dealer. There are a lot of considerations when selecting strategies, as to which metals and type of products are to be held. Additionally, those strategy options can diversify even further, depending on whether they are held in personal possession, or by way of a Gold IRA.

John Reese

American Bullion, Inc.

-END-

.

end

5.OTHER COMMODITIES: RICE

end

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.9609

OFFSHORE YUAN: 6.9752

SHANGHAI CLOSED: DOWN 26.25 PTS OR .80%

HANG SENG CLOSED DOWN 479.76 PTS OR 2.48%

2. Nikkei closed DOWN 796.01 PTS OR 2.48%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 109.30/Euro RISES TO 0.9995

3b Japan 10 YR bond yield: FALLS TO. +.249/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 143.31/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.762%/Italian 10 Yr bond yield RISES to 4.07% /SPAIN 10 YR BOND YIELD RISES TO 2.91%…

3i Greek 10 year bond yield FALLS TO 4.29//

3j Gold at $1730.30 silver at: 19.90 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 21/100 roubles/dollar; ROUBLE AT 59.69//

3m oil into the 87 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 143.31DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9612–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9608well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.457 UP 3 BASIS PTS

USA 30 YR BOND YIELD: 3.529 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,25

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

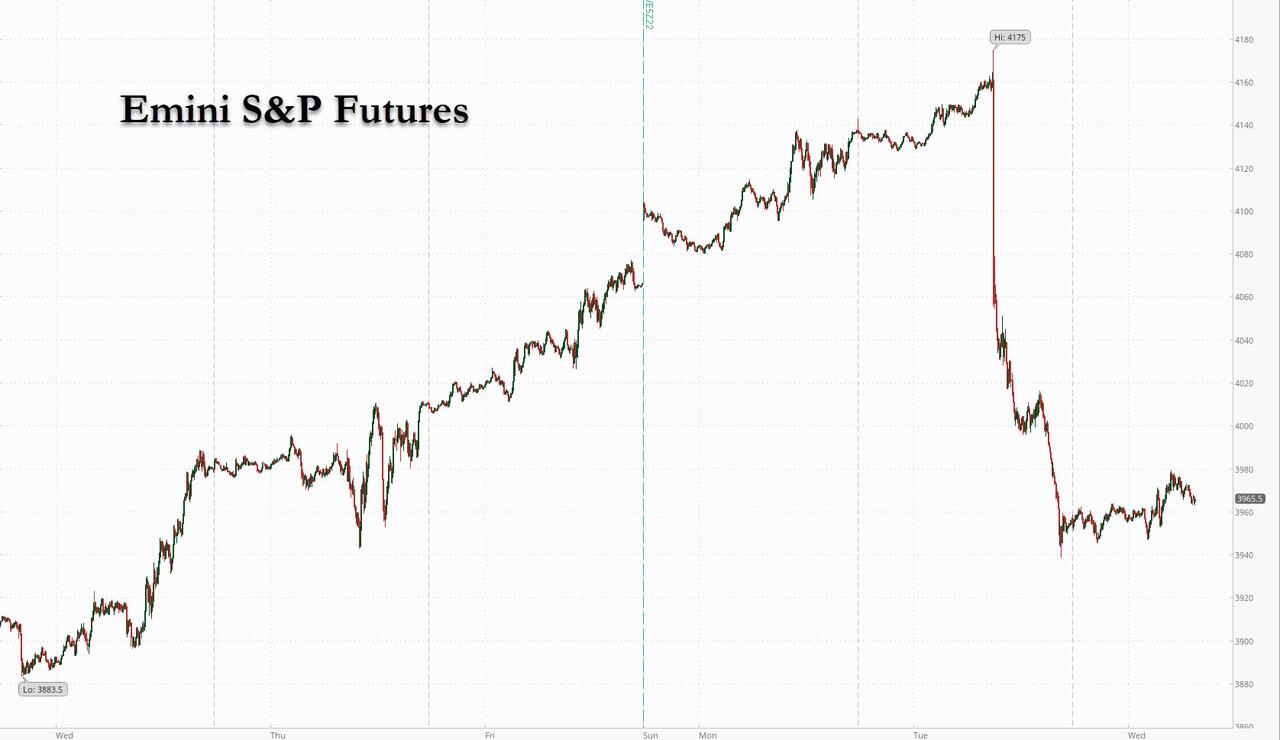

Futures Try To Rebound From Biggest Market Rout In Over Two Years

WEDNESDAY, SEP 14, 2022 – 07:54 AM

US equity futures are trying to rebound after their biggest plunge in more than two years, when the hotter than expected CPI print wiped out 4.3% or $1.5 trillion in market value from the S&P, and are up a modest 0.2% at 730am ET, erasing most of an earlier gain of 0.6%. Nasdaq 100 futures rose 0.7% after the tech-heavy gauge tumbled 5.5% in its worst day since March 2020. Ahead of today’s PPI print, the Bloomberg dollar index retreated after jumping the most in three months on Tuesday, while 10-year Treasurys ticked higher, hovering near a decade-peak. Oil was flat now that the traders consider $80 as a “Biden Bottom.”

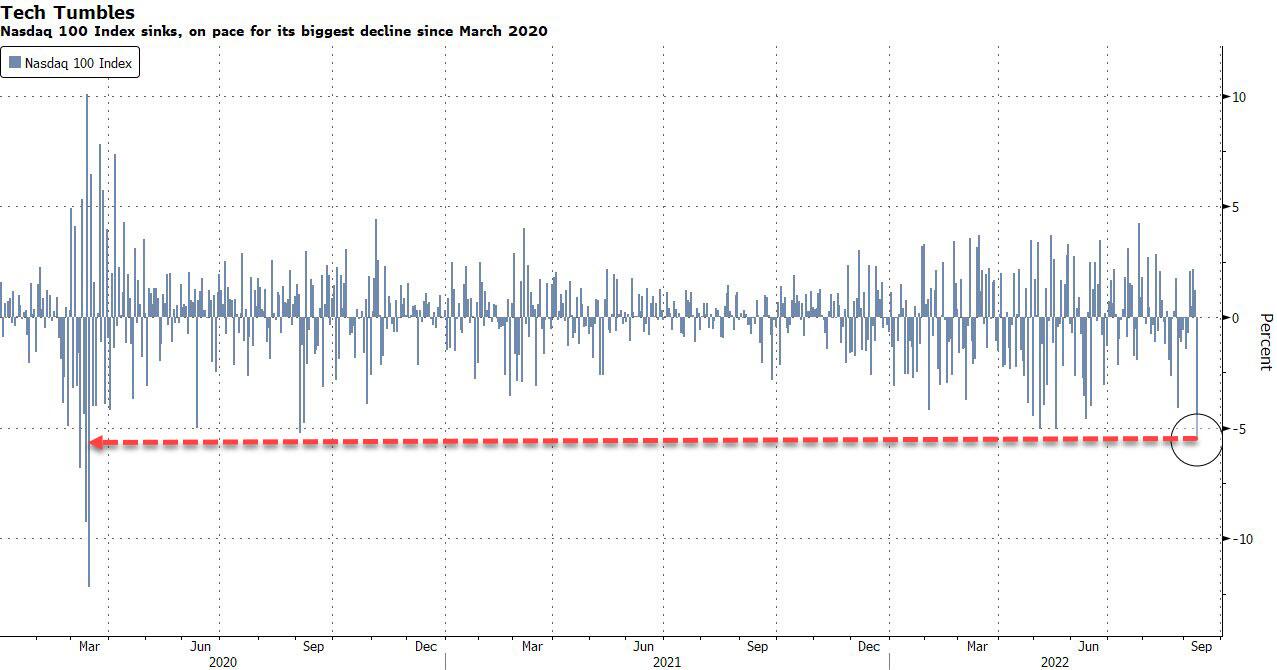

In premarket trading, heavyweight tech stocks posted modest gains a day after the Nasdaq 100 Index saw its biggest decline since March 2020. Apple (AAPL US) +1%, Microsoft (MSFT US) +2%. Other notable movers:

Starbucks (SBUX US) shares rise 2.3% in premarket trading after the coffee giant raised its three-year outlook for profit and sales at an annual presentation to investors. Analysts were mostly positive on the upgrades, with Jefferies finding the new three-year targets achievable.

Oracle (ORCL US) was initiated as hold at Berenberg as the broker sees balanced opportunities and risks for the software firm, while not expecting a major re-rating over the medium term.

“The equity rally over the past week was based more on sentiment than a material change in the underlying economic drivers,” UBS Global Wealth Management strategists led by Mark Haefele wrote in a note. “Tuesday’s selloff is a reminder that a sustained rally is likely to require clear evidence that inflation is on a downward trend.”

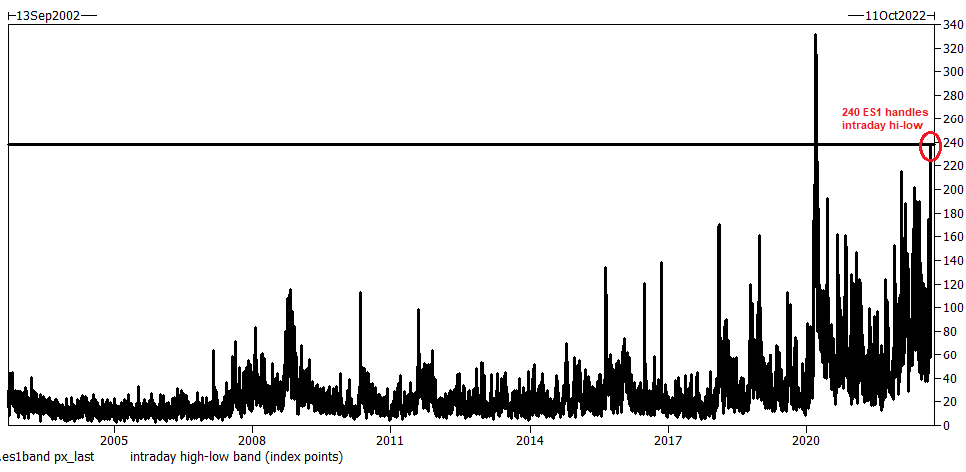

While the magnitude of Tuesday’s drop was indeed historic, and the intraday swing in spoos was one of the top 5 on record…

… the S&P 500 only reversed gains made in the previous four sessions that had been fueled by expectations of a softer reading on the US consumer price index. Investors have been waiting for any sign of peak inflation to come back to the equity market, while the previously discussed lack of a spike in the VIX shows that Tuesday’s selloff was more a recalibration of expectations than panic selling.

“Heading into the August CPI print, a number of traders thought they had information, and positioned very aggressively in the cash equity and derivatives markets,” said Christopher Harvey, head of equity strategy at Wells Fargo. “It turns out they did not have any real information on CPI (only a hunch based upon recent trends), and now they do not have as much AUM.”

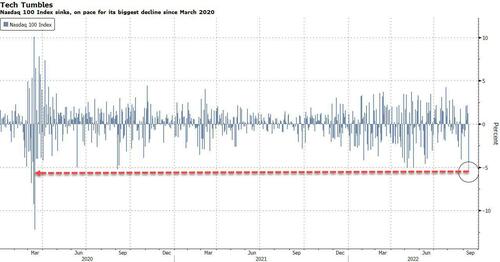

The selling on Tuesday was most acute in the more speculative corners of the market that are particularly sensitive to higher interest rates. Technology falls into this category because the stock prices are based on expected future earnings, which are devalued when interest rates rise. Every single stock on the Nasdaq 100 was in the red on Tuesday, with the Index plunging the most since the world nearly ended in March 2020.

Tuesday’s hot CPI data added to concern the Federal Reserve will need to push interest rates much higher to contain price pressures, with many now expecting a 4.50%-4.75% terminal rate (and in the case of Nomura, a 100bps rate hike) raising the risk of a recession. Now all eyes will be on the Fed decision next week, with swaps traders certain the central bank will raise interest rates three-quarters of a percentage point, and odds of a 100bps hike rising as high as 47% yesterday before easing.

“Multiple compression will continue as long as we have sticky inflation,” said Marija Veitmane, a senior strategist at State Street Global Markets. “Profits will crater. We still see a lot of downside on equities.” She added that central banks need to slow demand and cause pain in the economy to rein in inflation. The longer recession is delayed, the harder it will be, she said, which is true but politicians simply lack to will to enact a massive recession with millions of unemployed workers and is why the Fed will be ordered – soon enough – to reverse.

In Europe, the Stoxx 600 index slipped about 0.4%, though it pared a deeper drop as retailers gained, led by Inditex SA after the owner of the Zara fashion chain reported a jump in profit. Utilities were the among the worst-performing sectors as the European Commission considers plans to contain the energy crisis, which may include revenue caps. FTSE MIB outperforms peers, adding 0.7%, FTSE 100 lags, dropping 0.7%.

Earlier in the session, Asian stocks and bonds tumbled in the wake of the broad-based selloff on Wall Street while the yen strengthened after Japan warned of possible intervention in the currency market. Equity indexes in Japan, Hong Kong and Australia slumped, led by Nikkei which closed down 2.8%. Hang Seng and Shanghai Comp were also negative amid headwinds from an approaching typhoon and with the US reportedly in early talks on sanctions against China to deter it from invading Taiwan.

Japanese equities tumbled the most in three months, following a broad selloff in the US as inflation data fueled expectations for tighter Federal Reserve policy. The Topix fell 2% to close at 1,947.46, while the Nikkei declined 2.8% to 27,818.62. Both gauges slid by the most since June 13. Keyence Corp. contributed the most to the Topix loss, decreasing 5.1%. Out of 2,169 stocks in the index, 172 rose and 1,943 fell, while 54 were unchanged. “The content of the CPI data clearly showed that inflation is quite persistent and it’s difficult to see any clear outlook,” said Hitoshi Asaoka, a strategist at Asset Management One. “Wage inflation was seen in a wide range for the service-related sector and there are no signs that it will slow down.” Inflation Surprise Puts Onus on Fed to Hit Brakes Even Harder Stocks pared losses in late morning trading before retreating again in the afternoon as the yen strengthened about 0.6% against the dollar. The Nikkei reported that the Bank of Japan conducted a so-called rate check in the currency market, a move considered a precursor for intervention.

In Australia, the S&P/ASX 200 index fell 2.6% to close at 6,828.60, the most decline since June 14, as Asian stocks and bonds tumbled in the wake of the broad-based selloff on Wall Street. All sectors declined, with banks and mining shares weighing most. In New Zealand, the S&P/NZX 50 index fell 0.9% to 11,658.04.

In FX, the yen pulled back from a slide toward the key 145 level versus the dollar after a Nikkei report that the Bank of Japan conducted a so-called rate check with traders to see the price of the currency against the greenback. The finance minister warned he wouldn’t rule out any response if curr ent trends continued. The country’s 10-year bond yield rose to 0.25%, the upper end of the central bank’s policy band. The Bloomberg dollar spot index fell 0.2%. NZD and AUD are the weakest performers in G-10 FX, JPY and GBP outperform.

Japan’s currency rose more than 1% to around the 143 level after falling to 144.96 against the dollar early in the Asian session after reports that the Bank of Japan conducted a rate check on forex with market participants, a move that’s seen as a precursor to intervening in the currency market. Benchmark 10- year bond yields rose to the upper end of the central bank’s designated range.

The euro briefly rose above parity against the dollar before paring gains. European bond yields were steady to a few bps higher

Swedish bonds underperformed European peers as markets were increasingly looking for a 100bps Riksbank rate hik next week after inflation rose to a three-decade high

The pound erased an early gain after UK headline inflation missed economist estimates, only to rebound. The UK yield curve steepened as short-dated bonds fell while longer maturities were little changed

UK inflation eased from its highest rate in four decades after petrol declined. The CPI rose 9.9% from a year ago last month, slower than the 10.1% pace in July. Economists expected a reading of 10%

The Australian dollar was steady amid losses in iron ore

“Many emerging markets are feeling the heat of the strong US dollar,” said Chi Lo, senior market strategist for Asia Pacific at BNP Paribas Asset Management, citing their debt burdens in greenbacks. “Only China can afford to defy this global rate-rise trend by keeping its easing policy stance.”

In rates, Treasuries fell across the curve, sending yields 2-3bps higher, and near the bottom of Tuesday’s range, a sharp bear-flattening move following hot August CPI and strong 30-year bond auction. Curve spreads are little changed with 2s10s and 5s30s spreads inverted. US yields cheaper by 2bp-4bp across the curve with 10-year around 3.45%, underperforming bunds by ~1.5bp, gilts by ~2.5bp. The yield on short-end gilts eases about 3bps to 3.14%, while bunds 10-year yield climbs about 1bp to 1.73%.

In commodities, WTI trades within Tuesday’s range, adding 0.3% to near $87.54. Most base metals are in the red; LME nickel falls 1.7%, underperforming peers. LME lead outperforms, adding 0.6%. Spot gold is little changed at $1,704/oz. The IEA cut its 2022 demand growth view by 110k BPD to 2.1mln BPD (prev. 2.21mln BPD); faltering Chinese economy, slowdown in OECD countries undercutting demand.

Bitcoin and Ethereum trade sideways just above 20k and 1.6k respectively, after crashing again on Tuesday.

To the day ahead now, and data releases include the UK CPI reading for August, Euro Area industrial production for July and US PPI for August. From central banks, we’ll hear from the ECB’s Villeroy. And in politics, European Commission President Von der Leyen will deliver her State of the Union address.

Market Snapshot

S&P 500 futures up 0.6% to 3,955.50

MXAP down 1.9% to 152.39

MXAPJ down 2.2% to 500.13

Nikkei down 2.8% to 27,818.62

Topix down 2.0% to 1,947.46

Hang Seng Index down 2.5% to 18,847.10

Shanghai Composite down 0.8% to 3,237.54

Sensex down 0.2% to 60,447.02

Australia S&P/ASX 200 down 2.6% to 6,828.62

Kospi down 1.6% to 2,411.42

STOXX Europe 600 down 0.2% to 420.19

German 10Y yield little changed at 1.72%

Euro up 0.3% to $1.0001

Gold spot up 0.2% to $1,704.99

U.S. Dollar Index down 0.33% to 109.46

Top Overnight News from Bloomberg

Jeffrey Gundlach of DoubleLine Capital is worried the Fed will choke off economic growth by raising interest rates too fast. Former Treasury Secretary Larry Summers is among those saying the central bank needs to hike even faster to restore its credibility

The EU’s executive arm plans to recommend cutting funding for Prime Minister Viktor Orban’s administration on concerns about widespread graft in Hungary, according to senior EU officials

French Finance Minister Bruno Le Maire raised this year’s economic-growth forecast to 2.7% from 2.5% as consumption and corporate investment hold up, and job creation remains dynamic

France’s power-grid operator expects to ask households, businesses and local governments to reduce energy consumption several times over the next six months, to avoid rotating power cuts as the country grapples with a regional energy crisis

A more detailed look at global markets courtesy of Newsquawk

Asian stocks declined following the bloodbath on Wall St where the S&P 500 had its worst day since June 2020, the DJIA slumped by nearly 1,300 points, while the Nasdaq 100 led the declines with all constituents in the red after hot US inflation data spurred more hawkish Fed rate pricing. ASX 200 was pressured with losses in all sectors and underperformance in real estate after ASIC moved to stop investment in two major property funds. Nikkei 225 fell below 28k amid notable losses in the tech industry and with stronger than expected Machinery Orders doing little to inspire a turnaround. Hang Seng and Shanghai Comp were also negative amid headwinds from an approaching typhoon and with the US reportedly in early talks on sanctions against China to deter it from invading Taiwan.

Top Asian News

PBoC set USD/CNY mid-point at 6.9116 vs exp. 6.9003 (prev. 6.8928).

US congressional panel was told by experts that the US ban on sales by Nvidia to Chinese clients will slow Beijing’s efforts to build a facial recognition surveillance network and further restrictions on high-tech product sales should be imposed, according to SCMP.

Hong Kong is to tighten rules regarding issuing provisional vaccine passes to travellers, according to SCMP.

Japanese Finance Minister Suzuki said FX intervention is among the options and FX moves are apparently rapid, while he added they are very concerned about sharp yen weakening and will take necessary steps if such moves persist.

BoJ reportedly conducted a rate check on FX in apparent preparation for currency intervention, according to Nikkei. JiJi suggested the rate check was conducted with USD/JPY at 144.90. Note, officials have since refrained from confirming the rate check.

Japanese Finance Minister Suzuki said recent JPY moves have been quite sharp; reiterates will not rule out any options when asked about intervention, via Reuters.

Indian Trade Body executive said that the State Bank of India is ready for INR trade with Russia; Indian trade body executive expects exports from the country to pick up in October.

Indian trade body executive sees a singing of India-UK Free Trade Agreement by the end of October; India-Australia trade pact likely by November.

European bourses trade mostly lower but off worst levels, but the sentiment remains dampened. European sectors are mostly lower with no overarching theme. Stateside, US equity futures consolidated overnight after yesterday’s detrimental losses, with a relatively broad-based gains performance seen across the main futures contract in the early European hours

Top European News

Queen’s Coffin to Lie in State as Mourners Face 30-Hour Wait

EU Aims to Boost Ukraine’s Economy With Single Market Access

EU Starts Talks With Norway to Try to Cut the Price of Gas

Auto Trader Downgraded by Morgan Stanley; Schibsted Raised

Russia Earns Less Despite Higher Oil Flows in August, IEA Says

FX

The JPY is in focus and stands as the outperformer amid overnight reports of a rate check conducted by the BoJ, whilst verbal intervention continued from Japanese officials.

DXY is subsequently pressured but holds onto a 109.00 handle whilst EUR/USD trades on either side of parity

The Pound bounced firmly in spite of softer than expected UK inflation data, albeit after an initial decline and following very heavy losses on Tuesday.

Fixed Income

Bunds are regaining a firmer grasp of the 143.00 handle between 143.76-142.83 parameters following a strong 2044 auction.

Gilts and the 10 year T-note have also bounced from deeper intraday lows in consolidative trade.

Commodities

WTI and Brent are relatively contained after the front month futures settled lower yesterday.

US Private Inventory Data (bbls): Crude +6.0mln (exp. +0.8mln), Cushing +0.1mln, Gasoline -3.2mln (exp. -0.9mln), Distillates +1.8mln (exp. +0.6mln).

IEA OMR: Cut its 2022 demand growth view by 110k BPD to 2.1mln BPD (prev. 2.21mln BPD); faltering Chinese economy, slowdown in OECD countries undercutting demand

Spot gold holds onto the USD 1,700/oz mark after dipping to a USD 1,696.10/oz low yesterday, with upside levels including the10, 21, and 50 DMAs

Base metals are relatively flat awaiting the next catalyst.

US Event Calendar

07:00: Sept. MBA Mortgage Applications -1.2%, prior -0.8%

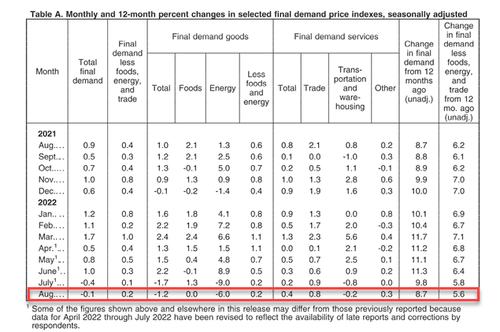

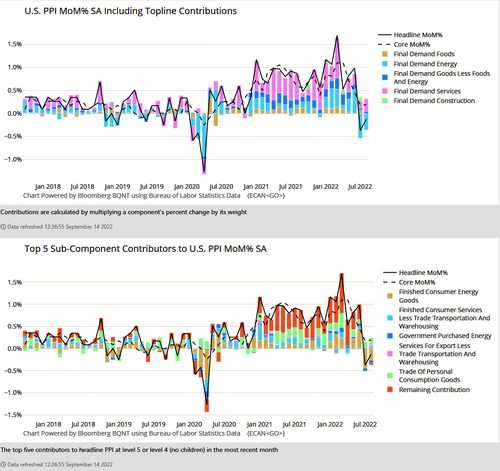

08:30: Aug. PPI Final Demand MoM, est. -0.1%, prior -0.5%; YoY, est. 8.8%, prior 9.8%

08:30: Aug. PPI Ex Food and Energy MoM, est. 0.3%, prior 0.2%; YoY, est. 7.0%, prior 7.6%

08:30: Aug. PPI Ex Food, Energy, Trade MoM, est. 0.2%, prior 0.2%; YoY, est. 5.5%, prior 5.8%

DB’s Jim Reid concludes the overnight wrap

After a recent run of optimism that the US economy might achieve a soft landing, and that upsides on inflation were now behind us, yesterday saw that narrative take a significant blow on the back of another stronger-than-expected CPI release. Both the monthly headline and core CPI prints surprised on the upside, which in turn led investors to ratchet up the amount of rate hikes they’re pricing in for the coming months. Indeed, futures are not only pricing in another 75bps hike from the Fed next week, but they are now pricing in a meaningful probability of a 100bp hike, while also viewing the prospect of a fourth consecutive 75bps move in November as an increasingly likely outcome.

The material tightening of policy expectations sucked the life out of equities, making it one of the worst single-day performances since the onset of the pandemic with the S&P 500 (-4.32%) and the NASDAQ (-5.16%) each having their worst day since June 2020.

In terms of the details of that CPI print, the monthly headline number was actually pretty subdued again at +0.1%. However, that was two-tenths above the -0.1% reading that had been anticipated by the consensus, and meant that the year-on-year measure only drifted down to +8.3% (vs. +8.1% expected). Furthermore, the bulk of that downward pressure came from energy once again (-5.0% on the month), and if you look at the core CPI measure that excludes the volatile food and energy components, that was still rising at +0.6% on the month (vs. +0.3% expected), which is well above rates consistent with the Fed’s target. In fact on a year-on-year basis, core CPI rose to its fastest pace since March at +6.3% (vs. +6.1% expected).

Looking at some alternative measures, the details of the report are even less flattering than the headline +0.1% number. For instance, the Cleveland Fed’s trimmed mean (which excludes the biggest price outliers in the consumer basket) saw a +0.6% gain on the month, which shows that inflation is still broad-based, and that the headline number is being dragged down by outliers. On top of that, the “stickier” components of the consumer price basket were the ones seeing the more rapid increases, with the Atlanta Fed’s Sticky CPI series gaining +0.6% on the month, which contrasts with the -0.9% decline in the Flexible CPI series. So ultimately there was a sense following the report that many market participants may have got ahead of themselves after the previous month’s downside inflation surprise, which after all was the biggest downside surprise relative to consensus in over five years. As I outlined in my CoTD yesterday (link here) that came out before the data, it’s easy to conclude that inflation has peaked due to a collapse in many supply side factors of late but the problem is that we think most of the inflation is now demand led and until the lagged effect of Fed hikes bites inflation will be sticky. The good news about demand side inflation is that the Fed have a fair amount of power over it. The bad news is that it might require notably higher interest rates still. If you’re not on the Chart of the Day (CoTD) and want to be, please email jim-reid.thematicresearch@db.com.

Given the latest inflation data, investors moved to price in a much more aggressive pace of rate hikes from the Fed over the coming months, with a number of new milestones reached. First, investors are now fully pricing in a 75bps move at next week’s meeting, with a non-negligible chance (c.34%) of 100bps as well. Second, a 75bps hike is now seen as more likely than not for the November meeting too. And third, the implied rate by the December meeting now exceeds 4% for the first time, which is a far cry from the 0.82% rate expected when 2022 began. Markets are also expecting a more hawkish Fed into 2023 as well, with the December 2023 rate moving up +18.7bps to 3.82%.

Those expectations of a more hawkish Fed led to a major selloff for Treasuries, with the 2yr yield soaring +18.5bps to a post-2007 high of 3.76%, whilst the 10yr yield rose +5.0bps to 3.41%. That was driven by higher real yields, and at one point the 10yr real yield even exceeded 1% in trading, before falling back to close at 0.96%. The entire yield curve flattened given the higher probability of a harder landing, with 2s10s ending the day at -34.8bps and 5s30s falling -15.5bps to finish inverted (-10.3bps) for the first time since the start of the month. In Asia, US 10yr USTs are another +1.2bps higher with 2yrs +0.5bps. It was a similar story on the other side of the Atlantic too, as the CPI report led investors to expect more rate hikes from the ECB as well, with 129bps of further hikes priced in for the remaining two meetings this year up from 118bps at the start of play. In turn, yields on 10yr bunds (+7.5bps), OATs (+6.4bps) and BTPs (+3.3bps) all moved higher.

As previewed at the top, the sharp tightening in rates led to the worst day in a while for US equities.The S&P 500 experienced a rout that saw it shed -4.33% on the day, its worst day since June 2020, where just 5 companies in the entire index moved higher on the day. Tech stocks were particularly impacted, with the NASDAQ down -5.16%, whilst the FANG+ index of megacap tech stocks fell by a massive -6.56% (worse day since September 2020) given its particular sensitivity to raising discount rates. Bear in mind that up until the CPI release, futures had actually been pointing to gains in the US, following which there was a sharp turnaround in the other direction. That was evident in Europe too, where the STOXX 600 swung from an intraday high of +0.64% just before the release before closing -1.55% lower.

In terms of yesterday’s other news, the UK unemployment rate fell to 3.6% in the three months to July (vs. 3.8% expected), marking its lowest rate since 1974. The number of payrolled employees in August was also up by +71k (vs. 60k expected), and growth in average total pay was up +5.5% in the three months to July (vs. 5.4% expected).So cumulatively the data is pointing towards further hikes from the BoE, and the hike priced in for next week’s meeting went up by +2.6bps yesterday to 68.7bps. Gilts underperformed their counterparts elsewhere in Europe, and the 10yr yield rose +9.0bps to a fresh high for the decade at 3.17%.

Elsewhere, Brent crude oil prices rebounded more than +2.5% intraday (to close down -0.88%) following reports that the United States was considering purchasing crude at $80/bbl to rebuild the Strategic Petroleum Reserve. However, that price level had been floated a few months back, and any repurchases will likely take place over the course of a few years, and wouldn’t begin in the near-term. So those headlines probably are not as incrementally important as yesterday’s intraday price action may suggest.

Elsewhere, the ever-looming geopolitical tail risks provided another nugget yesterday, with Reuters reporting the US was in early discussions of considering sanctions against China to deter an invasion of Taiwan, with Taiwan lobbying EU to take similar steps. Early days in this story, but unquestionably a potential flashpoint to keep an eye on. Regular readers will know we think a bi-polar world with sanctions and trade barriers between the two blocks is a reasonable medium-term scenario.

The strong inflation print has also shaken stocks across Asia with the Hang Seng (-2.58%) leading losses followed by the Nikkei (-2.18%), Kospi (-1.68%), the CSI (-1.24%) and the Shanghai Composite (-1.02%).

S&P 500 and NASDAQ 100 futures are trading +0.20% and +0.13% higher respectively. Stoxx futures are down c.-0.75% as the main index closed before the last leg of the US sell-off.

Elsewhere, China extended its currency defense as the People’s Bank of China (PBOC) set the daily reference rate for the yuan at the strongest bias on record at 6.9116 per US dollar, 598 pips stronger than the Bloomberg average estimate. Separately, yields on 10-yr Japanese government bonds (JGB) advanced to 0.25% for the first time since June, touching the upper end of the BOJ’s target range. This story has gone quiet in recent months so it’ll be interesting if the risk of the BoJ YCC policy going starts to bubble again. Indeed, the Japanese yen is hovering close to its 24-year low at 144.43 against the US dollar after the dollar jumped +1.4% on the surprisingly strong US inflation report.

There wasn’t much in the way of other data yesterday, but the German ZEW survey for September came in beneath expectations, with the current situation component falling to -60.5 (vs. -52.1 expected), and the expectations component down to -61.9 (vs. -59.5 expected). That’s the lowest reading for the expectations component since October 2008 at the depths of the financial crisis.

To the day ahead now, and data releases include the UK CPI reading for August, Euro Area industrial production for July and US PPI for August. From central banks, we’ll hear from the ECB’s Villeroy. And in politics, European Commission President Von der Leyen will deliver her State of the Union address.

AND NOW NEWSQUAWK

European bourses trade off lows, JPY in focus, debt in consolidative trade – Newsquawk US Market Open

WEDNESDAY, SEP 14, 2022 – 06:40 AM

European bourses trade mostly lower but off worst levels, but the sentiment remains dampened; US futures are modestly firmer

JPY is in focus and stands as the outperformer amid overnight reports of a rate check conducted by the BoJ; DXY is pressured

Gilts and the 10 year T-note have also bounced from deeper intraday lows in consolidative trade, Germany saw a strong 2044 auction

WTI and Brent are relatively contained, spot gold holds onto 1,700/oz, base metals are flat

Looking ahead, highlights include US PPI, New Zealand GDP, ECB’s Lane and Villeroy

For the full report and more content like this check out Newsquawk

Try a 14-day trial with Newsquawk and hear breaking trading news as it happens.

The European Union is expected to reconsider its sanctions policy in the fall due to cold weather in Western Europe, Hungarian Foreign Ministry State Secretary Menczer said, according to UrduPoint News/Sputnik.

EU Commission President Von Der Leyen said the energy market is being manipulated by Russia and is not functioning any more.

CHINA-TAIWAN

Taiwan was reported to host dozens of lawmakers in Washington to gather support for measures to deter China and visiting lawmakers are set to pledge support in their home countries for sanctions as a deterrent against China’s hostility, according to Reuters.

ARMENIA-AZERBAIJAN

Armenia’s Defence ministry said Azerbaijan resumed shelling Armenian territory on Wednesday, according to Tass.

EUROPEAN TRADE

EQUITIES

European bourses trade mostly lower but off worst levels, but the sentiment remains dampened.

European sectors are mostly lower with no overarching theme.

Stateside, US equity futures consolidated overnight after yesterday’s detrimental losses, with a relatively broad-based gains performance seen across the main futures contract in the early European hours

The JPY is in focus and stands as the outperformer amid overnight reports of a rate check conducted by the BoJ, whilst verbal intervention continued from Japanese officials.

DXY is subsequently pressured but holds onto a 109.00 handle whilst EUR/USD trades on either side of parity

The Pound bounced firmly in spite of softer than expected UK inflation data, albeit after an initial decline and following very heavy losses on Tuesday.

WTI and Brent are relatively contained after the front month futures settled lower yesterday.

US Private Inventory Data (bbls): Crude +6.0mln (exp. +0.8mln), Cushing +0.1mln, Gasoline -3.2mln (exp. -0.9mln), Distillates +1.8mln (exp. +0.6mln).

IEA OMR: Cut its 2022 demand growth view by 110k BPD to 2.1mln BPD (prev. 2.21mln BPD); faltering Chinese economy, slowdown in OECD countries undercutting demand

Spot gold holds onto the USD 1,700/oz mark after dipping to a USD 1,696.10/oz low yesterday, with upside levels including the10, 21, and 50 DMAs

Base metals are relatively flat awaiting the next catalyst.

Bitcoin and Ethereum trade sideways just above 20k and 1.6k respectively.

NOTABLE EUROPEAN DATA

UK CPI YY (Aug) 9.9% vs. Exp. 10.2% (Prev. 10.1%)

UK CPI MM (Aug) 0.5% vs. Exp. 0.6% (Prev. 0.6%)

UK Core CPI YY (Aug) 6.3% vs. Exp. 6.3% (Prev. 6.2%)

UK Core CPI MM (Aug) 0.8% vs. Exp. 0.8% (Prev. 0.3%)

EU Industrial Production MM (Jul) -2.3% vs. Exp. -1.0% (Prev. 0.7%, Rev. 1.1%)

EU Industrial Production YY (Jul) -2.4% vs. Exp. 0.4% (Prev. 2.4%, Rev. 2.2%)

NOTABLE US HEADLINES

Microsoft (MSFT) sees FY23 Q1 more personal computing segment rev. USD 13.1bln-13.5bln, Q1 intelligent cloud rev. of USD 20.2bln-20.5bln Y/Y and said Q1 devices revenue should be in the low single digits.

Apple (AAPL) is to use TSMC (2330 TT/TSM) next 3 nm chip tech in iPhones and Macs next year, according to Nikkei.

APAC TRADE

APAC stocks declined following the bloodbath on Wall St where the S&P 500 had its worst day since June 2020, the DJIA slumped by nearly 1,300 points, while the Nasdaq 100 led the declines with all constituents in the red after hot US inflation data spurred more hawkish Fed rate pricing.

ASX 200 was pressured with losses in all sectors and underperformance in real estate after ASIC moved to stop investment in two major property funds.

Nikkei 225 fell below 28k amid notable losses in the tech industry and with stronger than expected Machinery Orders doing little to inspire a turnaround.

Hang Seng and Shanghai Comp were also negative amid headwinds from an approaching typhoon and with the US reportedly in early talks on sanctions against China to deter it from invading Taiwan.

NOTABLE APAC HEADLINES

PBoC set USD/CNY mid-point at 6.9116 vs exp. 6.9003 (prev. 6.8928).

US congressional panel was told by experts that the US ban on sales by Nvidia to Chinese clients will slow Beijing’s efforts to build a facial recognition surveillance network and further restrictions on high-tech product sales should be imposed, according to SCMP.

Hong Kong is to tighten rules regarding issuing provisional vaccine passes to travellers, according to SCMP.

Japanese Finance Minister Suzuki said FX intervention is among the options and FX moves are apparently rapid, while he added they are very concerned about sharp yen weakening and will take necessary steps if such moves persist.

BoJ reportedly conducted a rate check on FX in apparent preparation for currency intervention, according to Nikkei. JiJi suggested the rate check was conducted with USD/JPY at 144.90. Note, officials have since refrained from confirming the rate check.

Japanese Finance Minister Suzuki said recent JPY moves have been quite sharp; reiterates will not rule out any options when asked about intervention, via Reuters.

Indian Trade Body executive said that the State Bank of India is ready for INR trade with Russia; Indian trade body executive expects exports from the country to pick up in October.

Indian trade body executive sees a singing of India-UK Free Trade Agreement by the end of October; India-Australia trade pact likely by November.

DATA RECAP

Japanese Machinery Orders MM (Jul) 5.3% vs. Exp. -0.8% (Prev. 0.9%)

Japanese Machinery Orders YY (Jul) 12.8% vs. Exp. 6.6% (Prev. 6.5%)

New Zealand Current Account QQ (NZD)(Q2) -5.2B vs. Exp. -4.7B (Prev. -6.1B, Rev. -6.5B)

New Zealand Current Account YY (Q2) -27.8B vs. Exp. -26.6B (Prev. -23.3B)

New Zealand Current Account/GDP (Q2) -7.7% vs. Exp. -7.4% (Prev. -6.5%)

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 26.25 PTS OR .80% //Hang Sang CLOSED DOWN 479.76 PTS OR 2.48% /The Nikkei closed DOWN 796.01 OR 2.78%. //Australia’s all ordinaires CLOSED DOWN 2.51% /Chinese yuan (ONSHORE) closed DOWN AT 6.9609//OFFSHORE CHINESE YUAN DOWN 6.9752// /Oil UP TO 87,19 dollars per barrel for WTI and BRENT AT 92.72 / Stocks in Europe OPENED ALL MIXED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

3 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

Bank of Japan warns of an imminent FX intervention as the USA/Yen approached 145. (now at 142.84)

BOJ Warns Of Imminent FX Intervention: Here’s How Far USDJPY Can Fall… Before Surging Even More

WEDNESDAY, SEP 14, 2022 – 11:25 AM

One of the biggest casualties of yesterday’s CPI shock was the Japanese yen which, after gradually rebounding after last week’s collapse which sent the currency to 24 year lows, plunged as the USDJPY spiked by nearly 300 pips in response to the soaring dollar and expectations of a 100bps rate hike by the Fed.

However, just as the yen appeared set to take out the critical 145 level, the USDJPY dropped shortly after midnight ET, when Japan’s Nikkei reported that the BOJ (which intervenes in the FX market on behalf of the MoF) conducted a FX “rate check” on Wednesday, asking market participants about rates at which it could intervene.

Bloomberg confirmed reporting that the BOJ conducted a rate check in the FX market after top currency official Masato Kanda delivered a verbal warning Wednesday morning: “BOJ called asking for an indicative price at which it could intervene” the Bloomberg source said. The rate check, which is sometimes a precursor for actual intervention, followed Kanda’s statement at 8:30am local time.

Unlike prior heavy if ineffective verbal intervention by the central bank, where various official had warned that they are keeping a close eye on the yen however failing to slow the yen’s collapse, the latest media leak was seen as a move meant to prepare for imminent currency intervention by inquiring about trends in the foreign exchange market.

The verbal intervention worked, and USDJPY was last seen trading around 142.60, a steep from just shy of 145, where it traded earlier this morning.

While rate checks can be a precursor to physical intervention, it’s unlikely such a move would lead to an imminent action as they are likely an extension of verbal intervention, said Akira Moroga, manager of currency products at Aozora Bank in Tokyo. Still the rate check does underscore the authorities’ resolve against the weak yen.

Additionally, Japan’s Jiji reported that the BOJ asked the market situation at 144.90, which implies that BOJ/MOF has 145 in mind as a red line. Credit Agricole FX strategist David Forrester, confirmed as much, writing that a break of 145 by USDJPY would “probably lead to intervention by the Japanese authorities.”

That said, as Goldman notes, whether they actually do an intervention there or not is a separate issue, as they:

need to get a consent from the US,

FX intervention traditionally has been swallowed by the market in a matter of seconds ending up with no impact, especially when fx move is borne out of US fundamentals.

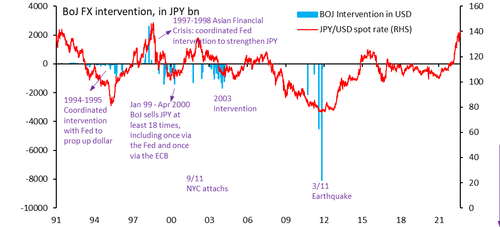

Japan does have large FX reserve (FX currency reserve is $1,172Bn in Aug), but if one intervention doesn’t work, the moment they stop JPY would shoot to the moon. Furthermore as shown in the chart below, BoJ FX interventions have not only failed to halt a sliding yen but have in fact preceded even bigger drops.

Looking further back in time, to the mid-1990s when the BOJ was more aggressively involved in FX intervention (and before the BOJ’s QE), shows a similar pattern: interventions were successful only in the very beginning, and then failed to in driving sustained declines in the USDJPY.

Or, as Goldman puts it, “once they start, it’s difficult to stop.” Of course, nobody wants to be stopped out during the first big move which is why the BOJ will wait until the very last minute before it fires it first and potentially last FX intervention bullet.

Meanwhile, a BOJ adjustment on the YCC would have a impact on the JPY. With the Fed Funds rate heading towards 4%, a 0.1% adjustment on YCC wouldn’t make any impact, and would be again swallowed by the next strong US economic data.

Furthermore, unlike FX intervention, BOJ’s YCC adjustment can only be done once probably. The Japanese domestic economic data still doesn’t warrant a change in YCC.

In any case, the strong warning signal sent by the MOF/BOJ today – whether the rate check at 144.90 was actually done or not – was itself a strong enough message to cool down the market by 1 yen. But put it in another way, US CPI strong print moves the yen by 2 yen, but intervention warning has only half the impact. As such today was a good experiment for the MOF & BOJ (to see just how powerless they are to contain the drop in the yen).

Assuming the BOJ does in fact proceed with an intervention, how far could the USDJPY drop? According to Bloomberg’s FX strategist Vassilis Karamanis, following news of the “rate check”, risk reversals rallied in favor of yen topside this morning across the curve and the Japanese currency is up by 0.6% in the spot market. He notes that whether unilateral intervention can be successful over the medium-term is up for discussion, but “should we see the BOJ buying the yen in size, the dollar could move toward the 137 handle after a round or two of interventions are through. That’s where the 55-DMA and a Double-Top projection coincide. Note that nine-day RSI is sending early bearish signals, and momentum trading could take over should soon. To the topside, 145 remains the key level.”

Seiichi Nozaki, general manager at securities investment department at Fukoku Mutual Life Insurance in Tokyo, said that while Japanese authorities may strengthen the tone of the language if the yen falls beyond 145, any upward yen move would soon be taken over by market players looking to take fresh positions.

“I would put the probability of actual intervention at around 30%,” said Adam Cole, chief currency strategist at RBC Europe in London. “Today’s events may put a temporary cap at 145, but don’t expect that to hold for long” with pair seen rallying to 150.

Looking ahead, if the surge in the yen leads to a burst in inflation, it is likely that the Kishida administration will address the high inflation via Fiscal measures rather (subsidies for gasoline, wheat, and other items, in particular). BOJ head Kuroda, who has been a proponent of a weak yen, has explicitly dismissed rate hikes as an option to counter the weak yen….we would have expected Governor Kuroda to make more cautious comments if he was significantly concerned.

3c CHINA

CHINA/